Deeply discounted rights issue watch: KPN NV (NL0000009082)

I had briefly covered deeply discounted rights issue as a potential “special situation” opportunity a couple of weeks ago.

Now, with KPN, we have an interesting non-financial candidate. This is what KPN issued today:

Dutch telecoms group KPN confirmed a €4bn rights issue to shore up its capital position after heavy expenses on bandwidth that have led to dividend cuts and lower profit margins.

The company announced the move along with its 2012 annual results, which showed a 3.5 per cent drop in revenues and a 12 per cent fall in earnings from the year before.

As one might expect, the stock tanked some 16% or so. Currently, at around 3.45 EUR per share, KPN has a market Cap of only 5 bn EUR, so raising 4 bn via a rights issue might require a large discount on potential new shares.

The “wild card” in this game will be Mexican Billionaire Carlos Slim who owns currently 27.5% of the company. If he fully participates as lead investor and even taking up more than his share, then the “forced selling” aspect might not be too relevant.

If for some reason, he would refuse to participate, the situation will become very interesting.

Just for fun, let’s look how the performance was for Unicredit. I would distinguish the following events / time periods:

– 4 weeks before announcement

– announcement day

– period between announcement and price setting (for new shares)

– price setting day

– period between price setting and start trading of subscription rights

– trading period

– 4 weeks after end of trading period

First the relevant dates:

| Unicredit | |

|---|---|

| Announcement first trade date | 14.11.2011 |

| Price setting of rights issue | 04.01.2012 |

| First trade date subscr. rights | 09.01.2012 |

| Subscription trading until | 01.02.2012 |

| Discount | 43% |

| New share | 2 new for 1 old |

Now the relative performance:

| Performance | UCG | MIB | Relative |

|---|---|---|---|

| – 4 weeks before announcement | -18.35% | -4.98% | -13.37% |

| – Date of announcement | -6.18% | -1.99% | -4.19% |

| – announcement until price setting | -14.40% | 2.95% | -17.35% |

| – day of price setting | -17.27% | -3.65% | -13.62% |

| – price setting to start trading | -26.46% | -4.45% | -22.01% |

| – trading period | 73.75% | 12.94% | 60.81% |

| – 4 weeks after trading period | 0.05% | 2.82% | -2.77% |

| – 6 months after trading period | -32.25% | -11.39% | -20.86% |

| – 12 months after trading period | 12.53% | 9.53% | 3.00% |

In the Unicredit example, clearly the period where the subscription rights were traded showed the best relative performance of the shares. Interestingly, on the announcement day, the price drop was much less in percentage points than KPN. This might have to do with the short selling ban which was in place (at least to my knowledge) when Unicredit announced the rights issue.

Again for fun, a quick look at Banco Popular’s rights issue from the end of last year.

Again the dates first:

| POP | |

|---|---|

| Announcement first trade date | 01.10.2012 |

| Price setting of rights issue | 10.11.2012 |

| First trade date subscr. rights | 14.11.2012 |

| Subscription trading until | 28.11.2012 |

| New share | 3 new for 1 old |

and then relative performance to the IBEX:

| Performance | POP | IBEX | Relative |

|---|---|---|---|

| – 4 weeks before announcement | -3.95% | 5.11% | -9.06% |

| – Date of announcement | -6.17% | 0.98% | -7.15% |

| – announcement until price setting | -29.95% | -1.71% | -28.24% |

| – day of price setting | 4.56% | -0.90% | 5.46% |

| – price setting to start trading | -8.86% | 1.39% | -10.25% |

| – trading period | 8.12% | 2.16% | 5.96% |

| – 4 weeks after trading period | -6.71% | 3.74% | -10.45% |

One can see a similar pattern first, with the stock losing 4 weeks before announcement, as well as on the announcement date until the final price setting. However of the date of price setting, the stock jumped, until loosing only a little bit until starting of the trading period.

Then however, the gains within this period were relatively low compared to Unicredit. Overall it looks a lot less volatile than Unicredit, so maybe less forced selling here.

Back to KPN:

Other than Unicredit and Banco Popular, KPN had outperformed the AEX almost +11% in the last 4 weeks, so today’s large drop might compensate for this (unjustified) outperformance.

If the other two stocks are any guide, one could still expect lower prices until the price for the new shares will be set.

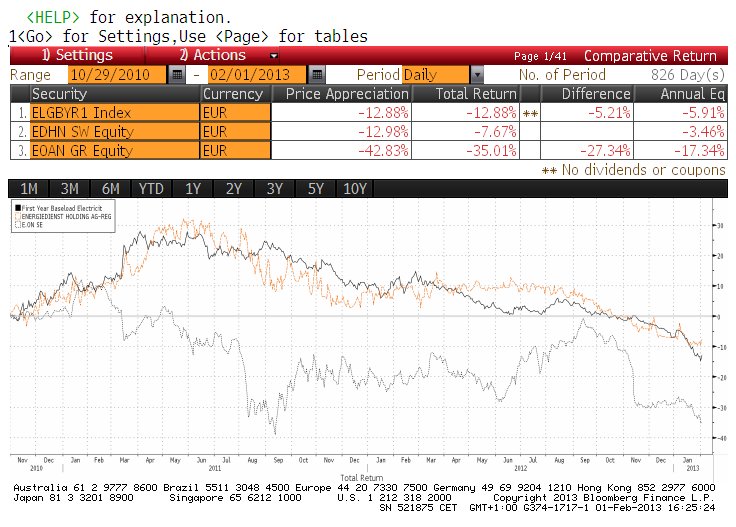

The stock price of KPN look really really ugly long term:

But make no mistake, any company which needs to go into deeply discounted rights issues is in trouble. This is “distressed” territory.

(…to be continued….)