SportsDirect (SPD) – Bad PR but maybe good Capital Allocation ?

Already some days ago, I linked to an interesting write up from Wertart on UK retailer SportsDirect.

![]()

In general, I liked a lot of things at SportsDirect from a share holder perspective:

+ It is kind of “Owner operated” with an experienced management

+ Aldi/Lidl like business model (Some brands, own brands, “hard discount”)

+ good growth track record since IPO

+ very good profitability

+ looks cheap based on past performance

Of course there are a couple of issues as well:

- it is retail after all

- Brexit / GBP issues (higher import prices, potential issues with consumer confidence)

- Bad PR (low wages, zero hour contracts, incidents)

- some governance issues (related party dealings etc.)

PR Desaster

I personally think that Mike Ashley and SportsDirect haven’t handled the issue with regards to salaries and incidents etc. well. The parliament hearing was not well prepared and for instance his refusal to speak with trade unions outside the AGM doesn’t look good.

It is no secret that Amazon doesn’t treat its employees very good, but somehow they seem to be better in “spinning” a positive story. And just to be clear: Personally; I don’t think that a company with a discount model needs to treat its employees badly. Aldi for instance clearly requires a lot from its employees but pays clearly above average.

One rarely hears complaints from employees at Aldi about their employer. In contrast, former drugstore king Schlecker was infamous for treating employees badly. I don’t think that it is a coincidence that they went bankrupt a couple of years ago and opponent DM who treats employees fairly is thriving.

I guess the strategy to “squeeze” employees worked a lot better in the early days of the company but today, with the discussions on inequality and especially social media a retailer cannot afford to openly treat his employees so badly.

In the upcoming AGM there will be even a vote for an independent review into the matter. I think Ashley could have avoided this by being more open upfront and actually talk to the unions.

In this post I want to focus however on something else:

Is Mike Ashley / SportsDirect a good capital allocator / Capital manager ?

Just to recap: Capital Allocation is what a company actually does with the money it earns. Capital Management includes also any increase/decrease in external capital.

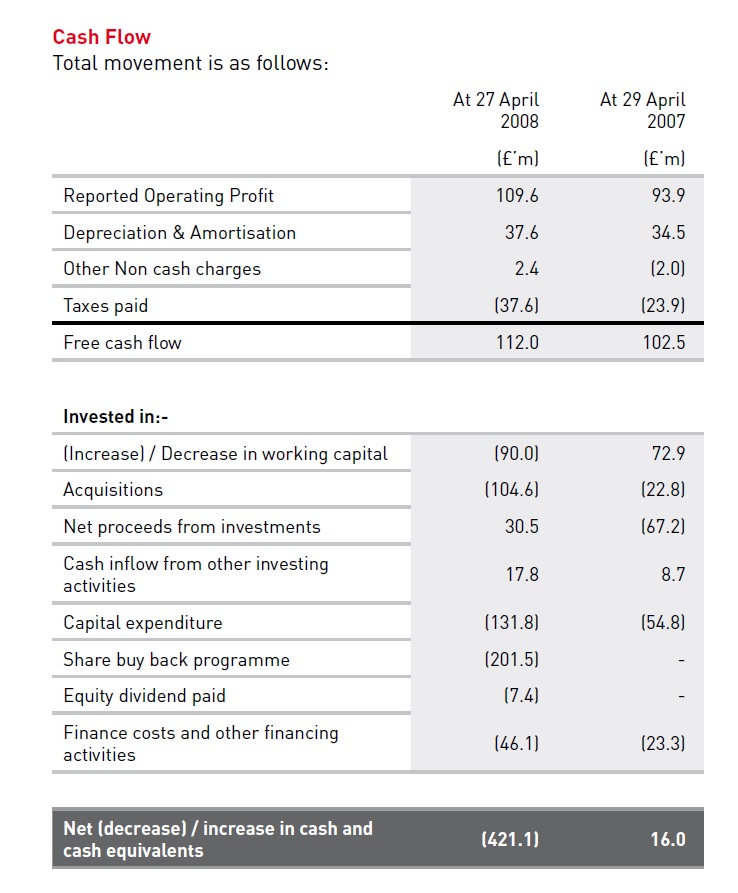

What I do find interesting is that beginning with their first annual report 2008, SportsDirect actually gives a pretty good overview how they allocate and manage capital. This is how they presented it in the 2008 annual report and how they still do it:

This table together with the explanation is very helpful to see how and where they allocate capital. In most other companies one needs to extract this numbers from aggregated CF numbers and notes.

This is my own table where I summarized the capital allocation since 2008:

| OpCF | Portf | WC | Capex | Acqu. | Share bb | Div | Fin | Total | Depr. | Growth Cpx | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2008 | 112,0 | 48,3 | -90,0 | -131,0 | -104,0 | -201,5 | -7,4 | -46,1 | -419,7 | 37,6 | 93,4 |

| 2009 | 125,7 | 28,9 | -31,5 | -34,8 | -6,6 | – | -25,6 | -22,5 | 33,6 | 45,5 | -10,7 |

| 2010 | 85,9 | -8,3 | 80,5 | -18,8 | -3,3 | – | -6,9 | -9,7 | 119,4 | 47,5 | -28,7 |

| 2011 | 173,4 | – | 14,0 | -21,0 | – | – | – | -4,7 | 161,7 | 59,9 | -38,9 |

| 2012 | 192,0 | – | -32,0 | -131,0 | -26,0 | – | – | -5,3 | -2,3 | 58,2 | 72,8 |

| 2013 | 245,0 | 1,0 | -131,0 | -49,8 | -47,0 | -21,7 | – | -6,1 | -9,6 | 54,8 | -5,0 |

| 2014 | 277,5 | -4,6 | -118,0 | -69,0 | -144,0 | – | – | -7,2 | -65,3 | 56,9 | 12,1 |

| 2015 | 301,0 | 4,1 | -64,0 | -79,0 | -3,8 | – | – | -5,9 | 152,4 | 62,4 | 16,6 |

| Total | 1.512,5 | 69,4 | -372,0 | -534,4 | -334,7 | -223,2 | -39,9 | -107,5 | -29,8 | 422,8 | 111,6 |

| In % of OCF | 100% | 5% | -25% | -35% | -22% | -15% | -3% | -7% | -2% | 28% | 7% |

Observations / Interpretations

First of all one can clearly say that SD is actively allocating / managing capital. This shows in their decisions to cancel the dividend after 2010 and to buy back shares only in very selected time periods.

Secondly it is interesting to see that also working capital and Growth Capex are managed actively. They were able to save/generate cash in 2010 and 2011 by reducing inventory and growth Capex. I am a little bit surprised how little growth capex they required considering that sales have increased 150% since 2007.

What I found interesting is that right after their IPO they were aggressively leveraging up, making acquisitions and buying back shares. After that “burst” they basically reduced the leverage more or less completely.

Dividend/Stock Buybacks

They use stock buy backs selectively and only when the stock really went down. Many companies start buying back when the stock is still high.

From the 2011 annual report:

When deliberating on whether to make a dividend payment in respect of the Year, the Board assessed a variety of potential investment opportunities and the Company’s financial performance. Although FY12 results and cash flow performance were ahead of management’s expectations as at December 2011, which means that the balance sheet is stronger than originally expected, there are a number of inorganic growth opportunities under review. This being the case, the Board believes that it is in shareholders’ best interests for the Company to maintain maximum flexibility in the near term and therefore it has decided not to return any cash at this time

Also in the current situation, they waited quite some time until they actually started buying back stocks a few weeks ago.

So in this regard, I would give good marks to SportsDirect. Just paying a dividend because everyone pays a dividend is not good capital management. Paying only selectively however is and buying back stocks when the price is really down is something which is very rarely seen.

Acquisitions:

Let’s look at the biggest ones only. In 2008 they bought Everlast (Boxing Brand) for around 80 mn GBP. This seems to have been a relatively expensive but good acquisition. That’s what they write in 2009 which was a difficult year in general:

The contribution made by Everlast in the year for revenue and profit after taxation amounted to £35.9m and £4.4m respectively

Overall it seems that they were able to grow their brand portfolio consistently and made good capital allocation decisions in that area

From 2011 on, they created a new division called Premium Lifelstyle:

During the year, UK Retail created a Premium Lifestyle division with the acquisition of 100% stakes in USC and Van Mildert and an 80% stake in Cruise clothing. These were for a cash consideration of £7.5m and commitment to a £20m working capital facility.

and 2013:

Premium Lifestyle sales grew 49.4% to £214.1m (FY13: £143.3m), in large part due to the inclusion of a full year’s trading in Republic which was acquired in February 2013. Premium Lifestyle gross margin for the year decreased by 350 basis points to 40.3% (FY13: 43.8%) due to the clearance of old stock in the year

For the time being, Premium Lifestyle does not look like a success. They had to close many stores and sales decreased. Profitability never came close to the core business

In 2014 they did a bunch of European acquisitions

The acquisition of Sport Eybl and Sports Experts AG (EAG), and a controlling interest in Sportland International Group (SIG) alone increased the store portfolio by 135 stores in five countries

Again this doesn’t seem to go well and let already to a 50 mn GBP write-down in the last year.

In 2015 they then diversified into fitness studios:

The Group has acquired 25 former LA Fitness gyms, all of which are located in the UK.

Here the judgement is still open. Overall I would rate the acquisition strategy especially in the last years as “medium” at best. Especially the “diversification” strategies away from UK hard discount seem to be quite difficult.

Incentives structures

Initially. SD’s management had a bonus plan based on EPS growth and Total Shareholder Return (TSR) compared to a peer group of retail companies.

When SD’s stock price slumped, no bonuses were awarded. Then in 2009/2010, they implemented a new plan which only had absolute “underlying” EBITDA targets as performance hurdles. In 2012 they implemented a second EBITDA based plan until 2015. Both plans were fully hit, leading to nice pay offs especially for the CEO who got shares for 6,6 mn GBP awarded in 2015 . Then in 2015 they implemented a new 4 year plan which however was knocked out already in the first year by not reaching the first hurdle.

As I have mentioned before, I don’t think that EBITDA based plans are very useful to align the interest of management and shareholders.

I think this is also one of the reasons for the rather mediocre acquisitions in the last years. If you target EBITDA, then almost any acquisition os EBITDA accretive although it might not create a lot of shareholder value.

On the other hand, the CEO actually forfeited his first stock award from the recent plan as one could read in the 2016 report:

In the FY15 directors’ remuneration report, we reported that all the performance conditions for Dave Forsey’s award over 1m shares granted in August 2011 under the Executive Share Scheme had been met, and the value of those shares was included in the single figure table for FY15. Vesting of those shares was deferred until 2017. On 6 June 2016 the Company and the Committee were informed of the decision of Dave Forsey to forego the vesting of these shares. At the time of the announcement this represented a value of approximately £3.6m. The Committee believe that this is very much reflective of the Executive Directors sharing risk with shareholders and taking responsibility for results that fell short of their expectation.

This is extremely unusual, as Forsey only gets a 150 K salary. This to a certain extent mitigates in my negative opinion the potential adverse effect from a pure EBITDA incentive scheme. Overall I would say the incentives are again medium, not great but not bad either. I would prefer to have some kind of “return on capital” measurement even with an owner/operator at the steering wheel

Stock Portfolio

One of the other specialties of SD is clearly the stock portfolio they run on their balance sheet. This is how they started in 2008:

John David (JD) Group 21 mn GBP

Blacks Leasure Group 21 mN GBP

Adidas 13,2 mn GBP

Amer group 9,7 mn GBP

Of the 2 big positions, JD Sports was a big success, Blacks Leasure Group went bankrupt. If we look at the survivors, interestingly all “survivors” performed better than SportsDirect itself.

So one could argue that maybe Mike Ashley should actually run a Retail stock fund instead of a retail company….

In 2009 he sold Adidas and bought a JJB Sports position, another retailer which would soon become bankrupt.

In 2010, both the Amer and JJB position had been sold. In 2011, no changes were made, in 2012 Blacks went into liquidation and interestingly JD Sports bought most of the stores.

Only in 2014 the began to add a position in Debenhams which they then build up into a 15% position over 2015 via derivatives. Additionally in 2015 they acquired shares in Tesco and Mysale Group. Both, the Findel and the Debenhams trade doesn’t look that great either for the time being:

However they seemed to have hedged some of their exposure via put options. In 2015/2016 finally they sold half of their JD shares and bought 29,9% of Findel Plc plus 2% of US-based Dick’s Sporting Goods.

Interestingly they use a lot of derivatives and margin in their stock investments. This lend to some problems in 2008/2009 as on of their creditor banks from Iceland went into bankruptcy and took some of the shares “with them”.

All in all, since the IPO, they had one real hit with JD Sports, the rest of the “stock trading” activity was not really adding value.

So is Mike Ashley a retail stock picking genius ? So far, I would not say so.Too many misses and only one good trade doesn’t make a genius.

Mike Ashley seems to be however very smart when it comes to selling his own stock. He sold a nice bunch of Shares (110 mn GBP) in January 2015 at ~7 GBP per share. He sold an even bigger stake (340 mn) in Apri 2014 at a price of 8 GBP.

Interestingly, Ashley also seems to do deals with his private money, such as the 11% stake in House of Frazer he bought in 2014.

One other observation: Strange “Like-for-like” numbers

SportsDirect shows some strange like for like growth numbers. In 2015 for instance they show this:

Retail Stores UK 2015 sale: 2.015 mn GBP

Retail Stores UK 2015 sale: 1.939 mn GBP

“Like for like contribution growth”: 7,4%.

Those numbers are strange. Overall sales grew only 3,9% and UK stores grew 5,5% to 440 from 417. So you need to do some quite creative adjustments to come up with “like for like” growth of 7,4% if store count grows faster than sales.

Summary:

As is stated in the beginning there is a lot to like at SportsDirect. The core “hard discount” Uk business and the online business look very solid as well as brands. I think it is also a very “entrepreneurial” company.

However it looks like that the growth runway of this model within the UK has ended and that for further growth they need to try different things, such as moving onto Main Street or go European. But this doesn’t seem to be easy and especially now with potentially significant negative effects from the “Brexit” and increasing pressure on minimum wages etc.

For the time being, I will put SportsDirect on my watch list “only”, as I do belive that there is some pain to come and it needs to be seen how they cope with it. I think I will need to understand the company better as the business doesn’t seem to be as easy as it looked at first glance. If they manage to overcome their issues, the current price would be attractive, but at the moment I have a hard time to judge this.

P.S: Some Ashley / SD links:

https://www.theguardian.com/business/2015/dec/09/sports-direct-warehouse-work-conditions

http://www.telegraph.co.uk/finance/11563435/How-fair-does-Sports-Direct-play.html

https://www.theguardian.com/business/2008/may/21/sportsdirectinternational.consumeraffairs

http://www.retail-week.com/dave-forsey/5020513.fullarticle

http://www.heraldscotland.com/sport/13193432.Mike_Ashley__The_Elusive_Billionaire/

New article on Sport’s Direct in the Guardian:

https://www.theguardian.com/business/2016/aug/25/sports-direct-corporate-governance-criticised-investor-forum

When I hear “low-price, own-brands, hard-discount sport retailer, I intuitively think “Decathlon”.

I know the are on the Run in Germany and a new big thing in Berlin, every german sport retailer may feel it.

So my question: What is the british Strategy of decathlon and how well can sport direct compete with them?

Has Decathlon the same disruptive potential for sport retailing as Aldi has for food retailing and perhaps Ikea for furniture?

I mentioned this to Wertart to no avail…keep an eye on unfunded pension liabilities and litigation provisions.

This is the eye of the storm post BHS – Ashley and Green were inspired by each’ other business practices. Look what happened there.

SportsDirect has no pension issue. I am not sure about “litigation”….

Not sure about that:

http://www.thisismoney.co.uk/money/news/article-3457260/Sports-Direct-pension-plan-UK-s-meanest-staff-getting-average-annual-payment-88-research-claims.html

Great analysis on Sports Direct! thanks. It would also be great to get your opinion on the current price level – is they express enough margin of safety or not.

The company has impressive returns on equity (21.75%) especially considering the low leverage – I find it hard to believe that is all at the cost of exploiting employees while waiting for a security check.

– A 6.5 p/e (ttm) and consistently good underlying free cash flow (if we trust what they say on their earnings report) seem to make Sports Direct a solid bargain.

– I looked at the company’s “underlying cash flow” minus Capex and this gave me a price/adjusted_fcf ~ 7 for the past couple of years (at today’s price)

Good point made on their mediocre inorganic growth and stock picking adventures.

Also very helpful explanation on the capital allocation.

I am long Sports Direct (opened a position less than a month ago) but I am leaving some room to buy more if price falls another 10-20%

if you look at “trailing P/E” you should adjust for the JD Sports stock sales.

Leverage for a retailer always comes via Operating leases. If you include this, the returns are still ok, but ther is clearly leverage.,

Fraser, not Frazer

Joe Frazier? I didn´t know he had to sell a part of his house.