Installux:

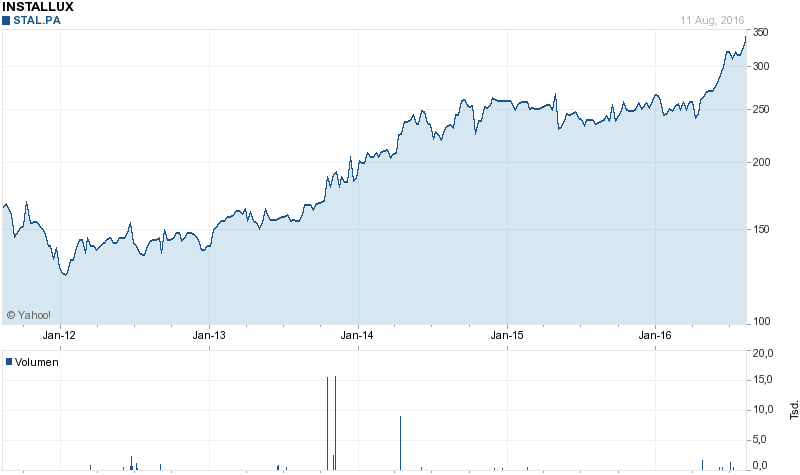

Installux is surprisingly one of my best performing stocks this year, including dividends the stock is more than 30% and is at an all time high.

I did not fully understand why until I read the 6 month report.

Sales are up ~7% yoy, 6M earnings per share are 17,16 EUR vs. 14,37 EUR, an increase of almost 20%. Profit improvements happened across most of their sectors, so it doesn’t look like single special effects or so. Despite the recent run-up, the stock remains exceptionally cheap.

Kuka & MDAX exit

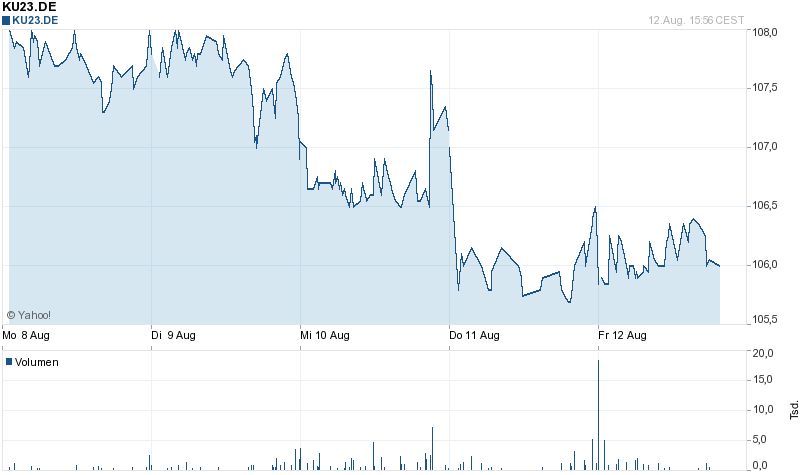

For those who did follow my comments on the original Kuka post, they might have noticed that I sold the stocks 2 days ago and bought them back yesterday slightly cheaper.

The reason was that in the meantime, the tendered shares were kicked out of the MDAX, the popular German MID Cap index.

As I was not sure how the shares would react I decided to manage the risk by staying out.

At the end of the day not much happened:

Nevertheless I was able to cheapen my purchase price from ~107,5 to 106 EUR. As the deal now is more attractive, I invested a total of 4% of the portfolio.

Aixtron – another special situation (with a Chinese buyer)

Aixtron, a former TECDAX star has fallen on hard times. However a few weeks ago, a Chinese buyer showed up and finally made an offer for the company at 6 EUR per share.

With a share price at currently 5,53 EUR, the discount is similar to Kuka at around 8,5%.

The situation differs slightly from Kuka:

- the buyer is a financial buyer, not a strategic one (more opportunistic ?)

- The purchase price is “optically” not as rich as the one for Kuka (below book)

- they require at least 60% acceptance as closing condition (vs. 30% for Kuka)

- within the offer they have a “put” if the index (DAX or TEcDax) goes down more than 30%

On the plus side, there is little risk that anyone complains about the deal as Aixtron was not doing well anyway and they are not deemed “strategically important”. The time horizon here should be shorter than for the Kuka deal.

The offer runs until October 7th. So far, the acceptance is low, as of today, only 1,64% of the shares have been tendered.

I think the risk is slightly higher than in the Kuka case as they might not reach their threshold, on the other hand there might be a chance for a better offer.

Although the situation is less clear for me as in the Kuka case, I start here with a 1% position at 5,53 EUR and will monitor it closely.