Again, this has turned out to be a long post. So a quick “executive summary” upfront:

Electrica S.A. looks like an interesting play on infrastructure in Romania. The stock is attractive as

– the current valuation is cheap compared to grid companies in Spain, Portugal and Italy

– the underlying business (electrical grid monopoly) looks structurally attractive due to high guaranteed returns on investment

– there is good visibility on growth for the next 5 years

Overall, based on relatively conservative assumptions, an investor could expect to earn 17-21% p.a. in local currency over the next 5 years.

There are clearly lots of risks (regulatory, politically) but overall the risk/return profile looks good and the risks are less correlated to overall market risks.

DISCLOSURE: This is not an investment advice. Do your own research !!! The author may have already invested in the stock prior to publsihing the post.

When analyzing Romgaz I said this:

Why Romgaz ? Well that one is easy: This is the only Romanian stock you are able to invest if you don’t have access to the Bukarest Stock Exchange. There are no ETFs on Romania either.

Well, that was wrong, because another formerly Government owned Romanian company IPOed in June this year on the LSE, the grid operator Electrica.

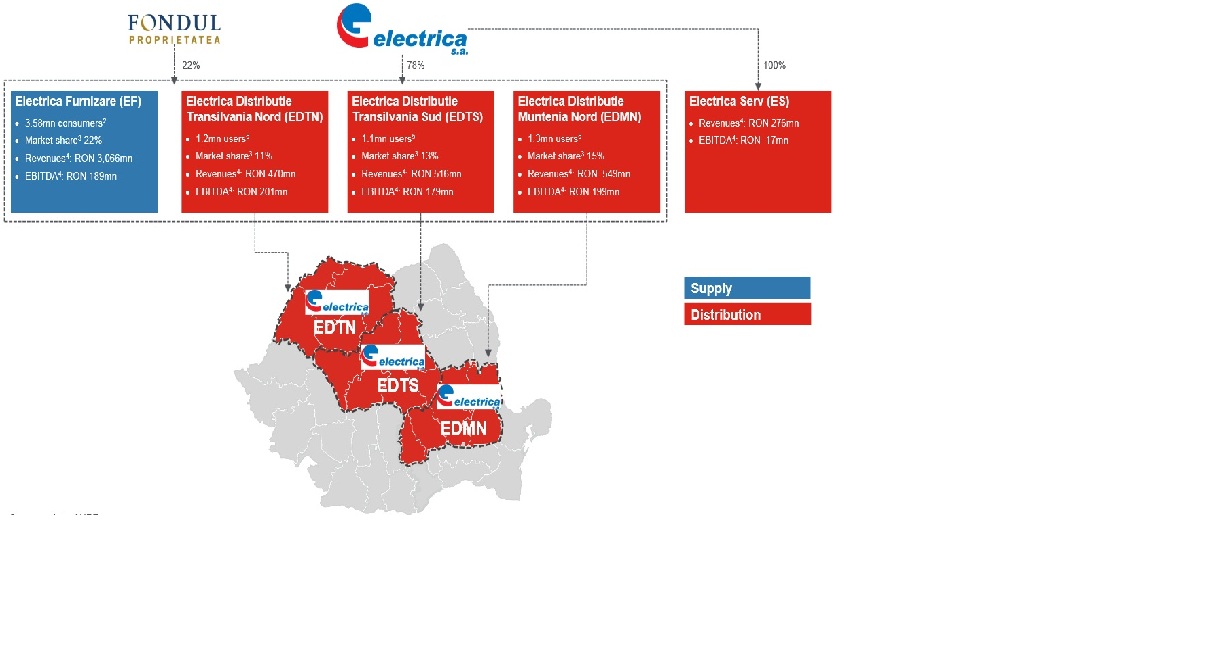

Electrica – the business

Electrica’s main business is owning and running the electrical grid in an area covering ~40% of Romania. Additionally, they are also an electricity supplier, however they do not generate any power. This graphic from the recent 9 month presentation shows how this looks on the map:

Similar to Romgaz, the IPO prospectus is a pretty interesting read, covering many aspects of the Romanian electricity market. Those were the major points that I extracted from reading the prospectus:

+ IPO proceeds went 100% to the company to fund future growth

+ significant potential for additional guaranteed investments

+ conservative balance sheet

+ efficiency gains possible (10% grid loss)

+ underlying growth potential

+ valuation ex cash VERY cheap for a grid company

+ potential M&A opportunities (ENEL assets)

+ EBRD as shareholder actively protecting minority rights

+ local regulation creates attractive “float”

– guaranteed return on regulated assets has been just lowered from 2014 peak (7,45% vs. 8,35% in 2014)

– business is partly electricity distribution, no pure “grid” play (no guarantees for distribution)

– limited experience with regulator (previous head of regulator convicted for bribery)

– some distressed subsidiaries (external grid maintenance)

– 22% minorities in all major subsidiaries

Electrical grid as a business

Building and maintaining an electrical grid is a very capital-intensive business. The electric grid is one of the most dominant monopolies available. There is competition on the generation and supply side, but there is always only one electric grid as this represents the archetypical network effect.

There is just no reason to build a second electrical grid and unlike as for instance telephone landlines, there is a pretty low risk that electricity could be distributed via an alternative way. This is one of the reasons that grids are almost always heavily regulated as the potential power to abuse this monopoly would be pretty high.

One additional features is the fact in many countries the grid was not designed to cope with locally generated renewable energy, so there is clearly a need for massive additional investments. Normally, a sector with large investment requirements is not that attractive, but if you combine this with stable yields and leverage potential, things can suddenly become very interesting in a low growth environment.

I had written 2 years ago that even Warren Buffett thinks utilities can be attractive, if the earnings are stable or even guaranteed, especially if you then can leverage up accordingly. Also the announced E.On spin-off ties to move grid and end-user supply into the good ship

Although there is always a risk that regulators run amok, at least for electrical grids the seem to be on the soft side as they know that a lot of capital is required to cope with the renewable energy revolution. As a consequence, the valuation of listed grid operators are the highest among the overall utility sector.

Let’s look at the valuations of 4 listed electric grid companies in Europe:

| Name |

Mkt Cap (EUR) |

BEst P/E:2FY |

P/B |

ROE |

ROA |

Debt/capital |

| |

|

|

|

|

|

|

| REDES ENERGETICAS NACIONAIS |

1.352 |

12,2 |

1,2 |

11% |

2,4% |

70% |

| RED ELECTRICA CORPORACION SA |

9.922 |

16,5 |

4,2 |

24% |

5,8% |

60% |

| TERNA SPA |

7.811 |

14,6 |

2,5 |

17% |

3,7% |

71% |

| ELIA SYSTEM OPERATOR SA/NV |

2.442 |

16,1 |

1,1 |

9% |

3,3% |

55% |

It is interesting to see that despite being located in the more critical countries of the Eurozone (Portugal, Spain, Italy and Belgium) those companies enjoy quite rich valuations. ROAs are low single digits but due to the monopoly character of the business, it can easily be leveraged up between 50-70% of the total capital (and several times equity).

Romanian electricity market

This is an interesting quote from the IPO prospectus:

The average electricity consumption per capita in Romania is still significantly lower than the average electricity consumption in the 28 EU member states. In 2012, Romanian electricity consumption per capita was 2.3 MWh, whilst the average electricity consumption per capita in all the EU countries was 6.0 MWh and in the selected Central and Eastern European countries (excluding Romania) in the table above it was 4.3 MWh.

<

So assuming that Romania will catch up to a certain extent with the Eurozone, underlying growth in the electricity market should be strong. Romania has separated grid and power generation, however, at least in the case of Electrica, supply to end users is still part of the package.

The power market for end users is still highly regulated to a large degree but will be liberalized going forward. For Electrica’s grid business, this is irrelevant, but the supply business could be affected.

Electrica has a 25 year concession to operate the grid with an option to extend another 25 year. They can charge a fee to customers which guarantees them a certain pretax rate of return on assets if the meet minimum requirements set by the regulator. The base rate which they can charge is currently 7,45% for the next 4 years, higher rates seem to apply for “smart grid” investments.

One interesting specialty of the Romanian market is the existence of the “connection fee”. This is what they say in the IPO prospectus:

According to the law, the value of new connections to the electricity network is charged to the final users as a connection fee. The new connections to the electricity network are the property of the Group. The Group recognises the connection fee received as deferred revenue in the consolidated statement of financial position and subsequently records it as revenues on a systematic basis over the useful life of the asset.

The total amount they show as deferred revenue is 1,4 bn RON which is quite significant. For them, this is a very attractive “float” as it doesn’t carry interest and no covenants are attached. I assume that this also explains why they don’t use external debt as the investments are basically financed by the clients.

Valuation – simple version

Electrica has a market cap of 4 bn RON. Including IPO proceeds, the sit on 2,8 bn liquid assets, so the core business is valued at 1,2bn RON. With a run rate of 250 mn Earnings, this equals P/E of 4,8 ex cash. Assuming that a unlevered grid company in Romania could be worth 10 times earnings (still cheap compared to a highly levered Portuguese grid company at 11x earnings), the upside for the stock would be at least 30% based on current earnings.

Valuation including growth

Now comes the interesting part. Normally as a value investor I would assume zero growth. But in Electra’s case I would make a difference. Why ? Well, because:

1. They can invest (“compound”) at a guaranteed rate

2. The have already raised the money

3. The guaranteed rate can be charged irrespective of power prices or volume

4. There is no competition

The “only” risk that remains is the regulator. In order to model the profit growth, I have built a very simple model for the next 5 years using the information form the IPO prospectus:

I made the following (conservative) assumptions:

– supply business remains more or less constant despite significant growth yoy 2014

– I assume the losses from the “distressed” service subs will be phased out over 3 years

– they will distribute 85% of earnings as dividends

– they will invest according to plan at a blended guaranteed rate of 7,7%

Based on those assumptions, the profit after tax and minorities should double within 5 years. Assuming 8%% dividend payout (all of which can be funded by existing cash on operating cashflow), one can expect a return of 17-21% p.a. assuming an exit P/E multiple of 11-15.

Assuming exit multiples is of course already quite aggressive, on the other hand, if the price wouldn’t move, the assumed dividend yield of Electrica would be more than 10% in 2019. So some multiple expansion would not be unrealistic.

Addtitional (significant) upside could come via profit increases in the supply sector or opportunistic M&A as the ENEL grid seems to be for sale. My required rate for such an investment would be 10-15%, so at the current price Electrica looks attractive.

Other considerations

Stock price: In local currency, the stock price is only slightly above the IPO price of 11 RON:

Analysts: According to Bloomberg, a surprising number (8!) of analysts cover the stock. Their price target on average is around 14,6 RON, a potential upside of 30%.

Shareholders: During the IPO, the EBRD (European Developement Bank) acquired 8,6% of the shares. According to this article they are actively working to protect/ensure minority shareholder rights:

“Our participation demonstrates the EBRD’s commitment to supporting the government’s plans for increased privatisation of the energy sector,” Nandita Parshad, Power and Energy Director at the EBRD, said in a statement.

Parshad said the EBRD will work with Electrica to align its corporate governance with international standards: “This will provide additional comfort and confidence to potential future investors.”

The Romanian government still owns 49%.

Management: There is unfortunately not a lot of information on management. The CEO is an “Old timer”, joining the company in 1991. there seems to be some variable component in their companesation package but it is not clear how this looks like.

“Frontier” market: Despite being an EU member, Romanian stocks including Electra are considered “Frontier” stocks by MSCI, not even “Emerging”. That might make it more difficult for “established” funds to invest.

Summary:

As I have written in the Romgaz post, I find Romania fan interesting market in general especially with the lection of the new President. Electra is similar to Romgaz a privatization story. What I like about Electra is the fact that there is good visibility on growth.

The major risks are from the regulatory side, although I am quite optimistic that with the new president there will be even more of a “pro business” and “pro growth agenda”. Plus, the risks in this case in my opinion are relatively uncorrelated to other issues within my portfolio, so I think this could be a good diversifier.

With relative conservative assumptions and the guaranteed part of Electrica alone, one should expect between 17-21% return per annum over 5 years. If the non-guaranteed supply business improves or they are able to get other parts of the Romanian grid then the upside could be even higher.

I am pretty sure that not many investors will be interested in the stock as it seems to be both, too exotic and a strange mixture between “deep value” and growth, but for me it is the perfect stock as I don’t have to track any indices.

For the portfolio, I will buy a 2,5% position at current prices. This increases my “Romania bet” to 5% and total EM exposure to 13%. Time horizon is 5 years.