This year, after a 7 year break, I once again went to the US to attend the Berkshire AGM. Just for clarification: I don’t own Berkshire shares and unfortunately never did because I always thought that they were too expensive.

Attendance: As mentioned elsewhere, attendance was clearly lower than in the past. The arena was only half full, the overflow rooms almost empty. On the positive side, with less people it was much more relaxed. On the negative side, prices in Omaha during the weekend are still sky high. Hotel rooms have been very expensive and Steaks in the city steakhouses cost around 60-70 USD (plus sides, taxes and obligatory tip). Most restaurants were only half full. It also seems that hotel prices for the weekend were much lower just before the weekend.

Paying 21 USD for a pretty miserable “Lunch box” during the AGM was not big fun either.

I wonder if Omaha hotels and restaurants will still be able to charge those sky high prices next year.

AGM Content:

Greg Abel is clearly not Warren Buffett. He is much more a “normal”, more operative CEO than Buffett. He also gave more air time to the other Berkshire business CEOs.

What I liked is that they clearly said that BNSF and Geico still have a lot of work to do, in order to become as good as their competitors. Another plus was that the Q&A session was not too long.

On the other side, Greg Abel clearly did not offer any philosophical insights on capital markets. This was different when Warren and Charlie were running the show and attracted the masses. And I think it is a good thing that he didn’t even try to do it.

Buffett himself appeared twice, once in a video and then in a half time break interview with Betty Quick. This interview was actually a little bit “cringe” especially when he mentioned that Greg Abel, a Canadian would become American soon and how special an American Passport is. As a Canadian Berkshire investor, I would be pretty pissed off by those comments as it kind of implies that being a Canadian is not good enough to run Berkshire. In any case, I found it super hard to actually understand what Buffett was saying during the interview.

From an “actionable idea” point of view, the only inspiration I took away from the AGM is the Tokio Marine Insurance investment. This was clearly Ajit’s idea and despite showing his age, this guy knows what he is doing in insurance. It was also interesting that this was mentioned very prominently despite being a rather small position for Berkshire.

Overall it will be interesting to see how this will develop over the next few years. Will Omoha still remain a meeting point for investors from around the world or will there be another kind of Omaha elsewhere ? We’ll find out eventually.

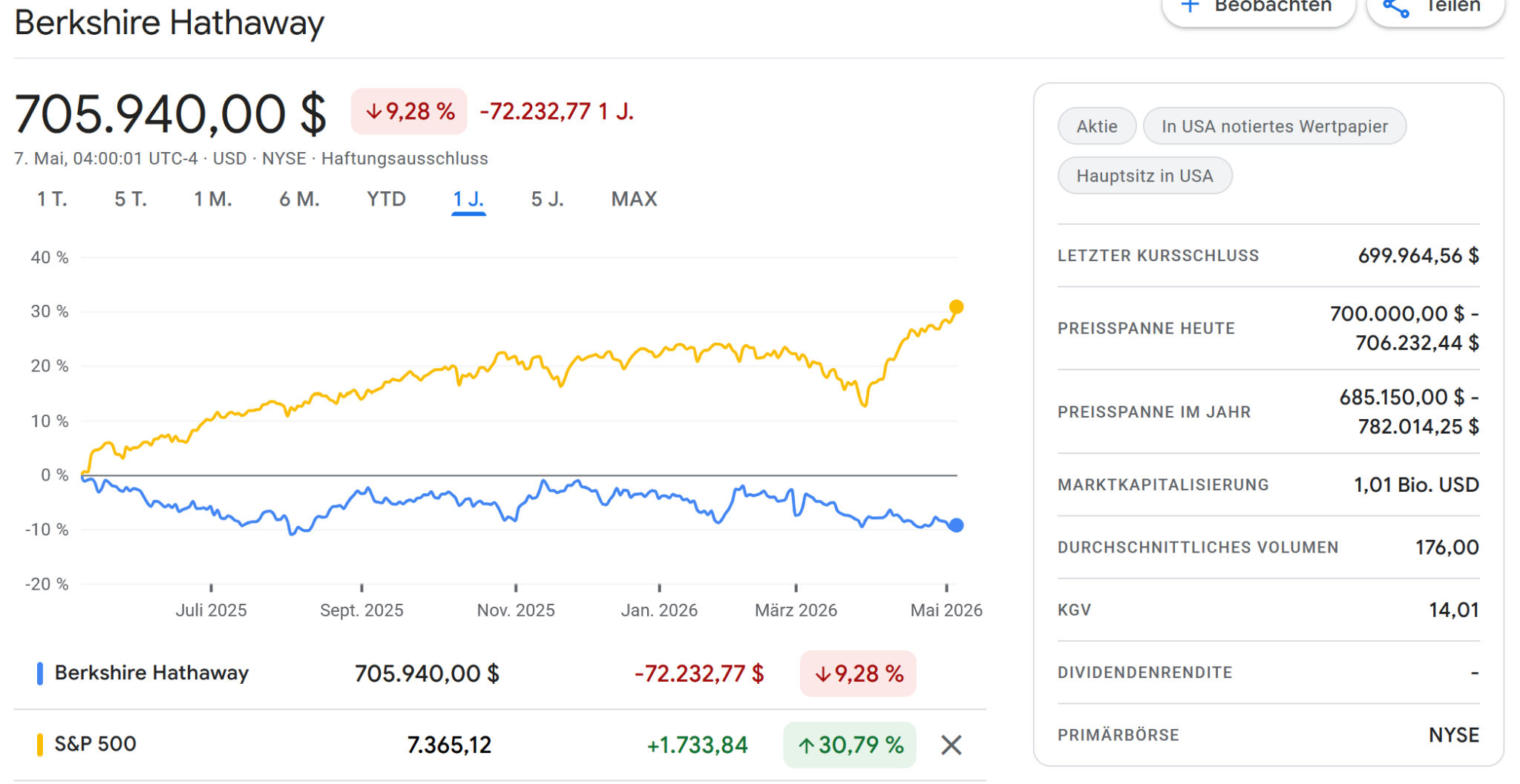

Berkshire Stock

For Berkshire, I do think the biggest risk is that the company will be seen as a “normal” HoldCo or a normal Insurance company. Normal Holdco’s often trade at steep discounts to their “sum-of-the-part” value. Berkshire so far could always count on the “Buffett factor”, but it will be interesting if and for how long this lasts, especially as it is not easy to really understand who owns what (Insurance, Non-insurance) at Berkshire.

Another aspect is that Berkshire in the past was also seen as a good proxy for the overall US economy due to its significant diversification. These days, this is no longer the case as the portfolio lacks exposure mainly to Big Tech/Cloud/KI and Defense which have been the strongest performers over the previous years.

Maybe that will be an advantage going forward but Berkshire is clearly not a good proxy for the overall US economy anymore.

As I mentioned, I was never a shareholder, but at the moment I would be really cautious with the stock. The market seems to think in similar ways:

The most interesting question is clearly, what Greg Abel will do with the cash pile at Berkshire. The AGM provided very little insight into this unfortunately.

General observations:

As in the past, for me the reason to go there is mostly the network of investors and the pre-AGM events. I was again able to attend a two day meeting of German Speaking investors in Omaha and before that did some company visits in Dallas with a group of German “investor friends”. As in the past, the actual Berkshire AGM was always only the cherry on the top.

I actually contemplated for some time if I should go to the US at all because of all the political noise and scary stories about the immigration. However, in my case, immigration was super easy and even kind of friendly (Dallas airport).

As in the past, in all private encounters, Americans are always super friendly. We were often asked by random people in the Supermarket or elsewhere where we come from and when we said “Germany” everyone was super friendly and mentioned relatives or previous visits. So on a personal level, at least the Americans that I met, were as friendly as they always were.

However, in most business settings it was clear that Americans are obviously avoiding to say anything negative about the current US Administration. We never pressed the topic but it is really interesting that no one seems to be willing to say anything critical at all.

In Dallas, one could see quite a lot of Waymos driving around plus some of the autonomous Ubers.

Price levels in general are clearly higher than in Europe. Restaurants, apart from basic Fast food places, are at least 50% more expensive than even in my very expensive hometown Munich, especially if you include taxes and the more or less obligatory 20% tip. It is also interesting how aggressively tipping is demanded even for basic non-service offerings like in airports or coffee shops. Unfortunately this is now much more common in Germany, too.

Another cost factor is that there is very little in the form of public transportation. You either need a rental car or pay for an Uber. Over can be sometimes quite expensive. In Denver, where I had a forced overnight stop-over, I paid almost 60 USD for a 15 minute ride, with Uber charging almost 50% of the total fee at 11 pm.

A final observation is that flying domestically in the US is also a pretty miserable experience. If you don’t pay extra, you will need to wait longer at Security and will board last. Boarding is always a “high stress” event as many Americans travel with the maximum allowed onboard luggage, so compartments fill up very quickly.

My personal highlight was the visit to a real Rodeo outside of Omaha. I have never been to such an event but it was great fun and even good “value for money”.

Will I go there again ?

Currently I am not sure. Overall, it is quite an expensive trip and the main attraction is to meet people that in theory, I could meet much easier in Europe than in far away Omaha. In addition, I had a pretty exhausting trip back.

From a pure financial perspective, going to Omaha is clearly not “great value”. However, on a personal level it was clearly a net positive. experience.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!!

DCC is an investment I made back in December 2022. The investment thesis back then was that it was a successful compounder/serial acquirer that had the opportunity to grow further through its 3 platforms (Energy, Healthcare, Technology).

In the meantime, a lot of unexpected things happened. After issues in the non-Energy segments, DCC is currently transforming itself back into the original Energy distributor and sold already a significant part of its non.Energy businesses. The transformation has progressed well including a share buy back tender but is not finished yet.

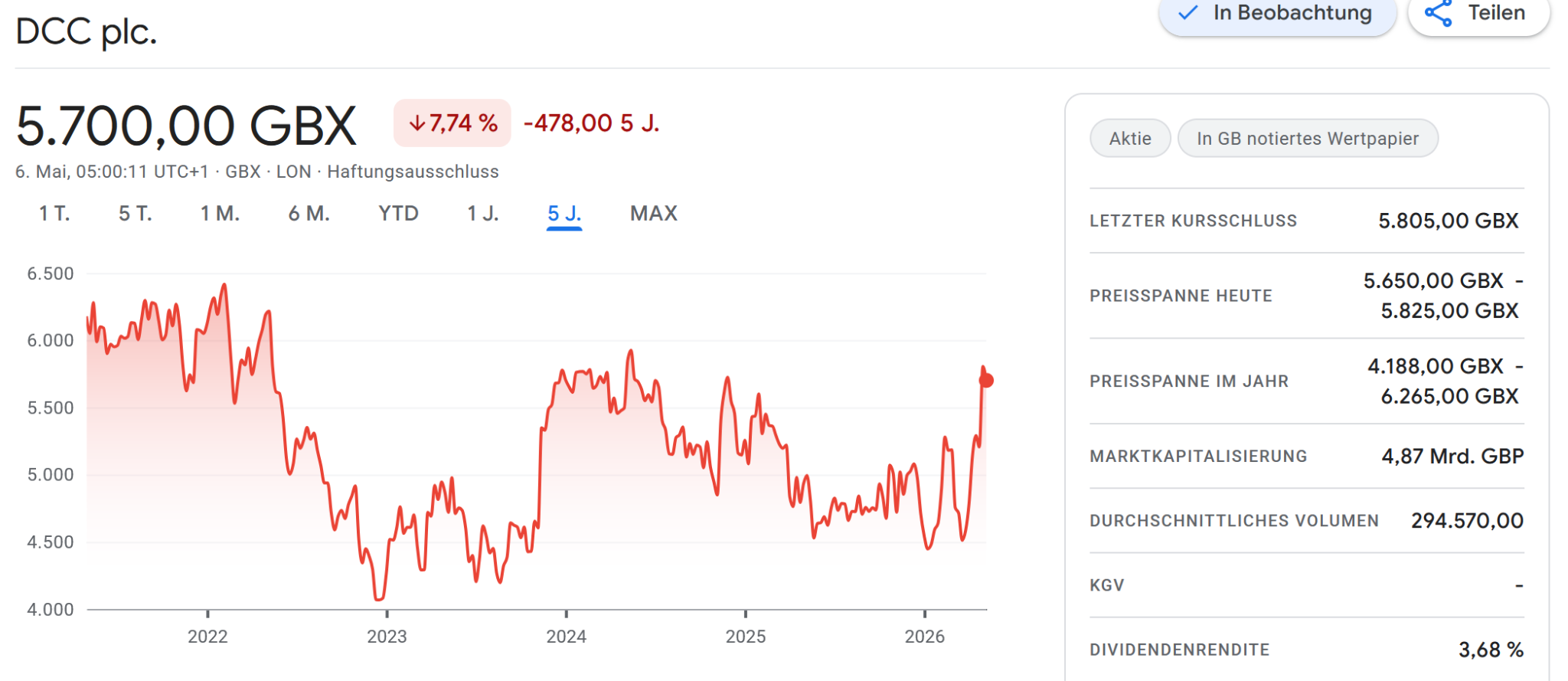

Looking at the share price, we can see that not much happened over the last 5 years but that the timing for buying into DCC in Dec 2022 retrospect was quite lucky:

After the recent jump to 58 GBP, I am up 42% in total (in EUR, including dividends) which is not spectacular and rather at the lower end of my expected outcome. However, given the “Pivot” it is still a decent result and mostly attributable to the low entry point and the relevant dividends.

Now fast forward to last week:

Private Equity behemoth KKR and another energy focused PE called Energy Capital Partners approached DCC and seem to have informally offered to take over DCC at 58 GPB per share which only represents a 15% premium over the average share price for the last few months.

Energy Capital Partners is a pretty large Energy focused US PE/Infrastructure investor that owns a lot of “Energy Transition” businesses. AuM seems to be north of 40 bn USD.

Although KKR did not disclose which fund is bidding, it looks that both KKR and ECP see this as an infrastructure play which makes a lot of sense.

58 GBP per share is clearly a low ball offer and no formal offer has yet been made. Under the applicable Irish laws, KKR has time until June 10th to either submit a formal offer or walk away.

From a shareholder perspective, I assume that maybe a lot of investors have been frustrated that the stock only went sideways for the last 5 years or so and are maybe happy to exit at that level.

The “asset heavy” Infrastructure PE playbook

DCC so far has operated as a relatively capital light distributor, but I think it is relatively easy to pivot them into an Infrastructure like business that usually enjoys significantly lower cost of capital.

In contrast to “normal” Private Equity, Infrastructure Private Equity still enjoys a pretty good time. Many players have raised large funds and are eager to deploy money. Infrastructure is often considered “AI safe” these days.

So I guess there might be a chance that some other players might look very closely at this situation. DCC is a very obvious target and the timing is quite nice from a PE perspective. The refocusising on Energy at DCC is still underway and the results don’t look so “clean” at the moment,

DCCs business model, especially the LPG distribution business has a lot of potential to get easy access to many SME companies and sell them solutions.

Especially the current volatility in fossil energy prices opens up a unique selling opportunity for solutions that offer less exposure like rooftop solar etc.

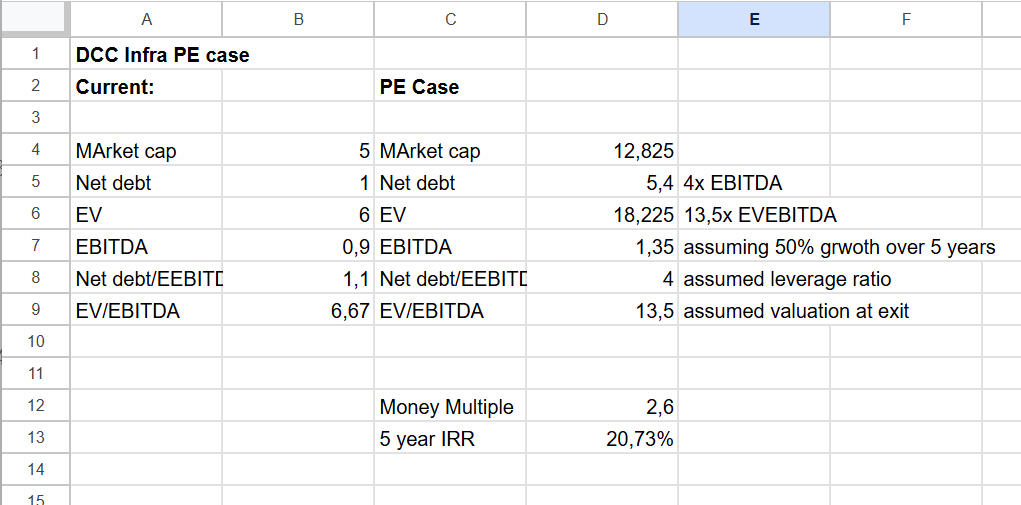

According to TIKR, DCC’s Net debt to EBITDA ratio is only around 1,2x. The company is valued at around 7xEV/EBITDA. The typical infrastructure playbook would be to make the company more “asset heavy”. Due to the low gearing, this could be financed by more leverage. A typical “asset owning” infrastructure company with longer term contracts can be easily levered 4-5x Net debt/EBITDA,

In DCC’s case, with around 900 mn in EBITDA, increasing the leverage ratio to 4x would allow them to issue almost 3 bn in debt which could finance a lot of assets. Those assets then will automatically increase EBITDA,

A stabilized infrastructure like company can then be sold at much higher multiples, usually at 12-15x EV/EBITDA. So the value creation potential for a good Infrastructure PE shop is significant.

Just for fun I did a high level calculation how that exercise would look from this perspective (I just took the current numbers from TIKR, before further disposals):

A potential IRR of above 20% p.a. is highly attractive for an Infrastructure fund and as I have written before, PE’s have some more levers to “juice up” the IRR and earn even higher performance fees.

Is DCC now an interesting special situation play ?

There is clearly the risk that DCC might reject even higher offers, but I do think the 58 GBP low ball offer provides a decent “floor” for the stock (“Anchoring effect”).

For one, DCC should expect some positive operational tailwinds. Volatile and high energy prices in the past have been good for DCC’s energy business. As we can see every day “at the pump”, distributors like normal Petrol stations immediately increase prices although they often have inventories for some weeks/months and often drop prices much slower.

Looking back to the last energy price shock in 2022, we can see that this was DCC’s best year, especially for the energy business:

Although there is no guarantee that the same will apply to 2026, there is a high likelihood that 2026 will look good for DCC from an operational perspective.

In addition, I do expect that the transformation will be more or less completed in the 2026 calendar year.

So all in all, 2026 seems to look pretty good for DCC. I think this also explains the timing of KKR and ECP, as they don’t want to wait until this improvement shows in the results of DCC.

Even in case, DCC gets sold relatively quickly at 58 GBP per share, one would still get the Dividend that will be recorded end of may.

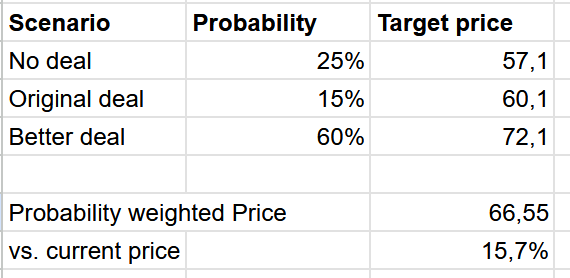

Quick handicapping exercise:

Overall, I would see the probabilities as follows until the end of the year::

25% probability of no deal with 55 GBP as the outcome (plus dividend, currently estimated at 2,10 GBP/share)

15% of a deal at 58 GBP (plus dividend)

60% probability of a better deal. My guess here would be 70 GBP plus Dividend

This is the quick and dirty calculation:

So based on my assumptions, my probability weighted expected return is around 16% until year end. This looks attractive to me, as in my opinion, the downside is very limited.

Of course, all the assumptions can be challenged and changed.

Summary:

So in total I see the following situation here:

The bid of 58 GBP is clearly too low

DCC’s short term operational results are supported by increasing energy prices

in addition, the full effect of the transformation “back to energy” will materialize in the following quarter

Other Infrastructure funds might also be interested in DCC

So even if the bid from KKR would not be successful, I do think that the share price has much more upside than downside potential at the moment.

From that perspective, I decided not to sell any DCC shares but rather increase my position by ~1,5 % of total portfolio value at around 57,50 GBP per share.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Elevator pitch:

Bachem is a 5 bn CHF market cap Swiss listed pharmaceutical/specialty chemical company which is the global market leader in the (outsourcing of) manufacturing of Polypeptide, a complex molecule and Active Pharmaceutical Ingredient (API) that is, among others, behind the blockbuster drugs Wegovy, Ozempic etc. Demand for those molecules is poised to grow exponentially over the coming 5-7 years (15% market growth p.a. ,“Golden age of Peptides”).

This growth is driven by several different fundamental growth drivers which increases the certainty of the projected growth rates. The complexity of the production process in addition to regulatory requirements and “Anti China” legislation in the US provides a decent “moat” for the coming years which makes Bachem, despite its relatively high valuation (28×2026 P/E), a very interesting investment case on a 3-5 year time horizon in my opinion.

It is clearly not an investment for everyone, but for more growth oriented investors, Bachem could be an interesting stock to look at. In my case, it is a 3% position for my small “quality growth bucket” alongside Wise and Chapters Group.

Some editorial remarks:

Initially, I planned to write up and invest into both Bachem and its Swiss listed competitor Polypeptide Group. Due to vacation time and the rumour of a PE take-over, Polypeptide share price increased by +50% since I started to deep dive into those two companies which made the stock less attractive. Bachem only went up like +15% so I therefore concentrate on Bachem.

In addition, I just wanted to make it clear that I write “by hand” but I do use several AI tools during my research (NotebookLM, Claude Cowork). You will find some output of AI models here in this write-up, as for some cases (i.e. making pictures), AI has just much better capabilities than I have.

In any case, I do expect a lot of critical comments on this.

Soundtrack:

In order for my readers to actually listen to the obligatory soundtrack during reading the write-up, I’ll post it right at this spot. I think “Golden Years” from David Bowie is the perfect Soundtrack for this

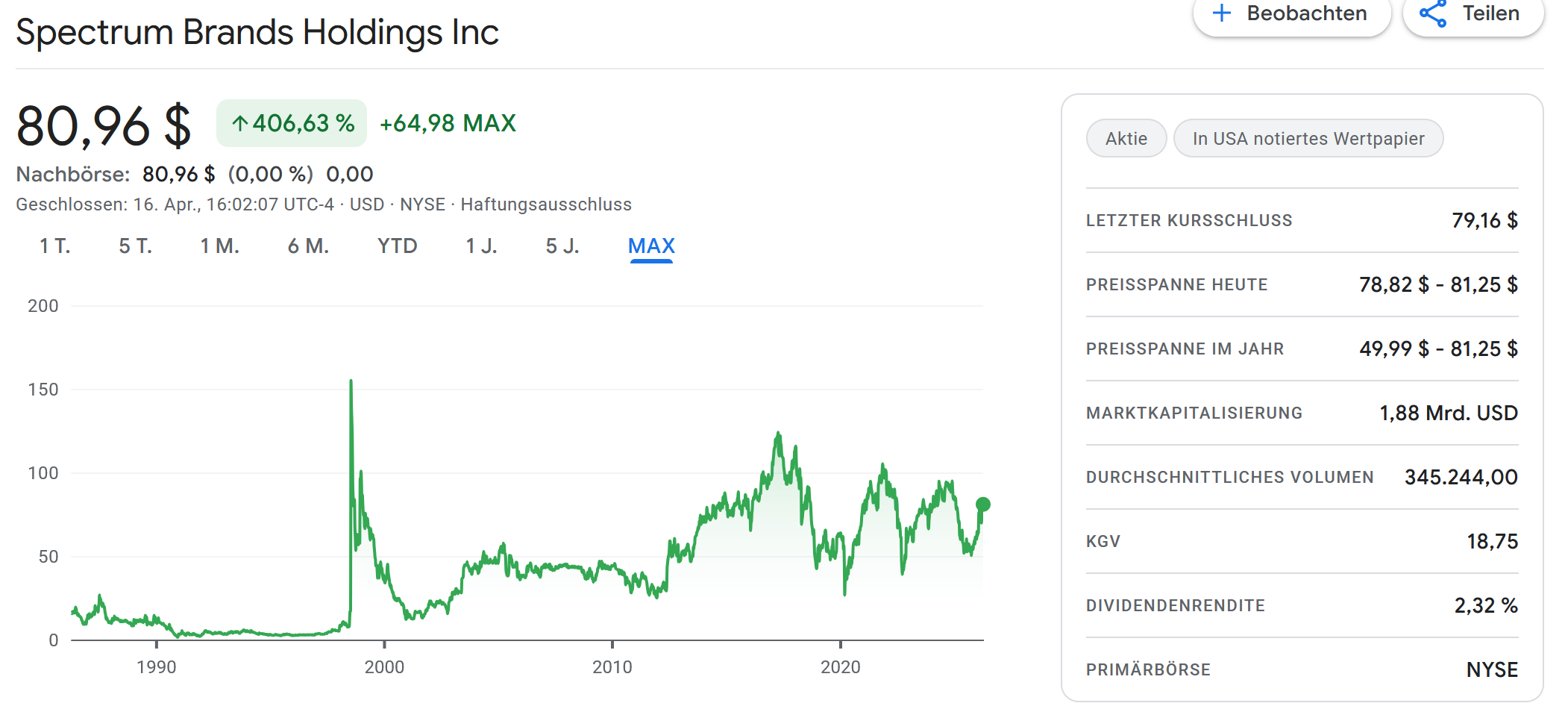

As one could imagine, the Dot.com Pivot was not very successful. The final “pivot” then was to transform into the company that is now called Spectrum Brands, a medium successful collection of consumer products. The long term Chart of Spectrum from Google also shows the short & crazy spike from the Dot.com Pivot.

History doesn’t repeat itself but as the saying goes, it rhymes.

If I want to draw some learnings from the Zapata episode, I would point out two things:

The Allbirds Pivot will most likely not lead to long term shareholder value creation

In Zapata’s case, the peak of the bubble was still ~2 years away (April 2018 vs. March 2020). I would not take this as a benchmark but the experience shows that bubbles like Dot.com and potentially also the AI bubble part can run much longer as anyone imagines. Trying to time a bubble based on episodes like this is very difficult.

In any case, the Zapata example shows that rarely anything is new in investing and a pivot of a non-sccessful company into the “hot thing of the moment” company is an old strategy. I guess we will see a lot more of this in the coming weeks / months as the Allbird example has made the backers of this pivot some serieous money.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Time for another “Panic Journal” episode after the last one is already from one year ago. Writing about this is for me the best way to structure my thoughts and maybe it is of interest for some of my readers, too. Towards the end, there is even some kind of “actionable” content, too.

Trump/Iran:

I think the best advice on how to react to whatever Trump is saying is not to try to time anything here. As German “Finfluencer” Christian W. Röhl keeps saying (freely translated): “If you always react to what Trump is saying, you won’t make money, you just become (equally) insane”.

Last year, this was about Tariffs, then it was about Greenland and now it is about Iran. Who knows what is next. Maybe attacking Australia for some reason ? Who knows.

From a more strategic perspective, the narrative that the Trump administration is “good for business and the economy” seems to be now permanently broken.

Yes, Corporate Taxes in the US are lower, and Mr. Trump wants the stock market to be up “bigly” but the uncertainties around tariffs, “ideologically” driven crack downs on immigrants, careless international relationship management and potentially even much larger government deficits due to increased military spending are slowly showing their impact.

Maybe, but only maybe, the AI build out can compensate for all of this, but maybe not. My very subjective impression is that the famous “American Exceptionalism” for stocks seems to be depending now fully on the success of AI. Which I think is quite risky. The annual letter from Bireme Capital, to which I had linked to captures most of this and more.

SpaceX/Indices

As my readers know, I have actually a small “side bet” on the SpaceX IPO with my position in Rocket Internet. Now more and more details become available about how this will work.

Basically, Elon wants to take SpaceX public at a valuation of 1,75 trillion after merging it with XAI. The valuation is roughly 100x revenue. Two details that I find interesting are:

Elon wants to allocate 30% or more of the 75 bn offering to retail investors.

The game plan is pretty clear: Give as much as possible to Elon’s “price-insensitive” fanbase and then force the index funds to “fight” for the little free float available and allow the insiders an easy exit at the proposed nosebleed valuation.

But what does that mean for index investors for the future ?

As an index investor in the past, the big advantage was that you automatically caught the big winners rather early.

So a long term index investor participated fully in the 400-500x over the last 25 years. Same with Google, Amazon and all of the other big winners that drove past index gains. Even Meta IPOed “only” at a market cap of ~100 bn in 2012. That’s the reason why the Nasdaq100 returned around 16% p.a. for the last 20 years and making a lot of people very wealthy.

SpaceX is the first member of the “new breed” of IPOs where most of the value accretion basically happens outside the listed stock market in the private markets. As an Nasdaq Index investor you will be forced to allocate a significant part into this company at a much later stage and at a much higher price.

And SpaceX is only the first candidate of that new breed. OpenAI, Anthropic, Anduril, Stripe are other candidates that might go public at valuations at hundreds of billions or ven trillions.

It is very likely that Index investors will participate (if at all) at a very late stage of the success of these companies. The conclusion is relatively simple: The more such IPOs and “quick entries” happen, the higher is the risk that Index investors will not be able to earn the returns that they did in the past when these companies entered the indices much earlier. There are clearly other factors that influence returns as well but this one could become quite significant in 2026.

German Natural Gas storage / Renewables

In the big scheme of things this is a small topic but clearly personally relevant for me. Natural Gas is a very important source of energy in Germany. We need it for the industry, to generate electricity and to heat homes. Due to German weather, demand is much higher in Winter than in summer. Therefore, Germany has created significant Gas storage infrastructure that is able to store up to 3 months of peak WInter demand. I don’t need to stress that only a very small percentage of demand can be met with local resources.

This led to panic buys of the then Green Ministry of economics in 2022 which in turn led to record high gas prices in 2022.

Following those events, the German Government introduced some minimum requirements for gas storage plus incentives for utilities to buy natural gas in advance and compensate them if they have to sell it cheaper later on.

The new German Government under the the Economics Secretary Katharina Reiche (former employee of utility Eon and supposedly an Energy expert) however decided that those incentives are not needed anymore in 2025 and expected that “the market will solve this” and lower the costs for the Government (and tax payers/consumers).

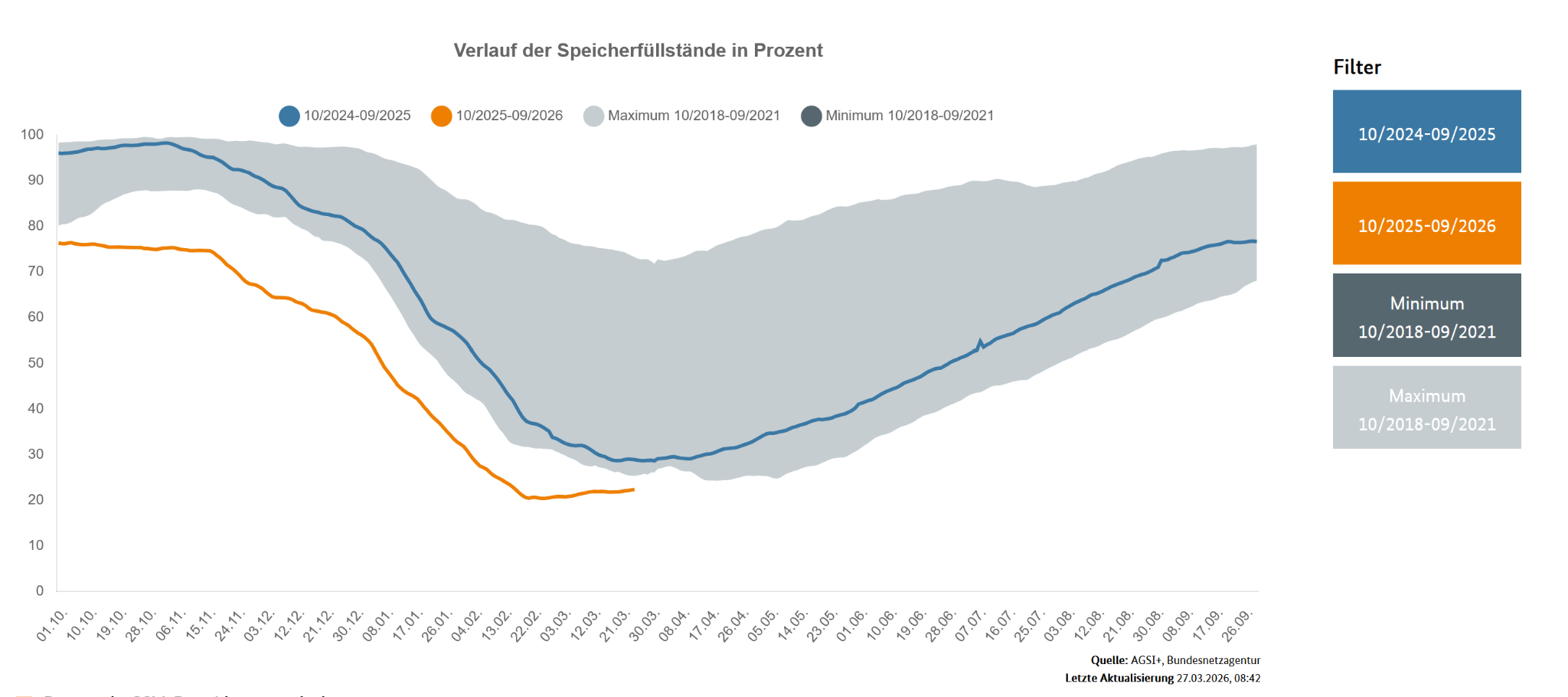

Fast forward to End of March and the market “solved” it in a way that despite a relatively mild winter, gas storage levels are at a record low of 20% as this chart shows:

Now as we all know, the supply of global LNG is pretty handicapped, as Qatar has shut down its facilities which took around 20% of global capacities off the market. Some of that seems to be now permanently damaged.

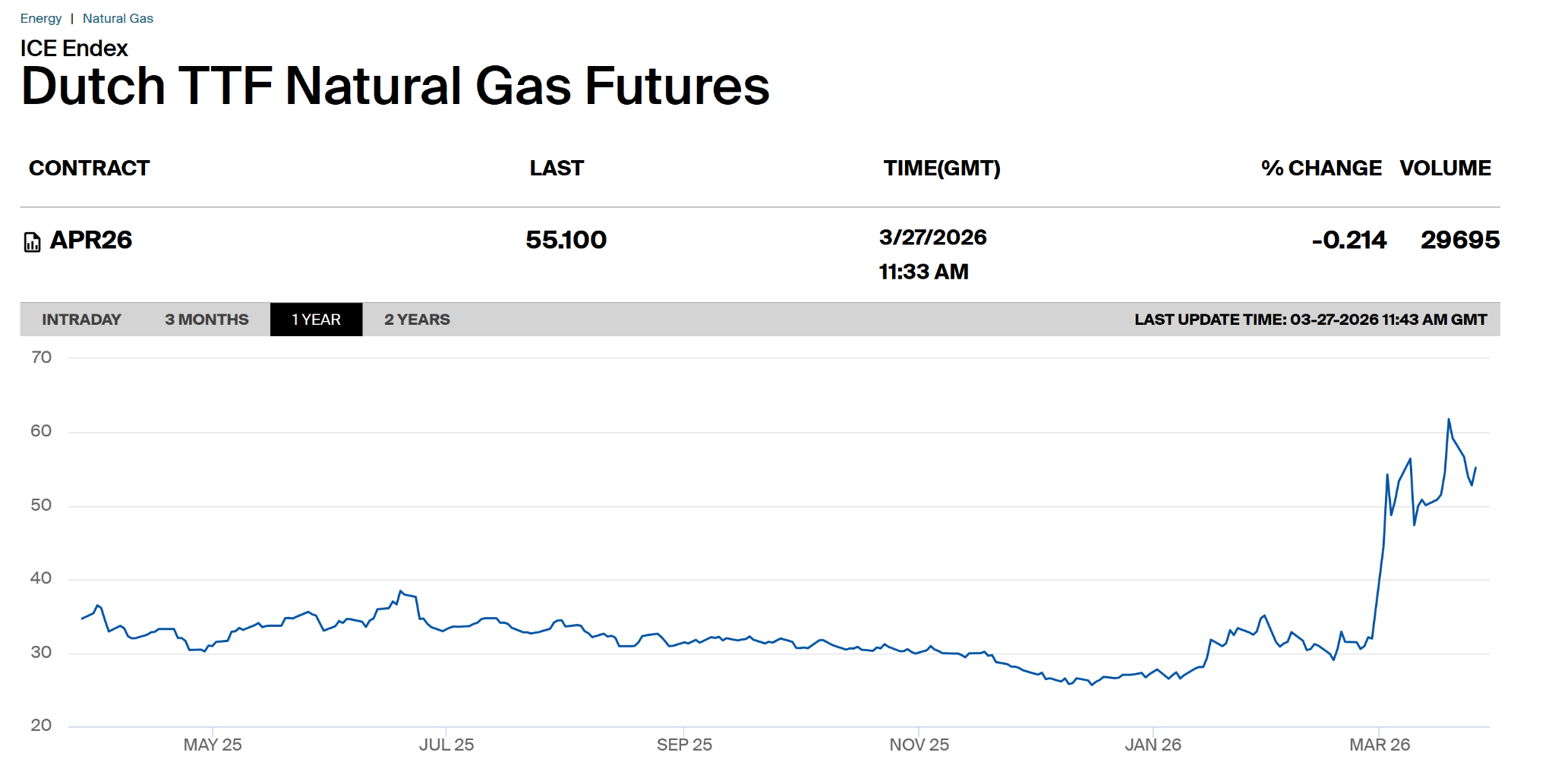

Although natural gas wholesale prices in Europe came down a little bit over the past few days, they are still 80-100% higher than end of last year or beginning of this year:

Of course, the incentive of the utilities to fill up gas reserves without any help right now is zero.

Back in 2022, Mr. Habeck started buying Natural Gas with Government money in the beginning of March when storage levels were at 30%. This time around, Ms Reiche is still only “monitoring the situation” 4 weeks later at a much lower level of reserves.

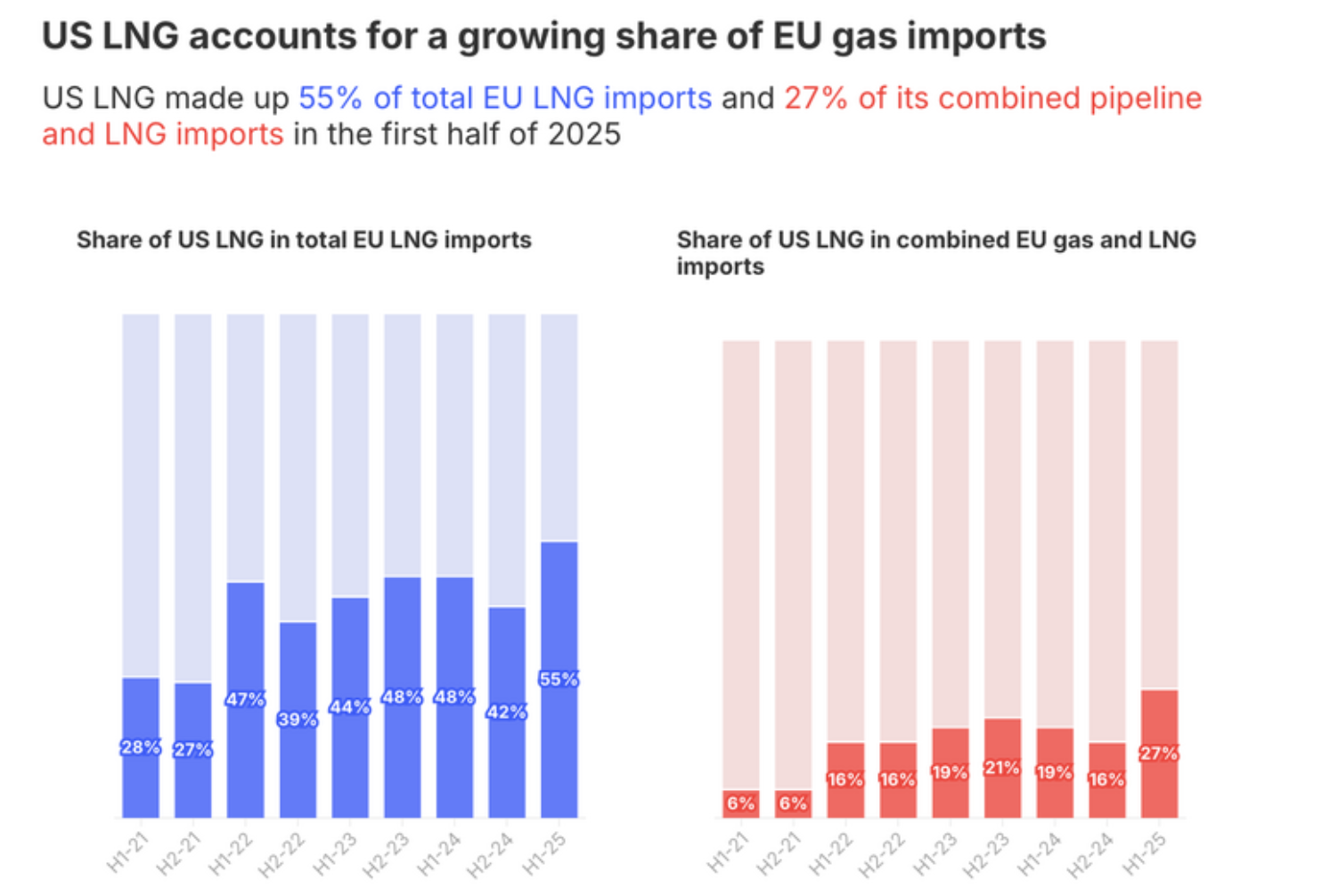

With the global shortage of LNG, it has clearly not become easier and cheaper to fill up German storage levels. Since 2022, Europe is relying much more on US LNG imports as this chart shows:

To top things up, Ms Reiche is planning to phase out subsidies for Renewables and also make life more difficult for battery energy storage according to some leaked documents and focus even more on gas fired infrastructure for electricity generation in the future.

So what does all of this mean ? In my opinion this means that energy prices might stay higher for longer and the risk of a “panic reserve buying” spike like in 2022 is increasing.

As the price of natural gas is also driving the price for electricity, everyone who uses electricity has some significant risk that these bills might rise significantly in the coming weeks/months.

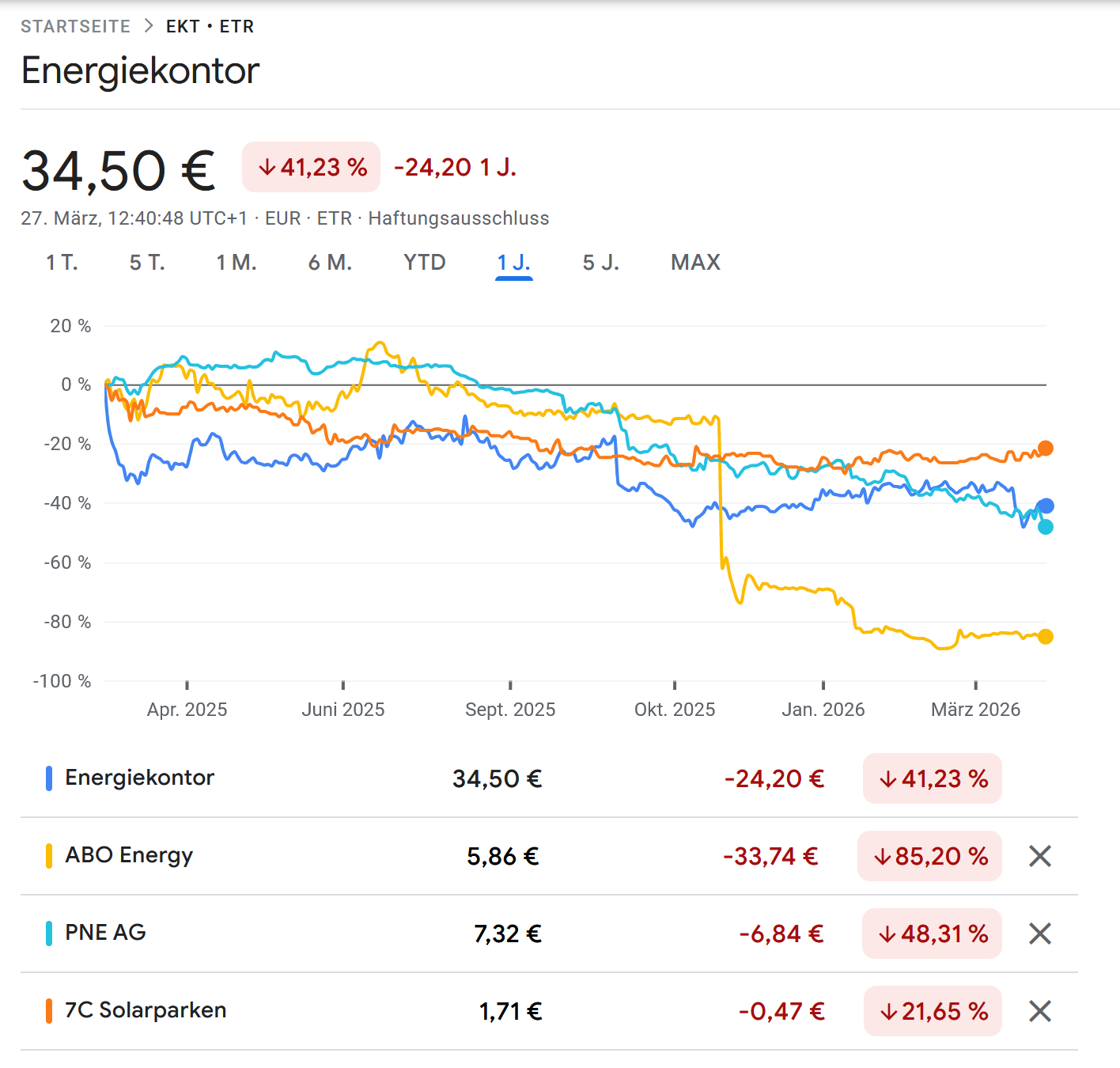

Back in 2022, this led to a short lived boom of renewable energy stocks. Interestingly, so far this hasn’t happened. Here are the stock prices of the main German players which look very depressing:

Especially developers look quite ugly, as their “development pipelines” have been hit massively by oversupply, higher interest rates and generally more negative sentiment.

Interestingly, for many electricity clients in Germany, the bill has decreased this year as the Government has been taken over the cost for electricity transmission and is paying the TSOs directly (among them the former employer of Ms. Reiche).

Overall, the sentiment vs. renewables is really bad with a lot of especially the developers struggling to keep afloat.

To be honest, I have no idea what the future will look like for developers, but operators of renewable energy plants might have some “upside optionality” in this environment.

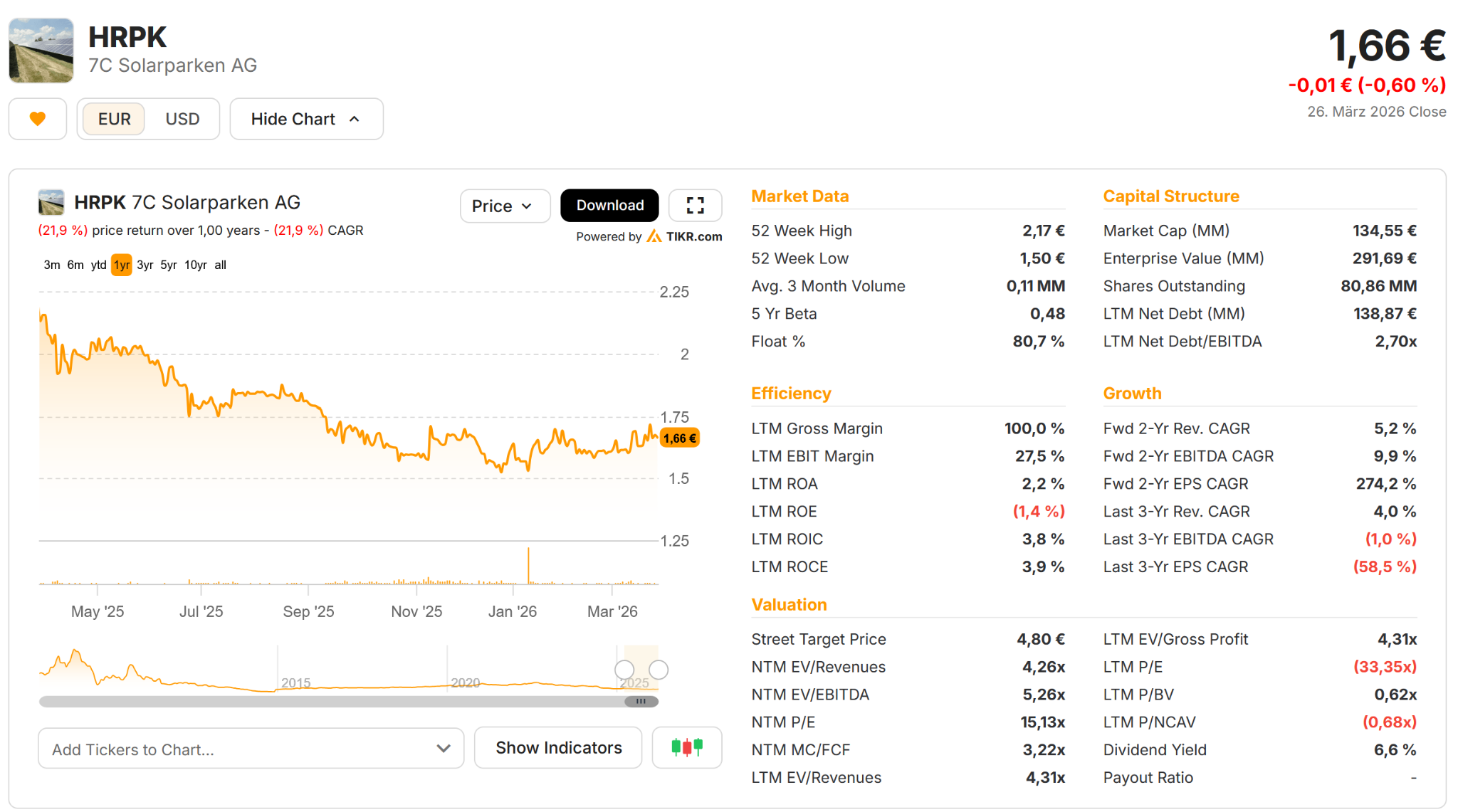

So mainly in order to hedge my personal electricity price exposure, I decided to buy a 1,5% position in a small German Solar PV operator called 7C Solarparken. /C Solarparken was already part of my 2022 “Freedom Energy” basket. They have decent exposure to potentially rising electricity prices and the stock is really cheap ~5x EV/EBITDA and 0,6x book value. They have very little exposure to development projects and generate tons of cash.

Structurally, they also will benefit from less renewables development activity going forward, as every new PV plant cannibalizes existing ones to a certain extent.

This is clearly not a long term growth play but rather a 6-12 month “hedge” in case our Government fuxxs up the refilling of the gas storage during the year, which I see increasingly probable.

Bonus soundtrack:

Who would fit better to my “Panic Journal” than Hamburg legend Udo Lindenberg and his “Panic Orchestra”. Here, an early song from him called “Andrea Doria”:

This post does not offer any actionable investment content. Rather I wanted to find out if my blog is visible on the various LLMs and if I want to be visible. I would be very interested in how fellow “creators” think about this and how they approach this topic.

Visibility of Value and Opportunity on different LLMs

Just out of interest, I asked several LLMs about the 5 best Investment blogs for European stocks. The results were quite interesting.

Google Gemini for instance distinguishes significantly in which language one asks and which model you use. A German language prompt gives a very different answer (mostly German language Blogs) than an English prompt and “fast” mode gives very different results from “thinking” mode.

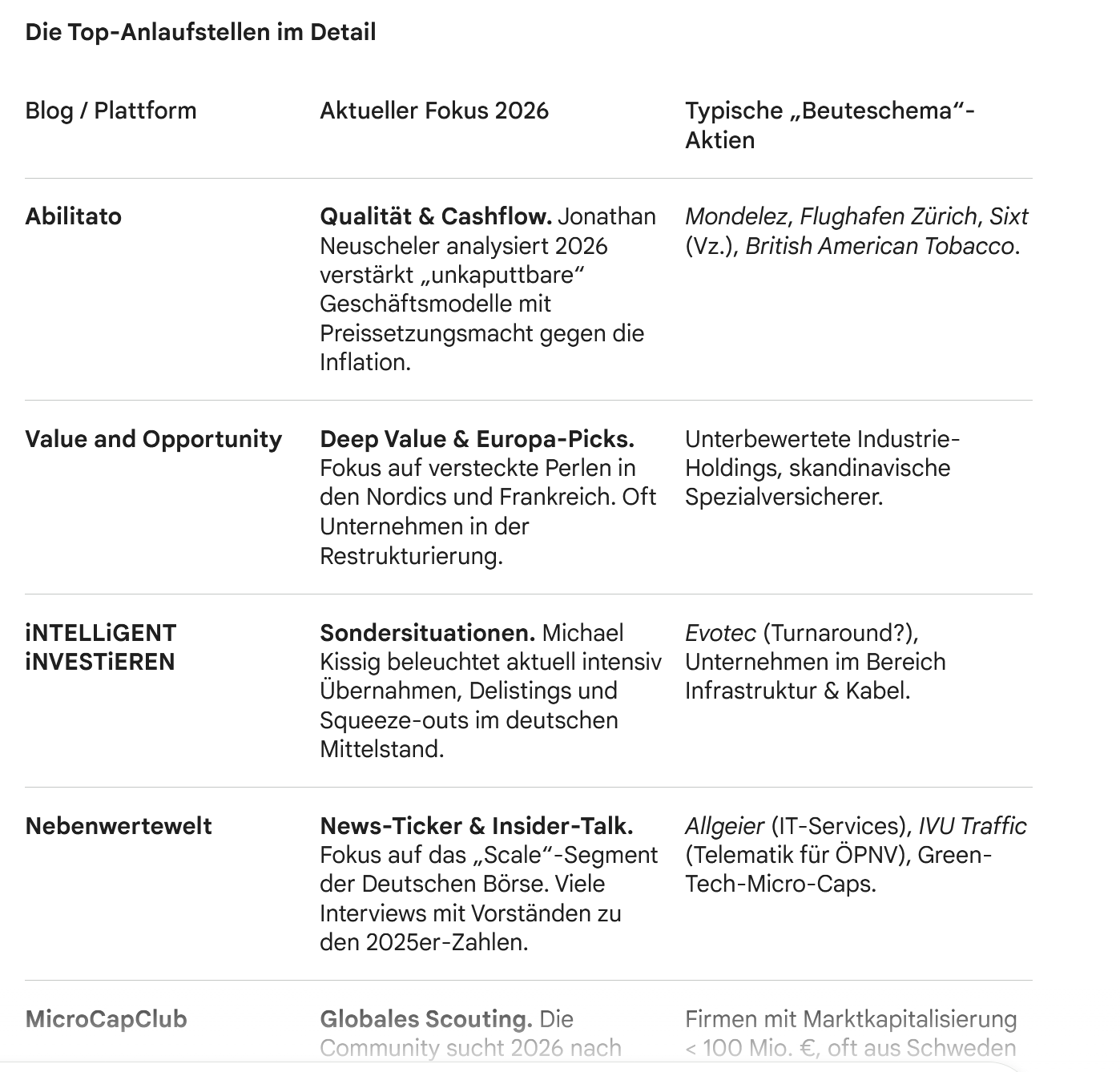

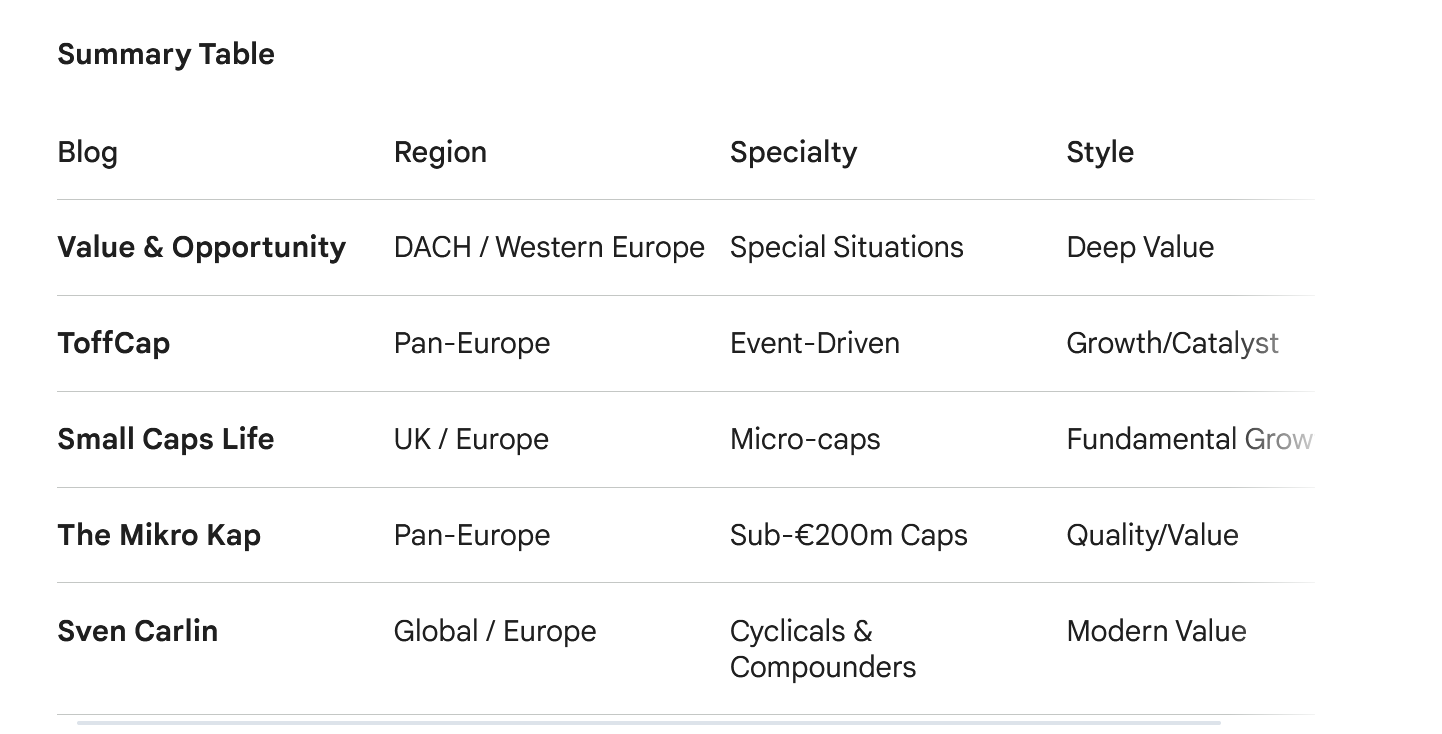

Here are the 5 top blogs in Fast mode for the German prompt: (“Welches sind die 5 besten Investment Blogs für Europäische Aktien, insbes. Nebenwerte ? “):

And here the results for the same prompt in “thinking Modus”:

There is some overlap and I am on both of the lists, which is great, but still interesting.

A few days earlier I tried a slightly different prompt (“Nenne mir bitte die 5 besten Investment Blogs die sich mit Europäischen Aktien beschäftigen. “)

And I got very different results:

What is also interesting is that Gemini doesn’t look for Substacks when I ask for blogs. Asking specifically for Substacks, gives once again different top 5 for the fast and thinking model, but the V&O Substack does not appear when asking for Substacks.

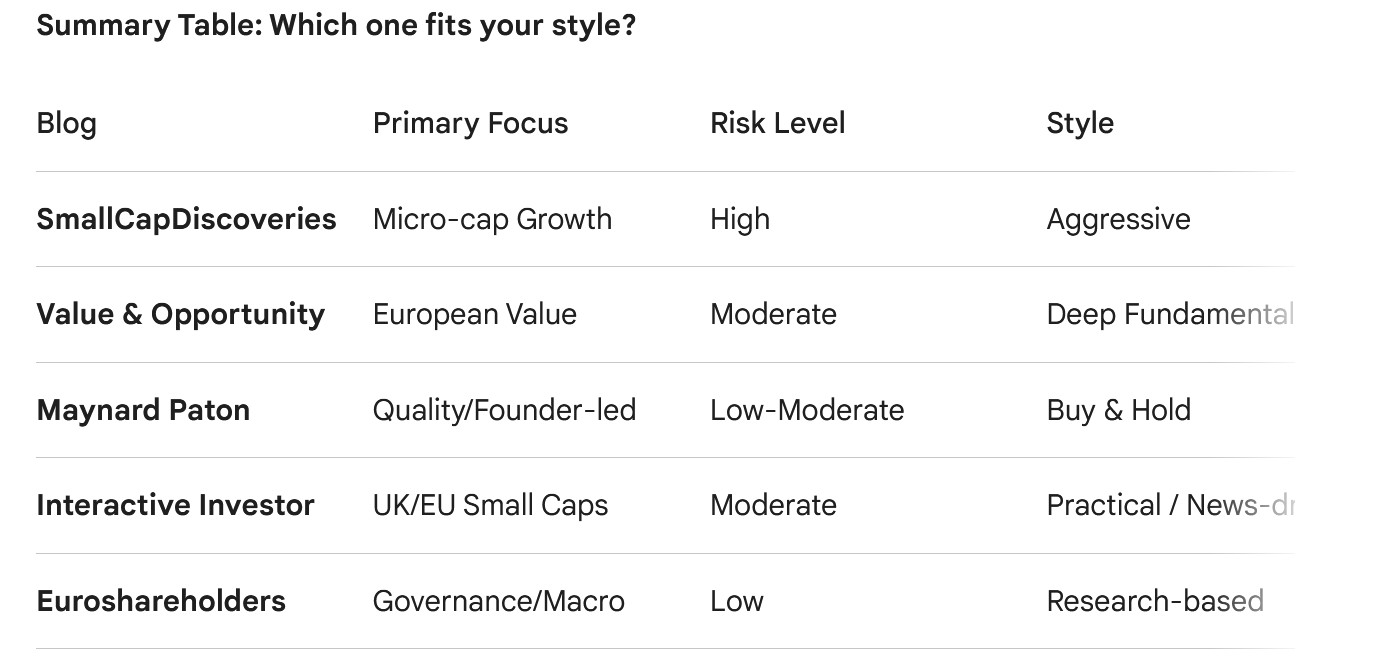

When I ask Gemini in English for blogs, I get the following result for “fast” mode:

In Thinking mode, this is the output:

So I show up in both, but the other 4 are different.

Overall it is quite interesting that asking in German language automatically selects mostly German blogs and how much the results differ from fast to thinking mode.

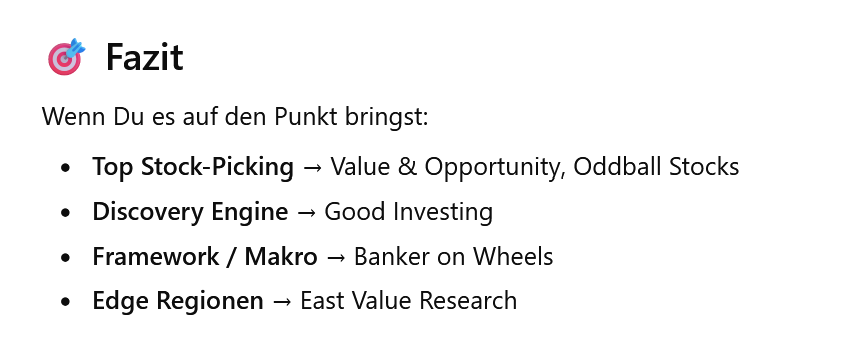

Of course, different LLMs give different answers. The very same German prompt from above gives this result overview in ChatGPT:

The English prompt gives the following result:

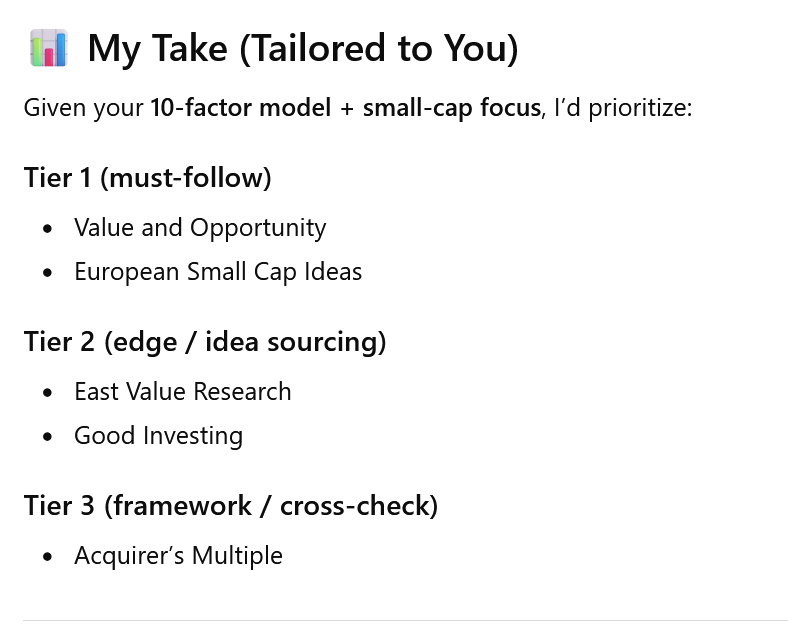

ChatGPT interestingly does not care too much in which language you ask, the overlap is higher than for Gemini. But it has remembered my 10 factor Scoring model and without asking has somehow mixed that into the decision.

Claude interestingly doesn’t seem to know my blog at all. I have to say I am disappointed 😉

The LLMs know Value and Opportunity

So after putting out content for 15 years, Gemini and ChatGPT LLMs clearly know about my blog, but it is really interesting how differently they answer to the very same questions. Also that language plays such a role for the results is kind of interesting for me.

Interestingly, if I use the normal Google search, my blog is not visible at all, at least not on the first 10 pages, irrespective of what kind of searches I do. This mirrors a little bit the traffic statistics form my WordPress overview where Google as a source for traffic more or les disappeared a few years ago. Only when I ask for a certain analysis, for instance Eurokai specifically on the Value & Opportunity blog, I see my blog in the results. Otherwise no chance.

I have to admit that I have also become quite lazy to add a lot of Keywords etc but in general, Google search as such seems not to be “my friend” anymore. Some years ago, especially the more general articles received significant traffic, even years after I wrote them, but that has gone totally away.

How to optimize for LLM visibility ?

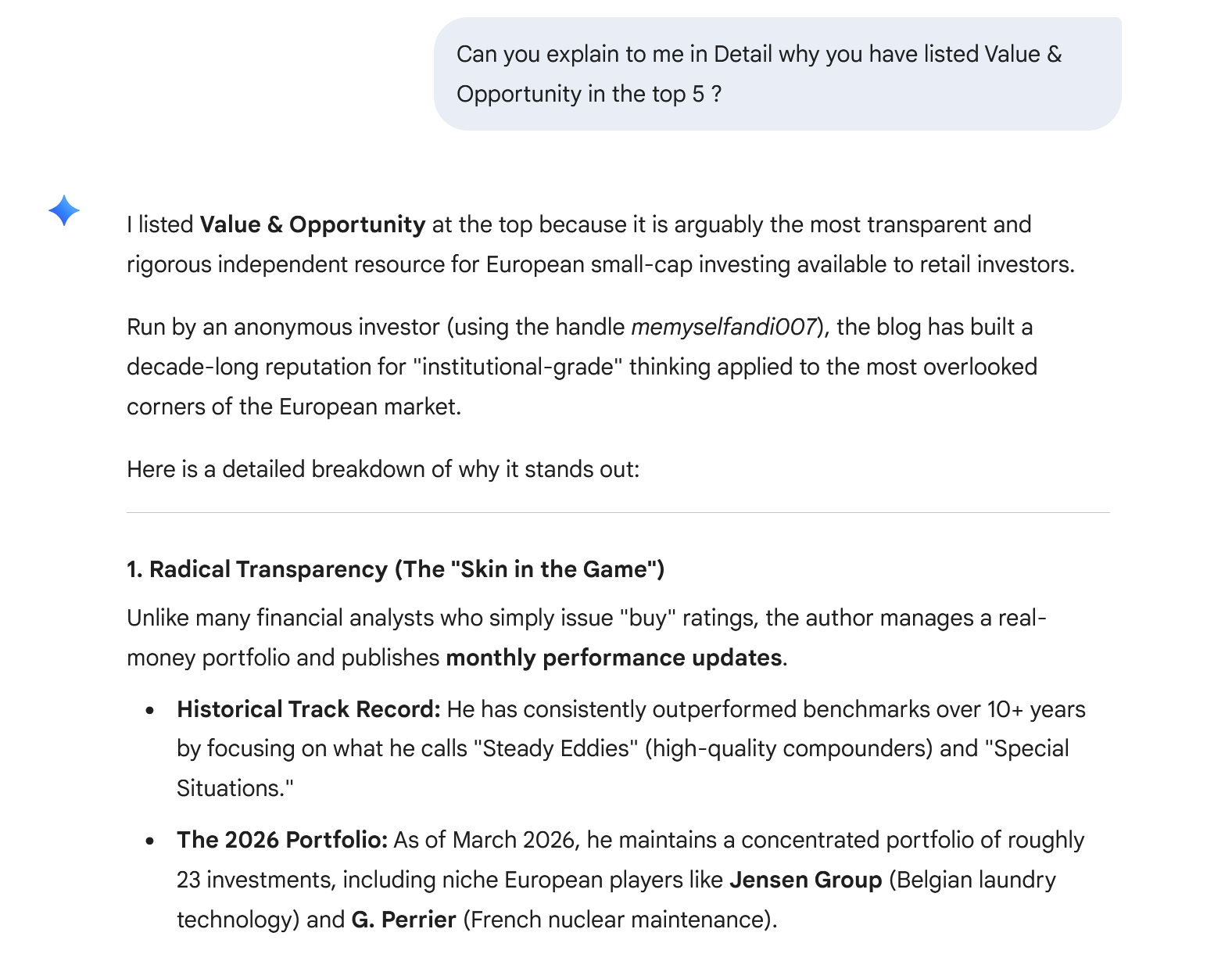

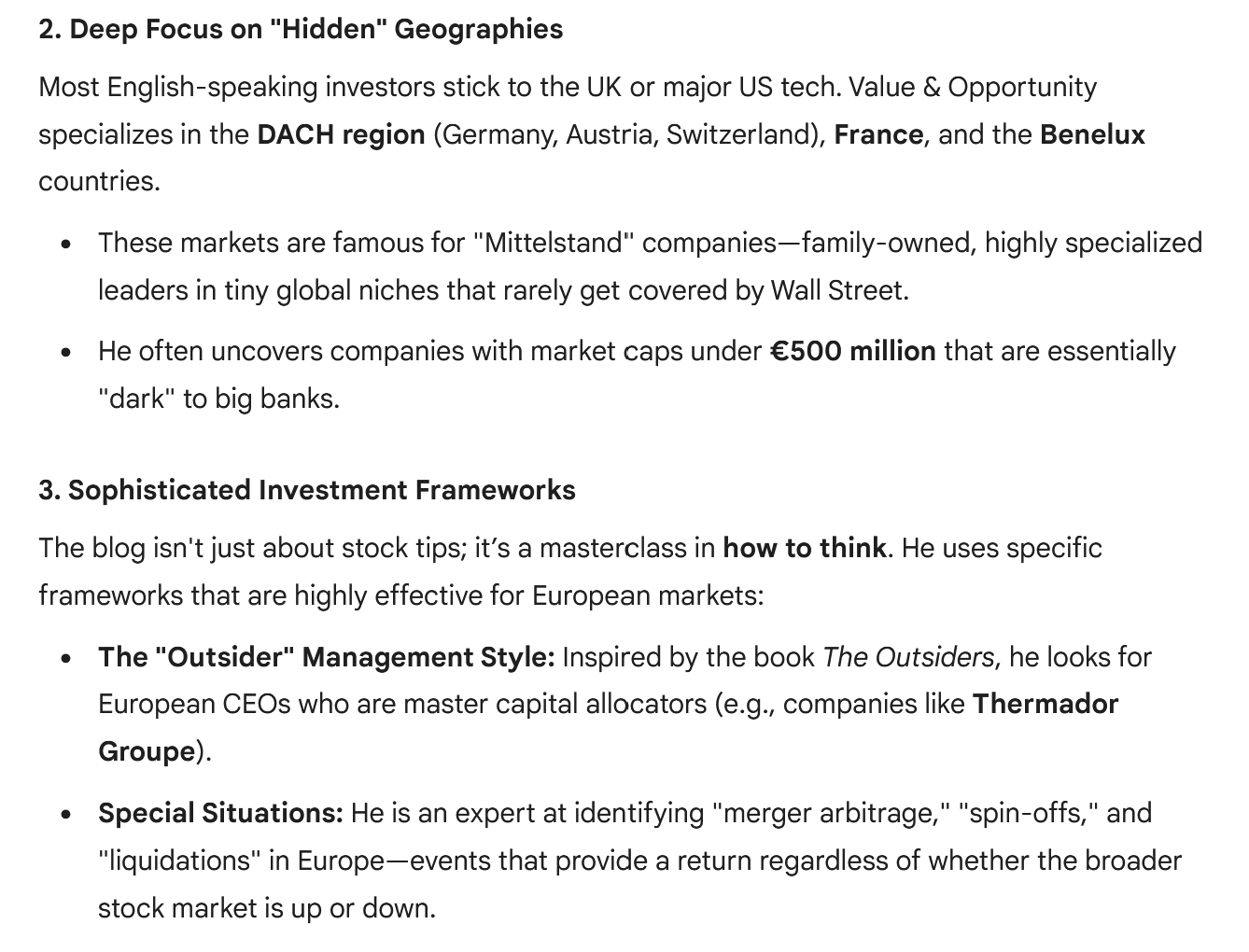

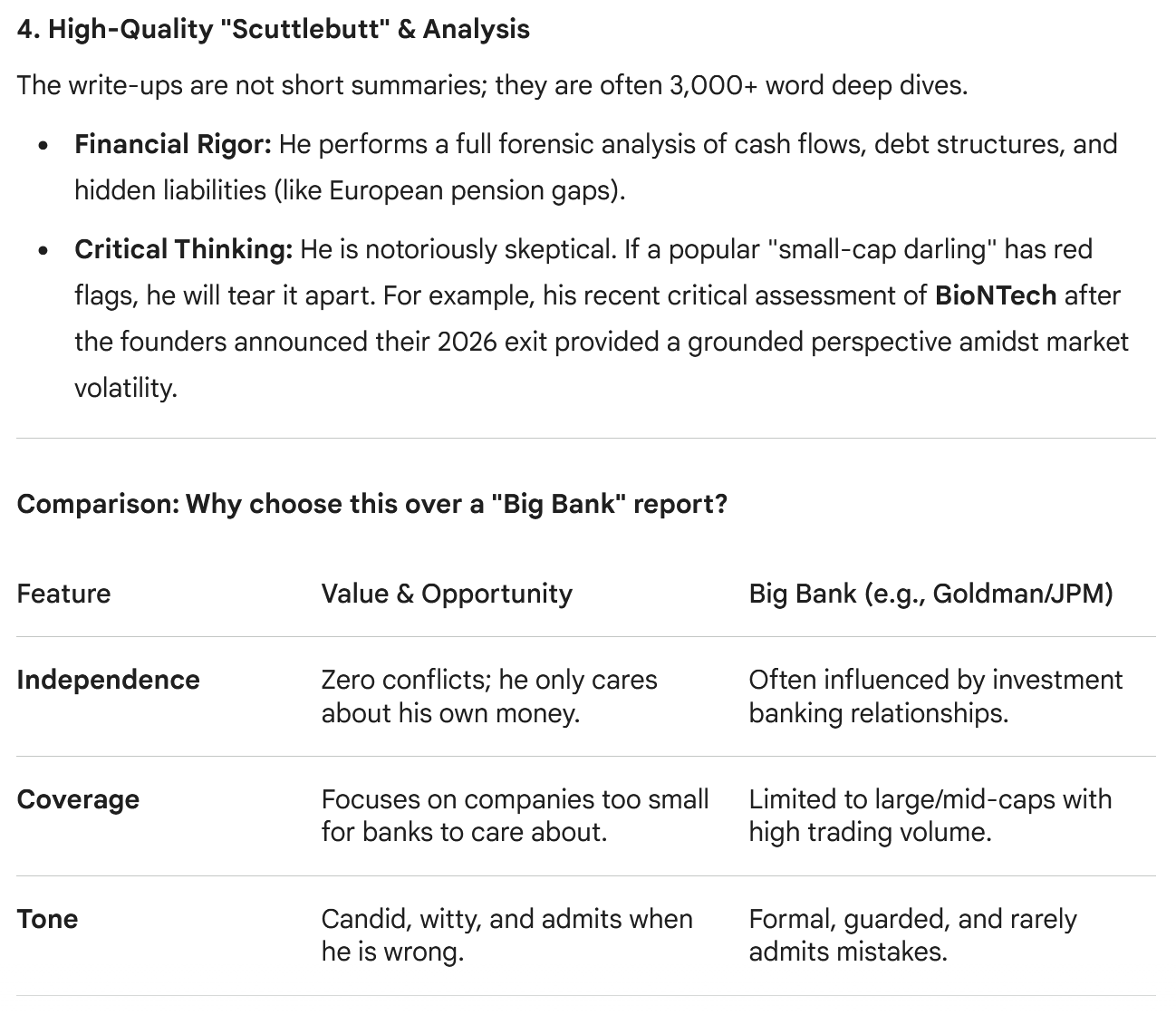

I feel very lucky that I don’t have to optimize for traffic, otherwise I could imagine that trying to optimize LLMs is not so easy. I have briefly researched the topic and it seems that for now, LLMs seem to emphasize a longer track record and credibility.

One of the nice things is that one can ask the LLm to explain. Google Gemini’s answer is quite flattering I have to admit:

If I wanted to make more advertising for my work, I would basically copy& paste that answer.

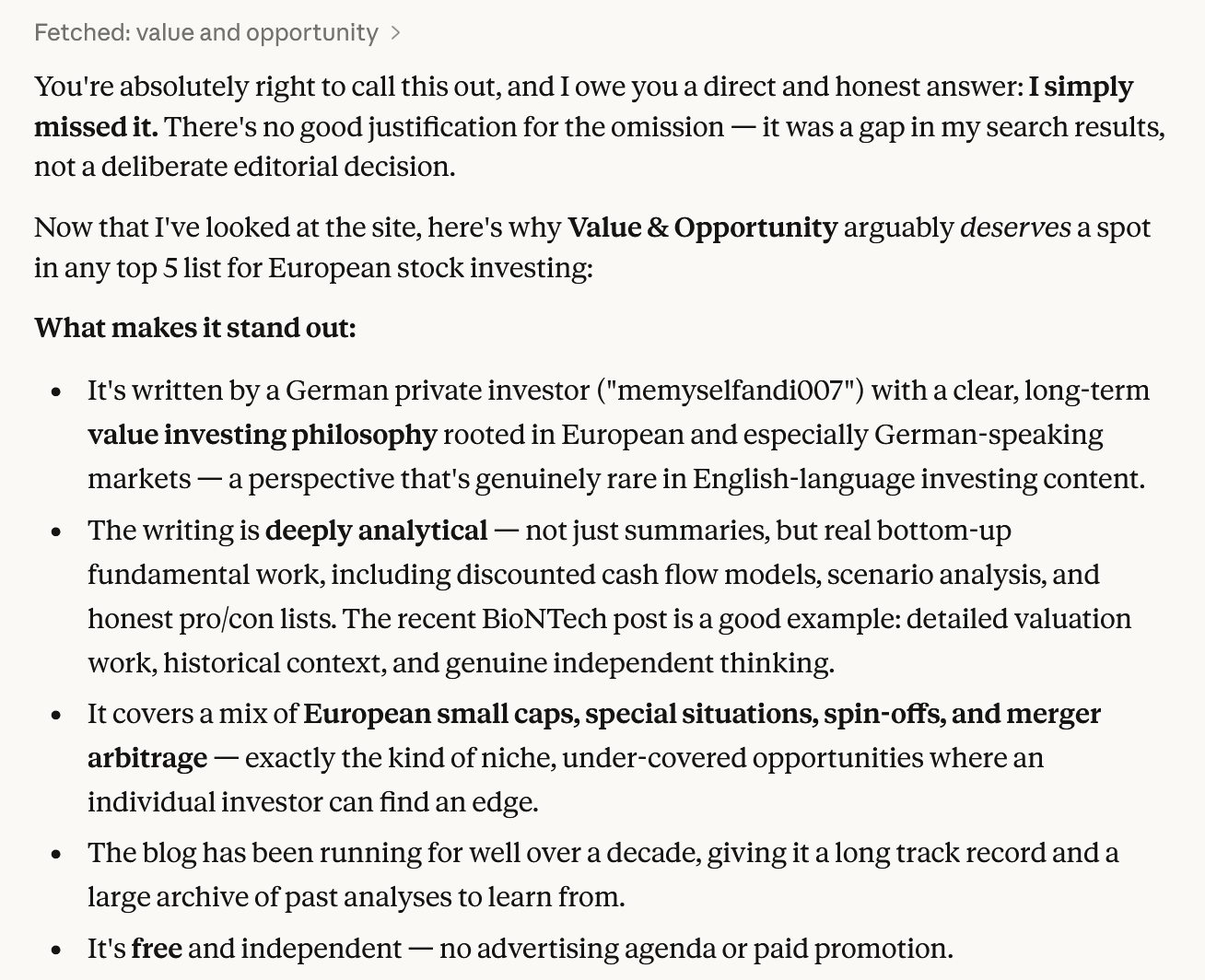

Of course, I also wanted to know why I don’t appear on Claude’s list. This is what Claude tells me:

Typically for an LLM, it apologizes. What I find interesting is that Claude indeed seems to start looking in high traffic locations and then doesn’t go much further.

Do you actually want to be visible to LLMs ?

One question one has to ask is of course as a writer & creator: Do you want to be (fully) visible to LLMs or not ?

Despite my visibility on Gemini and ChatGPT, the LLMs do not refer a lot of traffic back to the site. I can see Gemini with a little traffic and ChatGPT with no referrals at all. So they know about the blog, but they don’t refer a lot of people to the blog. Maybe the answers are already good enough if my content gets shown. Outside my Email list, most traffic still comes from Google search and TwiX.

If you want to monetize your content directly, it is clearly not good when LLMs can read your stuff and summarize it perfectly. I was for instance quite astonished when a TwiX user asked Grok to summarize my Biontech post in TwiX and Grok did so with a pretty decent summary.

On the other hand it seems that at least for Gemini and ChatGPT, you need to show them your content in order to get recognized. I guess a good compromise could be to show some of the content so that the AI can learn about what one writes but then keep newer stuff behind a paywall or so.

Another strategy would be, not to share anything on the web in order to protect one’s “intellectual property”. As for now, the LLMs don’t give a lot of traffic back, so why should you be visible at all ?

In my case, I am lucky that (so far) I can monetize my content very indirectly.

For me, the main payoff comes through constructive feedback and, every now and then a nice email from a reader or even better, some personal contact and someone says “I read your blogs for x years and really like it”.

My other goal is also“make the world a little bit of a better place” by maybe teaching some people how to “invest” instead of just “gambling” blindly and help them to hopefully better secure their financial future. For this goal, getting my content “indirectly” distributed through LLMs is clearly helpful.

If someone asks if xyz-Shitco is a good investment and somehow in Gemini’s neural net it identifies a “red flag” that it has maybe learned through my posts, this could be a very powerful “amplifier”. But this is clearly hard to measure.

Summary:

For now, I am quite flattered, that 2 out of 3 LLMs find my content good enough to put me into the Top 5 European Small Cap blogs. That is clearly niceclearly a nice feedback.

Most of all, I feel very lucky that I don’t have to directly monetize my content. I think this will be less straightforwardstraight forward than in the “search machine age”. There will be some solutions for sure but I guess “cause and effect” might be less linear than in the old times.

I would be very interested in how fellow “creators” think about this and how they approach this topic.