This post does not contain any actionable investment advice but rather some personal ramblings on Vibe coding and the attempt to analyze a specific Software company (Guidewire) according to a Template of 10 Moats for Software companies and their vulnerability to the AI threat.

Introduction:

My track record as a Software investor is to put it mildly, very poor. My best Software Investment so far is Chapters Group which I bought as a net-net before it even became a VMS Serial Acquirer. My blog and portfolio archive also tell me that I sold Microsoft in 2011 at ~25$ per share with a 4% gain because I thought that the Office products had no future. So please take everything I say about Software with a grain of salt or even better, just ignore it.

I do have a background in Software development. Although I would not call it Software development but “Code butchering”. It started as a teenager on a C64 with Basic and Assembler and ended in the late 1990s with Cobol/PLSQL working for a large US Consulting Company (yes, I was young and needed the money). Knowing the speed of financial institutions, I would not be surprised if some of my Spaghetti code would still be running somewhere….

Why am I saying this ? Because of course, Software stocks have been doing quite poorly over the past weeks/months. In addition, I also had the opportunity to play around with Claude Code first hand.

Disclaimer: This is not Investment advice. The stock discussed is very illiquid and trades at the unregulated market (Freiverkehr). If you want to buy this stock, work very carefully with strict limits. The author owns the stock and might buy/sell it without giving prior notice. And as always: PLEASE DO YOUR OWN RESEARCH !!

After having two (relatively) exciting stocks in the last two weeks with Rocket Internet and Innoscripta, I decided to tune down the exitement a little bit and focus on a very boring, family run German small cap this time. In order to not fall asleep, you might want to listen to the Soundtrack while reading:

Elevator Pitch:

This write-up is special in two ways. For one, I have privately bought the stock already a few months ago. Secondly, I base this write-up on another write-up from my friend Jon from abilitato.de. So please read that one before you read my “mini-writeup” where I only focus on a few specific aspects.

In a nutshell, Frosta is a boring, under-the-rader German family owned and run frozen Food company that does not do a lot of investor relations but runs a very convincing strategy focusing on additive-free ready made frozen meals. Inventing this category more than 20 years ago, the main Frosta brand is now growing with solid “mid teens” percentage rates p.a., has succesfully managed to enter and grow in neighbouring countries and with profitability that is steadily increasing. For the quality of the company and the potential growth prospects, the stock is still relatively cheap in my opinion at around 12×2025 P/E (ex net cash).

Here ist the write-up. Best read it after having a decent “Chicken Paella” from Frosta 😉

This is an investment idea that I have “borrowed” from my friend Jonathan Neuscheler from Abilitato. Therefore I highly recommend to read what he has written first. And this is also the reason why this write-up is rather short.

In short, I think Fraport is an interesting turn-around/deleveraging story with a near term catalyst in form of the resintatement of the dividend in 2026. Relative to its peers, Fraport trades at a significant discount which could disappear if things go according to plan which adds to the potential upside.

Here is the write-up (don’t worry, only 9 pages incl. pictures):

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Background:

Bombardier is a Canadian company that after a colorful past as a conglomerate and an “almost bankruptcy” in 2020 is now fully focused on manufacturing Private Jets and until recently has been a poster child of a very successful turn-around. My friend @Govro12 from the Wintergems substack has written a very nice post on Bombardier just a few weeks ago which I highly recommend to read.

High level Presentation:

Although I only could convince myself to buy a small starter position (<1%, to keep me interested), I presented Bombardier as a potential interesting investment case in a private investor meeting some days ago. Here is the presentation which I admit is pretty high level. Spoiler alert: I would not recommend to invest right now.

Portfolio company SFS published 2024 numbers last week. Intitially, the stock reacted very negatively, dropping ~-9% only to recover fully by the time of writing:

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!!

As mentioned in the Performance review, I had already build up a new position in late 2024 in a new stock. This time I will try something new: I will only post a few sections of the write-up and only those who send me an email will receive the full version (for free of course).. The reason for this is that I am really interested how many of the readers are actally reading the full document. The bonus song of course is included in this post at the end.

0. Investment meme

For some strange reason, I felt the urge to start the pitch with this rather “German humor” meme:

Elevator pitch:

Jensen-Group, a company originally from Denmark, now listed in Belgium, is a 420 mn EUR market cap “hidden champion” that is the world market leader in “Heavy laundry” equipment and automation. The company is run in third generation by the Jensen family which still controls 40% of the shares.

Energiekontor has been one of my worst performing stocks in 2024, the performance was much worse than the borader renewable peer group. To be honest, I am not sure why the stock performed so bad. On part of the explanation is clearly that the overall political shift to the righ (Trump, Germany etc.) might be bad for renewables, which explains the overall bad performance to some extent. It didn’t help either that they announced a 2024 profit warning some days ago.

However, they didn’t adjust the mid term guidance (2028) and it seems that the profit warning was clearly just a short term timing issue with a required approval of a purchaser for a large UK wind farm. So next year could look very nice especially for the developer segment.

Despite the political uncertainty, I still think that Energiekontor is one of the best bets in the sector. Here is a table I did some weeks ago showing that Energiekontor, among a European peer group, is both the cheapest and the least leveraged player:

DISCLAIMER: This is not investment advice. The Author is known for making lots of mistakes in his write-ups and will frontrun you whenever possible. DO YOUR OWN RESEARCH !!!!

As always in my longer write-up, this post only contains selected sections of the write-up- A full pdf is embedded below.

Management Summary

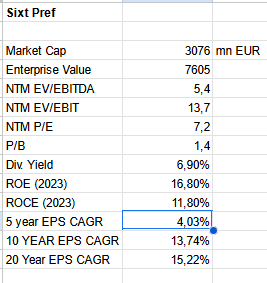

Sixt AG, a family-owned and -run Car rental company from Munich, has been compounding profits and shareholder returns at a double digit CAGR for the last 20 years. Following Covid, they accelerated their organic growth in the US which now represents ⅓ of their business and is growing rapidly at 20% plus p.a..

As most of their competitors (Hertz, AVIS, Europcar) are overleveraged, they will continue to take market share from them in the coming years. The recent (temporary) issues with residual (EV) car values depressed valuation multiples so that Sixt trades at a very low P/E for 2025 (~8 times for the Prefs, 11x for the common) for what I consider a high quality company resulting in an attractive risk return profile.

Background

Sixt is a company I owned several times in my investment career, unfortunately never long enough. During the initial Covid panic, I bought a “half” position as a part of a wider Covid basket” without any deep fundamental research at that time. Initially, this turned out to be a brilliant investment and almost tripled until the end of 2021, however since then, the stock struggled.

Following that Tweet, I thought it’s a good time to dive a little bit more into the rental car industry and see if I should “re-underwrite” Sixt or not.

3. Sixt History & some KPIs

3.1. Company history

Sixt was founded in 1912 and so technically is the oldest of the large car rental companies. However, only with Erich Sixt, who became CEO in 1969, Sixt started to expand significantly. Sixt went public in 1986 and opened the first US Branch in 2011. In 2021, Erich Sixt after 42 years finally passed to lead over to his two sons who now run Sixt as Co-CEOs in the 4th generation.

3.2. Some KPIs

We can see that over 10 and 20 years (based on 2023), Sixt has been a great compounder. Only over the last 5 years (EPS 2018 adjusted for DriveNow one off gain), EPS growth slowed. But one has to remember that this time period includes a beginning recession (2019), Covid, interest rate increases etc.

It’s also worth mentioning that all that growth was achieved organically. To my knowledge, Sixt never acquired another company.

As always, when a stock is cheap, the question is: Are there any perfectly good reasons for the stock being so cheap ?

Despite the general weakness in European small and midcaps, these factors might play a role:

A common theme I hear is that the rental car business is a shitty one. I think this is mainly due to the fact that the problems of AVIS, Hertz and Europcar are very public, but the success of Enterprise is not. On a P/E basis, both Hertz and Avis have traded at similar multiples (but with a lot more debt). As Enterprise is not publicly traded, some analysts might look at Sixt and decide that it is even “expensive” compared to Hertz and Avis.

Falling residual values for cars have impacted Sixt in 2024. Initially, an EBT of 400-520 mn had been forecasted. After Q1, where they had to book a loss because of unexpected depreciation, they had to cut the guidance again with the Q2 results in May to 350-450 mn EUR. In Q2 once again they again reduced the outlook to 340-390 mn EUR. So investors might be afraid that Q3 might contain more negative surprises.

Investors might still not fully trust the two sons to continue what Erich has achieved over more than 40 years. I have to admit that I am also not 100% convinced. Only time will tell.

Sixt is clearly also exposed to the overall economic situation. A deepening recession in Europe might soften the demand, both for vacation rentals and business customers. Or customers might trade down from Sixt’s premium offer to a cheaper competitor.

11. Summary & conclusion

The initial question that I asked myself before writing this post was: Should I re-underwrite Sixt despite the quite disappointing performance over the past months ?

Thea answer after this exercise for me is clearly YES.

Sixt is a stock that offers an interesting growth story, a strong track record for a very low valuation which in my opinion creates a very attractive risk-return profile on a mid-term time horizon.

There are clearly some risks, as mentioned my main concern is how the sons will perform once Erich is not around anymore.

In any case, I decided not only to “re-underwrite” the stock but to increase my exposure by buying an additional 1% of the portfolio of Common shares.

I might add further, both to the Prefs and the Commons in the future if no negative surprises happen. The date for the release of Q3 earnings is November 11th.

Disclaimer: This is not investment advice. The guy who is writing this has problems distinguishing USD and GBP. PLEASE DO YOUR OWN RESEARCH !!!

A friendly reader alerted me that I made an error in the Ocean Wilson Special Situation NAV calculation. I seem to have gotten confused by the fact that Ocean Wilson reports in USD. I did translate the Wilson and Sons stake into GBP but not the investment portfolio. Instead of 319,6 mn GBP, the investment portfolio is worth 319,6 mn USD which equates ~ 239,7 mn GBP

So the initial calculation should have rather looked like this:

The expected return is a full -8% lower than inititally (and wrongly) calculated. Still not bad, but clearly less advantageous.

Based on this, I reduced the positon to a ~1% position.

I am deeply sorry for this mistake and a big thanks to the reader who alerted me. Going forward I will need to be more dilligent for these calculations-

One other remark: A reader congratulated that my post has moved the stock price. This is not my intent for the blog. I try to avoid writing about illiquid stocks as some readers tend not to read the posts and seem to blindly buy. With Ocean Wilson, I was very surprised how illiquid this 500 mn Market cap stock actually is. For me this is a good lesson for the future that I don’t write much about illiquid stocks. I leave that to others.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

As always with my more detailed writeups, I will focus on the general sections in the post and attach the full pdf for anyone interested in the details. And of course the Bonus Sound Track.

Elevator Pitch

Fuchs SE is a 4,5 bn EUR market cap, family owned and run Lubricant manufacturing and distribution company that had been a super star performer until 2013/2014. Since then, the stock traded more or less sideways and had to fight some margin compression. Since early 2023 however, Fuchs seems to be back on a growth and margin expansion path.

This very well managed company earns double digit EBIT margins and Returns on capital of >20%.The valuation is very moderate with 13,5x 2024 or 12x 2025 earnings for this very boring but high quality small cap company. Based on company projections, EPS should grow organically by ~9% plus any additional effects from share buy backs and M&A over the next 4-6 years and the current dividend of around 3,5%.