Groundhog day: Another BMPS (ISIN IT0005092165) deeply discounted rights issue “Italian style”

Health warning: Do not try to trade in such situations unless you know exactly what you are doing. This is not investment advise, do your own research.

Almost exactly 1 year ago, I already looked at last year’s deeply discounted rights issue of struggling Italian Bank BMPS. Well, the same time in the year again and of course, BMPS is again in the market…. somehow this reminds me of this great movie:

As readers know, I am strangely fascinated by those “Italian style” capital increases where a company issues a large number of new shares at a huge discount,reulting in very valuable subscription rights and almost worthless shares.

In the current case, BMPS wants to issue 10 new shares for every single old share at a price of 1,17 EUR, a huge discount compared to the last price of around 9 EUR. “Wanting” is maybe the wrong word here, BMPS was actually forced to do so, having the worst result of last year’s European stress test for banks.

Interestingly enough, the effect of last’s years capital raising has literally been “evaporated”. BMPS issued 5 bn EUR new shares back then, but before the new rights issue, the market cap was only 2 bn EUR.

At the time of writing, the stock trades at ~1,78 EUR and the subscription right at 5,57 EUR. Theoretically, the subscription right should be worth (10:1)*(1,78-1,17) =6,10 EUR. So again we do have a theoretical mis-valuation with the subscription right being undervalued but only by around 10% (but the spread is very volatile) vs. the 50% we have seen last year.

The “arbitrage” trade again would be to short shares and buy the rights but as we have seen last time, this resulted in quite a substantial short squeeze during the trading period of the rights. The technical problem with this trade is that despite general problems to short the shares, the available market value is tiny. The market value of the “equity stump” is only around 500 mn or a third of the market value of the rights.

Last year the better strategy was actually to go long the shares during the trading period and betting on the short squeeze as we can see in this chart from 2014:

The big drop in the share price came actually before retail investors got their new shares so buying the rights cheap and exercising into shares was not a good strategy either.

Long term, the 2014 short squeeze looks even more strange if we look at the chart from January 2014 until today (adjusted for the rights):

It is pretty obvious that this time waiting did not help BMPS much.

The banks running the rights issue at least seem to profit nicely, they expect to make 130 mn fees on the transaction according to Bloomberg.

Funnily enough, the Italian regulator Consob warned investors on Friday that shares could be volatile. This is from the Reuters article:

But the highly dilutive nature of the rights issue risks artificially inflating the ex-rights share price during the period when the rights are traded separately, from May 25 to June 8, and before the new shares are actually issued, Consob said on Friday, urging investors to “behave properly” or risk fines.

Monte Paschi tapped shareholders for cash only a year ago, in a 5 billion-euro share sale that was also highly dilutive and led to some disruptions to trading due to the large number of new shares being issued.

Demand could not be met ahead of the delivery of the new shares, pushing the stock price higher during the offer period.

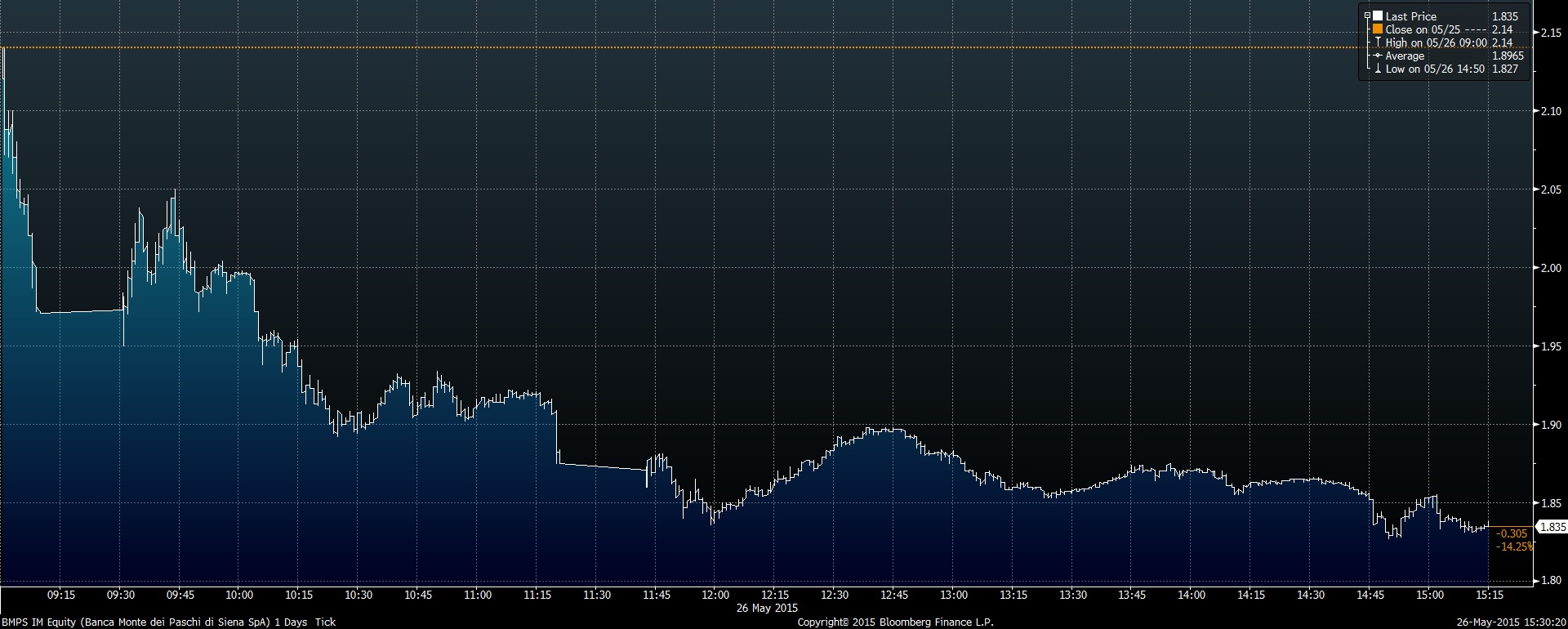

This is quite interesting. There weren’t any fines last year but I assume that someone had orchestrated some kind of short squeeze last time. Already on the first day, BMPS was both, limit-up and limit-down already, the intraday chart looks fun (if you haven’t bought in the first minutes of trading):

For the portfolio I am actually prepared to “speculate” for my “special situation” bucket with a small amount (1% of the portfolio) exactly on that outcome, i.e. that there will be some short-term upwards pressure on the share during the rights trading period. My entry-level is 1,80 EUR, the stock price at the time of writing. I do think that the issuing banks will support the share price at or around this level for the trading period (May 26th to June 8th) and that the shares now include a “cheap option” on something strange happening to the upside over this period.

I am looking for a potential gain of +20%, I will sell if the position goes down more than -10% against my entry-level. I will definitely close out the position before the end of the trading period because I have no intention of becoming a longer time BMPS investor.

Again please remind: This is really risky, don’t speculate here if you do not exactly understand how a typical Italian rights issue works. There is no margin of safety for this single transaction, anything can happen here.

For me this is acceptable because I only invest a small portion of the portfolio, I look at those situations often and over time I expect to make money “on average” on those kind of deals. But any single deal can lead to large unexpected losses. Also, the entertainment factor of those situations compensates me personally already against some losses and I am aware that not everyone looks at this from an entertainment perspective.

Do you use stop loss or just notification and sell manually when the price drops 10%? For me momentum strategies are difficult to follow manually due to loss aversion. Good luck.

#Martin,

I do this “manually”. Loss aversion is not a big issue for me. Also, this is not a momentum trade.

mmi

Hi – interesting read, what is that makes you say that there is no chance you want to hold a long term interest in this bank? surely there must be some other forces behind this ‘oldest’ bank of the world that will stop it from going down the tube?

I don’t think that the “age” of a bank has any corellation with success. The best example is Sal. Openheim in Germany, which went out of business after 220 years.

In general I think Italy is overbanked and within Italy, Intesa and Unicredit are better run than BMPS.

well that’s fair enough – i was just thinking about some belgian banks that had this old capital sitting behind them and they have survived from some rough rides in the last 6-7 years….

At least it closed strong today. Price needs to go up above at least the fair ex price of 1.92 so the options squeeze can start.

Check out http://www.borsaitaliana.it/borsa/derivati/stock-options-landing-page/sottostanti.html?lang=en. 52187 calls vs 13895 puts outstanding. With a multiplier of 1000 that’s 52 million shares that could be pulled. There are around 256 million old shares outstanding.

Unfortunately their site doesn’t show open interest by strike which would be very nice to know.

yes, according to the Consob document, the exercise of call options seemed to have been “the trick” being used in the past….

Check out http://www.consob.it/mainen/legal_framework/consultations/consultation_20140806.pdf

#Joe,

thank you very much. VERY interesting stuff,great !!!

MMI

A similar thing happened when the Spanish bank, Bankia was rescued by the Spanish government. I didn’t know that much about stocks at the time, so I didn’t understand very well what happened at the time. The price (of the old shares) did very weird things in the days when the subscription rights were issued.

It was a 100:1 capital increase I think. It was on all the news because the share price multiplied by the number of the shares after the capital increase implied Bankia was the largest bank in the Eurozone by market cap. Of course the price tanked one day or two before the new shares were issued. Someone made a lot of money there.

You should definitely check it out.