Performance review 2023

2023 overview

2023 was a in absolute terms quite good, in relative terms however below benchmark. The Value & Opportunity portfolio gained 14,3 % (including dividends, no taxes, AOC fund as of 30.09.2023) against +16,2% for the Benchmark (Eurostoxx50 (25%), Eurostoxx small 200 (25%), DAX (30%), MDAX (20%), all performance indices including Dividends). Links to previous Performance reviews can be found on the Performance Page of the blog.

Some other funds that I follow have performed as follows in 2023:

Partners Fund TGV: 19,6%

Profitlich/Schmidlin: +23,2%

Squad European Convictions +9,9%

Frankfurter Aktienfonds für Stiftungen +7,4%

Squad Aguja Special Situation +4,4%

Paladin One -5,2%

Alphastars Europe +13,7%

The performance of the peers reflects to a large extent the weakness esp. in European/German small caps, especially those outside indices. If you missed out on the few bright spots, you underperformed significantly.

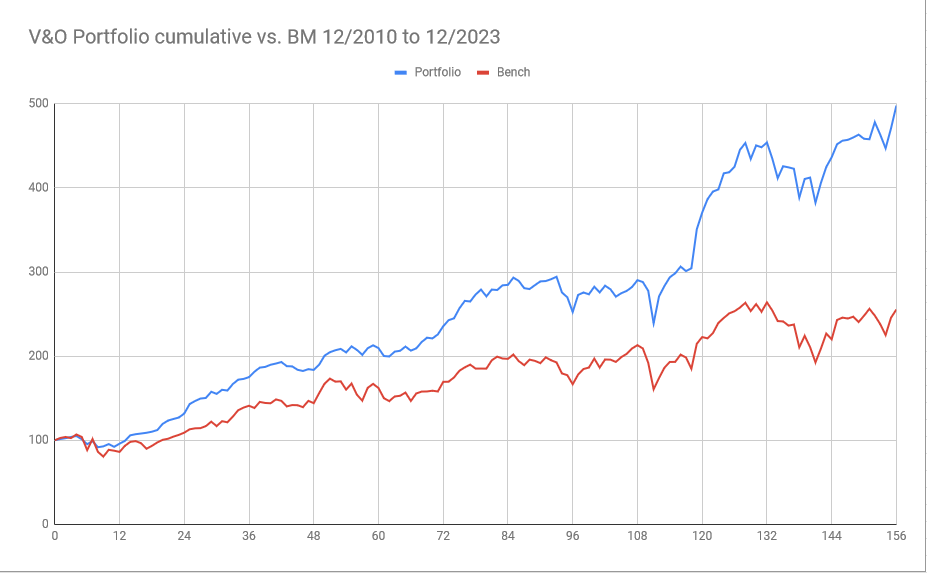

Over the 13 years from 12/31/2010 to 12/31/2023, the portfolio gained +398% against +120% for the Benchmark (before taxes). In CAGR numbers this translates into 13,2% p.a. for the portfolio vs. 6,2% p.a. for the Benchmark. The portfolio ended 2023 also with a new All-time-high. As a graph this looks as follows:

I have to admit that I am still surprised by the extent of the compounding effect. The ~13% p.a. have now resulted in 5 EUR out of 1 EUR invested back in December 2010. As mentioned before, I expect a lower rate going forward, but over time, compounding is incredibly powerful.

Current portfolio / Portfolio transactions & New positions:

In 2023, portfolio activity was medium busy as already mentioned in the 22 (+1) Investments for 2024 post.

New positions were: SFS Group, Logistec, Energiekontor, Italmobiliare, Laurent Perrier, DEME and SAMSE.

Sold positions: In 2023, I sold Meier Tobler, VEF, Rockwool, Recticel, Schaffner and Nabaltec. Temporary members were Scor and Broedr. Hartman (Special Sit). The current portfolio per 31.12.2023 can be seen as always on the portfolio page.

Some Portfolio statistics

The weighted holding period as of 31.12.2023 has been 4,2 years and is within my target of 3-5 years. The 10 largest positions account for around 52% (56%) of the portfolio, the largest 20 for around 86% (87%). The lower concentration in the top 10 is the result of either selling (Meier Tobler) or getting bought out (Schaffner) two of the largest positions.

“Active share” vs “do nothing”

The “Do nothing” approach, i.e. just letting the Portfolio run from 31.12.2022 and collect dividends would have only resulted in a performance of 8%, so my “active contribution” in 2023 was again quite significant. The main reason for this were some timing decision, e.g. selling Meier Tobler pretty much at the top, new positions (Logistec, DEME), but most importantly, increasing the Schaffner position before the take-over offer to a full position. That increase alone was resposble for a 400 bps “uplift” vs. do nothing.

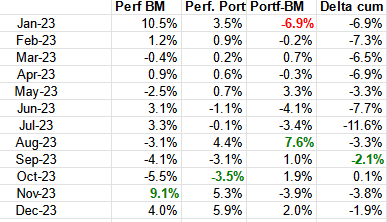

Monthly returns 2023

In relative terms, 2023 started pretty badly, as the portfolio underperformed the benchmark in the crazy January by almost -7%. The relative underperformance increased to almost -12% in July. Only in October, after 3 strong months and with the help of the Schaffner takeover, the portfolio matched the Benchmark:

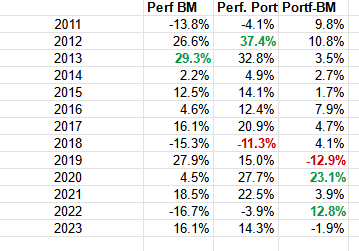

Annual returns 2011-2013

2023 was only the second year in 13 years in which I underperformed the benchmark. This was clearly driven by the significant underperformce of small caps as mentioned above. My benchmark consists out of 50% German/European Large caps, in contrast, my only large cap is ACT with a 5% weight. The second reason is the distribution of returns with very strong returnslat in the year, where my “low beta” portfolio requires time to catch up.

Mistakes made in 2023

As always, I made a lot of mistakes, among them selling Nabaltec a little to early (or too late actually) which created quite a few comments on the blog. In addtion, I clearly entered too early into construction/renovation related stocks like Sto and Solar.

Another mistake was to not move more agressively into out of favor stocks in October. Yes, I bought DEME, but I could have done more. I do hold my ~10% cash position to jump on opportunities like this, but I didn’t. I had a few high quality stocks on my watchlist (Tomra, Righmove), but I did set the limits too low.

In addition, I missed out on a really good year for banking and insurance. I added SCOR in the beginning of the year but got scared when the CEO suddenly resigned. Although I am still somehow sceptical on the fundamentals for many insurers and banks, the narrative “higher interest rates are great for insurers” was pretty obvious and I could have piggybacked on this.

What went well in 2023

Selling Meier Tobler at what I thought was a “full valuation” turned out to be good timing. Also increasing Schaffner when fundamentals improved and the stock did nothing was clearly good. Finally, investing into DEME and the bottom of the cycle for Offshore wind so far turned out to be a decent idea.

Lessons learned 2023

I think the biggest lesson learned (again) was that patience is the key. Even with the significant underperformance over the year, not changing the strategy was importent. If nothing significant changes from the fundamental side, my portfolio usually “recovers” with a time lag of a few months.

In addtion, I think it makes sense to check in into “very out of favor” sectors from time to time to see if there is a sentiment shift happening.

Strategy & Outlook 2024

Last year, I cautioned against Tech stocks and that they maybe won’t rebound quickly. That was obviously not a good call. So as a lesson, I won’t make any such calls this year. To be honest, I have no clue what 2024 will hold for the stock markets. It could be good, bad or totally uneventful.

For me, in 2024, (Renewable) Energy is still a big topic, as well as “bricks and machines”. Infrastructure is another setor that I find interesting. I guess we haven’t seen the bottom of the cycle especially in Europe, but as stocks usually “look forward” at least 6-12 months, I am optimistic that we could see better performance in these sectors in 2024 (in relative terms). But again, I might be totally wrong. For me the most important part is to focus on “quality companies”. In the long run, they offer adequate returns and let me sleep well. I leave the super cheap stuff to others. With quality, I mean a decent business with decet returns and capable management, preferably with equity stakes.

And of course, I will continue to turn a lot of stones and hopefully will find something valuable here and there, maybe in Belgium 😉

Bonus track:

In order to enjoy the fruits of long term compounding, the most important advice is to “Ride on” whatever happens:

Impressive performance. I really like your approach to investing. Thanks for sharing your thoughts.

Currently I am a resident of Germany and I am looking for a good Germany based brokerage solution.

You have mentioned consors a few times. Do you still use it as your recommended broker?

Consors is Ok, but quite expensive.

My highest respect to your consistency and this Impressive Track record!

What I really value is you reflecting yourself and showing what you have done right and wrong…

Please allow me 2 Short questions:

1) Any Chance you are opening a wikifolio or something similar? I think there would be a lot of potential investors

2) Why do you mainly stick with european small caps?

Regards

Dear Malt,

with regards to your questions:

1) Wikifolio: No, the main problem is that many of the stocks that I own cannot be traded (or only at very unfavorable spreads) via a Wikifolio

2) Because that’s where I think that my main expertise is

mmi

Congrats, outstanding performance! I recently read “French Hidden Champions” interview with the guy from Gay Lussac Gestion. With regard to their investment style I guess they would perfectly fit into your peergroup. Moreover I think their holdings would be a good hunting ground, a lot of boring stocks and also some old acquaintances (G. Perrier, Thermador, Samse, Bouvet,…).

On the topic of machinery, I’m currently working on Eurogroup Laminations. They produce electrical motor cores used in EVs (for motion as well as others like windows, wipers etc.) and industrial purposes (HVAC, pumps, generators). Largest supplier to EV OEMs globally with 50% share, sole supplier to a few of the largest OEMs. Mid-teens EBITDA margins with room to expand and a huge orderbook of EUR6,4bn relative to 2023 revenue of EUR800m. Founding family owns 45% of the shares. Market cap of just EUR650m which is a low-teens P/E multiple.

Thanks for the comment. Sounds interesting, never heard of them before…

Complimenta for your overperformance compared to your benchmark. Over a period of 13 years there must be something fundamental to it, this was no luck.

I took over from you some of my best investiment ideas of the last three years (ACT, Rockwool and DCC), but also my worst (JET). You at least were clever enough to exit it soon enough. Anyway, it was my own fault, because I remember not to be convinced from the very beginning. I have to learn to exit sooner in case I am not fully convinced. Or, even better, to not build the position at all.

In any case I would like to thank you for the sharing of your thoughts and ideas.

Thanks for the comment and sorry for JET….

Yes, JET hurts….

Solid performance. Why do you no longer have Ennismore as a peer?

First, it is a long short fund snd second the link broke to get the price into the sheet and I was to lazy to fix it.

RE: Construction and infrastructure. Check out Per Aarsleff in DK. Cheap and a stock that has provided superb returns for shareholders over the long term.

how about Eiffage – now much cheaper than the other large EU infrastructure companies (vinci, ferrovial, getlink, aena etc)

Thanks, Might be one to look at.