Kabel Deutschland is a stock which I have written about quite often. I was short the stock but closed out with a quite significant loss (-53% to be exact).

I am still following the stock out of interest because I think it is a prime example of a modern day high quality “stock promotion”.

Clearly, the performance of the stock since its IPO is outstanding. Without many setbacks, the stock has tripled since its MArch 2010 IPO, making it one of the most succesful German stocks in that time period:

Also the advantages of Kabel Deutschlands business model are clear:

– the business seems to be a “natural moat” business. Effectively, Kabel Deutschland makes contracts with the administers of multi family homes, so all those people become automatically clients of Kabel Deutschland and have to pay a base fee via their monthly rent bill. With this guaranteed inflow, Kabel Deutschland is then able to sell aggressively phone services, internet etc. to those clients

As a result, Kabel Deutschland is supposed to be a free cash flow machine with still significant growth potential, the rare exception in the European TelCo market. So it doesn’t matter that Kabel Deutschland has negative equity and the debt is mostly covered by goodwill and intangible assets.

Markets are clearly paying a premium for that. With a trailing EV/EBITDA of 11.4, Kabel Deutschland is ~30% more expensive than even the comparable cable operators in Europe and the US.

Recent developements

Telecolumbus acquisition

Kable Deutschland was on track to take over Telecolumbus, another regional cable operator. Taking over other regional cable operators is of course a no brainer for any aspiring cable company. Economics of scale is what counts in cable. However 3 days ago, the german antitrust office finally rejected the request from Kabel Deutschland due to anti trust concerns.

So this significantly reduces growth opportunities for Kabel Deutschland. Yes, they might be able to sell more internet etc. to existing clients but I am not sure if this really warrants the extra price paid for Kabel Deutschland

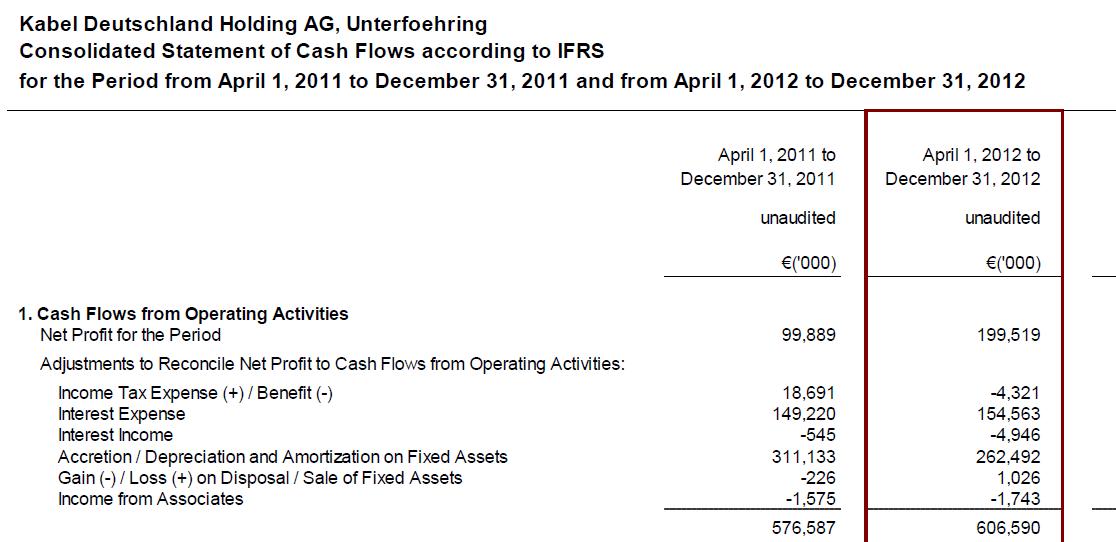

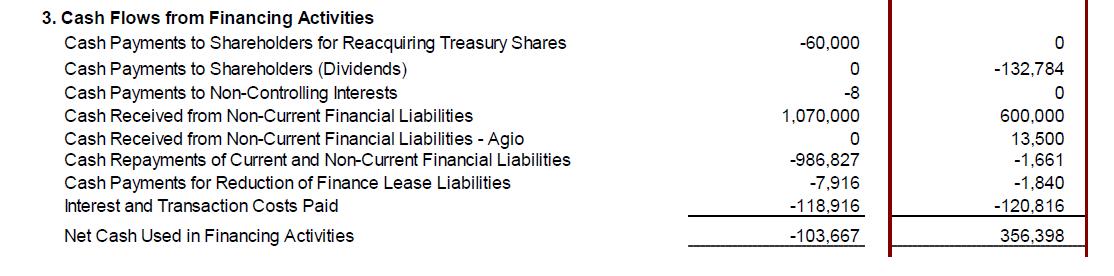

9m results

The official release came out with an encouraging dividend increase from 1.50 EUR to 2.50 EUR per share. Also all their self defined funky KPIs look fantastic.

However if you really look into the cash flow statement, one can see that 9 months free cashflow is only ~50 mn EUR, to significantly increased investments. The company even announced an “accelerated network investment” plan:

In order to enable accelerated growth, the Company intends to pull forward network investments of €300 million to be spent over the course of the next two fiscal years in addition to the Company’s existing investment plans.

Interestingly, the “operating cashflow” does not include interest charges. In my opinion, interest charges are operating, as they have to be paid regularly and there is no discretion like dividends. So in my view Kabel Deutschland currently runs free cashflow negative and dividends are paid out from the increase in debt.

All in all, one might think that those two issues might lead to a decrease of the valuation premium for Kabel Deutschland. Fat chance, because just by pure coincidence, the following story appeared in the Newspapers last week (before the other two events mentioned bacame public):

According to “insiders”, Vodafone is contemplating to take over Kabel Deutschland.

The reason seems logical: Vodafone needs to offer “quad play” services (Televison, Internet, fix line phone, mobile phones) and has already purchased in a similar fashion Cable and Wireless UK fixed line operations in 2012. So a clear no brainer.

Kabel Deutschland directly jumped more than 20% and the following bad news (Telecolumbus, 9 months earnings) were mostly ignored.

Vodafone Cable and Wireless UK acquisition

It is absolutely correct, that Vodafone acquired Cable and Wireless UK operations last year. However, what many “analysts” did not mention was the fact that Vodafone was very disciplined here.

When Cable and wireless split in two companies in 2011, there was always the rumour that Vodafone would be interested. However the waited a long time until the price was right before they came out with an announcement in April last year.

According to Bloomberg, Vodafone finally paid the following multiples:

P/S 0.3

EV/EBITDA 2.5

EV/EBIT 6.7

So Vodafone actually bought here at “rock bottom prices”. In my opinion, the days are over when Vodafone would move in and pay any price for Cable Deutschland.

In my opinion, there are also no other natural buyers for Kabel Deutschland. Liberty has already bought Kabel BW and will not be allowed to buy Kabel Deutschland. The big Telcos have enough problems already and for a PE buyer, Kabel Deutschland is already too “bootstrapped” to be interesting.

I am pretty sure that Vodafone knows that and will not rush into a Kabel Deutschland deal, if at all.

Conclusion

In my opinion, the “Vodafone Insider story” was a prime example of stock promotion, making the stock jump with a somehow plausible story and making people forget about the rather sobering underlying picture.

I am therefore once again, going to establish a short position in Kabel Deutschland, betting against a take over by Vodafone at a premium. As always with shorts, I will start with a 1% position.

At current prcies, I believe the risk/return ratio is quite good, as I don’t believe that Vodafone will buy at current prices (or even pay a premium) and there is a good chance that Kabel Deutschland’s valuation will approach average levels at some point in time.

Edit:

In my “home forum” benny_m posted a interesting link regarding potential cable regulation in Germany:

http://www.teltarif.de/kabelnetz-regulierung-bundesnetzagentur-homann/news/49249.html

That might be a game changer…….