Norma Group: Large Buyback Tender Special situation

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

Executive Summary:

Norma Group, a previously PE owned German manufacturer of small connector parts, is planning to use part of the cash it received from selling a division to buy back a significant percentage (>30%) of its outstanding shares via a tender offer at a premium of up to 20% compared to the current share price.

Although there are some moving parts and the overall case turned out to be more complicated than I thought initially, this represents a potential uncorrelated special situation for 3-4 months with an expected (probability) return of around 13% based on my assumptions.

Norma Group Background/Introduction

Norma Group has clearly seen better days. IPOed in 2011 as a previously PE held company (3I), the stock price did well until 2019 before then losing -80% when the stock price reached a low of below 10 EUR per share in early 2025:

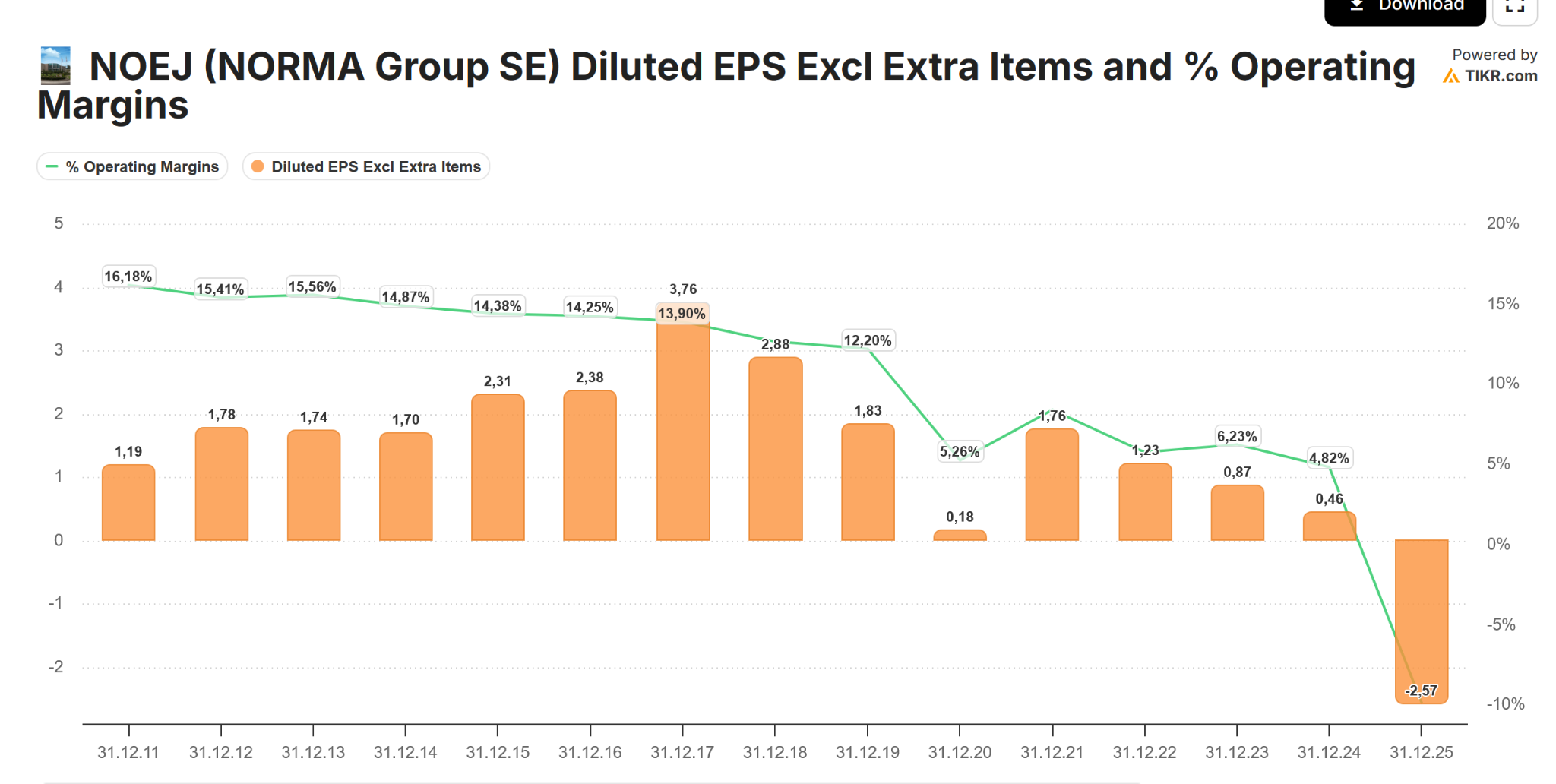

Interestingly, according to TIKR, Operating margins had been on a downtrend since the IPO date and EPS peaked in 2017, but until 2019 no one bothered too much:

Norma was active in what they called “joining technology”, mainly connectors and other small parts out of metal and plastics for industrial applications, the car industry and “water applications”. Here a sample picture:

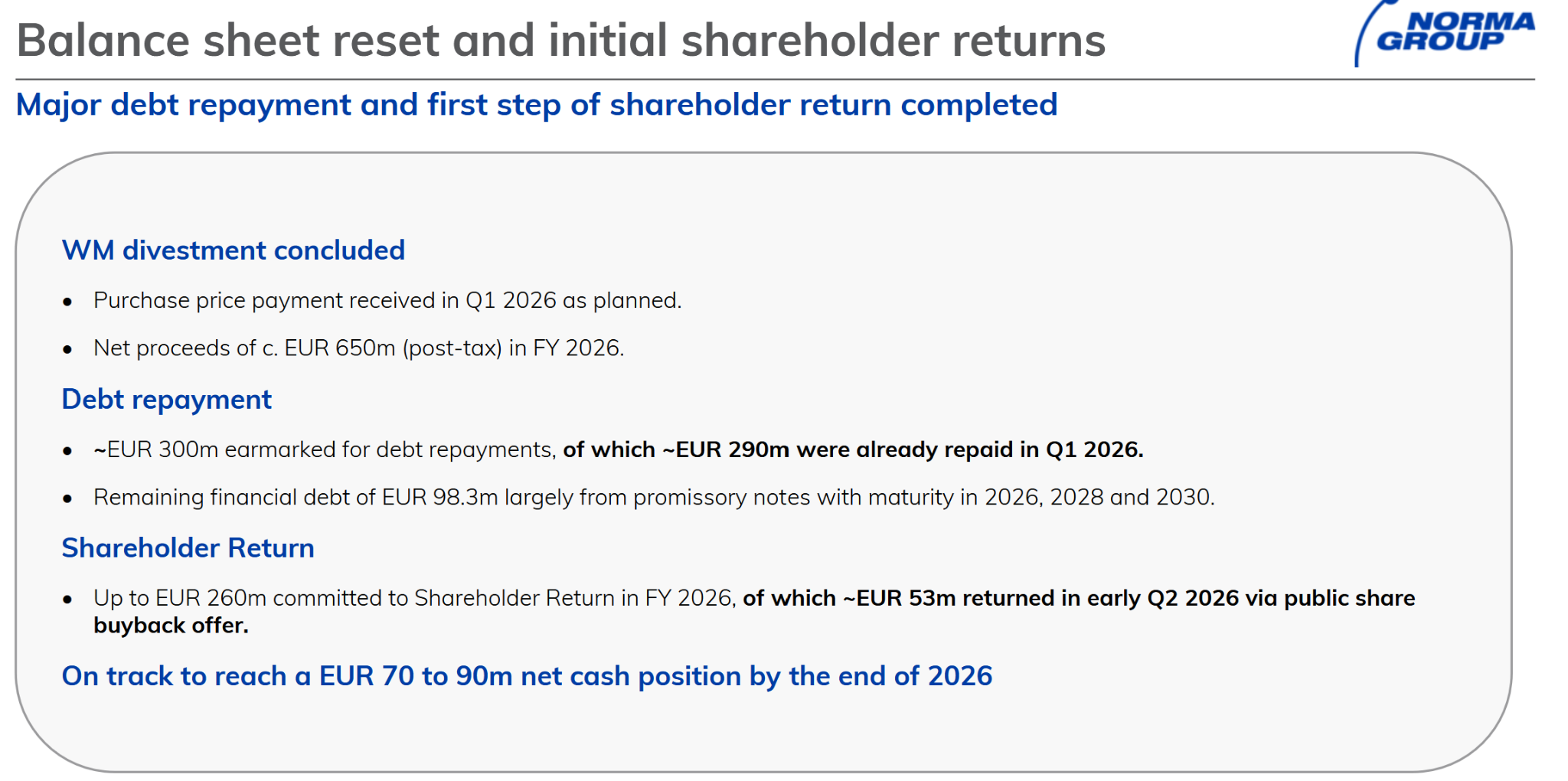

The latter, Water application business was sold for 850 mn EUR of which 650 mn EUR landed as Cash on Normas Balance sheet. Somehow they seem to have structured that deal very badly as they had to pay a lot of tax which is unusual.

Norma said that they already paid back most of their debt and will keep 70 mn for investments into the remaining business and use the rest to buy back shares.

They already made a buyback tender offer of 10% in February at a price of 16,59 EUR.

Here is the overview from the Q1 presentation:

However, that only partially resolved the Excess Cash problem which leads us to this

The special situation: A 30% (plus) buy-back tender at a (up to) 30% premium

Three weeks ago, Norma announced a 208 mn EUR share repurchase tender at a premium of “10% to 30%” to a certain reference price.

Under German corporate law, in this case the AGM has to approve this decision before the board can formally issue a tender offer. The AGM will take place on July 1st in Frankfurt.

Looking into the detailed document (which is the invitation to the AGM, TOP 10 plus the Supplementary Document): We already know the following:

- The long stop date for both, the acquisition and the cancellation of the shares is February 27th 2027

- The buy back premium will be between 10% and 30% (the management board has signaled that they are going for 30%) compared to a certain “reference price”

- The total amount that will be spent is 208 mn EUR in any case

- Shareholders will receive a dividend of 0,14 EUR after the AGM in any case

- That reference price is defined as follows

Initially I thought that this was referring to the date of the initial board resolution,which would have translated into a reference price of 15,62 EUR, but after an in-depth discussion with Gemini, I think it is the 90 day period prior to actually publishing the offer.

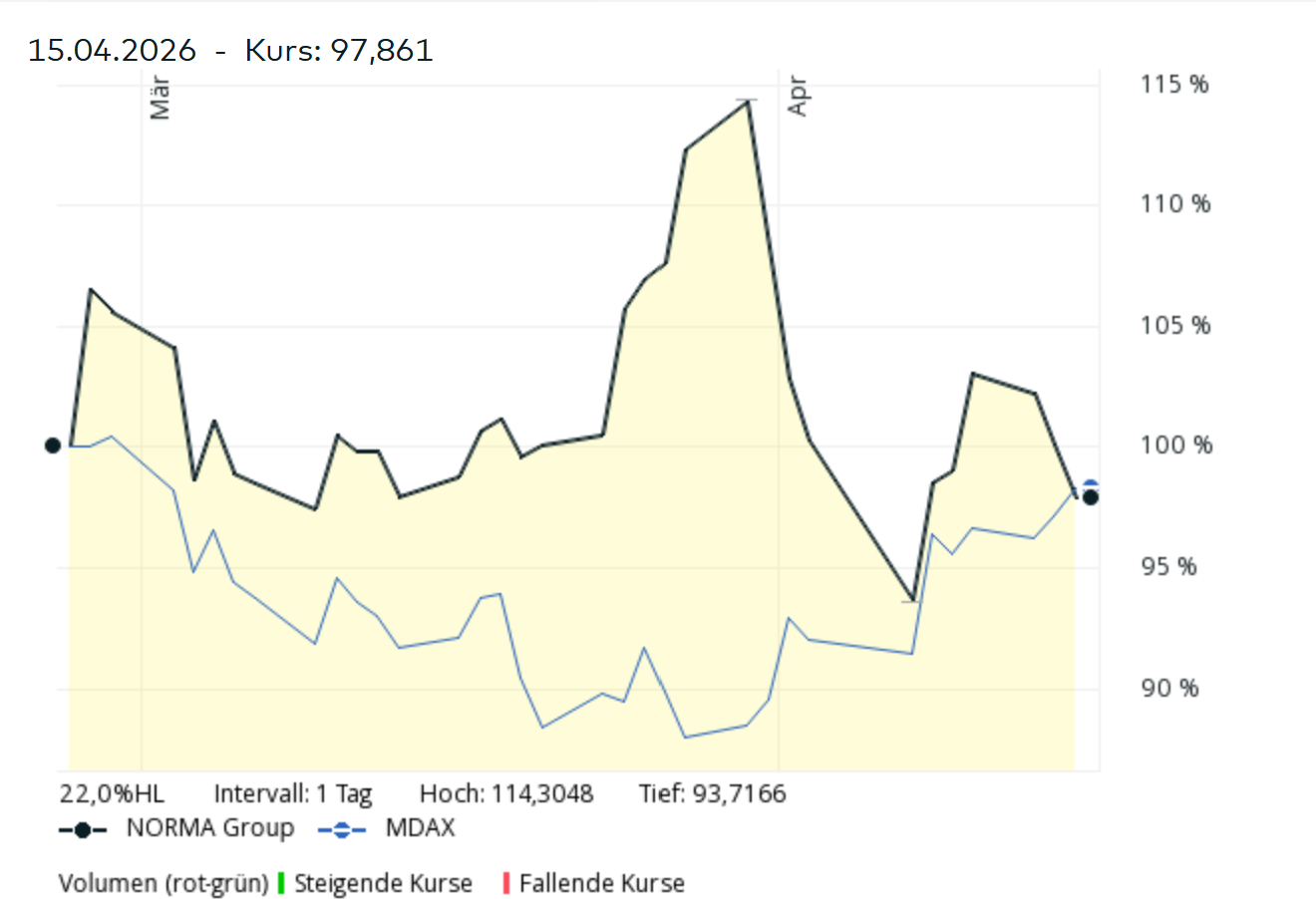

At the time of writing, the current 90 day average of Xetra closes is 16,09 EUR and increasing as long as the share price is at the current 17 EUR as we can see in this chart:

- That the upper cap of the buy-back price is 20,87 EUR which is a “fair value” estimate by the Management

This is how this has been derived:

The Management Board has therefore, in preparation for the Capital Reduction proposed to the Annual General Meeting, commissioned a valuation of the Company in accordance with the IDW S1 standard as at 31 March 2026. This valuation resulted in an average value of EUR 20.87 per NORMA Group Share as at that date.

Looking back: How did the first tender offer in March work out ?

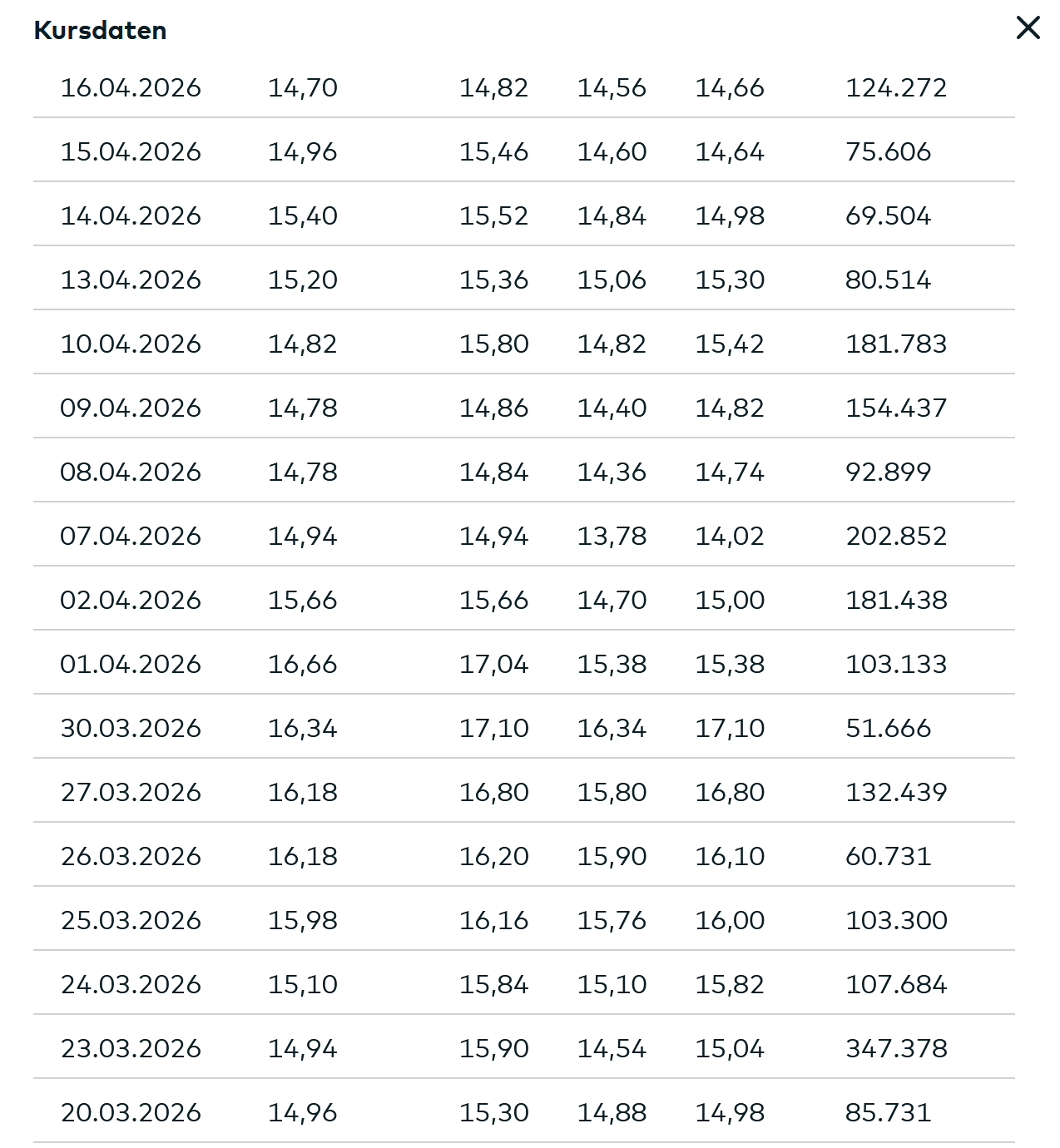

In March, Norma made a buyback tender for 16,59 EUR per share for up to 10% of the total share capital.

This was released on February 26th 2026. The closing price the day before was 14,92 EUR per share, so ~10% premium. The offer period ran from Feb 27th to March 27th.

Interestingly, 18,1 mn shares or around 57% of all shares were tendered, which is a lot for such a small tender with a relatively small premium. As only 10% of the shares were available, only 17,6% of the tendered shares were bought back. We will look at this later once again.

Interestingly, as we can see in the chart, the share price reached a high of 17,10 EUR on the day after the end of the tender period. One week later, on April 7th, the share price reached a low of 13,78 EUR, around -20% vs. the tender offer price:

Maybe that had to do with the release of the 2025 numbers on March 31st and the news that the CEO would step down.

The current Tender: What we don’t know

As I have outlined above, we know certain things about the tender already, but not everything. The main variables that we don’t know are as follows:

- What will be the ultimate premium & share price at which the tender will take place ?

Although they state that the buyback will happen at a range of between 10-30% above the reference price, certain wordings indicate that they will go towards the high end. The most telling sign is the wording in the supplement to the AGM invitation

“The price clause described in section 2.2 enables the Management Board to offer shareholders a repurchase price closer to the intrinsic value of the share.”

For me, this is a very strong indication, supported by their largest shareholder, which will join the Supervisory board, that they will aim for the upper end of the range or close to their “fair value”.

Just to show the numbers:

With 16,09 as reference price, the low end of the range would be 17,70 EUR per share, whereas at the high end would be 20,87 (capped by the “Fair value”).

- What will be the acceptance rate of the tender ?

If we assume the 20,87 as the ultimate tender price, this would translate into 208 mn/20,87 EUR = 9,97 mn shares which represents 31% of all shares or ~35% of all shares ex current treasury shares.

So if all shareholders tender fully, the minimum acceptance rate for every shareholder should be 35% (around 2x the acceptance rate from the first offer)

Another assumption is that Teleios, the 17,15% shareholder, will not want to lower their stake when they simultaneously join the board. So if we assume that they tender only 35% of their shares, we can assume that another 17,15-(0,35*17,15%)=11,2% of shares will not be tendered for sure.

This translates into a “worst case” acceptance rate of around 40% for the scenario with the maximum purchase price.

On the other hand, it is also very likely in such cases that not everyone tenders. I will solve this issue by creating several scenarios and weighting them with my subjective probabilities. More on this later.

- At what price will one be able to sell the shares that are not accepted in the tender

This is clearly a tricky one, but it is also necessary to assume that one in order to be able to calculate an expected return for this special situation.

My assumption here is that one should at least get the current reference price of 16,09 EUR per share. I will share some thoughts on the potential value of the “stub” at the end of this post.

- Actual timing of the offer

To be honest, I am not 100% sure how fast they can execute after the AGM approval. There might be some regulatory requirements (entry into the company registry) or maybe some of the usual suspects will try to blackmail the company with legal challenges.

But my assumption would be that the tender offer period starts in August and will be concluded in September. So from today, the time required for this to fully play out will be 3,5 to 4 months.

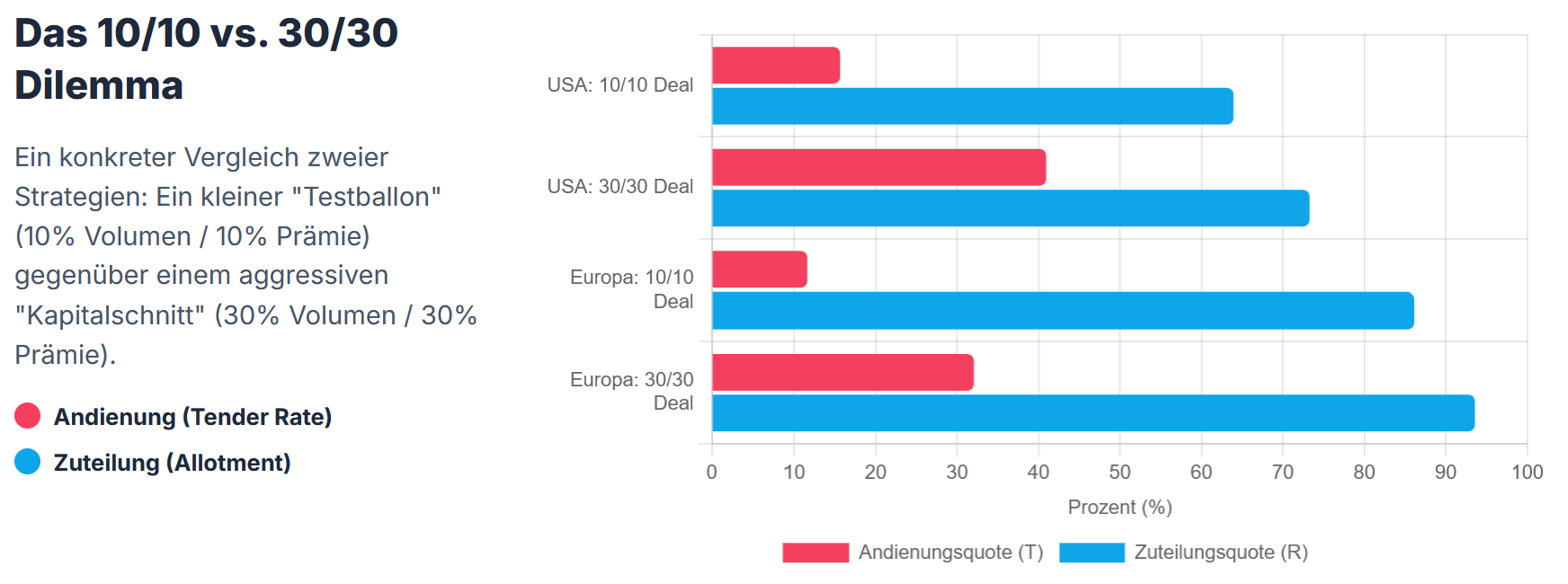

AI excursion: Analyzing the potential tender rate and resulting Acceptance rate

One main element that one needs to estimate is the percentage of shares that will actually be tendered. I have mentioned in the beginning, that in the first tender, 57% had been tendered with only 10% available, resulting in a relatively small acceptance percentage of 17,6%.

Based on empirical evidence, a higher premium increases the tender rate, but a bigger tender size relative to the outstanding shares increases the acceptance rate.

I asked Gemini to analyze tenders from the past years and estimate a regression. Interestingly, tender ratios are often quite low and acceptance rates much higher than one would normally think.

This is what Gemini estimated for a 30% Tender with a 30% Premium vs. a 10% Tender with a 10% premium both, in the US and Europe:

According to their regression, a 90% Acceptance/Allotment should be expected and only 30% of shareholders would tender. Now this sounds to good to be true and the first tender of Norma earlier seems to have been already a clear outlier.

So looking at historical data clearly helps but in any case one has to make one’s own assumptions for this case.

Overall; I do like to use AI models as a sparring partner especially in these Special Situations. Although one needs to get used to its “cocky” behaviour, I do think the discussions and additional analysis improve the process and hopefully, in the long run over many transactions, the outcome.

Return estimation based on a 30% premium to the reference price:

So now we have everything to estimate an overall expected return, of course based on all the assumptions I described above.

Here is my return estimate based on the 30% premium (capped at 20,87 EUR) and on a current share price of 17 EUR (including the dividend and 16,09 selling price for not tendered shares):

So 13,3% “expected return” over 3,5-4 months is not too bad given the current 2,25% short term interest rate in EUR.

Of course this is based on my assumptions that I have laid out above and different assumptions lead to different results.

Many of the uncertainties will go away over time such as:

- The AGM will take place on July 1st. After the AGM we will know if someone wants to play games with the tender offer or not and how a realistic time table will look like

- Once, the legal requirements are met, the management will formalize the offer and we will then know the actual premium

- Finally, after the end of the tender period, we will know the final acceptance rate and then also the share price for the shares that can not be tendered

What happens at the low end, a 10% premium ?

This would of course be less attractive but one needs to consider the following: Norma intends to spend the full 208 mn, so the assumption here would be that they buy back more shares and the acceptance ratio will go up. The minimum acceptance would be 47%.

Also, there would be more value for the stub, but I will stick with the 16,09 EUR as selling price for the non-tendered shares. The probability of the acceptance rates also needs to be adjusted upwards.

Based on these assumptions. my return expectation looks as follows:

So at the low end which is basically almost the worst case, I would have a return of ~2% based on a current share price of 17 EUR. Only in the worst case, when basically everyone tenders, there would be a small loss.

So based on my assumptions, the situation looks like a pretty cheap “option” on a potentially higher acceptance ratio.

Some thoughts on the “Stub”:

If we assume that the tender gets through and that the shares will go back to 16 EUR per share, we will have a company that has around 18,7 mn Shares outstanding at a market cap of 18,7*16= 300 mn EUR if they pay the 30% premium

They plan to have a net cash position of 70-90 mn EUR by the end of 2026 according to their Q1 presentation, so EV would be between 210 and 230 mn EUR.

For 2026, Norma expects 820-830 mn EUR in sales and a 2-4% “adjusted EBIT margin” which would translate into ~16-35 mn in “adjusted EBIT”. At the midpoint, this translates to 25 mn adjusted EBIT or an EV/Adjusted EBIT multiple of 8,4-9,2x.

In the case of a 10% premium and a 16 EUR share price, the market cap would be ~270 mn EUR and EV/EBIT between 7,2-8,0 x EV/EBIT.

Not “dirt cheap” but not expensive either. In the second half of 2026, they plan to present a “2028 strategy”.

I think despite the relatively unexciting business, the valuation of the stub is cheap enough that I think that from a fundamental side, the downside risk is limited to a certain extent after the execution of the tender. Of course, if there is an overall market crash, no one cares about fundamentals anyway.

One important point here: For the time being, I am not planning to bet on a turn-around.

For me this is a Special Situation investment and I will exit once the tender is settled.

Technicalities:

This is an interesting detail from the invitation to the AGM

To the extent technically possible with reasonable effort, tender rights trading (Andienungsrechtehandel) is to be established.

The shareholders’ declarations of acceptance are taken into account according to shareholdings by tendering the tender rights attributable to the shareholding as well as any additional tender rights acquired from other shareholders.

So this means that there might be a mechanism that similar to a capital increase with subscription rights, in this case the tender rights might be split of from the shares and traded separately.

I haven’t seen this before and if this is implemented, it could create a special situation in itself, if those rights might trade higher or lower than the intrinsic value. So from that perspective there might be an additional “option” to improve the outcome

Timing option

As we have seen in the example of the fist tender, during the official tender period, the shares had already approached the tender price. Depending on how this is structured, I will definitely make sense to tender rather late in order to keep the option of selling the shares at a decent price before the execution of the tender.

If we have separate tender rights, then the opportunity will be mostly in analyzing the tender rights as mentioned above.

Summary:

At the current price of 17 EUR, I do think that the upcoming tender offer of Norma Group offers a decent return to park some cash for 3-4 months at an expected (probability weighted) return of 13% (not annualized).

Even at the low end, under my assumptions one would be able to make a 2% profit and the very worse case would result in a small loss (less than 1%).

For a special situation, I think there is also a lot of additional optionality baked into this whole process which in my opinion outweighs the uncertainties.

There are still a couple of moving parts and the tender is rather complex, so my overall allocation to this is rather small at 3% of the portfolio.

I will watch this very closely and I might increase the position if the price goes down or if new positive information comes in and the price stays low.

What I do like is that the risks are very specific and not much correlated to the overall market, which makes it attractive for the “opportunity” part of the portfolio.

I guess that also the complexity of the offer creates an opportunity here.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

I think you’re a bit optimistic regarding the share price for shares which you’re not able to tender. If my understanding is correct, you assume 16.09 / share, which implies an EV of roughly ~€420m (16.09 x 22m shares + 98m debt – €80m cash + €46m pension and NCI). If we assume an EBITDA / EBIT for 2026 of €70.6m and €24.9m this would imply an EV multiple of 6x / 17x, which both seem a bit high for a small cap business with such low margins, little growth and a restructuring phase ahead. Happy to hear your thoughts on this, though. Based on my calcs – even if the tender price would be 20.87/sh – the probability weighted return would be around 2.3% only.

As I mentioned everyone csn mske his/her own assumptions. One specific remark: to my understsnding therr wiöl be 70 mn net cash.