Updates: EVS Broadcast, Jensen Group, Wise & Installux

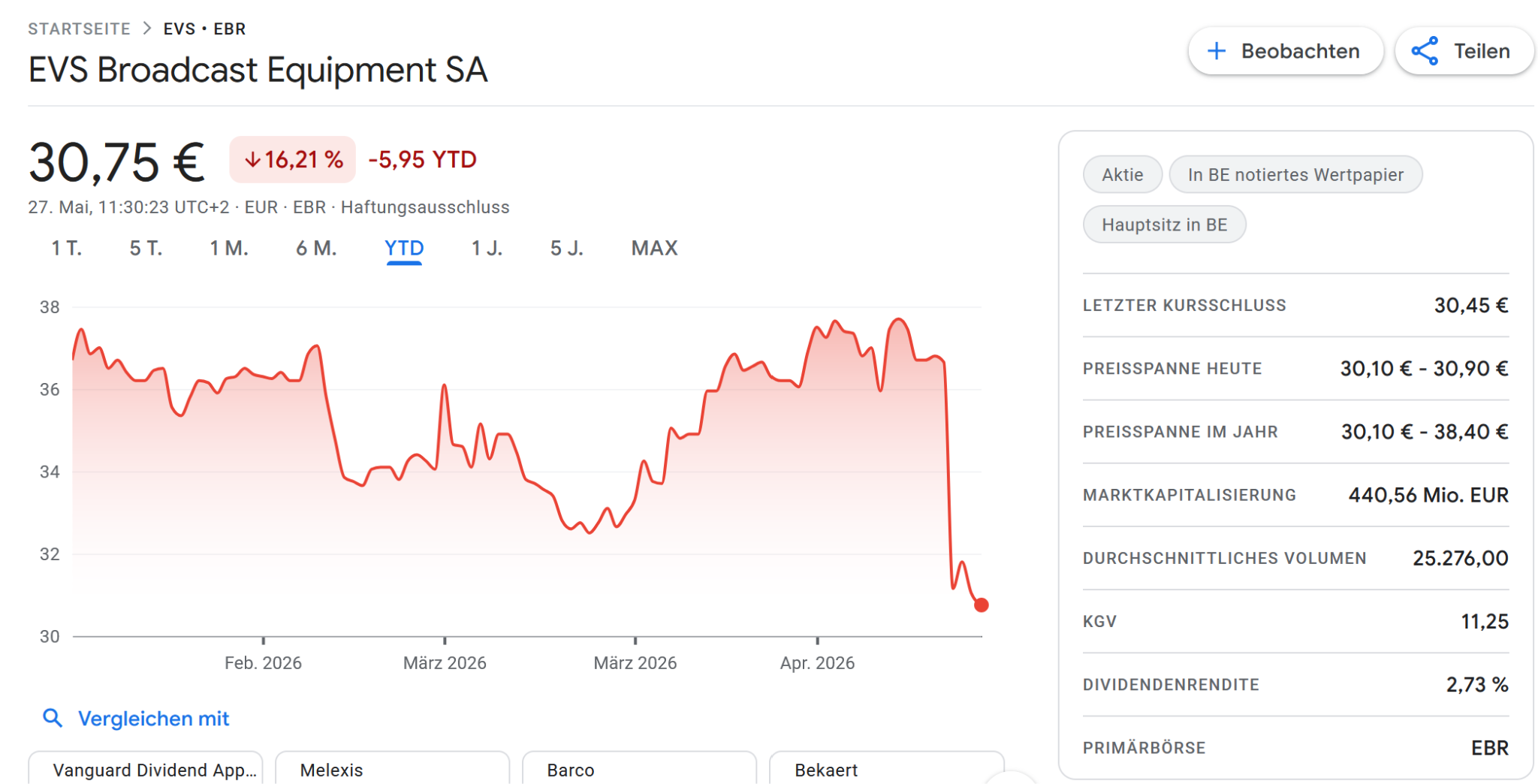

EVS Broadcast

Let’s start with the most disappointing update first: EVS Broadcast got slammed down after their Q1 trading statement:

I think three items spooked investors, including myself:

First, after confirming the guidance, both in the CEO and CFO statement, the press release suddenly contains this sentence in the Outlook section:

“In particular, the current situation in the Middle East may affect full-year revenue performance and could lead EVS toward the lower end of the guidance range. At the same time, given the strength of the pipeline and the opportunities currently identified, we believe there remains potential to offset this impact through execution in other areas of the business. “

Second, once again they mention that the 2026 year will be “back loaded”, i.e. investors will have little visibility how things will develop until the end of Q4.

And finally, the departure of the CFO lady without a direct replacement is also not optimal. I guess there has been some tension in the board.

Longer time EVS shareholders know that they always guide cautiously, but 2026 as an “event year” should have been a very good year and now it looks that it will not be materially better than the year before.

Anyway, at the moment I am clearly not increasing my position in EVS, rather the opposite. It was one of my larger positions and I think unless something changes (like maybe a big share buyback program), I will remain rather cautious.

Jensen Group

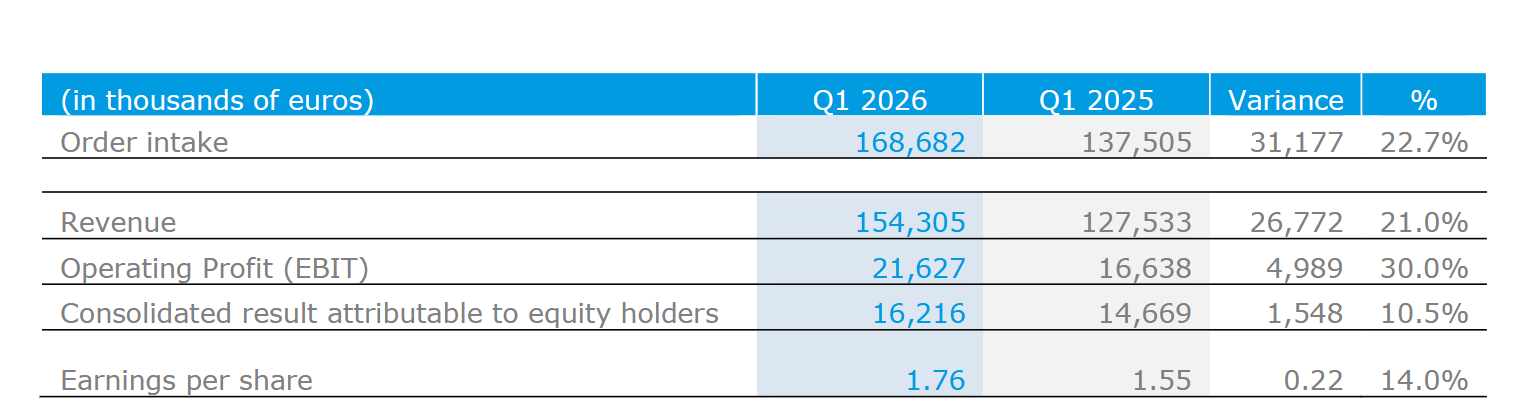

Luckily enough, my second Belgian stock, Jensen Group, is the exact opposite of EVS. Once again they started with a great quarter into the year and are “firing on all cylinders”.

The numbers look fantastic, the only question is why net income only rose by +10%, but maybe there was a tax effect:

They keep buying back shares ( a new 10% buyback program has been approved), book-to-bill is >1 and despite a new all time high, the stock is still cheap as earnings grow as fast as the stock price goes up.

There is currently Absolutely nothing to complain with this company besides the fact that investors think that 11xP/E is the right valuation for such an outstanding company.

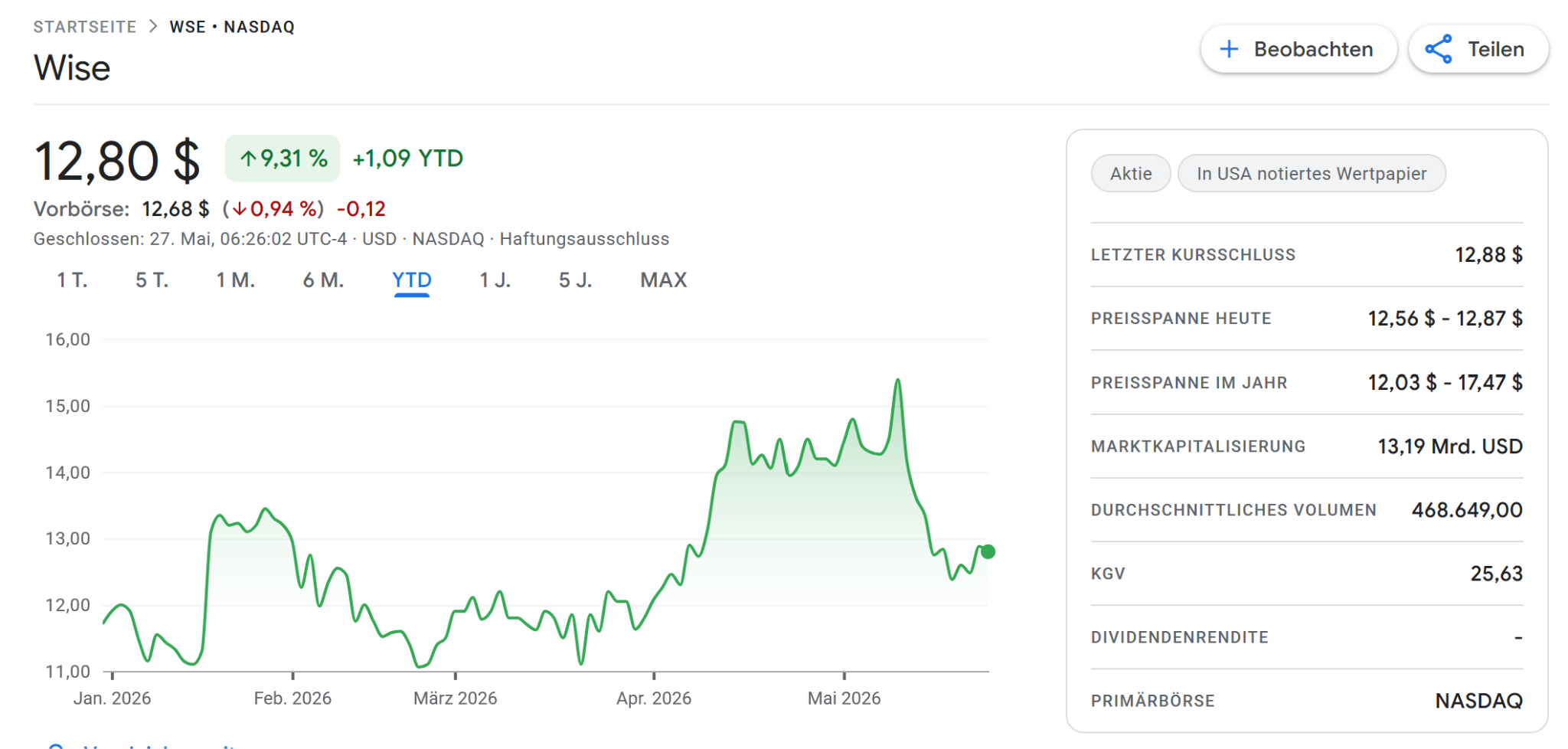

Wise Plc

Wise Plc finally listed on the Nasdaq and as a consequence, I do now have a Nasdaq listed share in my portfolio. The share price went up before the listing and actually reached its peak on the day of the listing on May 11th, only to drop significantly in the aftermath:

The listing for me was not the ultimate reason to invest, but of course it is interesting to see how much the stock dropped directly after the listing.

One factor might have been that JP Morgan seems to have reduced its price target by more than 10% following the listing.

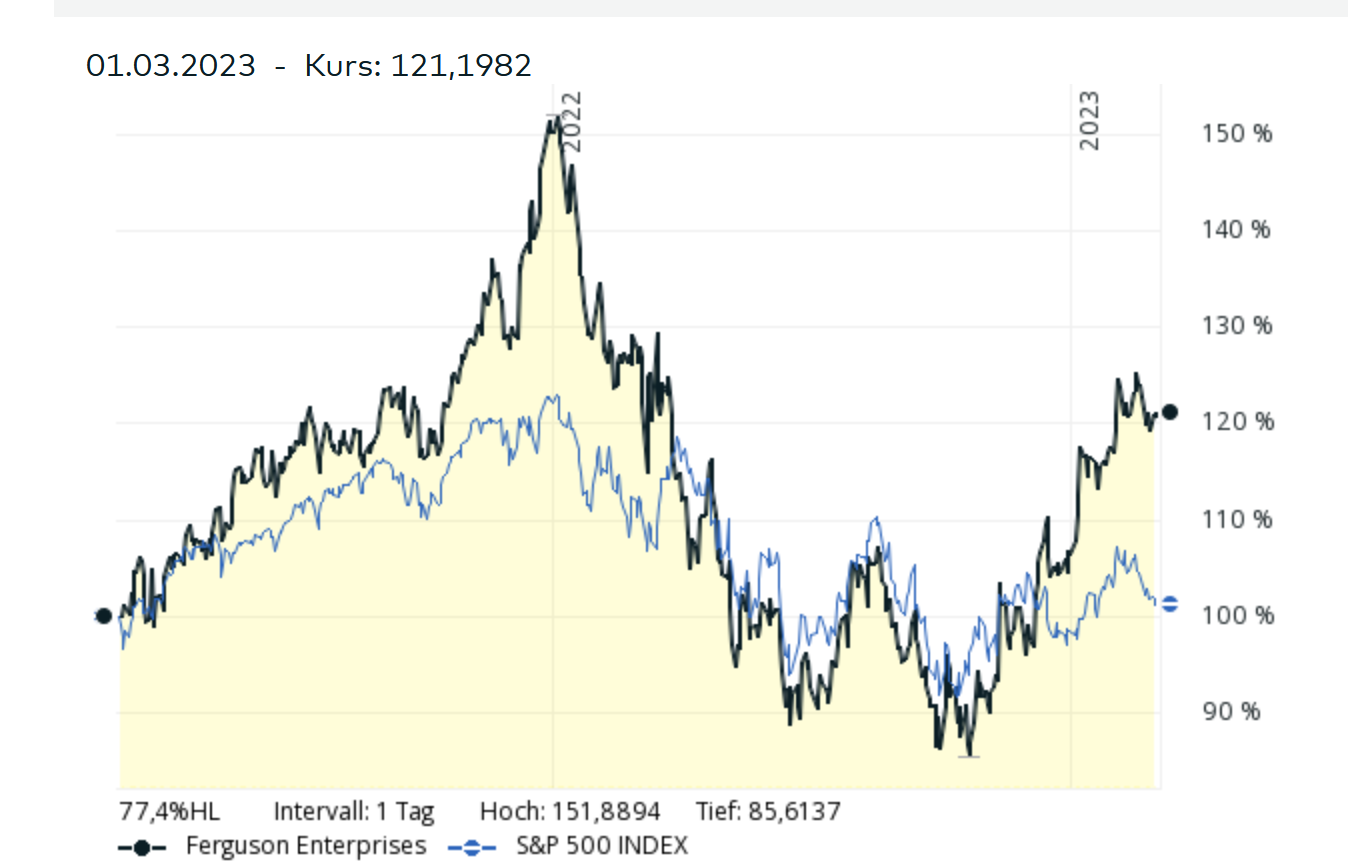

Although not exactly so, this resembles a little bit wehn Ferguson (Wolsely) moved its primary listing to the US in March 2022. As we can see in the historical chart, the stock outperformed significantly before that move but then underperformed for some time thereafter:

Sunbelt rentals (the former Ashtead) also so a drop in relative performance a few days after its listing in the beginning of MArch 2026, but that is most likely due to the start of the Iran war:

Anyway, from a fundamental side, there hasn’t been any change with regard to Wise’s prospects, so no action there.

Installux

Finally, some of my readers might remember that I owned the French Micro Cap Installux for some time (bought in 2012 during the EUR crisis) but sold in 2021 with a decent return despite the stock being still cheap.

Yesterday, out of nowhere, Installux suddenly published that they bought out the largest minority shareholder, French Value Asset Manager Amiral at a share price of 500 EUR per share vs. 290 EUR which was the last trade before that announcement.

Interestingly, the Canty family now has ~88% of the shares and is extending the offer to all other shareholders. Interestingly the 500 EUR are almost the all time high from 2021:

Installux is an interesting case study insofar as the family clearly had very little incentive to show to the outside how good the business actually is. Their long term mission was clearly to get full control of the company. Amiral really had a lot of patience here.

At the end of the day it shows that if you invest into shares like Installux, timing and patience is really everything. You either have to get in when they are extremely cheap or be lucky to be there when the family finally wants to gain full control.

On the positive side, the Canty family never did anything fishy and the final offer seems kind of fair.

congrats on you Rocket gain ! I hope you celebrate with a big Perrier Champagner !!!!

The ascertion on WISE that “…from a fundamental side, there hasn’t been any change with regard to Wise’s prospects….” didn’t age very well.

/Hopefully is not a new Wirecard (similar names though)… But well….

Not sure where you see the similarities with Wirecard. I still think that fundamentally not much has changed. Money laundering is an inherent risk for every bank or money transfer business.

Thank you for the update, always appreciated!

My reaction to the stock price slump of EVS was different to yours, I bought additional shares.

My reasoning was the following: The trading statement did not materially change the situation of the company. Yes, it was/is kind of a disappointment, that 2026 will possibly not be materially better than 2025 although the big events will lead to additional income.

On the other hand, the war in Middle East can for sure have some negative influence, specially on the local customers.

That the CFO has to leave, may not be a good sign, but on the other hand there is no need to overemphasize this. There is a multiple of possible reasons for this.

As you also write, they are known for lowballing, so maybe there will be positive surprises later in the year.

Maybe they chose to formulate it negatively, because a 100% positive statement in combination with the resignment of the CFO would have been even stranger.

For me it’s still the same good company it was before and I got it 15% cheaper.

In my opinion the strongly negative sentiment towards SW companies may have had an effect as well.

But here we are not talking about a US SW company, whose PE went to 50 from 100, but about a company, whose PE is around 12 at the lower end of the forecast and below 10 at the higher end.

And I am very sure, that the SW solutions delivered by EVS will not be easily replaceable by SW vibe coded with AI.

So far, I should have sold even more…

It’s always easier in hindsight… but it’s not over yet…the last weeks have been very difficult for many SW stocks and EVS is no exception. I would wait until the 2026 results are in to celebrate 😉

Yes, let’s see. They also have to find a new CFO. And I am not sure if the 2026 results will be the basis of a big celebration.

I meant it the other way round…you can celebrate, if the results 2026 are disappointing.

No, I will not celebrate, I still own some shares.

Ok, obviously until now you were right. We’ll see how it evolves.

Looking at the images streamed or broadcasted from the Football Worldcup I must say, that EVS seems to do an outstanding job, both quality and stability wise.

Something completely different, but also SW and also knowing, that it is not a european company (which you seem to prefer): have you lately looked at Adobe? To me it seems like an almost incredibile opportunity.