Quick Updates: Fuchs SE (Buy), Paypal Special Situation (Buy) & EVS SA Post mortem

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESERACH.

Fuchs SE (Buy)

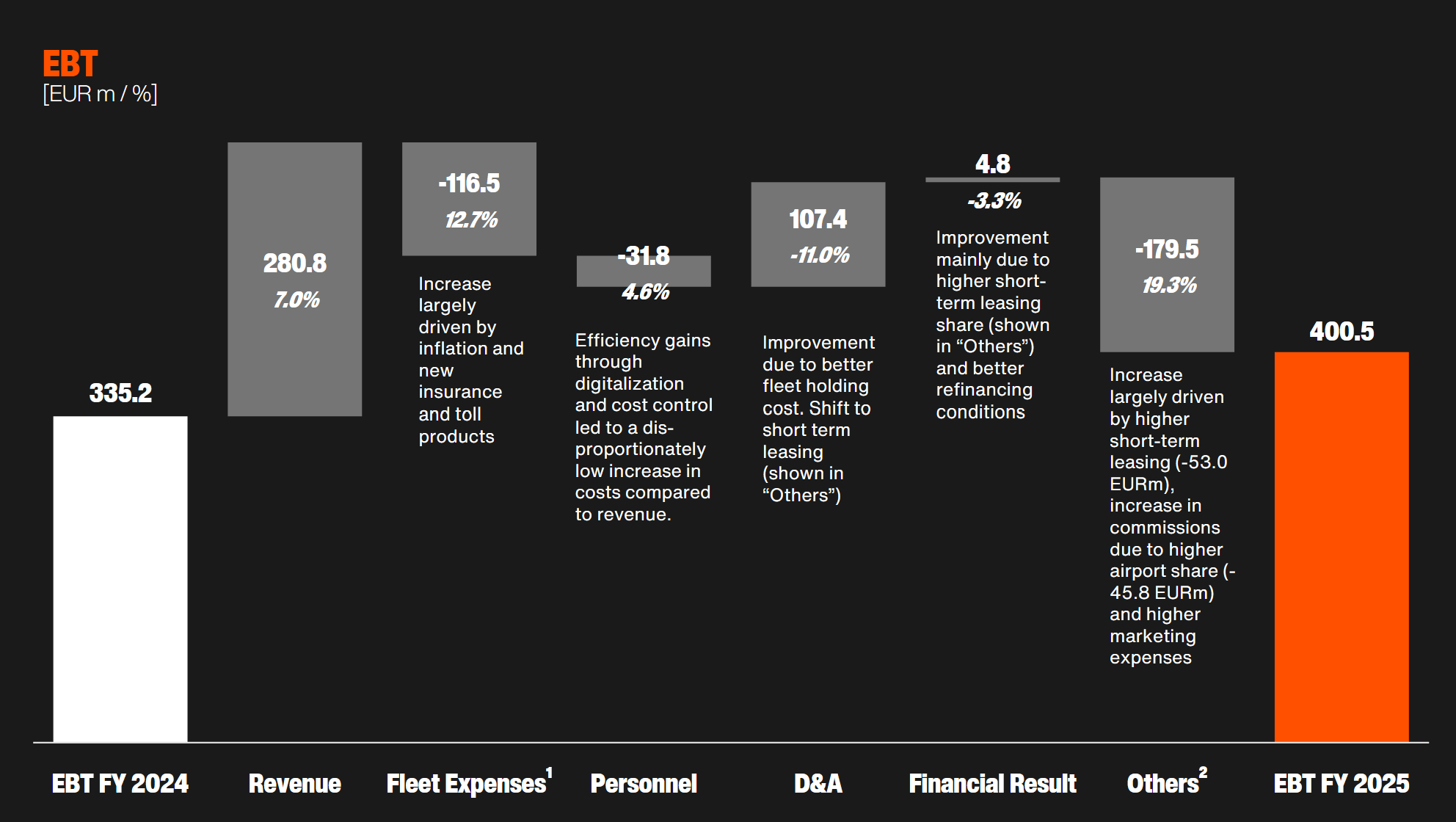

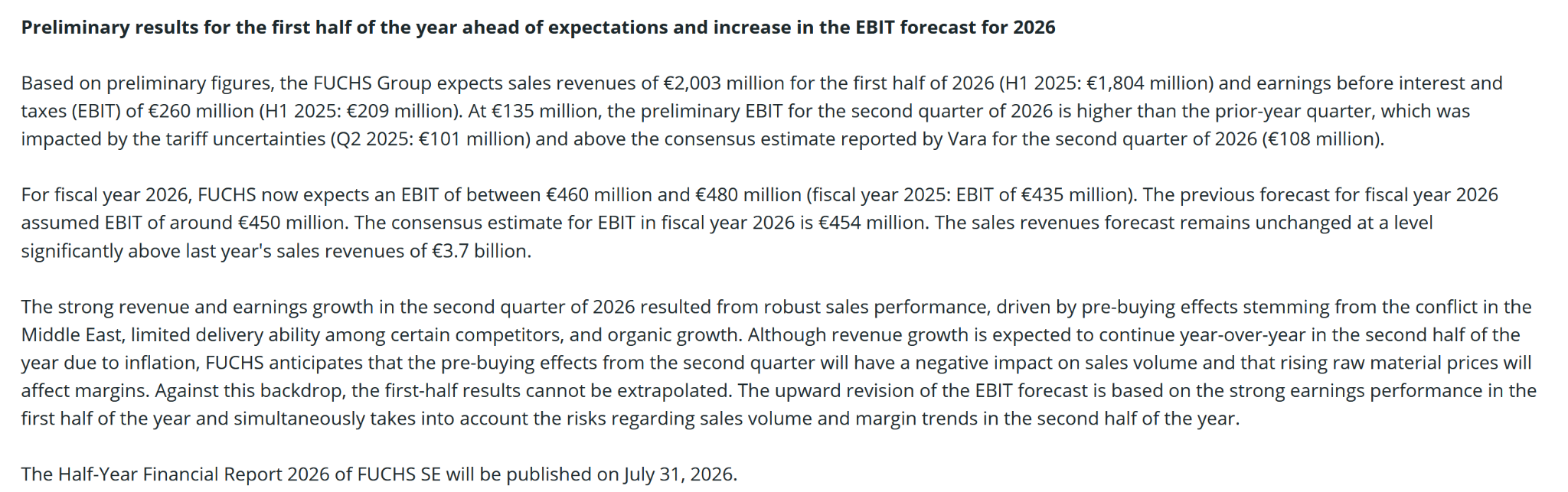

As mentioned in the comments of the initial write-up, I have re-entered Fuchs Common shares with a 2% position. I did sell Fuchs after a disappointment almost 1 year ago. So I was quite surprised that they actually announced “blow out” numbers for Q2 a few days ago:

I talked to some other investors about this and they mostly mentioned that this looks (once again) as a one-time effect with maybe compensating negative results some quarters down the road, very similar to what happened after the attack on Ukraine.

That most likely explains the very muted reaction to a 35% increase in EBIT in Q2 and a significant increase in the full year guidance that according to the release already is conservative.

I actually bought back the shares slightly higher to the level I solid them last year (33,50 EUR vs 31,50 selling price).

What I found especially interesting in the statement from Fuchs was the following passage:

“The strong revenue and earnings growth in the second quarter of 2026 resulted from robust sales performance, driven by pre-buying effects stemming from the conflict in the Middle East, limited delivery ability among certain competitors, and organic growth. “

Digging a little bit deeper one can relatively easily find articles that the Gulf region was and is a major exporter of lubricants and especially the underlying base oils that are needed for high performance lubricants.

In addition, on major base oil refinery in Qatar was directly hit by Iran according to this article:

“Approximately 44% of U.S. Group III demand is typically supplied from the Persian Gulf, but that supply is now largely offline. Damage to Shell’s Pearl GTL facility in Qatar—caused by Iranian rocket strikes—has halted production from a key source of roughly 30,000 barrels per day, with repairs expected to take at least a year. Additional disruptions stem from force majeure declarations by producers in Bahrain and the UAE, as well as the continued closure of the Strait of Hormuz, which has stranded product in the region. “

Although I don’t know exactly how Fuchs sources its base oils, it seems that for the time being that they are able to deliver while others have problems.

Of course the situation with Iran can change any day with a single Tweet, but I guess that some supply chain managers are maybe rethinking their dependence on Guld based lubricants which could be a structural opportunity for an independent player like Fuchs.

We will need to see how this develops, but I think Fuchs looks a lot more interesting now at least from my perspective.

Paypal Special situation (Buy)

In March I wrote about Paypal for the first time and back then, despite being cheap, Paypal was one for the “too hard” pile for me.

Then, after the approach from Stripe and Advent I mentioned the following:

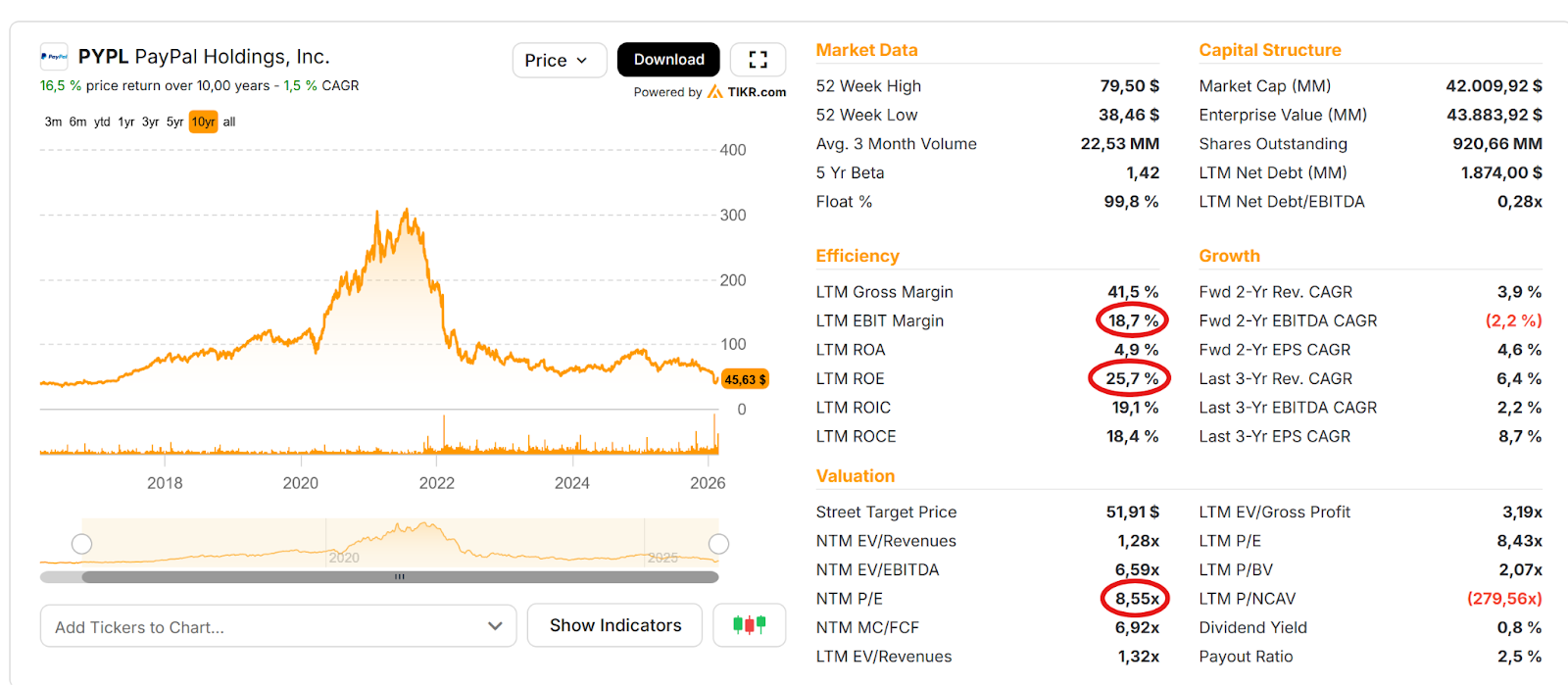

Last Friday, the stock traded at 55,5 USD, offering a 9% “discount” to the potential acquisition price which motivated me to buy a 1,5% position at that level.

The risk return ratio is not too bad at that level. The “undisturbed” price is ~47 USD and there is a pretty good chance of a higher bid either from Advent/Stripe or maybe another competitor might enter the race.

As always, one needs to prepare for volatility around any news in either direction but I think it offers a nice, uncorrelated “bet” on a potentially higher clearing price.

One key player here is clearly the new CEO whose massive bonus is tied to a stock price increase that to my knowledge is much higher than the 60,50 USD offered. So he clearly has an incentive to hold out for a high price OR a nice “golden parachute” from the buyers.

However one more thing is important to mention: This is a special situation investment for me. So if for some reason, Stripe & Advent withdraw their bid, I will sell, no matter what. For a “Value investment” I still find Paypal too hard at this stage.

At the time of writing, the Paypal share price has climbed back to 58,40 USD per share, a level where I would not buy (more).

(for some strange reason, Google Finance says Paypal is now called Adobe 😉

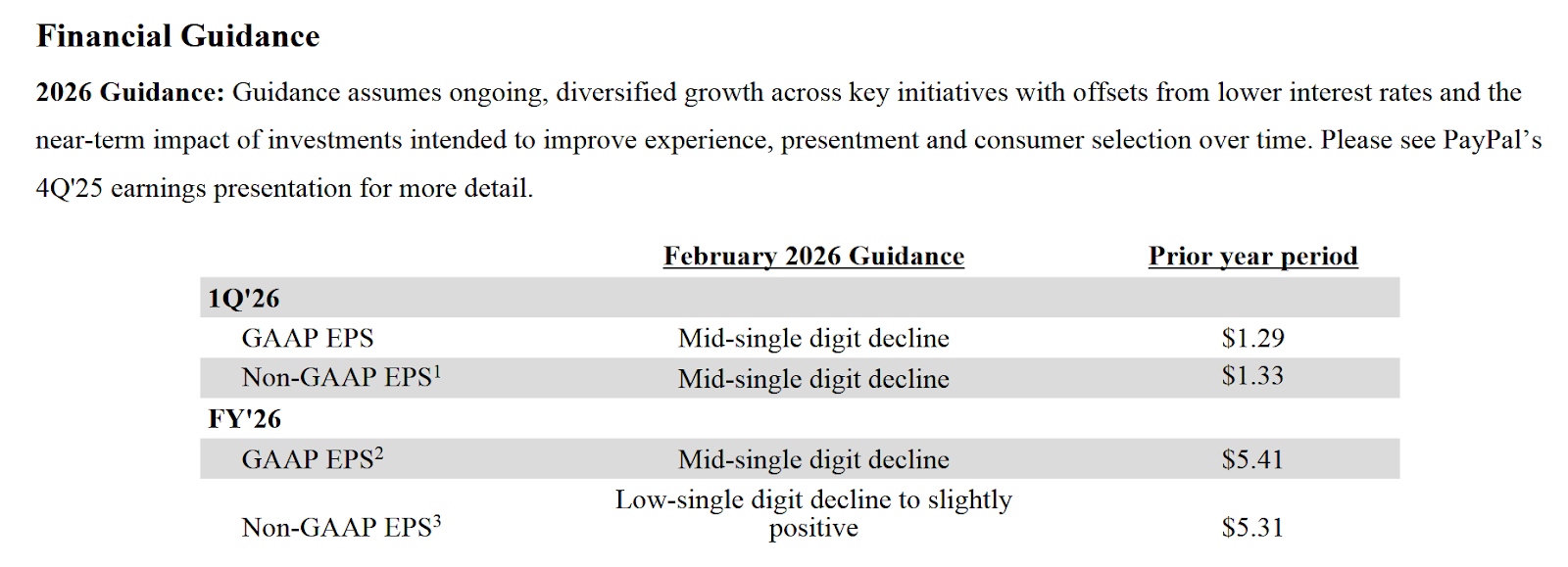

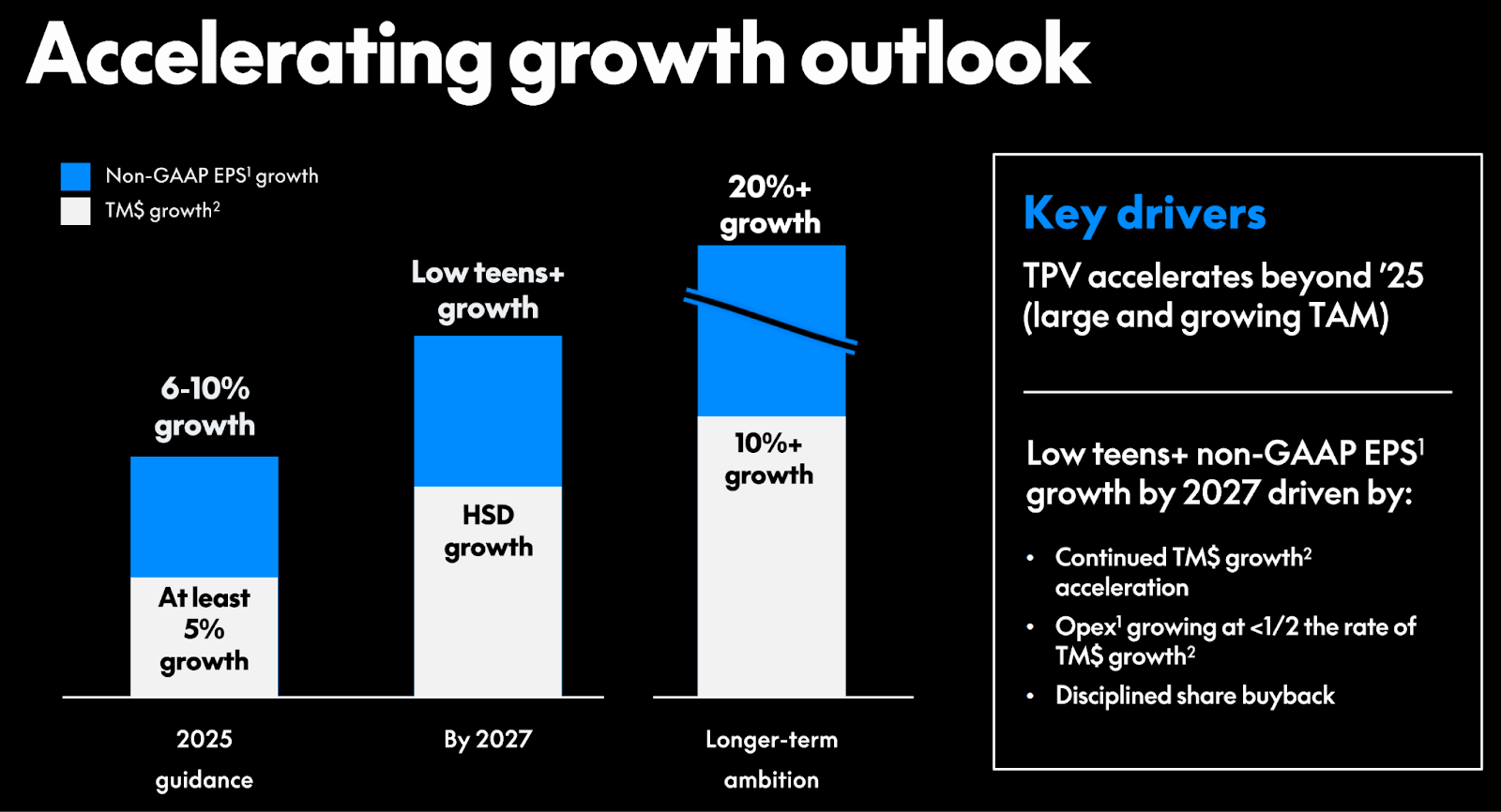

The main reason for the recent jump seems that Q2 numbers seem to have beaten expectations.

EVS (Broadcast) SA – Post mortem

I had written up EVS SA (formerly known as EVS Broadcast SA) some two years ago. The thesis was the following:

So the company had ambitious growth targets, was relatively cheap and financially super solid.

Initially, the case went well, with 2024 turning out to be a really good year.

However, 2025 started with a slight disappointment in Q1. Then the stock jumped as they had won a (biggish) contract for the Football Worldcup in Q2.

However, that was soon followed by disappointing 6M numbers. The preliminary 2025 numbers were not great, but back then the outlook for 2026 was still quite positive in March.

But then in May, together with the Q1 trading update, they already guided to the lower end of the range and the CFO lady suddenly left without direct replacement.

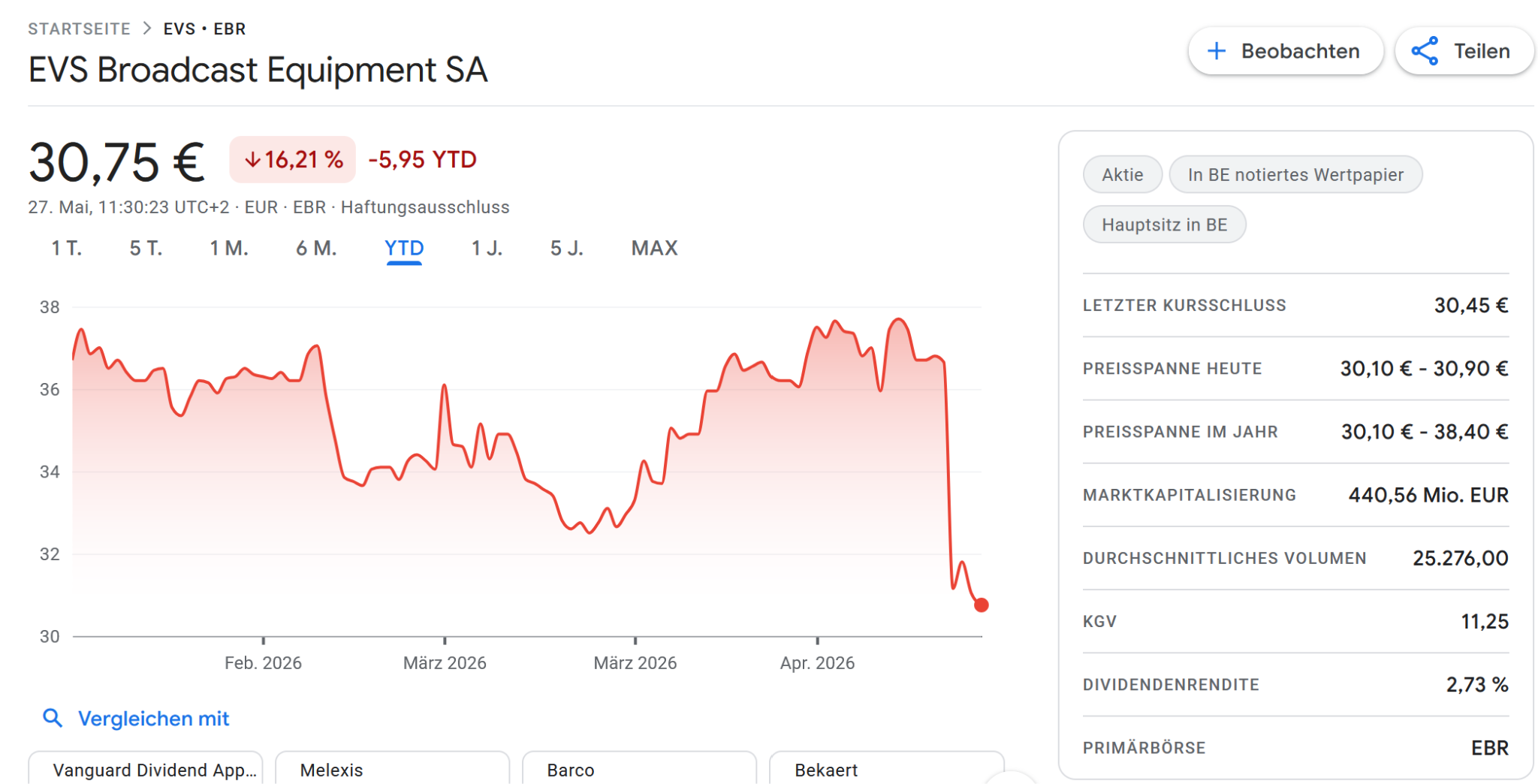

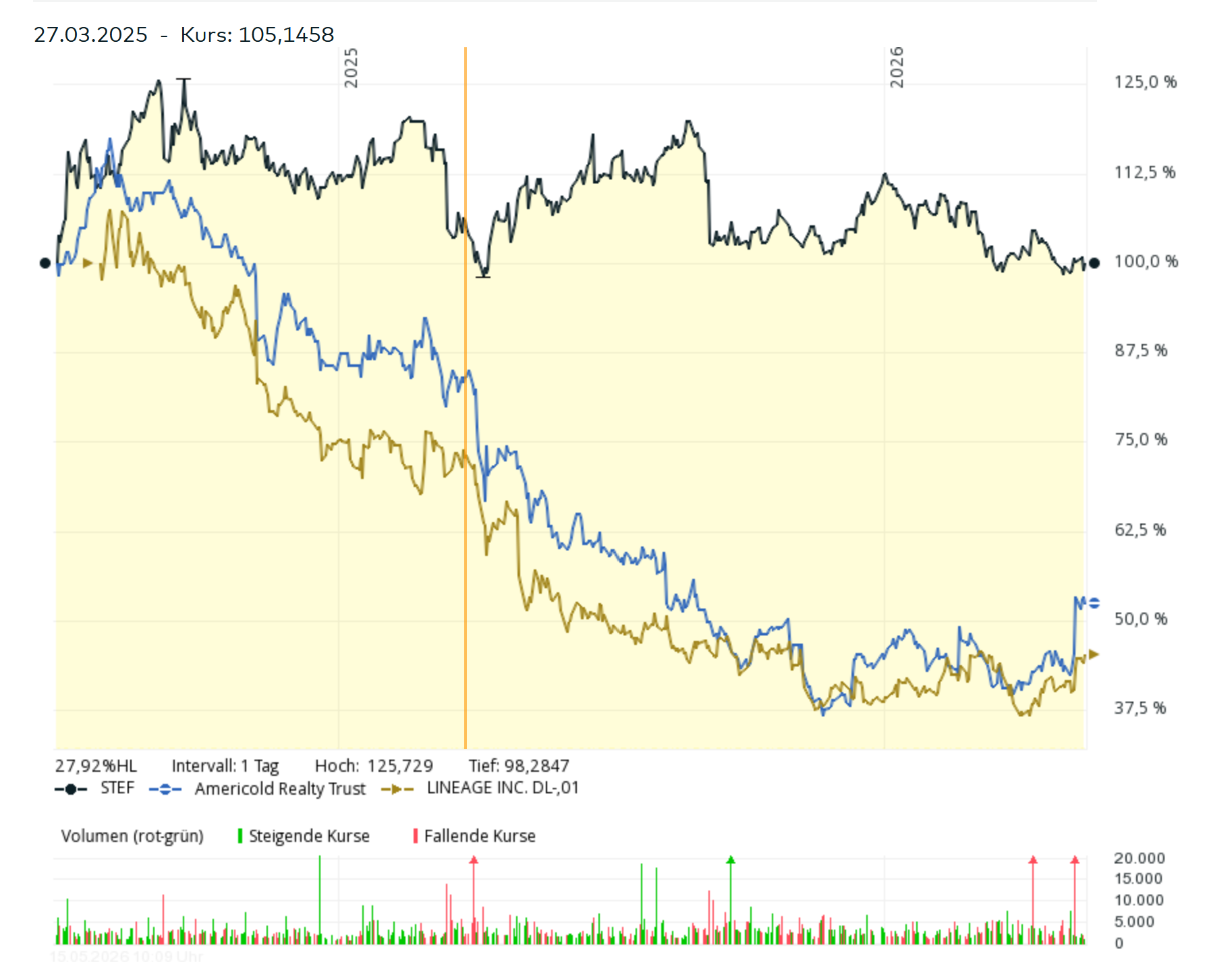

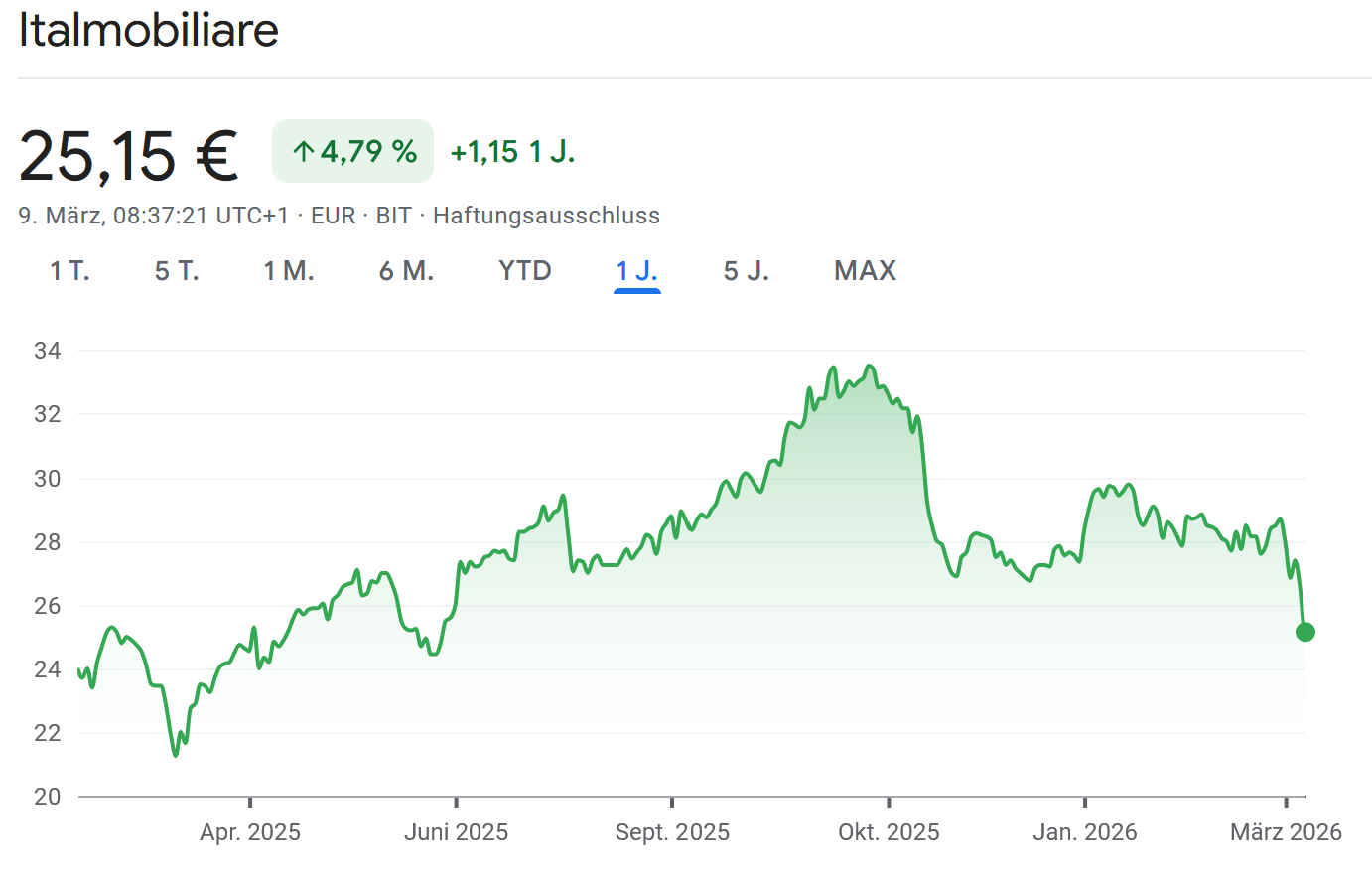

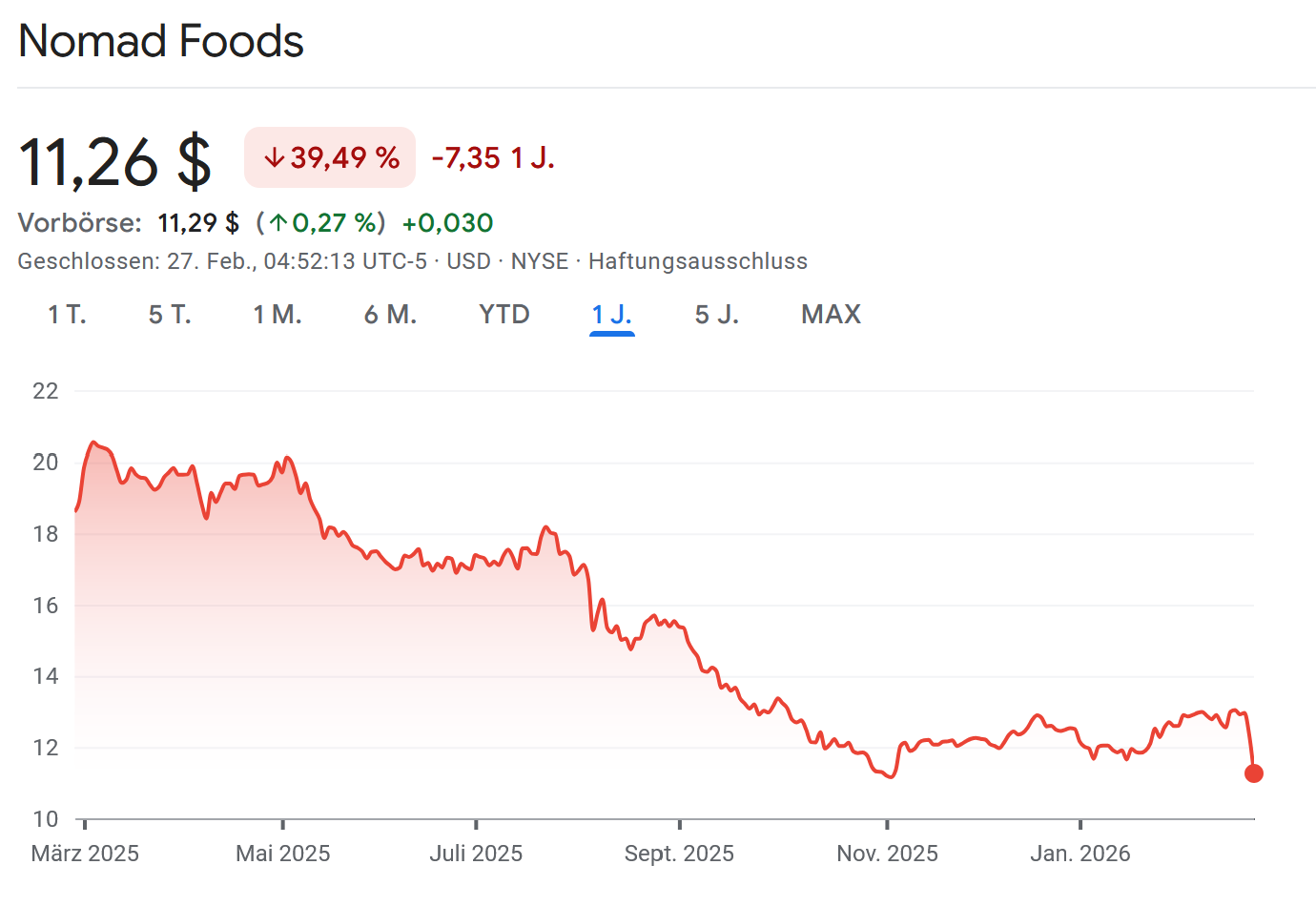

This was of course very disappointing and I started to sell part of my stake after that. We can also see that the share price is now lower than when I wrote up the stock in June 2024:

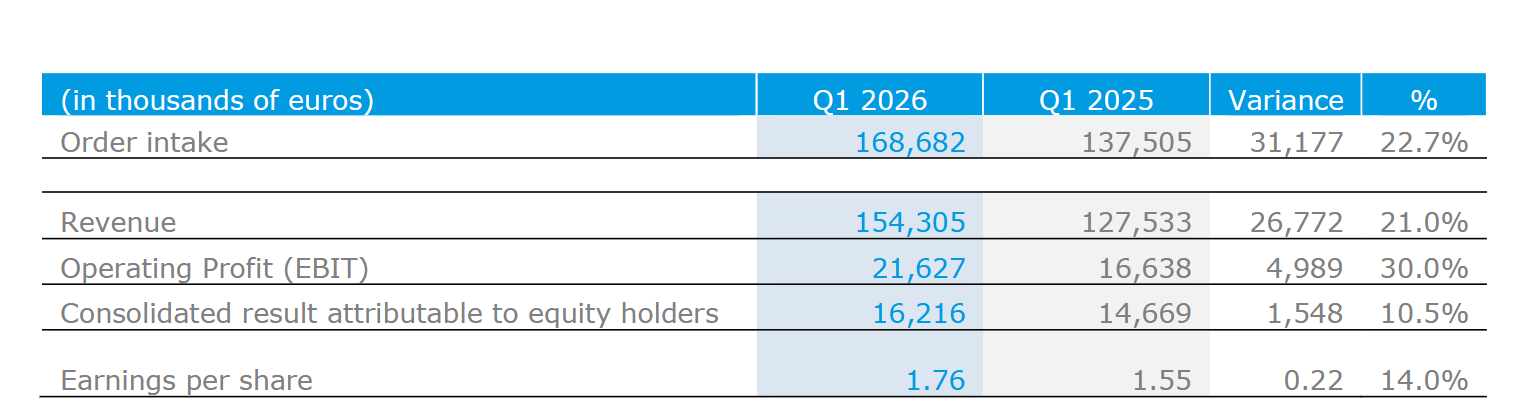

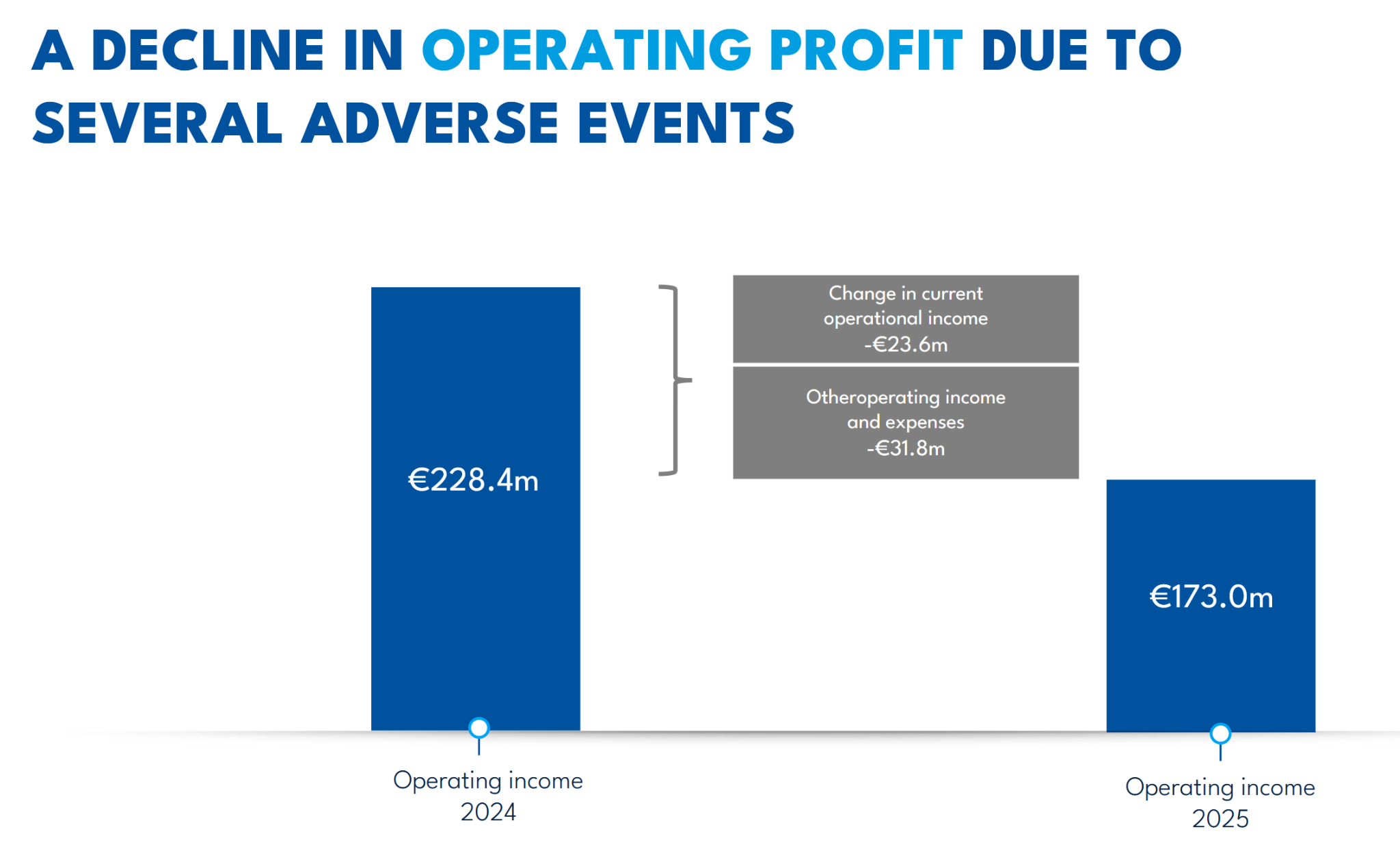

An EBIT /operating profit at the lower end of the 40-50 mn range would mean an EBIT similar to 2023 and that in a year with two very big events, the Winter Olympics and the Football Worldcup.

While that is not a catastrophe, they are now clearly far away from the 10% p.a. growth path that I had underwritten originally. To be honest, I don’t fully understand why the business is so weak.

What I also found interesting, that Canadian listed competitor Evertz has been doing very well over the past 12 months at least looking at the share price:

While Evertz struggled a little bit in the US market, that specific passage was very interesting in their latest report (that includes Q1):

So while EVS claims that the war in the Gulf is the culprit for the unsatisfactory business, Evertz speaks of “revived growth” in the Middle East. That is quite surprising in my opinion and casts some doubts on the EVS Broadcast story.

So overall, I am not that confident in EVS for the time being and decided to sell my position entirely as I see better opportunities elsewhere.