Energiedienst Holding AG (ISIN CH0039651184) and German electricity prices

I started my small 2013 utilites project with E.On 2 weeks ago. Instead of working through the list of German utilities I wanted to focus on Swiss listed Energiedienst Holding AG first.

Energiedienst is a slightly unusual stock. It is listed on the Swiss stock exchange, but its balance sheet is in EUR. The company basically runs a number of big Hydro power plants along the Rhine River plus some smaller Hydro Power plants in Southern Germany and Switzerland as this map shows:

Market cap: 1.3 bn Swiss Francs

P/B 1.1

P/E 12.0

EV/EBITDA 7.1

Dividend yield 2.3%

From a simple valuation point of view, Energiedienst does not look overly attractive, however one should mention that they do have net cash which is quite uncommon for utilities.

The company is majority owned by German ENBW (67%) plus a company called “Services Industriels de Genève (SIG)” which bought a 15% stake in 2011 from ENBW (remark: ENBW itself is in quite big trouble because of the Nuclear exit in Germany).

Business model

In addition to the Hydro plants, Energiedienst owns a distribution network with around 750 tsd clients in Switzerland and Southwestern Germany. The focus is clearly Germany with more than 80% of sales there. Energiedienst produces around 25% of its energy itself, the rest is bought in the market.

The interesting point is that their own electricity production is almost 100% Hydro power. Hydro power, in contrast to power from fossil fuel, is more or less a pure fixed cost business. You build the hydro plant, depreciate and that’s it. If electricity prices go up, you earn more, if they go down you earn less. You don’t have to worry about oil or coal prices. On the flip side, hydro power depends on the amount of water available, so in dry years you can produce less or more in wet years which introduces some uncertainty.

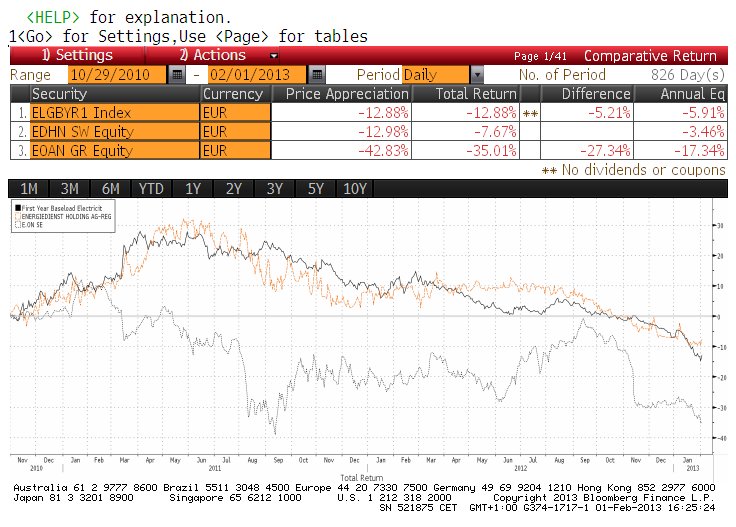

But in any case, a Hydro Power “pure play” is more or less a “bet” on electricity prices. In order to check this theory, I let’s look at EDHN’s share price (in EUR) against 1 year forward prices for German electricity (as a comparison, I plotted E.on as well):

I find it fascinating that over the past 2.5 years, Energiedienst more or less directly followed German power prices. We can see that E.on is much more volatile and most likely exposed to general stock market fluctuations.

Just for the complete picture a history of German wholesale electricity prices since 2007:

It is interesting to see that German power prices seem to be at the lowest level since the beginning of this time series in 2007. After the surprise phase out of nuclear power after Fukushima and the corresponding propaganda from E.on & Co, one might have expected exploding electricity prices. But it looks like that the new supply of alternative energy plus maybe reduction in consumption led to a dramatic decrease in electricity prices.

Digging deeper, I found for instance this German publication from 2011 which confirms the point, that the subsidized renewable energy will lower electricity prices in general. So for a renewable hydro player like Energiedienst, the subsidies to solar and wind have the “perverse” effect of lowering the profit of this very cheap type of electricity significantly.

The “trick” is that the electricity distributors have to buy the renewable electricity at fixed subsidized prices, but have to sell it at current market prices into the German electricity exchanges. The difference then gets charged to consumers. According to the paper, the electricity price clears at the level of the most expensive supplier. The mechanism for the renewable providers however introduces practically a big source of potentially extremely cheap electricity as it gets sold at market prices no matter how low they might be and “unelastic” to the actual demand.

Due to the low interest rates, subsidized wind parks and solar plants are still attractive investments despite the price for electricity being at multi year lows and demand being rather weak.

So the low prices are not a result of low demand, but mostly of subsidized renewable energy which will be sold as long as the price is higher than zero.

Zero hedge just had a post in its usual style, claiming that the falling energy prices are a harbinger for falling stock prices. That is correct for utilities but other than that it is just a result of the mechanism described above.

Summary:

The current system for renewable energy in Germany (selling renewable electricity into the market at any price with the consumer paying the difference) is hell for “traditional” utilities including hydro power.

The German utilities have maybe underestimated the extent of renewable production, otherwise they could have done the exactly same thing themselves. Now howver, the are in a kind of “death grip” between having to run their expensive black coal and gas plants for peaks and the articificially low electricity prices. Combined with unfavourable natural gas delivery contracts, especially for E.on the air will remain quite thin.

So unless something changes significantly, German utilities (including Energiedienst) will need a long long time to adjust capacity and change their business models.

Warren Buffet seems to be much more clever: If you can’t beat them, join them. I think this is the reason why his US utility is investing so much into Solar and Wind.

Der Kurs hat nachgegeben. Strom ist billiger geworden: http://www.eex.com/de/Marktdaten/Handelsdaten/Strom/Phelix%20Futures%20|%20Terminmarkt/futures-table/2013-10-28

Die Firma schreibt im Halbjahresbericht: “Mit einem konsequenten Kostenmanagement steuern wir gegen und wir hinterfragen auch unser Geschäftsmodell.”

Obwohl die Produktion durch günstige Bedingungen über Erwartung ausgefallen ist, ist der Gewinn eingebrochen.

Die sehr hohe Korrelation mit dem Strompreis macht Energieholding für die Watchlist interessant. Die Futures zeigen zwar keinen Anstieg in den nächsten Jahren, aber irgendwann könnte sich das ändern.

Aufgrund des klaren Geschäftsmodells wäre Energieholding für mich ein klarerer short als RWE basierend auf fallenden Strompreisen in DE vor Jahren gewesen, da RWE wesentlich diversifizierter z.B. DEA ist.

Energiedienst ist eine klare Wette auf den Strompreis. Inputkosten nahe null, relativ hohe Fixkosten.

You have written renewable energy will be sold as long as the price is higher than zero. Actually the price went already below zero several times.

The EEG is even impacting foreign competitors like CEZ as the czech prices are similiar to the german ones.

technically this is correct, there were even negative rates. Also you are correct, the low German prices will influence the neighbouring countries.

At university I attended only one class electrical engineering. Maybe I will never grasp a full understanding of electricity. Many things are counterintuitive for me. The grid is very complex. There should be better solutions than selling at e negative price.

At the end of 2011 I invested in RWE because I thought their coal powerplants would be cheapest source of energy. Fracking in the US should lower coal price but not so much gas price in europe. This was right and I trimmed significantly around 36. In retrospective this was sheer luck. Dynamics are high and regulatory risk remains. Powerplants are very long life assets and I underestimated the will to operate at a loss or not to shut down permanently for gas powered plants. My strategy for eon and rwe would have been to let the grid go broke, cut cost and put pressure on regulator instead of stabilising the grid and eating losses.

No problemn and no “hard feelings”. For myself, I honestly didn’t really understand the mechanics. I had thought that the Nuclear exit would have had a much bigger impact, driving electricity prices higher.

Bei firmen die produkte herstellen die die konkurenz auch herstellen kann indem sie auch eine fabrik errichten dann finde ich den buchwert ganz gut um zu sehen ob die firma substanz hat. Natuerlich muss sie auch gewinne machen.

#julius,

ja, ich finde den Buchwert auch ein ganz nützliches Kriterium, allerdings nur eines von vielen.

mmi

No surprise. In Germany large overcapacities of electricity production emerge al long as the renewable are pressed in the market.

so you were short utilities all along ?

No I’m at the beginning of my investment career and started sort selling not until a few month ago. I doubt utilities are good shorting candidates because, they usually pay high dividends.

Mit tatsächlichen mein ich die tatsächliche abschreibung was halt wirklich nach so und soviel jahren erneuert oder repariert werden muss. Bilanzen die mit goodwill aufgeblasen sind mag ich zum beispiel gar nicht(zb heidelbergcemet, tui-travel) Wenn ich richtig liege ist goodwill der nicht abgeschrieben wird der wert der sich durch markenwert und synergien rechtfertigen lässt.

Bei Wasserkraftwerken ist der buchwert aber auch nicht entscheidend sondern der gewinn und wie lange ich den gewinn mache bzw eeg-gesetz.

der Buchwert bei EDHN scheint mir (noch) mit den entsprechenden Gewinnen und Free cashflow abgesichert. Allerdings sehe ich auch keine stillen reserven o.ä.

Buchwert von Anlagevermögen hängt immer vom Gewinn ab, ausser es handelt sich um anderweitig vertwertbare Gegenstände wie Immobilien etc.

Hmmh gibt es bei iffrs eine Abschreibung die über der tatsächlichen liegt?

– Gehört jetzt nicht zum thema – hab mir nach der ivg wandelanleihe auch die draegerwerk genüsse ins depot gelegt – die gehen ja ab wie nochmal was. Verkaufst du die erst zum preis von 10 vorzügen oder wo würde deine grenze liegen 8 vorzüge?

Wie seriös ist denn der Buchwert? Wasserkraftwerke sind doch oft alt und sicherlich auch ordentlich abgeschrieben.

ROIC ist ungefähr 6-7%, d.h. wahnsinnig viel reserven sind da vmtl. nicht. Ausserdam haben sie gerade ziemlich viel renoviert z.B. in Laufenburg. Das rentiert sich jetzt natürlich nicht mehr ganz so.

Problem with Energiedienst: Most of their capacity is “flow”. You cannot leave the rhine dry for a couple of hours….

One of Energiedienst’s subsidiaries, EnAlpin AG, operates storages reservoirs. Their contributions to EBITDA is €42m. Not something to built an investment thesis around, but not small potatoes either.

thanks for the info. They are trying to do more projects in Switzerland, but I think the capacity is limited.

C02 supply side is political and demand is price elastic. I can’t put a value to it. This means I would assume price to stay flat forever for a valuation…

From an academic point of view electricity is no true commodity like gold etc.

I will look at energiedienst when I have more time. I think their electricity is worth more than the price at the exchange because of the lower carbon footprint. Shouldn’t hydro power be exempt from the eeg surcharge? It seems counterintuitive to charge such clean energy extra.

Would love to read your piece about electricity trading maybe with a link to enron 🙂

Electricity is no commodity as it can not be stored losless. This is why I don’t understand the price chart of electricity. Is this a volume weighted daily average?

Energiedienst could be interesting if CO2 prices rise. I think the exchange makes no difference regarding carbon footprint of traded electricity.

Martin,

the index is called “base load” but it is defintiely a commodity type contract.

Spotwise electricity is traded on a hourly basis, so Elctricity for 1 pm has another price than 1 am.

For instance today, 1 megawatt at 7pm costs 55 EUR, 5am is cheapest at 10 EUR. So storing electricity migth be the “killer” business.

Maybe i have to wirte a post about elctricity trading.

Interstingly, CO2 prices are at an all time low. Co2 certifcates are almost worthless.

One of the benefits of hydropower is that it can be used as a storage mechanism. During peak supply hours the surplus electricity can be used to pump water uphill by reversing the turbines, thereby refilling the water reservoirs.

The trouble is that the geography needs to be right. The ideal situation would have cascading reservoirs so that the water can be distributed without too much energy loss. Norway with its fjords has a geography like that, but I’m not sure about Switzerland.