Performance Q2 2015 / YTD

Compared to the first quarter, the second quarter was in relative terms much better than the first quarter. The Benchmark (Eurostoxx50 (25%), Eurostoxx small 200 (25%), DAX (30%),MDAX (20%)) actually lost -5,8% in the second quarter, whereas the portfolio remained almost unchanged with -0,1%. YTD the score is now 13,2% for the benchmark vs. 11,4% for the portfolio.

For me, the second quarter is a good feedback that the portfolio strategy is working. I expect to underperform in a strong bull market like we had in the first quarter, but then to outperform in weak or sideways markets. The monthly returns show clearly that the portfolio is less volatile and only relatively loosely correlated to the benchmarks:

| Start |

Bench |

Portfolio |

Perf BM |

Perf Portf. |

Delta |

| Jan 15 |

9.977,26 |

189,81 |

8,3% |

3,4% |

-4,9% |

| Feb 15 |

10.696,03 |

200,55 |

7,2% |

5,7% |

-1,5% |

| Mrz 15 |

11.078,60 |

204,69 |

3,6% |

2,1% |

-1,5% |

| Apr 15 |

10.847,76 |

206,98 |

-2,1% |

1,1% |

3,2% |

| Mai 15 |

10.871,99 |

208,60 |

0,2% |

0,8% |

0,6% |

| Jun 15 |

10.434,47 |

204,44 |

-4,0% |

-2,0% |

2,0% |

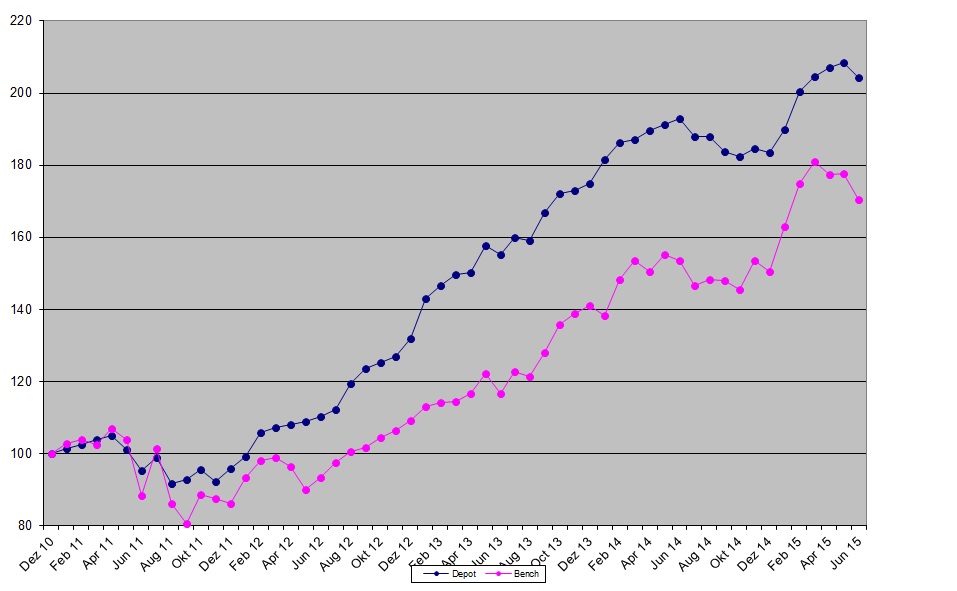

As I have mentioned before, time lags play a role here as well, especially for the lower liquidity small caps. Since inception, the portfolio is up 104,4% vs. 63,2% against the benchmark. Graphically, this looks like this:

Within the quarter, outperformers were Van Lanschot (+24,1%), Citizen’s (+13,1%). Lloyds Banking (+8,9%). Losers (not adjusted for dividend) were G. Perrier (-8,6%), Thermador (-7,9%) and Draeger (-6,9%).

Portfolio and transactions

I am actually quite proud of sticking to my 1 transaction per month goal in the second quarter. Overall I did 3 transactions:

The purchase of Lloyd’s Banking, the BMPS “trade” and finally Gagfah a few days ago.

The current portfolio can be found as always if you click the current portfolio page. Most noteworthy “aggregate” changes is that “opportunity investments” went up from 22% to 28% of the portfolio and “pure cash” went down from 15,5% to around 11%.

Comment: “Great ideas vs. great execution”

One of the most remarkable stories for me in the last 3 months was the following: In April, “Bond King” Bill Gross came out with a call that the 10 Year Bund Future is the short of a life time. A day or so later the Bund Future started to drop significantly and Bill’s call should have played played out wonderfully. But then something strange happened: The value of Bill Gross’ fund actually fell and he had to admit that he did not actually implement a simple short but a more complex strategy which backfired and he actually lost money.

So let’s take a step back and look at what has happened here: The best bond investor of all times has a great idea and even has timing right but fails to implement it in order to profit from it.

So clearly, just having a great idea does not automatically lead to great results. In addition, one has to implement it well. Other examples of bad execution: John Hussman with his market timing strategy who suddenly changed the strategy in 2009 and did not go back into stocks again, or Michael Burry, the guy from “The Big Short” who was right on subprime but who couldn’t convince his investors to keep their money in his fund.

These days I often hear from fellow investors: I don’t have any great ideas at the moment. If you look around in financial media and service providers, very often the focus is on idea generation. The more ideas the better. There is a lot less literature etc. on how to execute ideas.

If you look at Warren Buffett, it is clear that he is the master of implementation and execution. His success in my opinion relies to a large extent on only two factors:

1. Buy and hold

2. Permanent capital / safe leverage

Especially now in his later years, he is not the great genius stock picker anymore that he was in the past but he has structured Berkshire in the way that he still creates a lot of value even by buying “mediocre” assets like wind farms or solar power plants.

So why I am telling this ? In my opinion, just having great ideas is not enough. Implementation is maybe even more important. I would even argue that average ideas and great implementation works better over time than great ideas and mediocre implementation. As a private investor, it is clearly not possible to set up a reinsurance company but on the other hand there are a lot of simple things one can do to better implement ideas:

1. Don’t act (too) emotionally or spontaneous

2. Try to come up with a strategy or “game plan” for each investment, containing among others:

– target holding period

– targets when to buy more or sell down (based on fundamental data, ratios and/or stock prices)

3. Try to come up with a strategy for your portfolio: What do you want to achieve and especially HOW do you want to achieve it ?

4. Make sure the money you invest in risky assets is as permanent as possible. Do have a personal financial plan and buffers to make sure that you are never forced to sell

Since I started the blog, I made many mistakes and bad execution is clearly one of them.

Some good ideas in my blog which I didn’t implement well were for instance:

– Prada short: Too early, not patient enough

– G. Perrrier long: Started with a half position did not manage to increase position

– Sberbank: Did not cope with volatility, sold out at the worst time

– generally selling to early, not recognizing that fundamentals have improved (example Dart Group)

In other cases, good implementation saved me from an otherwise bad idea for instance when I got out of Praktiker bonds pretty early before the real xxxx hit the fan because I had predefined the condition where I would sell.

Just by chance i came across this article which wants to point out how the Apple watch will “revolutionize” investing. The “1 million dollar” quote is this one:

Another key area of focus is cutting the distance or time between investment research and action.

Vaed described the challenge of remembering a stock after reading an article or watching CNN. “But if you have a plug-in available on your browser that lets you act right away, that’s valuable.”

And that’s why E-Trade created such a browser trading tool on Google Chrome, after discovering it was the browser of choice among its clients.

I don’t want to sound arrogant but this is clearly a recipe for very very bad implementation. I actually do think that a longer period of time between research and action is benefitial for almost any investor. . For a value investor I don’t see any benefit of a mobile value investing app or similar bxxxsxxx.

So as a summary my advice would be: Although it doesn’t look as sexy as generating new ideas, the management of existing ideas or the “execution” is at least equally important. Try to take your time and work on this especially in a time right now where new ideas are harder to find. I think now is a good time to build the “foundation” for good execution.