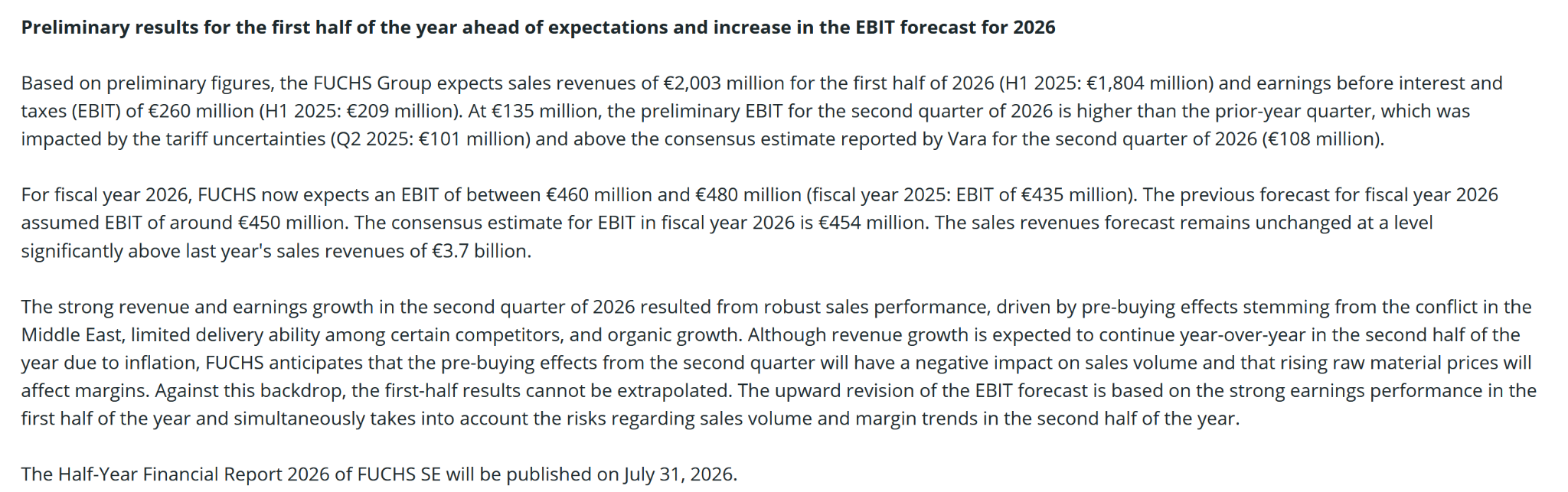

I talked to some other investors about this and they mostly mentioned that this looks (once again) as a one-time effect with maybe compensating negative results some quarters down the road, very similar to what happened after the attack on Ukraine.

That most likely explains the very muted reaction to a 35% increase in EBIT in Q2 and a significant increase in the full year guidance that according to the release already is conservative.

I actually bought back the shares slightly higher to the level I solid them last year (33,50 EUR vs 31,50 selling price).

What I found especially interesting in the statement from Fuchs was the following passage:

“The strong revenue and earnings growth in the second quarter of 2026 resulted from robust sales performance, driven by pre-buying effects stemming from the conflict in the Middle East,limited delivery ability among certain competitors,and organic growth. “

Digging a little bit deeper one can relatively easily find articles that the Gulf region was and is a major exporter of lubricants and especially the underlying base oils that are needed for high performance lubricants.

In addition, on major base oil refinery in Qatar was directly hit by Iran according to this article:

“Approximately 44% of U.S. Group III demand is typically supplied from the Persian Gulf, but that supply is now largely offline. Damage to Shell’s Pearl GTL facility in Qatar—caused by Iranian rocket strikes—has halted production from a key source of roughly 30,000 barrels per day, with repairs expected to take at least a year. Additional disruptions stem from force majeure declarations by producers in Bahrain and the UAE, as well as the continued closure of the Strait of Hormuz, which has stranded product in the region. “

Although I don’t know exactly how Fuchs sources its base oils, it seems that for the time being that they are able to deliver while others have problems.

Of course the situation with Iran can change any day with a single Tweet, but I guess that some supply chain managers are maybe rethinking their dependence on Guld based lubricants which could be a structural opportunity for an independent player like Fuchs.

We will need to see how this develops, but I think Fuchs looks a lot more interesting now at least from my perspective.

Then, after the approach from Stripe and Advent I mentioned the following:

Last Friday, the stock traded at 55,5 USD, offering a 9% “discount” to the potential acquisition price which motivated me to buy a 1,5% position at that level.

The risk return ratio is not too bad at that level. The “undisturbed” price is ~47 USD and there is a pretty good chance of a higher bid either from Advent/Stripe or maybe another competitor might enter the race.

As always, one needs to prepare for volatility around any news in either direction but I think it offers a nice, uncorrelated “bet” on a potentially higher clearing price.

One key player here is clearly the new CEO whose massive bonus is tied to a stock price increase that to my knowledge is much higher than the 60,50 USD offered. So he clearly has an incentive to hold out for a high price OR a nice “golden parachute” from the buyers.

However one more thing is important to mention: This is a special situation investment for me. So if for some reason, Stripe & Advent withdraw their bid, I will sell, no matter what. For a “Value investment” I still find Paypal too hard at this stage.

At the time of writing, the Paypal share price has climbed back to 58,40 USD per share, a level where I would not buy (more).

(for some strange reason, Google Finance says Paypal is now called Adobe 😉

However, that was soon followed by disappointing 6M numbers. The preliminary 2025 numbers were not great, but back then the outlook for 2026 was still quite positive in March.

This was of course very disappointing and I started to sell part of my stake after that. We can also see that the share price is now lower than when I wrote up the stock in June 2024:

An EBIT /operating profit at the lower end of the 40-50 mn range would mean an EBIT similar to 2023 and that in a year with two very big events, the Winter Olympics and the Football Worldcup.

While that is not a catastrophe, they are now clearly far away from the 10% p.a. growth path that I had underwritten originally. To be honest, I don’t fully understand why the business is so weak.

What I also found interesting, that Canadian listed competitor Evertz has been doing very well over the past 12 months at least looking at the share price:

So while EVS claims that the war in the Gulf is the culprit for the unsatisfactory business, Evertz speaks of “revived growth” in the Middle East. That is quite surprising in my opinion and casts some doubts on the EVS Broadcast story.

So overall, I am not that confident in EVS for the time being and decided to sell my position entirely as I see better opportunities elsewhere.

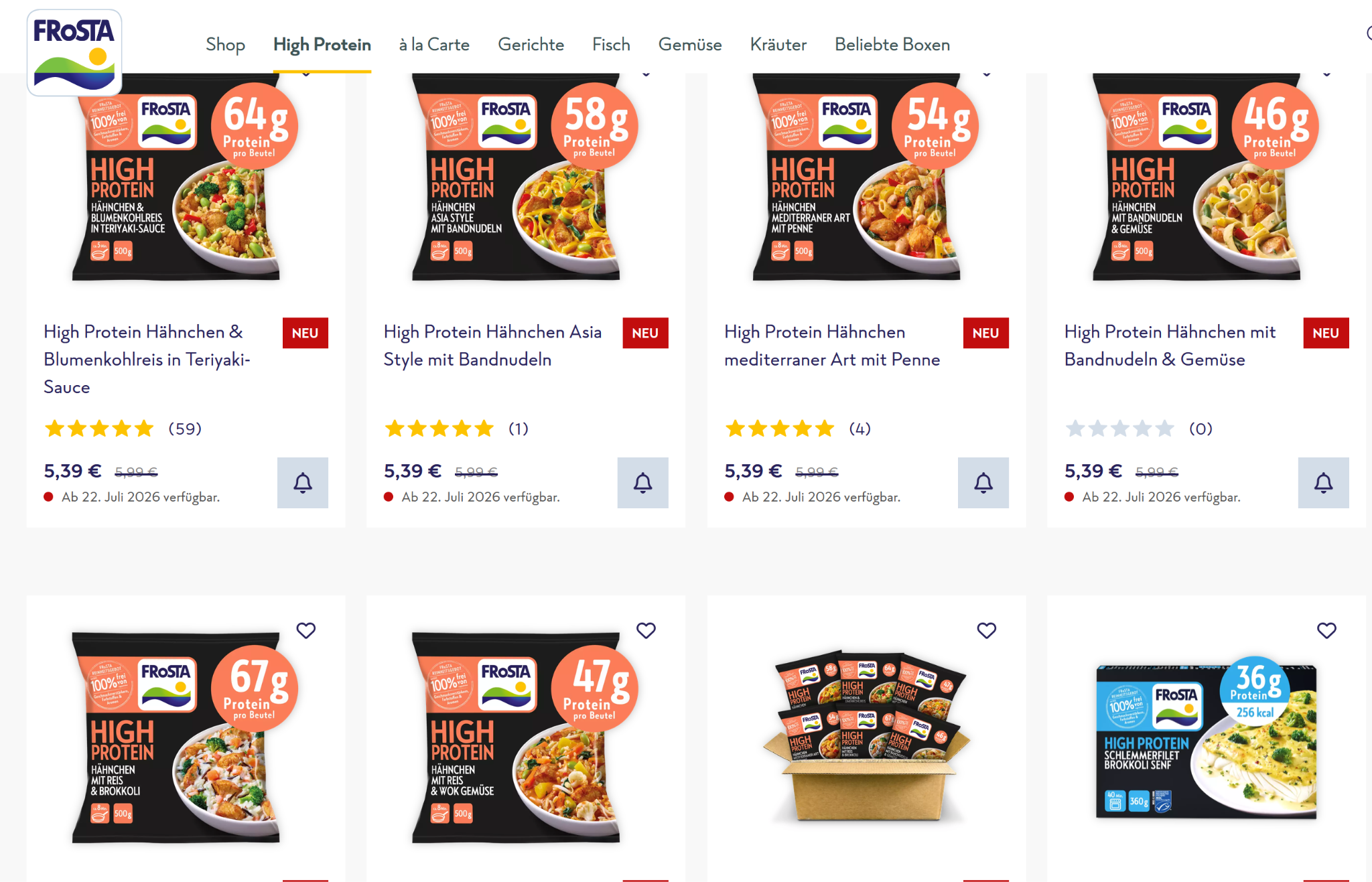

Frosta, the German “Hidden frozen Food champion” that I wrote up in February already released 6M results this week.

Highlights:

Overall sales volume increase by +11,7%. easily beating the market which was around +3%. The real kicker is that the Frosta Brand itself grew by +25% and seems to be further accelerating.

Among other things, Frosta has released two new lines of frozen meals: “High Protein” meals with more meat and “a la carte” restaurant quality meals. Both new lines are at a slightly higher priced point than the original.

I find this a clever strategy, not to increase the prices of their classic range but rather offer even better meals at a higher price point.

After tax income only increased by 2,4%. Gross margins increased a little from 48,3% 6M 2025 to 48,8% in 6M 2026, net income margin declined slightly from 5,5% to 4,9%.

However, the outlook for the full year is VERY positive.

If we take the two midpoints, 13% sales increase and 6,5% net margin, we would end up at 50 mn EUR net profit or an EPS of 7,35 EUR.

Considering that Frosta has ~10 EUR Net cash Cash per share, this translates into 13x P/E for a strongly growing company that is executing extremely well.

If we just compare this with the self proclaimed “Leading European Frozen Food” company Nomad foods, we can clearly see from whom Frosta is taking market share:

As always, Investors were not impressed very much:

I used however the opportunity to increase my Frosta position from 3,2% to 4,5%. And I will keep buying if the share price remains below 100 EUR.

Forsta is in my opinion one of these typical “Peter Lynch” investments: As a german, you can easily go into a supermarket, look how empty the Frosta Shelfs are and buy yourself a few packs to test the quality you get for the rather moderate price.

Paypal

In March I wrote about Paypal and just found it “too hard” for me, given my limited knowledge in the Payment sector.

Even back then, the rumor was that Stripe might be interested in Paypal but I found it not really realistic as there was a limited fit:

The share price jumped to around 57 USD, leaving only a 5-6% spread. which indicates that some arb players seem to expect and price in an increased offer.

As it is quite early in the process, I will keep watching this. If the price goes down a bit and we would see a spread closer to 10%, this could be a potentially interesting special situation.

From a structural perspective, teaming up with Advent makes a lot of sense for Stripe because then they can choose exactly the parts that they like and Advents monetizes the rest.

In this post, out of pure self-interest, I looked a little bit deeper into Terry Smith’s controversial 6M Fundsmith report and focus on the “Active vs. Passive” debate, how Fundsmith’s Buys and Sells look under my own Momentum scoring and some thoughts on changes in investment management styles.

Intro & Background

Terry Smith, the outspoken Boss of UK “Quality Value” Fund Manager Fundsmith dropped a quite unexpected 6M letter to investors where he basically communicated a pretty drastic pivot compared to what he said over the past 15 years.

In an “unprecedented” move, he switched ~50% of the portfolio within 6 months which is very unusual for his fund. In previous years, annual turnover of the portfolio was on average less than 10%.

His mantra of “do nothing” was repeated in every letter and often repeated in his talks.

In the most recent letter, he blames, as several times before, “passive ETFs” for market distortions and claims that those active managers that are currently successful are most likely “momentum chasers”.

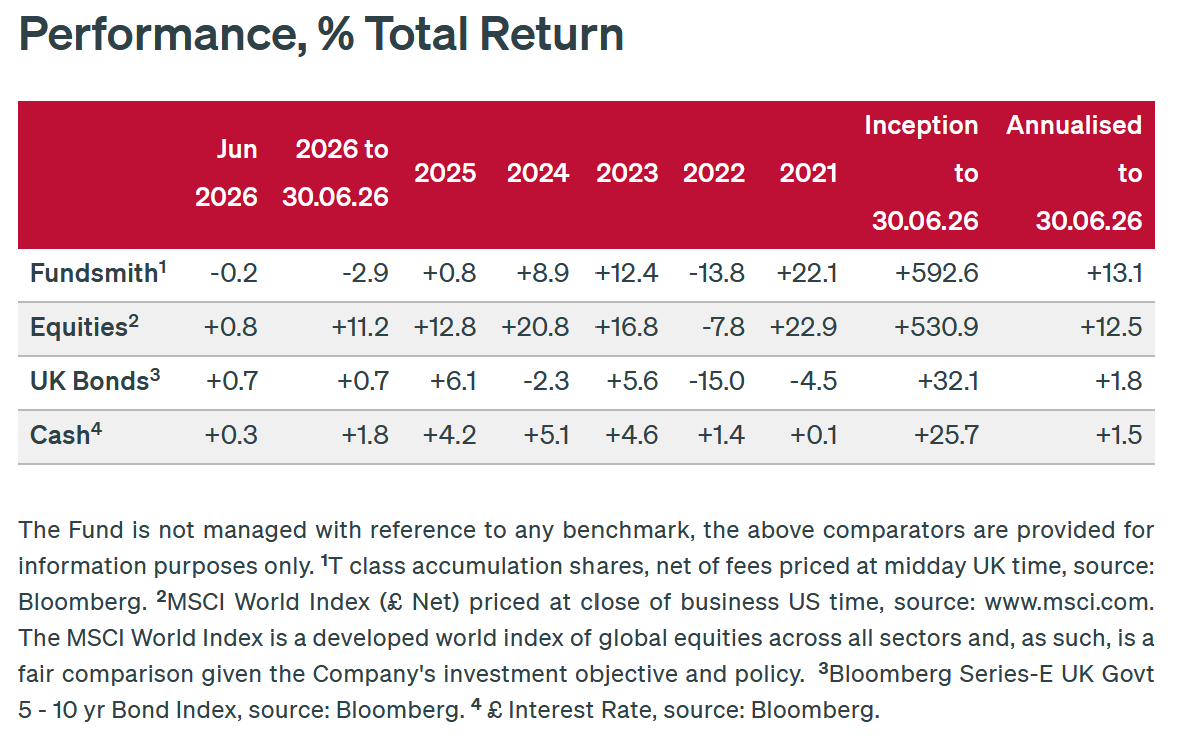

Fundsmith to be clear is not the worst active fund. With a TER of ~1% they are also not on the extremely expensive side and since inception, the track record is still pretty ok. However, a quick look at his recent fund factsheet shows that for the past 4 ½ years, the fund underperformed the MSCI World pretty drastically:

He underperformed both, in up markets and in the down year 2022. So it is clearly not a “low vol” effect.

Nevertheless I found that letter interesting due to the following aspects in which I will dive a little bit more:

Active vs. Passive

Smith’s somehow inconsistent treatment of “momentum” which is a factor I have been paying more attention to since some time now

The question of how to generally shift/pivot/adapt an investment strategy (if at all)

Active vs. Passive

I actually read the Substack post that Terry Smith referenced which can be found here:

It summarizes quite well the general view from many active managers why too much index investing is very dangerous and might end in a total collapse of the stock market. While there might be a (smallish) probability for this scenario, it sounds a little bit like the typical “Old man shouting to the clouds” cartoon.

On the other hand, the article also doesn’t really cover that as a whole, Active Management just has never really justified its rather significant cost.

In the “good old times”, active funds had been the gate keepers between individual investors and the stock market with the only alternative being stock brokers.

These days however, the ease of buying an ETF and the low cost is clearly a very attractive value proposition compared to “classical” funds where often still an intermediary is clipping an additional fee (and or the bank).

Only claiming that there will be Doom with too many passive structures is not so convincing and rather looks like an attempt to scare regulators in protecting the still very profitable business of underperforming asset managers and wealth advisors.

In my opinion, these days an active manager really needs to have a more convincing story than just that one from Mr. Evan-Cook. Your really need to offer something to investors that they can’t get through low cost Index ETFs which is not so easy.

They argue that the opposite is true: As the remaining ones are the smart ones, there are not enough “patsies” to make the “big hay”:

In any case, it will be interesting to see how the active vs. passive debate continues, but there won’t be a magic turnaround any time soon in my opinion. Index ETFs are here to stay and the Active Management industry really needs to find ways to create actual value for investors in some way.

2) Momentum

In the letter, it almost seems that Terry Smith has written parts without looking at the whole “enchilada”.

On page 3&4 he shows a chart that Momentum is dangerously high as last seen in 1999 before the Dotcom Boom. And then, only a few pages later he writes the following:

We will take more account of momentum — both fundamental and share price — in our investment decisions. In particular, we will be much less willing to deploy the time-honoured technique of buying quality companies when they hit a glitch

As some of my readers might remember, I did start to include momentum into my decision process a year ago. But in a less drastic way than Terry Smith and more “gradual”.

In my comprehensive Scoring system, Momentum is reflected by 4 indicators as part of an overall score that also includes “Quality” and “Valuation”:

For “momentum” my crude assessment looks as follows:

Current EPS momentum (i.e. EPS LTM is higher than the previous year): 1 Point if Yes, 0 otherwise

Stock price is above the 200 day moving average 1 Point if Yes, 0 otherwise

The stock price performance of the last 6 Months (1 Month lag) is positive or negative (1 Point of Performance is > +5%, -1 point if Performance is <-5%, 0 points otherwise)

The stock price performance of the last 12 Months (1 Month lag) is positive or negative (1 Point of Performance is > +5%, -1 point if Performance is <-5%, 0 points otherwise)

So overall, my “momentum score” can go from minimum of -2 to a maximum of +4 within a total score that can reach, including Quality and Valuation, scores a total score of 18.

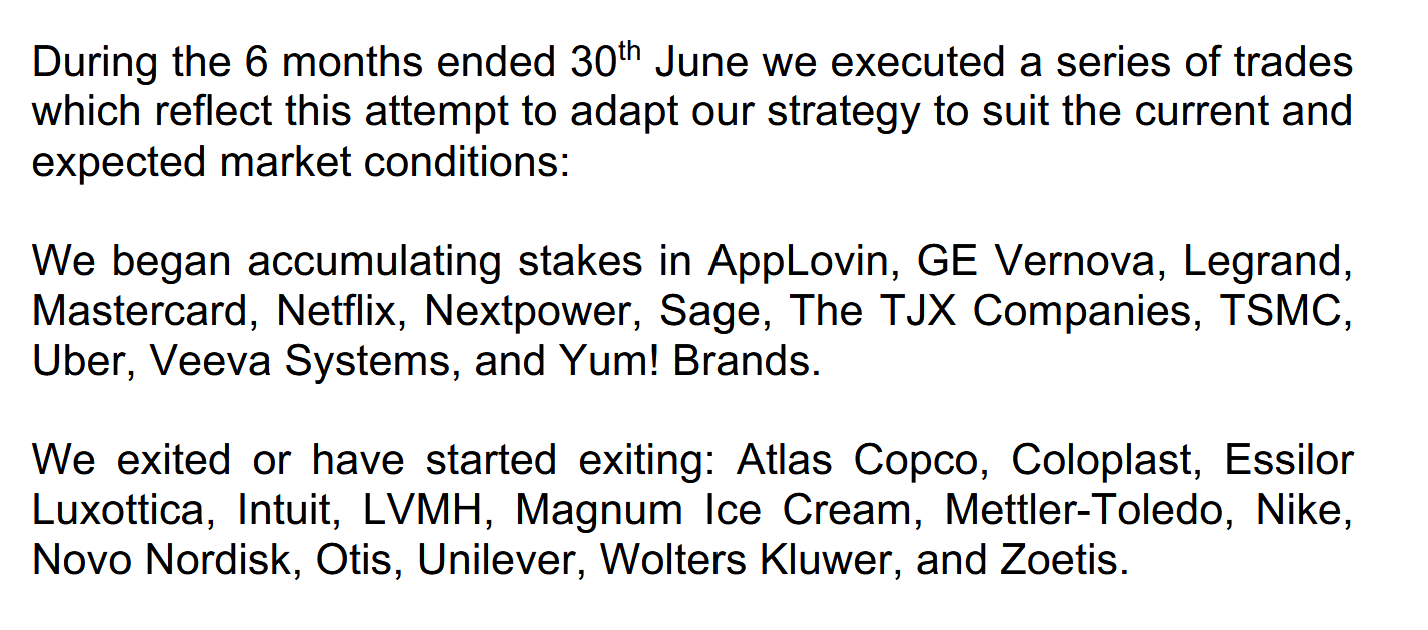

So for fun I just tried to score the stocks that Fundsmith sold and bought. Here is Terry’s summary:

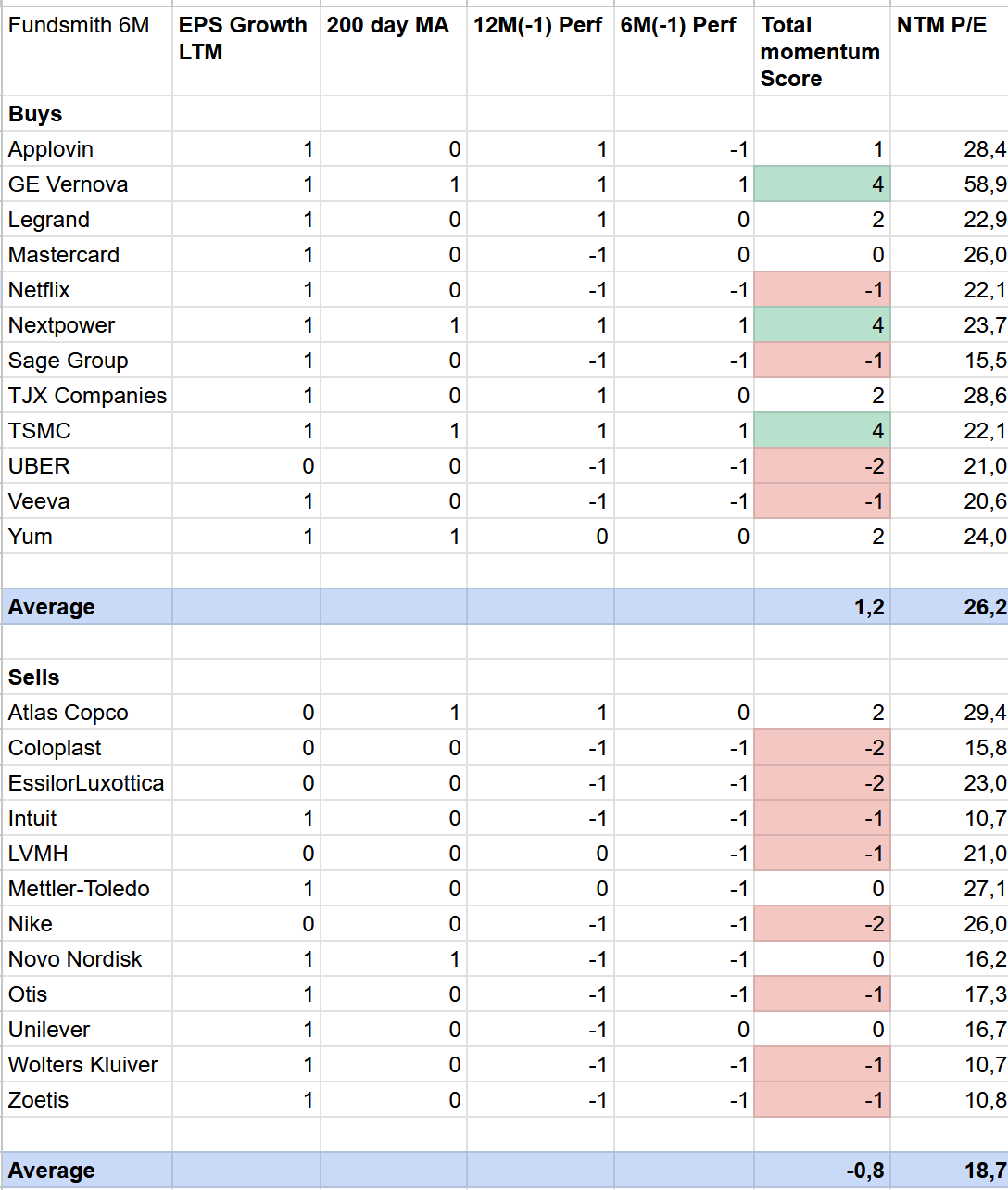

And here is the table scoring Terry’s stocks, both, the buys and sells with my crude momentum measure:

Two things stand out in aggregate:

The stocks that he sold, on average, look indeed worse from a momentum perspective than the ones he bought. And the stocks he sold are a lot cheaper than the ones he bought.

It’s also interesting that only 3 of the stocks he bought would get a maximum Momentum score in my system (GE Vernova, TSMC and Nextpower). Some of the stocks have rather negative Momentum under my definition (Uber, Netflix & Veeva).

It’s also obvious that he wanted to have some exposure to the Datacentre /AI theme via TSMC, GE Veronica, NextPower, Legrand and maybe UBER.

Overall it looks to me that he still focuses on fundamentals but looks for more “positive fundamental momentum”.

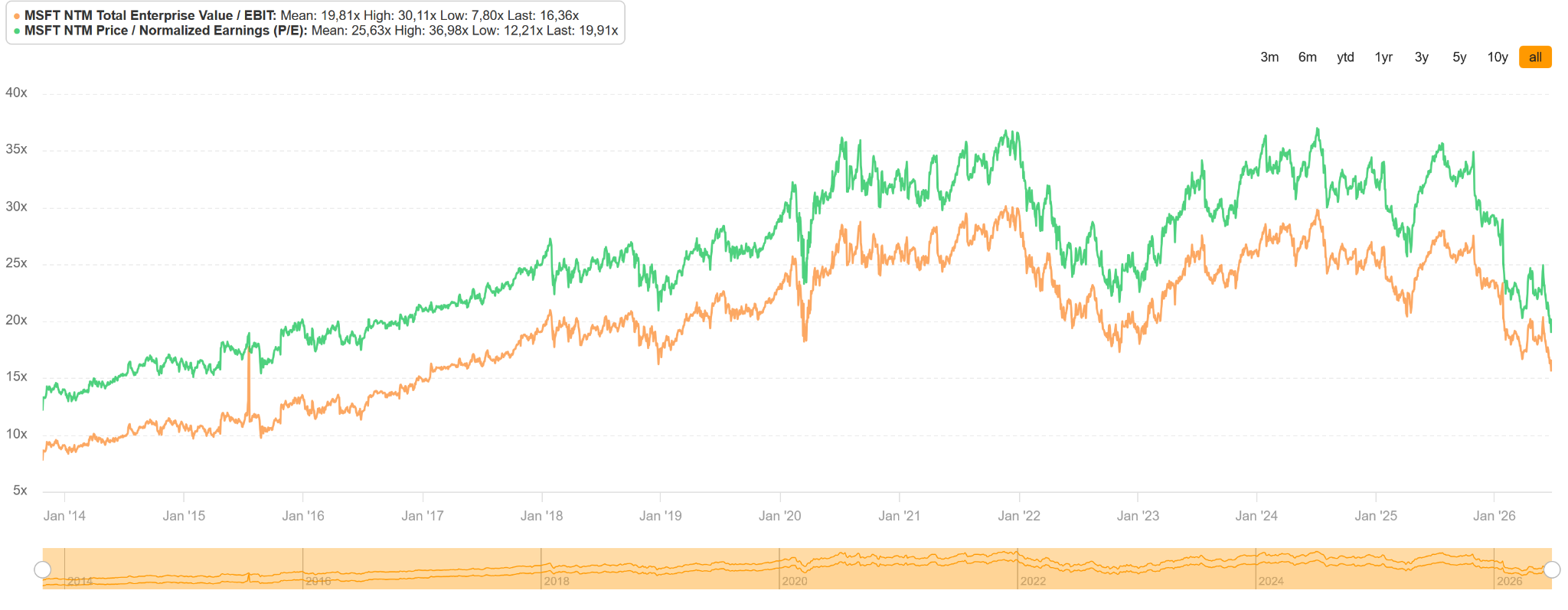

One question I have been asking myself is why he didn’t sell some of these stocks earlier. One example which I have looked into under another context is Essilor Luxottica. Here is the chart of the implicit NTM PE over the past 10 years:

We can see that until the end of 2025, the stock was valued at 40x NTM P/E, far above the average.

If we look at the margin and Return on Capital ratios over time we can see that after the merger between Essilor and Luxottica, margins never recovered there previous level and Return on Capital was a depressing mid single digit.

That begs the question why you would want to own such a stock at such a valuation in the first place.

Anyway, Terry Smith clearly now wants to avoid “unloved” stocks and is looking to invest more into stocks that do at least from a fundamental perspective well, even if the new stocks are on average significantly more expensive than the sold ones.

With such an approach, in my opinion, his “do nothing” mantra won’t work, because in the current environment, fundamentals can change ven more quickly than before.

It will be interesting to see if and how fast he will turn over his portfolio going forward.

3) If and how to shift/pivot/adapt an investment strategy

One “peer” to Terry Smith is Nick train from Linsell Train funds who has a similar “quality focused” approach. In his 6M letter (Global Fund) however, he is rather adding to his losers than selling them. One prominent example is Intuit:

But buying a consensus AI loser stock today doesn’t mean arguing no risk from AI (or anything else we haven’t yet seen coming). It means taking a calculated risk, based on

likelihood and the trade-off with price, and accepting the emotional discomfort of appearing unconventionally wrong. To give a pertinent example, Intuit was easily the Fund’s worst performer in June, declining 21% in USD terms, down now nearly two-thirds from last year’s highs. Whilst 2025’s valuation was arguably steep at a c.2.5% free cash flow yield, the collapse to what is now over 10% feels egregious. As above, we think it likely that the prior

bullishness resulted from the general extrapolation of past successes – with, it must be said, some justification: Intuit has grown revenues organically at double-digit rates every year this decade, whilst its EPS is up 4.5-fold versus FY2016. But the forward bearishness, predicated we assume on acute (but typically unsupported) fears of AI disintermediation, feels disproportionate. The non-GAAP multiple on next year’s EPS (which management still guide to grow at c.16-18%!) is now down to 11x. To achieve a normal nominal return (say the US market’s historic 9% p.a.) now implies negative forward earnings growth. As little as a year ago, analyst debate focused on whether Intuit could sustainably hit 20% revenue growth versus the prior mid-teens rates

I think the Nick Train vs. Terry Smith “contest” is an interesting case study on the merits of changing your investment approach abruptly.

One needs to mention that Nick Train’s track record for this fund is even worse than Terry Smith’s, underperforming the MSCI World by a pretty wide margin since inception in 2011:

Overall, I think in every long investment career, it will be necessary to change and adapt one’s approach to investment in order to stay relevant.

The most famous example here is Warren Buffett who changed his approach fundamentally at least 2 times. From Graham Deep Value to Quality to “Full scale take-over conglomerate” investing. With his initial approach, he would never had been able to reach the size that he has reached today. The same with listed-minority investments in general.

From what I have seen, a rapid increase in AUMs for any manager is often in the end much more a curse than a blessing. Yes, you earn a lot more fees but unless a manager significantly adjusts the strategy, returns will suffer after a certain increase almost inevitably.

The question is clearly how to do this in a way that does not create confusion on the investor side and is hopefully constructive for the future results.

In Terry Smith’s case, I am struggling a little bit with his previous mantra that “do nothing” is the one and only thing and then abruptly change that within a 6 month period. My feeling would have been that he should have toned down the language a little bit earlier already, unless he really did this pivot on short notice.

In Nick Train’s case, doing nothing (or not much) after now being down since inception is maybe also not 100% optimal.

For a lot of institutional investors, 3 years are maybe the maximum they can tolerate underperformance before they pull the trigger. Both Fundsmith and Lindsell &Train are clearly past that mark.

From my perspective, every active fund manager should realize that luck is a big part of the game and when things are good, one should give some credit to good luck instead of claiming all the outperformance due to superior skills. I guess that might make things a little bit easier when inevitably things don’t look so great.

In any case, I do think that a shift in strategy should be prepared and executed including relevant and documented changes in process and also personnel.

What you clearly also need is some patience. Don’t expect that a structural change will improve performance on day one. This will need time.

In any case, as mentioned above, Active Equity Management is facing a lot of headwinds any way, which makes it even more difficult to dig yourself out from an “performance hole”.

Summary:

It is obviously too early to tell if and what we can learn from Terry Smith’s recent actions, but on the surface they look a little bit like a “panic move”.

Going forward, Lindsell & Train will be a good comparison because they seem to keep doing what they have been doing and are even doubling down on their losers.

In any case, for me personally it is clearly some kind of evidence that completely ignoring “momentum”, being fundamental or purely stock price driven is not a good idea. “Do nothing” in my opinion is harder than ever and maybe not the dominant strategy going forward. In my opinion, using momentum as an additional factor in stock picking and portfolio management can clearly improve the process to a certain extent.

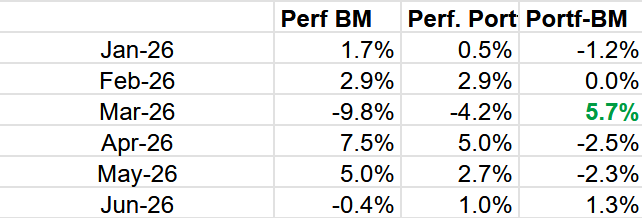

In the first 6 months of 2026, the Value & Opportunity portfolio gained +8,1% (including dividends, no taxes) against a gain of +6,2% for the Benchmark (Eurostoxx50 (25%), EuroStoxx small 200 (25%), DAX (30%), MDAX (20%), all TR indices).

Links to previous Performance reviews can be found on the Performance Page of the blog.

Performance review:

As mentioned in the last 12M review, I decided to do only one midyear review instead of 3 quarterly ones.

Relative to my European focused Benchmark, the first 6 months were pretty Ok. In absolute terms, once again I was lucky not to have had a Crystal ball at the beginning of the year.

With the Iran war, the Strait of Hormuz still being closed and inflation ticking up, I would have not thought that stock markets would be up in the first 6 months.

Some of my positions disappointed, such as EVS, Wise or the Active Ownership Fund (once again). However, my bigger positions, especially Jensen, Eurokai, Bombardier and DCC did well.

For the record, this is the monthly development of the relative performance for 6M/2026:

For the first 6 months, the portfolio performed as intended: Lower drawdown in bad months but also less upside in good months. As I have mentioned several times over the years, I feel better having less than market volatility in my portfolio.

Going forward this will be not only about feelings but also a necessity as I will soon enter the “harvesting” period in my investor career. Which means more money will flow out of the portfolio than inflows which makes it even more important to manage volatility. But more on that at a later time.

I have implemented everything now in my investment process. Did it help ? Hard to say, because a short term performance record is subject to a lot of random noise.

One thing I can say is that my portfolio would look differently if I had not implemented these changes. I might not have bought for instance more Eurokai, Jensen and Bombardier. I might have added to EVS instead after the share price dropped or actually sold some of the larger positions.

So far, I “feel” that these changes help me focus better but of course this could turn out to be wrong. To be continued.

Transactions 6M 2026:

The current portfolio can be seen as always on the Portfolio page. Cash is currently around 9% of the portfolio.

I exited Special Situation Bois Sauvage after a decent run up as well as SFS which I found too expensive in relative terms. I also sold my little bet in Sixt common shares, SAMSE and Laurent Perrier.

I bought and sold as Special Situations BioNTech and Rocket Internet.

New positions were Frosta, Bachem, Norma and 7C Solarparken. I added to Frosta, Gerard Perrier, Frosta and recently Sixt. I reinvested the gross dividends into Eurokai and Sixt. I reduced my EVS position after the quite disappointing outlook and the exit of the CFO. In addition, I also reduced STEF mainly because of their cutting the dividend. Both, STEF and EVS declined significantly in my internal ranking which makes it difficult to justify a large position.

In addition, I also decided to quit the Active Ownership Capital Fund and sent a cancellation order which will be executed by year end.

Current Cash levels are at around 9,3%, the largest 10 positions sum up to 56% with the top 3 totalling 25%,

Random ramblings: AI winners vs. losers, European AC, Volkswagen & Football 2026 Worldcup

AI winners & losers

Despite some setbacks, the “AI trade” is still strong and I think very few people now seriously doubt that the AI revolution is for real. Sometimes it is hard to believe that only 3 ½ years ago, the world experienced the “ChatGPT” moment when the first version of OpenAI’s chatbot had been released and this crazy journey started.

What I find very interesting is how quickly the favorites have changed on the “front end” side of things. Initially, everyone agreed that OpenAi and Microsoft would be the winners in this game among the big Hyperscalers. Microsoft secured early a big stake in OpenAI and immediately tried to integrate it into a product called “Co-Pilot”. The same playbook they used for instance to crush Zoom with Teams. “Distribution always wins” was the early verdict.

Now, It currently looks like Alphabet/Google is winning on the retail side and Anthropic on the B2B side if the current US Administration will let them do so. OpenAI, the “first mover” on the other hand seems to be pushing its much anticipated IPO into 2027 and Anthropic might not want to IPO either, as at any second, the US Administration could try to kneecap them again.

Microsoft’s Copilot is only used by people who have no other choice. Despite Microsoft having sold 20 million seats, some sources say that only 20-30% of those seats are used on a weekly (!!) basis.

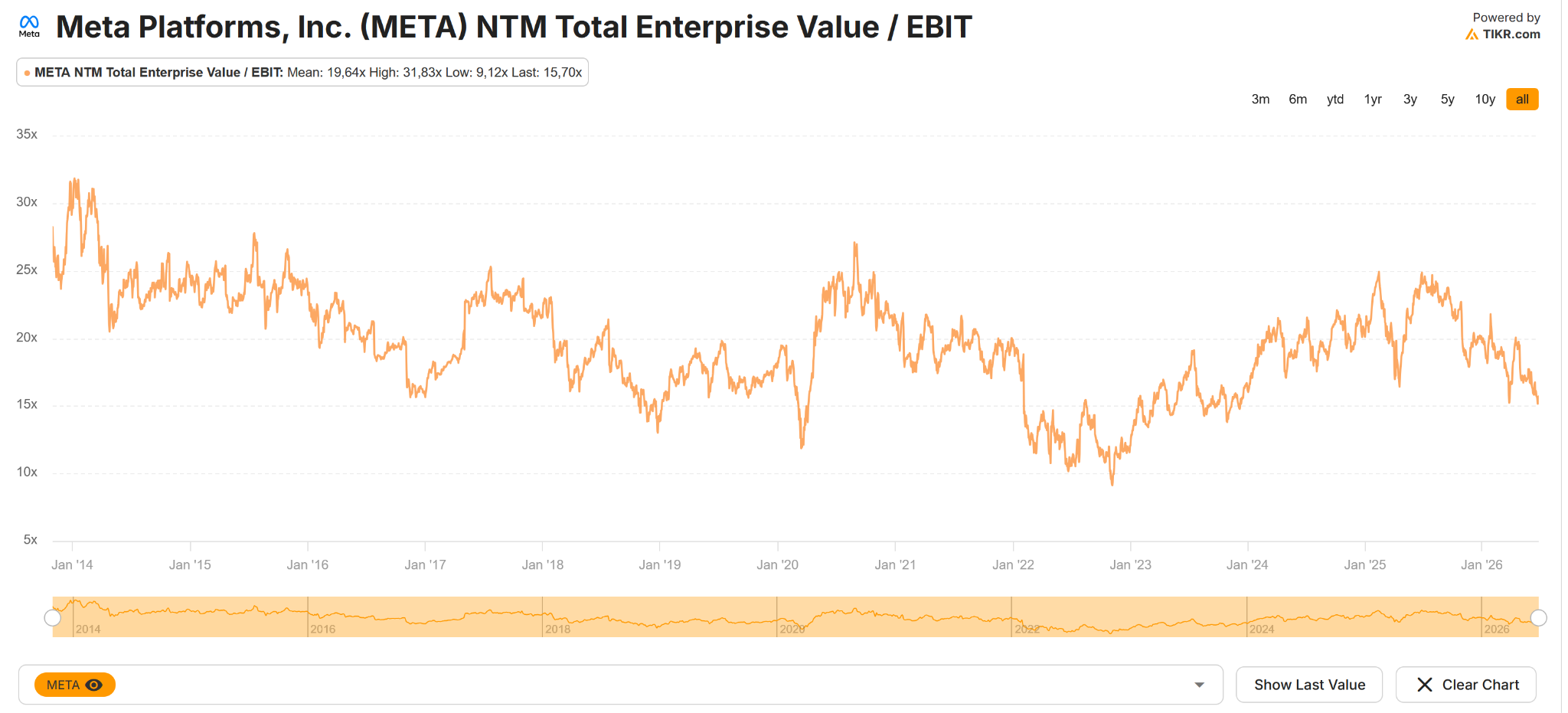

Looking at the “Mag 6 (ex Tesla)” stock charts since November 2022, the best trade was clearly Nvidia which is no surprise. But Meta, which clearly has not been very successful at the AI business, is clearly number 2.

Meanwhile the initial clear winner, Microsoft, is the worst performer. Even Apple, which so far has done very little on the AI side, is doing better.

For Meta, part of the explanation is clearly that they were trading historically cheap in autumn 2022 at around 10x LTM EV/EBIT. On the other hand, they also tripled EPS from 2022 to 2025:

Microsoft in comparison traded at around 20x EV/EBIT in Autumn 2022 and is now trading at a slightly lower multiple:

And more importantly, EPS “only” increased by less than 100% depending on where you make the cut-off.

So what I want to say here is that even looking at the Hyperscalers, starting valuation and EPS increase are at least equally important than the pure story telling.

We are still early in the race and so far, the “first mover advantage” didn’t really seem to have worked out for Microsoft and AI. I guess we will see in the next years if maybe even Apple’s approach of wait and see is maybe the best one ? Prof. Damodaran even praised them with an article called “An ode to restraint”. In my opinion, the winners of this “platform shift” are clearly not carved in stone and maybe we will see completely new players in the next few years and don’t forget the Chinese players.

On the other side, with all the Capex, the risk on the side of the Hyperscalers clearly increases, especially if they are not among the winners.

European AC & Climate adaptation

During the recent heat wave, my Twitter feed was full of posts that “Europeans are too stupid” or too poor to have AC.

As always, generalizations like this are generally extremely stupid (with the exception of this generalization of course). While I am writing this, we have heavy rains and ~20 degrees Celsius and the worst seems to be over for now.

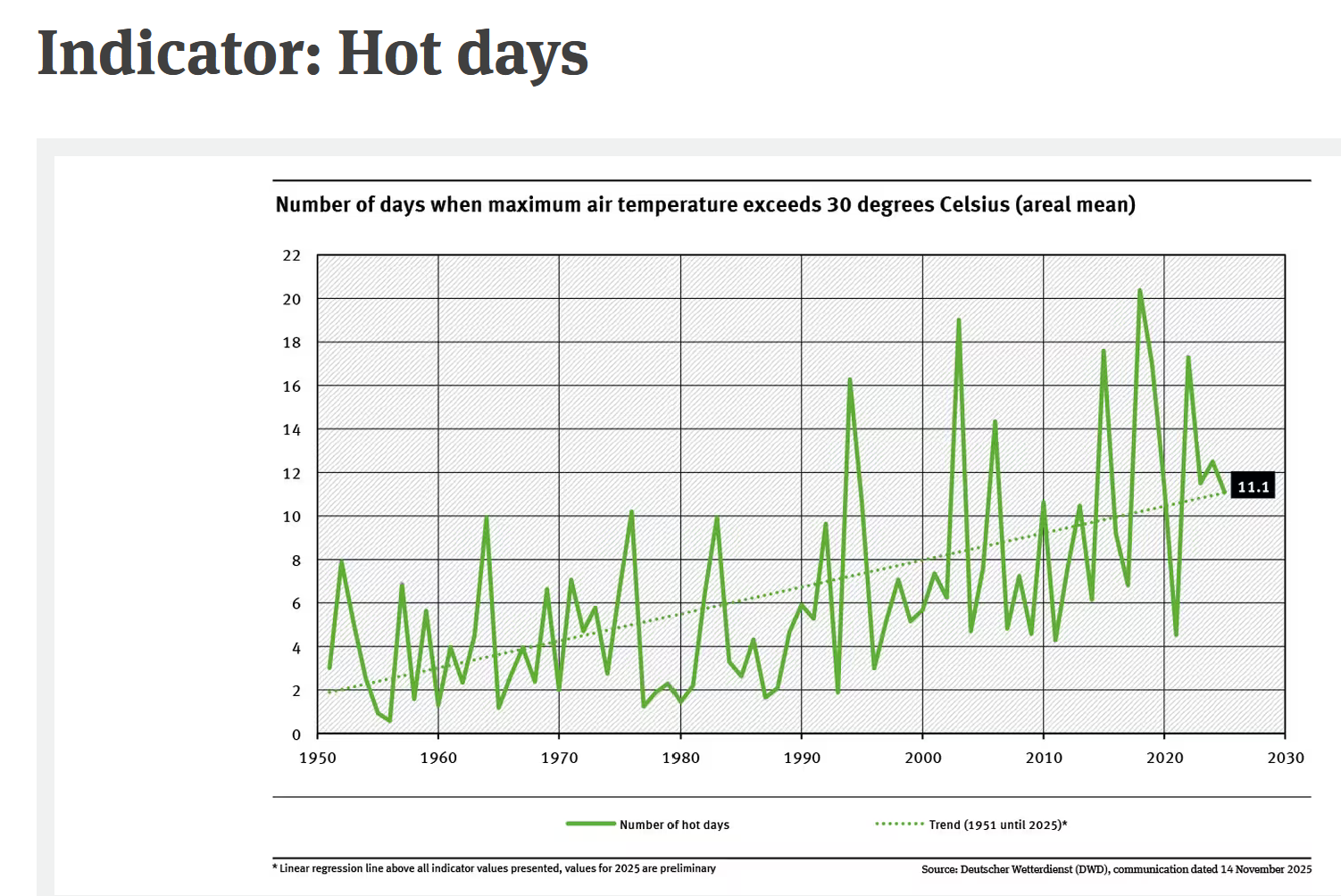

But behind that stupid discussion, there lurks an “unconvenient” truth: The climate is getting warmer and half a degree more on average in a year unfortunately does not mean half a degree more every day but more and more very hot days in summer.

20, 30 years ago, there were maybe 2-3 really hot days in Summer, now it is maybe on average 11 and still increasing:

This is surprisingly (or not) a bigger problem in the more moderate climate zones like central Europe than in the North or in the South of Europe. Anyone who has actually travelled in Europe for the last 20-30 years knows, that the poorer Mediterranean countries like Portugal, Spain, Italy or Greece are very well equipped with AC. Summers were always hot in Italy and that’s why Italians are at the Beach in July and August and only stupid tourists are walking around on foot in Rome and complaining.

The problem is clearly much more in areas like Southern/Middle Germany for instance. The Rhine basin where a lot of the big population centers are in Germany is generally a relatively warm region. Traditionally they have always been wine growing regions unlike for instance Bavaria where I live or Northern Germany near the coast,

Really hot days in a row, where the temperature does not go down at nights are clearly a strain without air conditioning.

The average age of residential buildings in Germany is around 40-50 years. That means they were built in a time where on average there were only half the hot days that we have now. In addition, a lot of renovations increased the “vulnerability” like increasing window size or remodelling roof storage units into apartments.

Many homeowners that I know have already installed AC in the last few years. However, one of the issues in Germany is that more than 50% of Germans are renters and installing an AC in a rental unit is much more difficult.

In addition, a lot of public buildings still get built without AC and authorities are really slow to retrofit AC in public buildings. This in my opinion is the real issue: Hospitals, old age homes, schools etc. need to be upgraded as quickly as possible. On the weekend, there was an “open house” of the brand new Fire Brigade building in my neighbourhood and of course it does not have AC.

According to some articles, an existing program to fund AC in public buildings has been actually cancelled for 2026 by the current Government. As always, there is a struggle between local authorities and the Central Government who is responsible.

But AC is only a part of the story. The much more inconvenient part of that story is that Global Warming is real, that countries with relatively moderate climates are not well prepared and that the lack AC might only be the tip of the iceberg. In the past few years, we already had some really dry summers that led to pretty bad harvests for instance.

Climate adaptation is a much bigger topic than just installing more AC units. I think even the hardcore Greens are beginning to understand that one has to face reality and cannot only dream of stopping Global Warming but really make an effort to compensate for the effects.

Right now, everyone is looking for more exposure to AC manufacturers, but in my opinion a company like Thermador which specializes in irrigation components also plays an important part in helping with climate adaptation. The stock chart already shows some life in the past few days:

Volkswagen

Volkswagen made a big wave this week that they are planning to “fire” up to 100K workers. As with the German National Football team, each and everyone seems to know exactly why Volkswagen seems to be doing so badly.

The main culprits mentioned are often the Decommissioning of the Nuclear plants in Germany or the EU guidance to not allow Internal Combustion Engine (ICE) cars to be built from 2035 onwards and the general laziness of German workers.

From my perspective, Volkswagen troubles are more a function of the following factors:

Legendary bad Corporate Governance: With the Government owning a “golden share” and the Porsche/Piech families not really knowing what to do, the only common denominator for a long time was just size which is never a good strategy in the long term

Too many brands that are hard to differentiate (VW, Audi; Cupra, Skoda…..)

The combination of US tariffs, JPY/KRW devaluation and cratering sales in China

The unwillingness and inability to fully compete with Chinese EV makers, reducing the profit in China from 5 bn EUR p.a. at its peak to currently below 1 bn EUR

Difficult footprint for accessing the US market (no Northern American plant for Audi/Porsche), Volkswagen is only in Mexico)

The inability to offer state of the art software for their “premium cars”

Badly managing their premium Sports car brand Porsche which became more and more similar to Audi

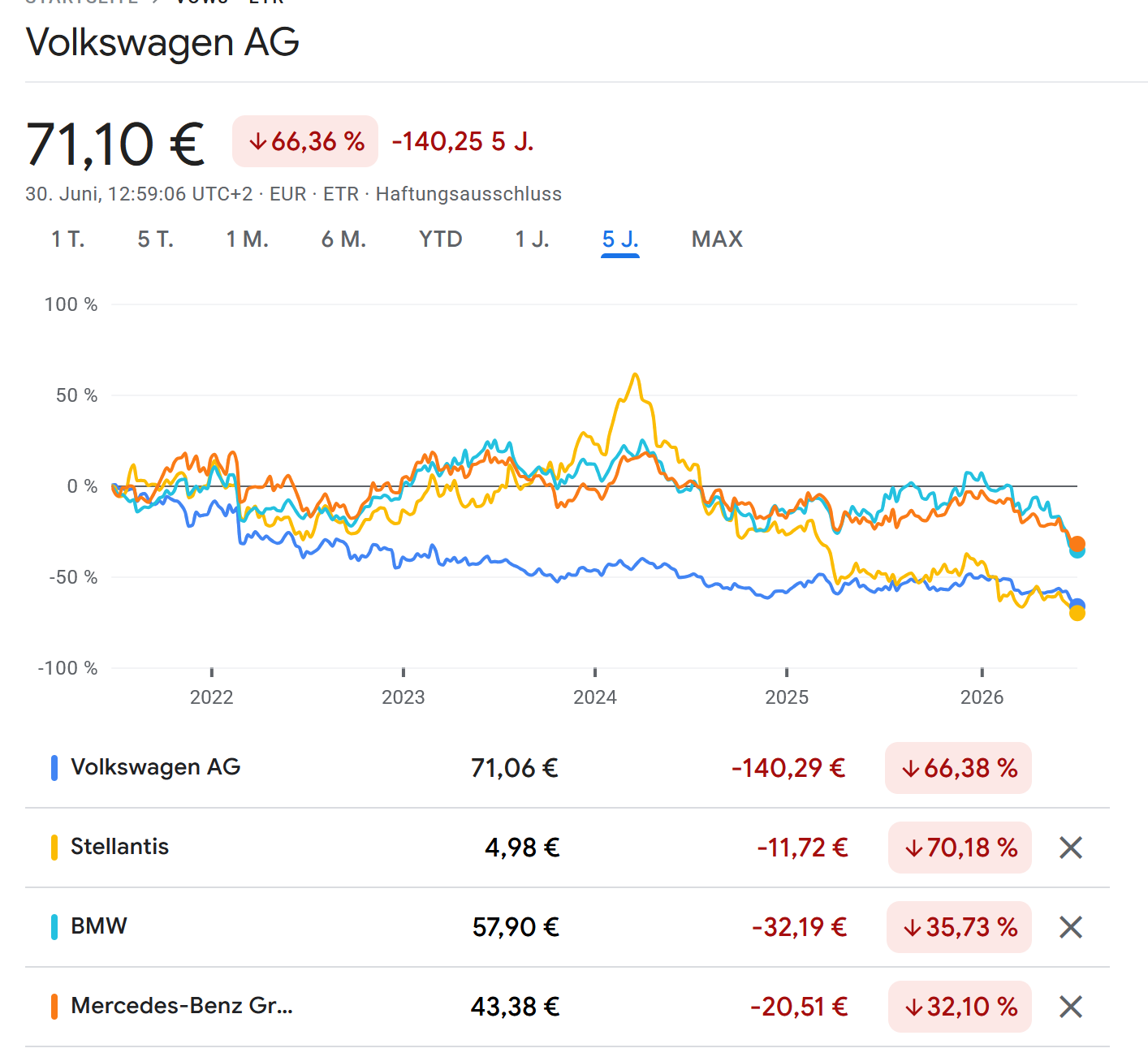

If we look at the stock chart of the big 4 remaining European car makers, we can see that we have two groups: The bad and the ugly:

BMW and Mercedes are kind of hanging in there but Volkswagen and Stellantis are both struggling. Interestingly, until early 2025, Stellantis looked like the superstar, but that did not last long.

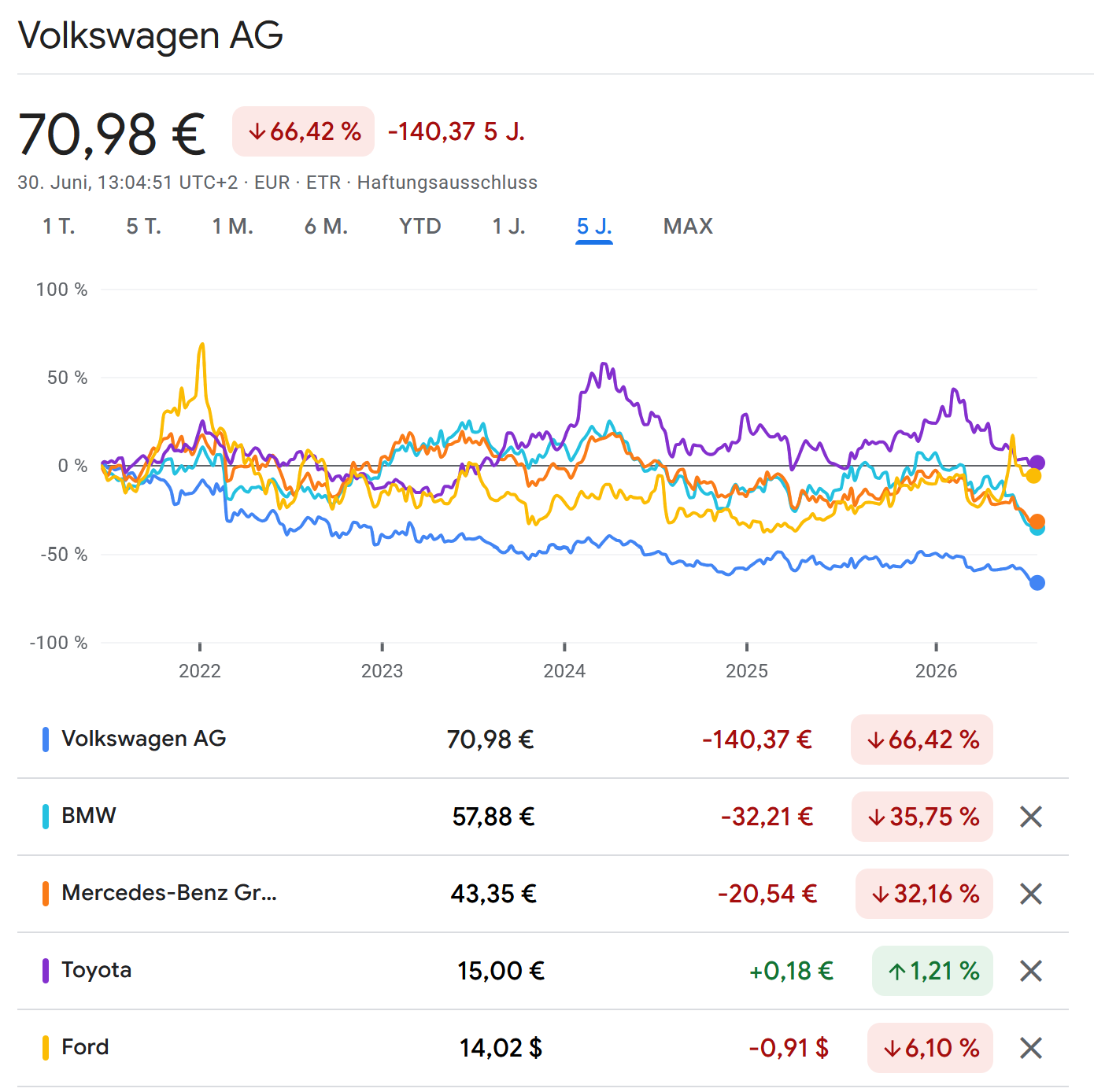

If we compare Toyota and Ford with the German players, we can see that especially Ford jumped from the Group with Mercedes and BMW into a new Group with Toyota.

My guess is that the market is pricing in the protection for Ford in its US home market via Trump’s “liberation day” tariffs.

In any case, there is no easy and quick solution for Volkswagen. If I have counted correctly, Volkswagen (incl. Audi) has ~13 or 14 main plants in Germany compared to BMW which only has 4. Per employee, BMW and Mercedes generate more than 2 the amount of sales than Volkswagen.

So if Volkswagen wants to remain competitive, they need to do some slimming down now or things might even get worse in the future.

From a pure tactical perspective, I guess Management may have mentioned a larger number than what they are aiming for in order to give the Trade Unions and the Government some kind of “sacrifice” during negotiations.

Overall, I see this as a necessary step. The worst case in my opinion would be if they are not able to increase productivity due to political interference. This would be really bad mid- and long term, not only for Volkswagen but for the whole economic complex around it.

It hink the only remotely interesting listed asset of the Group would be Porsche (the manufacturer, not the holding), if they were to become more independent from Volkswagen.

Football World Cup

With a one day period to stomach the loss against Paraguay, a few (maybe unqualified) thoughts on the 2026 Word Cup:

Overall, the decision to let more teams play in this final tournament was in my opinion a pretty good one, although I didn’t like it in the first place. A lot of interesting teams that might otherwise not make it to the finals played really well (e.g. Paraguay, Cabo Verde or most African teams)

Although people don’t seem to like the Hydration breaks, I personally find it quite convenient to have a quick break to get something to drink myself.

The new rule to require an “injured” player to stay out of the match for 60 seconds is a really good rule. It limits these situations very much which were very common in the knock-out matches before when one team had a narrow lead and suddenly players were falling like flies.

The quality of the matches on average is pretty good. I watched a few matches so far (with convenient starting times) and they were all very good and enjoyable.

In general there doesn’t seem to be a big skill difference at overall team level between the best 30 teams or so. So far, the main difference really has been the exceptional performance of some of the Superstars who then really make the difference

Teams like Germany (and Italy or Uruguay) are at the moment really lacking these individual Superstars which might explain the lack of success for those traditionally strong football nations.

The only negative is that for Europeans, the starting times of the matches are sometimes very inconvenient. On the other hand, the availability of summary videos on the next day compensates to a certain extent.

Another potentially interesting story is Easyjet, where a US investor with the name Castlelake is trying to buy Easyjet and has increased the bid price now for a fourth time.

According to some sources, the board might be willing to sell for 7 GBP.

At the time of writing, the shares trade at 5,72 GBP, a discount of more than 18% to the potential “clearing price” of 7 GBP and 12% to the last offer from Castlelake.

This is a pretty wide spread, but maybe justified because the case as such is not super easy.

For instance, in order to maintain its EU landing rights (which are essential for Easyjet), non-EU ownership is capped at 49%. To circumvent this, Castlelake seems to have teamed up with certain European individuals to restrict their ownership as US institution, put this structure will be heavily scrutinized if it comes to a bid.

What I also find interesting is that Castlelake has no track record in Private Equity. However, since 2024, they seem to be majority owned by Brookfield. But so far they have been focusing on Asset based lending, not Private Equity.

To me it is also not 100% clear which fund is sourcing this quite substantial deal.

Finally, at Easyjet, the founder is still owning 15% and he might have a lot of influence if and how this company gets sold.

Looking at the long term chart we can also see that as many other airline stocks, it was not such a great long term investment after all:

So overall, at least for me it is really difficult to “handicap” the risk of the deal not happening. Therefore I will stay away from this one despite the rather “juicy” spread.

Nagarro

Nagarro is a company I followed loosely over the years. It is a spin-off from German IT services company Allgeier and mostly considered to be a “Indian IT Outsourcing” shop.

Initially, the company became a “spin-off superstar” and went up to almost 200 EUR per share in 2022, before trending down the last 4 years to around 33 EUR:

There wer always some questions around the company and those outsourcing business models these days seem to be vulnerable to Ai Agentic coding.

For instance, the share price already increased by +20% on Friday, so it seems that some insiders were already front running the news.

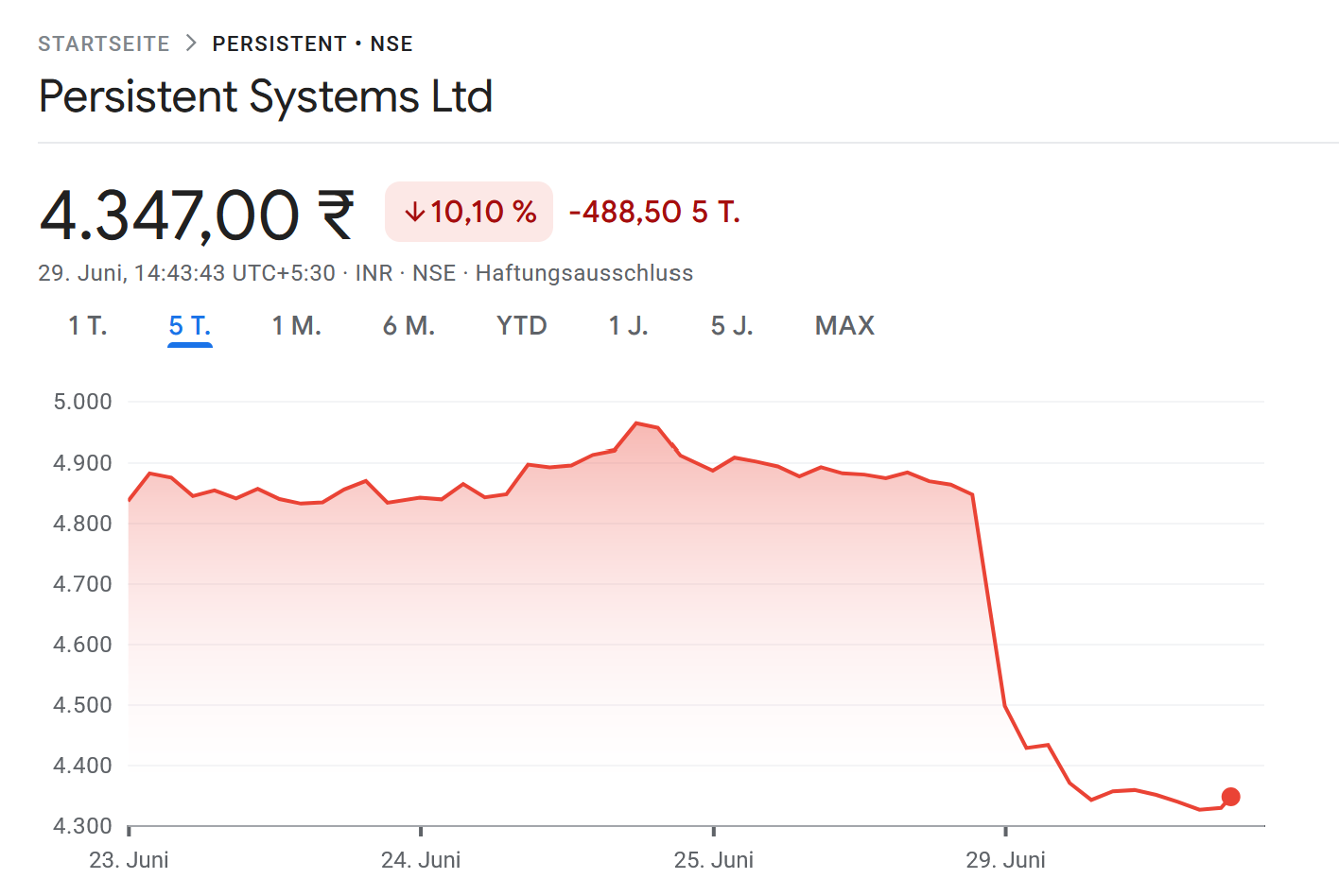

I also find it quite curious that the take over premium is so high. The bidder, Persistent Systems which is listed in India dropped by -10% today:

At the current price of 77 EUR, the discount is only 5%. There will be a dividend on July 2 nd of 1 EUR and record day is tomorrow, so this could be added to the discount, but still, something does not feel 100% right here from my perspective.

BioNTech:

Tomorrow is the day when BioNTech is supposed to announce how the separation between the founders and the company will look like.