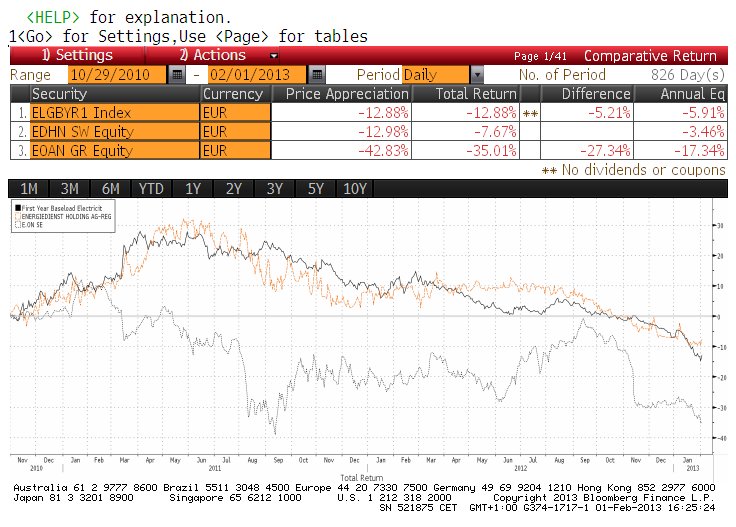

Almost exactly one year ago, I looked at Energiedienst Holding, the Swiss/German Hydropower utility.

That was my summary from last time:

The current system for renewable energy in Germany (selling renewable electricity into the market at any price with the consumer paying the difference) is hell for “traditional” utilities including hydro power.

The German utilities have maybe underestimated the extent of renewable production, otherwise they could have done the exactly same thing themselves. Now however, the are in a kind of “death grip” between having to run their expensive black coal and gas plants for peaks and the artificially low electricity prices. Combined with unfavourable natural gas delivery contracts, especially for E.on the air will remain quite thin.

So unless something changes significantly, German utilities (including Energiedienst) will need a long long time to adjust capacity and change their business models.

So the first questions is of course: Did something change ?

Well, firstly, the stock price of Energiedienst dropped a further -25% form around 38 CHF to currently around 29 CHF. So just from the pure valuation point of view, the stock clearly looks cheaper:

P/B 0.86

P/E 12

EV/EBIT 12

EV/EBITDA 7

Div. Yield 5.1%.

Energiedienst released preliminary numbers for 2013 today. At a first look, it doesn’t look pretty. EPS came in at 1.99 EUR per share, the third consecutive decline since the peak at 2.70 EUR in 2010.

Looking further into their preliminary numbers, I was especially surprised by this:

|

|

2013 |

2012 |

change in % |

| EBIT |

in Mio. € |

79 |

99 |

-20% |

| EBIT Segment Deutschland |

in Mio. € |

53 |

56 |

-6% |

| EBIT Segment Schweiz |

in Mio. € |

27 |

43 |

-38% |

Profit in Germany was only slightly lower, but we see a big drop in Switzerland which is surprising. In the text they mention that they took a special charge for long-term electricity purchases in the first half-year so one can assume that this has to do with the Swiss business. So not surprisingly, Free Cash Flow looks better than earning:

|

|

2013 |

2012 |

change in % |

| Free Cash Flow |

in Mio € |

79 |

83 |

-5% |

| Bruttoinvestitionen |

in Mio. € |

44 |

57 |

-23% |

This results in a total net cash balance of 146 mn EUR at year-end or 4.40 EUR per share which is almost 20% of the current market cap. So “cash adjusted” P/E is around 10. Additionally, they announced some kind of strategy change and review, however without any real details

OK, so we do have a relatively cheap but declining business, why bother ?

First, at least to me it looks that Electricity prices have at least for now stopped their free fall as those two charts show:

I am clearly not an expert on electricity prices, but with the currently mild winter (or no winter at all), I would have expected a further drop but that doesn’t seem to happen at least for now.

Political environment

Since last year, again some things have changed. We have now the “GroKo” in Germany, the coalition between the two large parties, conservative (CDU) and Social democrats (SPD). Interestingly, the boss of the junior party SPD, Sigmar Gabriel, has taken over the responsibility for Energy.

As I described a year ago, under the current system, mostly retail clients have to pay a surcharge in order subsidize above-market prices offered to the owners of solar and wind power plants. Many large companies are not subject to this “tax”.

The surcharge is increasing every year, both because of lower wholesale prices and additional capacity. However, pressure is building up against this system from many sides. Clearly, the established utilities are fighting against this as hard as they can and threaten to switch of expensive gas-fired power plants which are essential for net stability. But now, also the EU commission started to look into the exceptions for large companies already in December.

Also the core voters of the SPD are mostly lower-income recipients which are most effected by increasing electricity prices along rising rents. So Sigmar Gabriel, the SPD energy minister has to do something in order to stop further retail price increases or he will have no chance of winning the next election. Some ideas were already floated, mostly a limitation of future renewable capacity and lower rebates in the future. The concept drew a lot of critic from all side, although some parts, especially the requirement for direct marketing of renewable power doesn’t seem to be that bad.

In parallel, the bankruptcy of wind energy “pioneers” like Prokon shows that even under current high transfer payments, the big boom in new renewable energy seems to be mostly over and I guess investors will be much more careful in the future.

On top of that, the big utilities are taking out a lot of conventional capacity in Germany, party also in order to increase the pressure on the politicians.

So without being an expert in those issues, it looks like that the “tide might be turning” at some point in time in the future with regard to electricity prices or at least that they are not falling that much more. But this is clearly my own opinion and cannot be supported by a stringent theory or facts.

But why Energiedienst ?

As I have written before, the big traditional utilities like RWE, EON etc. have a lot of other problems, like too much debt, nuclear liabilities, pensions, problematic foreign subsidiaries etc. Even Verbund, thy Austrian Hydro Power utility has a lot of issues with Italian and other foreign investments. Energiedienst, on the other hand does not have those additional issues.

Energiedienst still looks more expensive than its peers:

| Name |

P/E |

EV/T12M EBIT |

EV/EBITDA T12M |

P/B |

Dvd 12M Yld – Net |

Net D/E LF |

| |

|

|

|

|

|

|

| ENERGIEDIENST HOLDING AG-REG |

11,8 |

10,2 |

5,9 |

0,8 |

5,2 |

-7,8 |

| VERBUND AG |

9,4 |

9,8 |

4,8 |

1,1 |

3,8 |

70,5 |

| RWE AG |

108,3 |

7,2 |

3,0 |

1,5 |

7,4 |

77,9 |

| MAINOVA AG |

15,4 |

50,5 |

23,3 |

2,3 |

2,4 |

76,4 |

| E.ON SE |

12,2 |

8,2 |

|

0,7 |

8,3 |

45,2 |

| ENBW ENERGIE BADEN-WUERTTEMB |

51,0 |

13,0 |

6,1 |

1,4 |

3,1 |

43,0 |

| LECHWERKE AG |

21,7 |

21,6 |

14,7 |

3,1 |

2,8 |

-55,8 |

They do not jump out of this comparison table as the “super cheap” utility. But if we look at Lechwerke in comparison, a comparable, regional, Hydropower utility in Bavaria owned by RWE, sometimes quality is honored with very rich valuations.

In my opinion, the quality of Energiedienst, especially in comparison to EON, RWE & Co is not reflected in the share price. Clearly they suffer as well from current electricity prices and they are not a growth stock, on the other hand, as a hydropower generator without variable input cost, they will benefit the most from increasing prices.

The downside at the current level is in my opinion relatively protected, unless they do something really stupid with their net cash. This is in my opinion the key issue to watch going forward. Energiedienst will generate a lot of cash as reinvestment requirements will be rather limited. If they owuld actually start ti buy back shares, this couldbe a nice surprise but there is no indication that they willdo so.

I am aware that buying a German utility stock now is a pretty contrarian play and many people will say EON and RWE are cheaper and could more speculative upside or not to invest in utilities at all. My focus however is more on the downside, where I think Energiedienst is much better protected than the big, indebted players. So overall, I think the “full” risk/return relationship of Energiedienst is better.

Summary:

An investment into Energiedienst is clearly a bet on constant or higher electricity prices based on potential political changes, so it is rather a “special situation” investment with regard to potential regulatory changes from the current, unsustainable status quo. What I like about this bet is that to a large extent this will be driven by political actions which will be either uncorrelated or even negatively correlated to the overall economic situation and hence, to the rest of my portfolio.

My return target over 3 years would be the annual dividend of currently 5% plus a stock price increase of ~30% which would indicate a target P/E of 13-14 at current Earnings (ex then cumulated cash).

So for the portfolio, I will initiate a 2.5% position for the “special situation” bucket at ~29.50 CHF / 24.50 EUR per share.