David Einhorn: Nice Q4 letter but E.On as a long pick ? Really ? C’mon !!!

As this has turned out to be a very long post, a quick “Executive Summary”:

David Einhorn has published that German utility E.ON is one of his major new long positions. Based on what I have written in the past about E.On, I do think his summary investment rational has some serious flaws, mainly:

- buying management’s “spin” that the recent share price decline was only caused by uncertainties about nuclear provisions

- assuming a quick and very benefitial (for E.ON) solution for nuclear liabilities

To me it looks like that he tries to come up with some short term, rather risky “bets” in order to make good on his horrible 2015 performance as quickly as possible.

As a new shareholder in Greenlight Re I have to seriously rethink if I want to stay invested, however as a German tax payer I might also be biased in this case.

A few days ago, Greenlight Capital sent out their Q4 2015 letter to investors , explaining their catastrophic performance for 2015.

The letter itself is clearly a “Must read” as Einhorn adresses all the issues very openly. He even manages to make some pretty good jokes such as the investment advise of his children:

“Dad, why don’t you just short your longs and long your shorts?”

After critizing Einhorn a couple of times (Consol Energy, Aercap, SunEdison, Go Ups, Delta Lloyd), I actually invested into his abilities via Greenlight Re. My case is that good asset managers often come back strongly after a bad year (or three) if they stick to their strategy.

First the good news:

A few days ago, Greenlight Re came out with an 8-K saying the following:

On January 19, 2016, Mr. Einhorn spoke at a private investor conference and provided certain information relating to the client accounts that Greenlight Capital, Inc. and its affiliates manage, including ours. To comply with Regulation FD, the following information is hereby provided:The managed account of GLRE, for the period from January 1, 2016 through January 19, 2016, reported an estimated investment loss of 1.6% net of fees and expenses. As at December 31, 2015 the account managed by DME Advisors on behalf of GLRE had net invested assets of $1.1 billion.

Yes, he lost money again, but with the S&P being down aroun -7,9% and the Russel 2000 being down -12,3%, this is actually a pretty good number.

But then: E.On – C’mon !!!

However my positive mood darkened when I actually read about his first new long position was (highlights are mine)

We established several new longs during the quarter: E.ON (Germany: EOAN) is one of Europe’s largest utilities, owning power and gas grids, and power generation from renewable, fossil and nuclear sources. In 2011, the German government outlawed nuclear generation, creating political and market uncertainty about funding for the retirement of nuclear facilities and the storage of nuclear waste. Concerns on both fronts intensified in 2015 leaving EOAN down 35% for the year. We believe that much of the confusion around the company’s earnings power and nuclear disposals should be cleared up this year, most likely through the creation of a national foundation.

EOAN, alongside the other nuclear operators, would contribute their disposal liabilities and financial assets into a foundation to be administered by the state, at arm’s-length, with no future recourse to the utilities. This will eliminate uncertainty and increase reported earnings, allowing the market to once again appreciate the strong underlying businesses of EOAN. In the meantime, the company has split into two – future E.ON retaining high quality grid and renewables assets as well as the German nuclear liability; the other company (Uniper) with generation and trading assets. EOAN will spin off a majority stake in Uniper to shareholders in the summer, highlighting attractive earnings on the remaining assets. We purchased EOAN at an average price of €8.92, or about 9x earnings, which appears to be cheap for a high quality utility sporting a 6% dividend yield. The shares ended the quarter at €8.93.

In contrast to Consol Energy and SunEdison, I consider E.On to be at least somewhere near my circle of competence as I have written about them several times over the last few years and have followed the stock and the company at least for 15 years.

E.ON coverage at Value and Opportunity

I looked at E.On already 3 years ago and decided not to buy, which was a good decision because the stock lost ~30% (including dividends) since then, although the stock looked cheap back then as well at 9xP/E and a 7,6% dividend yield.

I did not buy at that time because I identified the following issues:

- nuclear exit risks

- screwed up German energy market

- bad capital allocation (instead of investing into renewables they bought stakes in Brazil and Turkey)

- other potential disasters like their 300 bn “fossil fuel purchase commitments”

E.On was also my prime example how managers of large companies set themselves easy to achieve targets (like total EBITDA) with no connection to shareholder value and earning nice bonuses while the shareholders lose out. In this regard, E.On is clearly among the worst companies in Germany, showing that you can easily earn record bonuses and in parallel destroying shareholder value on grand scale.

Next were the liabilities including the nuclear liabilities which I consider materially underreserved. Finally, I looked at E.On 1 year ago when they first announced their “spin off” plan. I was sceptical back then that the original plan would work:

There could be some roadblocks on the way. The current German energy minister Gabriel seems to like the transaction (or doesn’ understand it) but there could be more resistance building up if people understand that the nuclear liabilities are dramatically under reserved.

Back to Einhorn’s E.On case/arguments:

In 2011, the German government outlawed nuclear generation, creating political and market uncertainty about funding for the retirement of nuclear facilities and the storage of nuclear waste.

Well, as a starter that is not the complete story. What actually happened is the following:

- Germany decided in 2000/2001 under Schroeder that they want to exit nuclear energy with a clear plan until when Nuclear energy has to be phased out over a ~20 year period

- 2010, after intensive lobbying form E.On,RWE &Co, the Merkel Gevernment extended the deadline by a further ~10 years on average

- 2011 after Fukushima then Merkel thought that it is maybe not such a good idea to run those old reactors and switched back (more or less) to the original plan with some additional direct close downs of really old reactors

So 2011 we basically had the same situation as one year ago with regard to provisions. One side remark: Over the first 10 years, the utilities were not yet able to come up with a solution where nuclear waste shall be finally deposited. In Germany, only intermediate deposits exist, ususally on the site of the reactor. This is important to keep in mind when we talk about costs later. In my opinion, the German utilities assumed that they will continue to mae easy profits with their old reactors and therefore missed out completely on the “renewable energy” bonanza in Germany.

Concerns on both fronts intensified in 2015 leaving EOAN down 35% for the year.

Uhm no, E.On was not down -35% because of those discussions. The major reason for the drop in 2015 however was an -8 bn EUR “impairment” in the “non-nuclear” segments in Q3 2015. Losing 4 EUR per share or 1/4 of your equity in a quarter is in my opinion the more likely explanation for the drop in 2015 than the Nuclear issue.

E.On is very cryptic about this 8 bn loss but I assume that most of it has to do with E.ON’s fixed price Nat gas contracts with the Russians. With sinking spot prics everywhere you are pretty much screwed if you negotiated 20-30 year contracts with the Russians at much higher fixed prices. As I have written, this is a 300 bn (yes three-hundred billion) EUR problem and it didn’t get better since then.

My personal take is that that E.ON’s management wants investors to believe that the Nuclear issue is the main reason for E.On’s problems and not the many bad decisions by E.On in the past (investing in Russia and Brazil instead of renewables, negotiating long term fixed contratcs with the Russians etc.).

Now to Einhorn’s key point:

We believe that much of the confusion around the company’s earnings power and nuclear disposals should be cleared up this year, most likely through the creation of a national foundation.

EOAN, alongside the other nuclear operators, would contribute their disposal liabilities and financial assets into a foundation to be administered by the state, at arm’s-length, with no future recourse to the utilities.

Now this is interesting. Yes, it is public knowledge that the German utilities want to get rid of their Nuclear liabilites. But I found it quite surprising that Einhorn assumes two things here:

- Timing: Something will happen in 2016

- ALL Nuclear liabilities will be taken over by the Governement

With regard to timing, I am very surprised because I found nothing in the German press which would indicate a solution in the near term. Clearly at federal level, the priorities are now very differerent with the big discussions about the refugees. Plus there are a couple of important elections on the state level in March and September this year where such a controversial issue could be used by the opposition to hurt the “big coalition” even more.

The recently formed “Atomkommission” has the task to come up with a proposal by February 2016 (see below). However this is also the timing for Merkel to report on what she plans to do about the refugee issue before the elections in March.

Personally, I highly doubt that something will be actually decided in February or this year. In 2017 then there are the general elections and I guess if it drags on until then, the chance is even lower to get a decision. If you have watched the current German Government, especially Ms. Merkel, their main strategy is not to make any fast decisions but to wait as long as they can until there is only one “inevitable” outcome. I would be very surprised if they would change their strategy now.

Now to the second part: Assuming ALL Nuclear liabilities will be transferred to the Government. As I had written before, in 2014 E.On first attempted to spin-off the Nuclear liabilities into the bad ship (Uniper).

Triggered by this attempt, the German Ministry of Economy then comissioned an official study on what to do with this and how to proceed. This study can be downloaded (in German, 150 pages) directly on the Minsitry’s web site and is most likely the basis for any decision that will be taken.

The study then led E.On to abandon the spin-off of the Nuclear liabilities into Uniper in September 2015 because Minister Gabriel threatened to change the laws in order to keep E.On “new” as liable entity.

After this failed attempt, E.On and RWE now with the help of Boston Consulting (BCG) tried to start the discussion to establish a “foundation” sponsored by the Governement similar to RAG which then would take over the liabilities. According to the WiWo article, the recipients of the “Atomkommission” were not amused. I guess because although being polititians they are not completely stupid. The article mentions also the “Swiss solution”, where in Switzerland the utilities could buy themselves out by transferring their liabilites plus 30% “top up” for future price risk.

It seems to be that the Atomkommision has to come up with a recommendation in February 2016. I found an interesting interview with one of the leaders here.

It is pretty clear at least to me that there will not be a complete transfer of all liabilities from utilities to the Government. In typical German fashion, I guess there will be a “compromise” solution.

This is also the solution which was favoured in the above mentioned study: There will be an external fund assuming some of the liabilities, most likely those for the final deposits but not for the more shorter term expenses for dismantling the reactors.

According to the report to the Ministry, reserves for final deposits at E.On are only ~5 bn EUR or 1/3 of the liabilities. I think this is actually the best case for the utilities that they maybe can bring those liabilities into a foundation with a 30% surcharge like in Switzerland.

The leader of the Atomkommission, Jürgen Trittin, the former Minister of Environment from the Green Party made it relatively clear in interview last year that a full non-recourse solution is not part of the possible outcomes. There are many other articles in the press that he is not exactly a big friend of German utilities and is not willing to accept the full liability from teh Government’s side. If I would need to bet on Trittin vs. Einhorn, I would prefer Trittin in this case…..

What amounts are we talking about at E.On ?

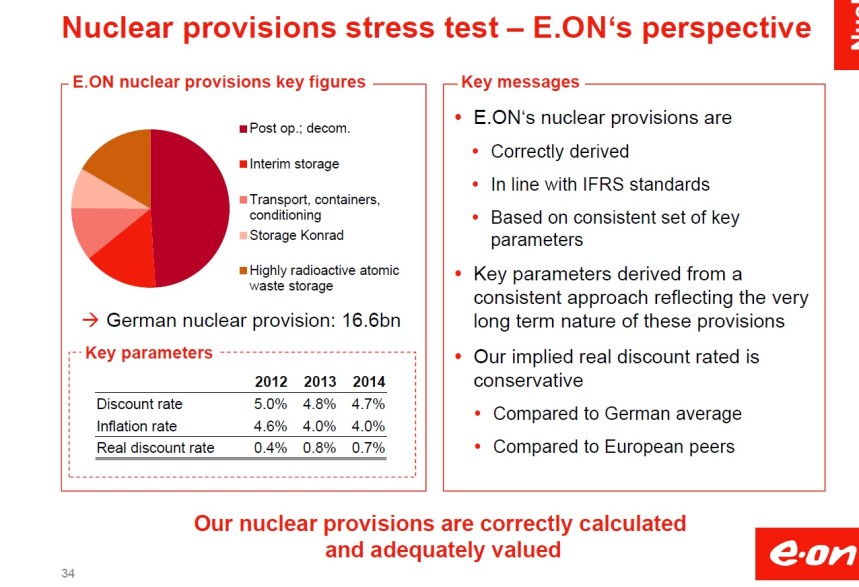

Let’s look at how E.on presents this issue:

What stands out is of course the discount rate they use (4,7%), the inflation rate and the argument that this is “adequat”.

As I have written before, the discount rate looks very high. Similar long term pension liabilities for instance have to be discounted with 2,25% p.a. Of course, inflation expectations are also lower for pension liabilities, normally around 1,5% or so.

So in theory now E.On can claim that the “real” discount rate is very similar.

This argument sounds clever but has one major logical error:

German pension plans actually are directly linked to CPI with a minimum of 1% increase. The nuclear liabilites however will be subject to the actual inflation of the actual costs to retire those facilties. If history is any guide and if you look at other large sacel constrution projects, cost inflation is always the main problem. So I think it is pretty fair to assume that the inflation assumption is for real.

However if we would for instance use the same assumtions for the discount rate as for pensions, we can easily calculate the “hole” in the reserves assuming a 15 year duration:

(4,7%-2,25%)*15*16,6 bn ~ 5,5 bn EUR

Depending at the actual cashflow profile, the value of the liability needs to be upward adjusted for the non-linear effect of lower rates which is called convexity.

Overall I guess we can assume that the real “arm’s length” value of the liabilities are at least 6 bn EUR higher.

The question is of course what is already implied in E.On’s stock price, but even if no transfer is implied, the “upside” is most likely + 2bn EUR as a maximum.

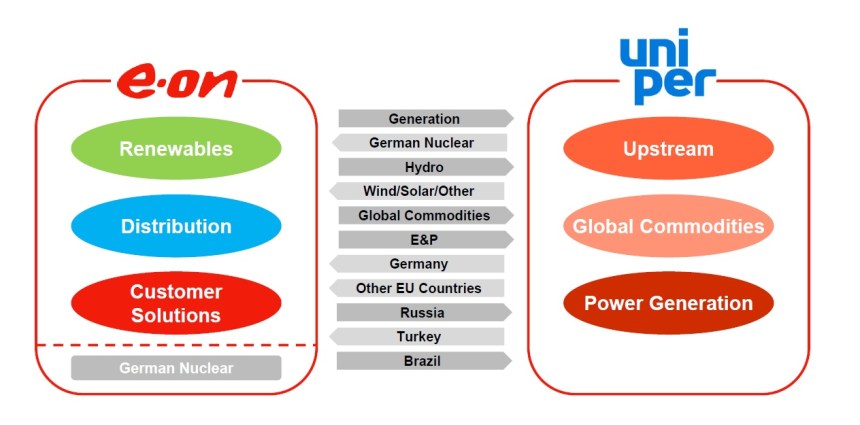

A short look at the “spin-off”

This is the proposed split between “new E.On” and the bad ship Uniper:

So clearly all the bad stuff goes into Uniper. As a side remark, it will be interesting to see how long Uniper survives and what the Russians will say to this….

However as I mentioned in my earlier post on the spin-off: It is not a real spin-off. E.On plans to keep a stake (less than 50%). Why ? Well, my guess is that they need the money from the sale of the rest at “E.On new”.

Of course this also makes the spin-off case a lot more risky than a clean cut: If Uniper shares fall very quickly, this could mean that E.On new has to get new capital from somewehere else.

We should also not forget, that the management who made all those mistakes in the past will stay at E.On new, so in my opinion there is little hope that E.On will change much in the future. I guess EBITDA will remain their main KPI because it is so easy to beat.

For me, Unier will be in big trouble very soon if the current environment (low energy prices persist. If, for some reason the spin-off wouldn’t work, E.On would be at risk either for a massive capital increase or worse…….

Final Summary:

Obviously, EInhorn’s major new long position is more a short term event driven “special situation” investment than a long term value play.

Based on how he explains his investment; I do think there are major flaws in his case:

- The bad performance of E.On in the past is not driven by the nuclear issue as Einhorn claims, but caused by decade long bad capital allocation plus losses from Nat Gas purchase contracts due to low oil and gas market prices

- It is highly unrealistic that E.On will ever get fully releaved (non recourse) from their Nuclear libailities. The best case is more likely a fund for 1/3 of those liabilities. Also the timing (somthing being decided in 2016) looks optimistic

- Finally I do think there is still a lot of potential downside in the stock, among others they are relying on selling part of the “bad ship” for cash which might turn out very difficult

Overall, for me the E.On case is more a high risk gamble than a value investment. Yes, it can work out well short term but there is a big downside potential in my opinion and little “Margin of Safety”. Maybe he has much better research than I assume, but looking at his recent investments in his home market the US, I am somehow sceptical.

I don’t know if Einhorn feels pressured to come up with some quick wins in order to compensate for his -20% in 2015. As a Greenlight Re Investor, I am not happy with such a “bet” and need to rethink this seriously.

Personal Bias:

On a personal side, I need to acknowledge that I am maybe biased in that case. If E.On would be really successful, as a German Tax payer I would be suddenly liable for everything. So it could easily be that I maybe see don’t see this totally objective and my analyis is biased.

Edit:

Funnily enough, just today BofA released a “research” report arguing similar to David Einhorn which boosted the share price almost +4%. Again, I am not sure how much of this is “wishful thinking”.

EON, RWE Rise; BofA Confident on Nuclear Liabilities SolutionBy Naomi Christie(Bloomberg) — BofA confident there will be a “pragmatic solution” to nuclear liabilities following meeting with policymakers in Berlin.

- EON +3.4%, RWE +3.7%; lead Stoxx 600 Utilities index

- German govt could offer to underwrite risk of changes in nuclear waste storage in return for insurance premium: BofA

- Nuclear operators could settle premium by ceding court cases

- German nuclear commission recommendation report expected at end of Feb.: BofA

Interestingly enough in this case, US based researchers/investors seem to be much more optimistic than local ones.

Hi,

Do you have any updated thoughts on E.On? Third Point has now jumped aboard as well with a clearly articulated thesis:

http://www.valuewalk.com/2017/04/dan-loeb-q1-letter-favorable-environment-investing-style-continue/2/

And it looks like they’ve reserved Eur 10bn for the nuclear liabilities (although still on the hook for contingencies).

I an pretty sure that Dan Loeb is much smarter than I am….I still wouldn’t touch E.on with a 10 foot pole.

Einhorn blew it with the one. He does not have people in his circle to understand the German situation well enough. I think has has become a below average investment manager since about 2010, maybe he just made enough money that his heart isn’t in it any more.

For the record, another cool 3 bn loss at E.on for the first 6 months:

http://www.handelsblatt.com/finanzen/maerkte/ipo/eon-mit-hohem-verlust-uniper-reisst-milliardenloch-in-die-bilanz/13989348.html

DüsseldorfIm September will Eon-Chef Johannes Teyssen die Scheidung von Uniper endgültig vollziehen. Dann soll das Unternehmen, in das der Energiekonzern seine konventionellen Kraftwerke, den Großhandel und die Gasproduktion abgespalten hat, an die Börse. Eon will sich danach mit ganzer Kraft dem Zukunftsgeschäft mit erneuerbaren Energien, Netzen und Vertrieb widmen.

Beide Teile gehen den Neustart aber äußerst geschwächt an. Eon hat im ersten Halbjahr einen Nettoverlust von drei Milliarden Euro verbucht, wie der Konzern in seinem Zwischenbericht mitteilte. Eon begründete den Verlust mit Wertberichtigungen und Drohverlustrückstellungen bei der Kraftwerkstochter Uniper von 3,8 Milliarden Euro. Die Aktien stürzten am Mittwoch um bis zu 6,6 Prozent auf ein Fünf-Wochen-Tief von 8,81 Euro ab und waren größter Verlierer im Leitindex Dax.

What a “surprise”: The German “Atomkommission” has delayed the report because there is no consensus with the utilities:

http://www.neueenergie.net/politik/deutschland/kein-konsens-in-sicht

They are negotiating. Remember that utilities have not withdrawn the legal claims (yet). A resolution is not expected before summer. Supposedly the commission outcome is not binding (obviously the Gov. is seeking to use it as a “technical” opinion).

Dave,

back in December/January, everyone expected a quick resolution at the beginning of the year. As I said, I already expected no resolution due to the upcoming regional elections. In my opinion, any kind of utility friendly resultion is highly unlikely before the federal elections in 2017. Ms. Merkel and Mr. Schäuble will not risk any unpopular moves until then. Accordingly, E.On hasd given back most of the outperformance for 2016 already.

I respectfully disagree with you on this particular topic (but life is full of different colors!).

For the time being you are proving right. As soon as June I hope I’ll prove to be right 🙂

In fact I would bet a couple of beers on this (problem is that Munich is a little bit far away)…

Today, I think those beers are getting a little bit closer to my advantage…:-)

Well, let’s wait and see. From what I have seen, the German Taxpayer seems to get royally screwed. Congratulations to the commission.

Hi mmy,

I think it is time to touch base on German utilities investment case 🙂 I wanted to show you one of the fundamental reasons behind the bounce back. I do attach the EEX baseload power prices:

https://www.eex.com/en/market-data/power/futures/phelix-futures#!/2016/07/12

As you will see, there is a clear rebound after touching the marginal price (as I said back in January: “In other words, the pool has bottomed –or is very close to bottom- at current prices.”). Those prices were the marginal set by a new coal power plant (around 20 €/MWh).

Now, bear in mind that there are positives that have not materialized yet: legal claim on nuclear tax (pending) and the closing of nuclear liabilities.

On the contrary, Brexit will definitely not help to support UK subsidiaries for the German utilities.

I’ll keep updating.

PD: I want my beer 🙂

Dear Dave,

congratulations for your utility investment (so far). The reason that Elctricity prices bounced back somewhat is in my opinion however mostly the bounce in oil and natural gas prices and not by any coal power plant. Here is a chart showing the movement of electricity prices and Brent over the last 12 monts:

Medium to long term I still believe that the chances of survival as listed companies for E.ON/Uniper and RWE are below 50%.

Esit: I would support my oil thesis with the fact that Verbund as “pure play” electricity price stock showed the same kind of rebound, without any exposure to nuclear tax etc.

mmi

“I don’t know if Einhorn feels pressured to come up with some quick wins in order to compensate for his -20% in 2015. As a Greenlight Re Investor, I am not happy with such a “bet” and need to rethink this seriously.”

This is a flaw in your rationale. Einhorn has produced an above average investment return sinc 1996. Unless you believe that his 2015 single year decline was more than an anomaly, you have no basis to second guess your investment in Greenlight Re. He has more than sufficiently proven his investment acumen over the last 20 years.

I’m new to your website and thus far I really enjoy it. However, it took me only a short time to recognize a huge flaw in your rationale. I believe you’re too intelligent to have this flaw. Get rid of it.

You didn’t mention David Einhorn’s economic moat that allows him to invest in a way that others can’t. There’s no doubt that the troubles you’ve presented are very real. However, David Einhorn is an activist investor and should be expected to take an active roll anytime he invests. This economic most allows him to unlock opportunities that were previously unknown to the retail investor.

hmm, investing into E.On doesn’t really fit into this I guess….anyone can do it-

That’s not what I said. I said that David is in a position where he can assume a position on the board of the company, and/or use influence to sway the executives decisions. The retail investor can’t do this.

Just want to say thank you for the best “amature” investing blog out there and for all the other insightful people helping out. Me myself I have been long RWE since it punched below 10 EUR for the first time and EON shortly after. My take has been very simple compared to all your insights, German politicians will need to come to their senses and redistribute some of that green energy subsidies to good old base power, but with time moving on I’m getting less sure.

There are two chances: Redistribution of energy subsidies toward old power base or toward the invention of new base power bases.

On the one hand I see a huge majority, a broad consensus in the German society deeply disapproving nuclear energy and strongly approving new, alternative energy, even if it costs some money. It is less about politicians but about the people electing and reelecting them. As long as the people quite consensually approve this way the politicians probably will not stumble.

On the other hand Germany has still a strong engineering and industrial base it can build and rely on when it comes to develop new and innovative technology. The last years have shown the energy production capacity is rising, not falling, Alternative energy production has earned quite some market share. Do you really want to bet this direction will change?

I think it is quite risky bet to go against the creativity and inventive talent of millions of people including quite some quite good engineers, knowing their society is consensually assisting their way. Not at least expecting that these new developed technologies may be asked in other countries as well some time later, further increasing the German industrial export capabilities.

Yes, it might be a German Sonderweg again, perhaps costing lots of money, but that’s nothing Germans are not used to do sometimes.

In German:How Nuclear plants are going to be dismantled in Germany:

http://www.wiwo.de/technologie/forschung/kernkraft-das-lukrative-geschaeft-mit-dem-atomausstieg/12858808.html

Hint: No 50 year cool off period….but a 30 year storage period “on site” for the nuclear waste.

Thanks for your reply! Let me comment on your comments. An answer from your side would very much be appreciated. Thanks in advance!

“I guess you are talking about “operating cash” flows right ? Using Operating cashflows as a proxy for the health of a capital intensive business is not really usefull. If I may borrow a quote here from Buffett: Any Dollar depreciation is a real expense. Free cash flow wise, E.On doesn’t look that great if you deduct asset sales.”

Usually I calculate free cash flow from as op. CF – CAPEX. I don’t consider asset sales as part of incoming cash flow but I consider aquisitions as CAPEX. If I may use numbers provided by Marketwatch for the past 5 years, E.ON’s operating Cashflow was 11 bln (2010), 6.6 bln (2011), 8.8 bln (2012), 6.4 bln (2013), 6.4 bln (2014). In the past 3 quarters, it was alone at 5.5 bln. So that looks stable. I know that operating cashflow can also be manipulated but I doubt it across such a long timeframe. To me, it looks stable and healthy (but also not increasing).

Regarding your point about CAPEX and depreciation: In every of those past years, CAPEX actually was significantly higher than depreciation, even in 2014. That doesn’t exactly tell me that E.On is spending less than its maintenance Capex it needs to at least maintain its operations. This all looks healthy to me. Not great, but healthy.

“I also think you haven’t really looked into the “energy trading” business. This is where the real problems come from because of the long fixed price contracts with Gazprom. This is where the just had to write of a cool 8 bn EUR in Q3.”

Yep, that’s a very interesting point. I must admit I didn’t know about it. Before I’m looking into it, just a remark: E.ON makes about 85 bln of revenue overall. More than 50 of those are from energy trade. In Germany, they only get revenues of 14,5 bln, a bit more in the rest of EU. So they are not as dependend on Germany as many claim. Conventional energy generation is just 5.8 bln, compared to renewables with 1.8 bln. Still a gap, but also not highly dependent on conventional energy in terms of revenues. They also have 1.3 bln of revenue from exploration and production (I think it is gas). That’s also not much and certainly beaten down at current prices.

With all that, not one single of these segments is EBITDA or operating Cashflow negative! All of them are positive

So, getting back to your assumption that global energy trade, which makes 50 bln of E.ONs revenue, is dominated by gas trade. They only seem to break down EBITDA for that segment, not revenue, but EBITDA contribution was 127 from energy and gas trade. The other half of the generated EBITDA of this unit comes from infrastructure and energy transport. That tells a different story than yours, in my opinion.

Regarding the Amortisations of 8 bln last quarter, E.ON names low prices for energy and electricity. On page 16 of the quarterly, they clearly state that these amortisations are mainly taken from their energy production assets, not trade or intangibles (what these contracts with Gazprom likely are)!

Page 37 further goes into detail about these amortisations. The biggest chunk is on Goodwill on the global unit energy production (4.5 bln). 2.5 bln are amortisations of tangible assets of the global unit energy production.

I think that disproves your statement. Those amortisations, that are not nice nor small, are mostly due to lower values of assets for energy production, caused by low energy prices. These are still non cash, no matter what Buffett says, and we discussed cash flow above (which looks healthy to me, not great, but healthy).

Overall, E.On is not a great company, but to me, it doesn’t look like the almost bankrupt company many want to make it. It is also a very diversified company (unlike RWE) and I calculated a gearing of 55% for 2014 (58% taking into account pensions, operating leasing and ready for sale securities), which is still ok in terms of debt. ICR is not so great, with a value of 2.3 from operating cashflow. Since the company has been able to reduce debt, it clearly shows they have cash left to pay down debt (and decrease interest payments). Again, RWE looks much worse when it comes to debt (that’s why I didn’t invest there).

With all this, the company trades below book value (even after all those depreciations) and an EV/EBITDA of less than 5 and a P/CF of less than 4 doesn’t look expensive to me.

To make it clear: It is a turnaround speculation, but every perfect storm comes to an end sometime.

Allow me some comments:

– using an unadjusted EV for E.On will lead to the conclusion that they are cheap. Adjusting for Pensions and nuclear laibilites will eliminate the “cheapness”, especially if you use “market values”.

– Gazprom contracts: This is the tricky thing: My interpretation is the following: They don’t impair the contracts, they impair their powerplants. They need to buy at high prices from Gazprom but sell at lower spot prices, so the powerplants make losses. I guess this is also some political tactic involved in not showing “contract losses” but “business losses”.

– non cash write offs: In my opinion, when a company devalues its asset at a massive scale, then clearly it is not directly cash relevant, but you can be sure that future cash flows will most likely be a lot lower.

– book value: According to the Q3 report, IFRS equity w/o minorities is ~17 bn EUR. So E.On is trading at 1,1x book value

The reduction in debt by the way is pretty much financed by aset sales. They sold around 10 bn assets in 2013&2014 alone. Without that they would have needed to take on additinal debt.

I wish you good luck with the investment, maybe it turns out to be a spectacular turn-around story. Who knows ?

This is turning into an upscale seeking alpha!

My 2 cents on this interesting debate: people also tend to forget that a provision for decommissioning on the balance sheet is not the same as cash contributed to a fund.

In the UK (https://en.wikipedia.org/wiki/Nuclear_Liabilities_Fund) and in France (http://www.world-nuclear-news.org/WR-EdF_seeks_to_bolster_decommissioning_fund-2207104.html), nuclear plant operators had to set up a fund where they are contributing cash or assets, which is invested long term to cover for decommisioning costs, which I personnally prefer to having large non cash provisions. I am not saying waiting for 50 years is better than tearing the thing down right now , and I am not saying the amounts contributed are correct, I would suspect like you that they are understated.

I don’t know the E.On / RWE situation on that front, but could they afford the €17B cash pay within a decade?

I don’t think they could afford those large cash payments without additional funding.

They need to invest a lot in parallel into grid infrastructure as well. I do think that other countries have handled this a lot better.

In my opinion, the most likely outcome is having the companies funding (upfront) the final storage facility (which by the way would “neutralize” the political debate around it -since it would become a problem of the Government coalition to finally decide on which site it will be built). That means that RWE would have to contribute 4.6 bn cash (upfront payment) and E.On 6 bn (idem). The rest of the provisions -mainly decommissioning- (4.8 bn for RWE and 11.8 bn for E.On) should be contributed throughout a relaxed time frame (min. 25 years, usually 50 as other reader mentioned).

The companies have earmarked significant funds for this. As of 9M’15 RWE had 4bn cash at hand and 6.7 bn marketable securities (mainly cash from the DEA disposal) while E.On had 6.3 bn cash and 1.9 marketable securities.

In other words, RWE had 103% of the funds to face the 10,4 bn provision (decommissioning and final repository) while E.On had 50% of the funds available.

The pace of the funding is critical. Should those funds paid 100% upfront, then I do agree with you guys and both companies would be forced to tap de market (among other things because leverage -in this case “real financial leverage”- would jump to a not so healthy ratio above x4 net debt/EBITDA.

In Spain and France the situation is different. There is a charge via tariff to pay for the nuclear dismantling. The logic behind is that since it was a State decision to go into nuclear it has to be the system as a whole (via tariff) the one partly sustaining the dismantling of operations. Overall I would say the German utilities have followed a very serious approach while in other European cases this dismantling debate is still very far away (in most of the cases the useful life has been extended for additional 10 years) but I am sure there will be both (problems/debate) in all those other European generators at due time…

By the way, thank you me for the Cheniere link (I wasn’t aware) 🙂

Obviously there is a large bunch of value investors reading and commenting here. Some very clearly with more knowledge (probably even professionals) and some with less knowledge (amateurs like me) regarding the energy sector. Each time I see these kind of intensive discussions I find it amazing that even among value investors the view of an investment can be so different from each other.

How can it be like that? Does it all boil down to how long the individual investor is prepared to hold the asset and what one expects to happen in the near future?

For instance at what price would you today MMI decide to step into E.On to account for all the risks and difficulties that you see? Or do you expect them to go bankrupt because if not then there must be a price?

Fredrik,

good question. For me, E.On would never be an investment at any price. Why ?

I don’t expect them to go bancrupt in the near term, but due to the significant leverage (Debt, pension, reserves) the risk of bancruptcy is high over let’s as say 5-10 years. Even higher is the risk of potential dilutive exercises (capital increases, forced asset sales) for shareholders like RWE already did and E.On to a certain extent as well.

Clearly, leverage also provides a lot of upside if things work out OK. In my experience, leverage combined with bad and/or wrongly incentivised management is often a toxic combination.

There are different styles of value investing, but mine is more focused on protecting the downside. If you run a highly diversified “deep value” portfolio, E.On could be worth a “punt” especially short term with regard to the spin-off.

So to come back to your question: I think the reason for different opinion reflects the different investment styles, even among value investors.

mmi

Haben rwe und e.on noch ölpreisbindung in ihren gaslieferverträgen mit gazprom? Die wurden doch mit gazprom neu verhandelt. Wenn ja müsste es doch positiv sein – bei so niedrigen ölpreisen???

E.On und RWE sind diesbezüglich sehr intransparent. Die 8 Mrd. Abschreibung in Q3 bei E.On sprechen eher für Fixpreise…..

I did invest in E.On after it sunk a few months ago. Its Cash flow is pretty stable and power generation is only a smaller part of its revenues. Much is energy trading in general and gas makes a big part of revenues as well. Also Germany contributes only a smaller part to its revenues. E.On depends much less on the german market than many people claim in those discussions. Germany is an important market but by far not the only one.

What I did like is the strong cash flow which has been pretty stable the last few years and an acceptable gearing. In addition, E.ON already receives a bigger part from its energy generation business from renewables. Dividends seemed to be well covered as well. Also the energy trading business has been contributing more to revenues in the past than they do now. I have no reason to expect this situation to stay this way.

RWE on the other hand has better margins, but is much more dependent on conventional energy production and also more dependent on Germany in general. In addition, RWE’s gearing is much worse than that of E.On, which is beyond of what I usually accept for an investment. I must admit that RWE’s margins are significantly better, but that is also due to the energy trading sector from E.ON (high revenues, small profit).

I am not saying E.ON is a great company but I think it is facing a perfect storm and there will be better times coming sooner or later. The company seems healthy in terms of financials, especially cash flow, which is most critical to me.

One more thing to consider: The German government needs conventional energy to keep the power grids stable. There have been incidents in the past which required E.On to turn on unprofitable gas power plants. There are already talks with the Netzagentur and it seems that E.On has something to put pressure on politics. You can’t force a company to support the grids and require it to make losses in doing so. These utilities are needed for the Energiewende and we are at a stage where pressure increases on politicians.

One last thing : Subsidies for renewables are lowered so I’d expect fewer newbuilts there. Also I expect E.On’s energy trading business to be independent from this development and, as I said already, their renewable energy segment is already quite big.

Dan,

thanks for the comment.

I guess you are talking about “operating cash” flows right ? Using Operating cashflows as a proxy for the health of a capital intensive business is not really usefull. If I may borrow a quote here from Buffett: Any Dollar depreciation is a real expense. Free cash flow wise, E.On doesn’t look that great if you deduct asset sales.

I also think you haven’t really looked into the “energy trading” business. This is where the real problems come from because of the long fixed price contracts with Gazprom. This is where the just had to write of a cool 8 bn EUR in Q3.

Good luck with the investment.

some comments re management ( hindsight is 20-20):

-selling safe distribution assets was a mistake

-international ventures did not pay off

-did not recognize impact of renewables early, because still invested in conventional for far too long

-no innovation

– no pivot of all cashflows to new business models

your German bias:

The utilities also pay taxes, have employees who pay taxes and RWE is partly owned by local taxpayers. The German taxpayer will not loose the whole euro if he gifted one euro to the utilities. You will observe foreign owned Vattenfall may get more money back 🙂

atomic waste:

-fact is that there is waste

One must feel ashamed as a German when observing how unscientific the process of finding an Endlager is. The already incurred cost for Gorleben were political and sunk. Why should utilities pay for it? Why do you think reactors can be dismantled fast? There is no solution for a endlager in sight. It does not make sense to spent money on exploring an endlager when there is no political chance the location will be used. I cannot understand the process logically here. But in my opinion the Greens should pay for cost overruns. The castor transport also were costly because of criminals, although not all protesters do break laws.

Martin,

one remark: As Bavarian tax payer I would not be a beenficiary if the NRW taxpayer get any relief from the RWE stake…..however I guess I would be on the hook for the Bavarian nuclear plants. On clear days I could see the steam from Gundremmingen from 50 miles away when it was still active. This looked very scary…

mmi

the german utilities are special situation event driven investments for sure – the event is the political outcome for the utilities. i think they are similar to the banks in 2009 where the governments saved them on the expence of the taxpayers (especially in germany). utilities are not so embedded in the whole economy like banks and the risk for the economy is much smaller. the other difference is that the german utilities are mainly in trouble because of political decissions: they are (at least in parts) controlled, owned and tightly regulated by the government. they entered into nuclear energy in some extend for political reasons and now they are forced to exit them purely for political reasons. the german government created the nuclear problem and therefore it is fair enough that the german tax payer is part of the solution.

Compared to the other european utilities the market value / megawatt of production of the german utilities are very low. The stock prices of the german utilities are driven mainly by the political outcome, at least it should be a good diversifier for greenlight… For the same reasons (relative cheap and uncorrelated) i find them interesting but at the moment i didnt buy stocks at all.

Dear memyself&i007,

I terribly do apologize for being this long, but there is no way I could make it shorter (my apologies for all of you). I wanted to share with you the German utilities discussion in previous posts but now it is the perfect timing/momentum.

On this occasion, I think you are losing some important data as a result of your German bias (is highly remarkable –as your correctly pointed out- that all value investors that (we) are currently invested long in German utilities are foreigners). Interesting!.

Here are some facts (please do not consider them opinions. These points are simply facts (no debatable, unless otherwise stated as opinion):

1. FACT: German utilities are –worldwide speaking- the largest payers when it comes to nuclear dismantling cost in an egregious way. The (dis)proportion vs. other utilities is 5 to 1 (see “German Nuclear: A day of two halves” Morgan Stanley, Sept. 2015 and many other documents). Although nuclear introduction has been a political decision, pretty much as everywhere, in Germany the utilities are responsible for 100% of the future dismantling costs and storage (this is unique). But what you are saying is that not only the decision must be accepted without discussion or comparison being made, but also they might grow in case a future upside deviation should occur. Remember 5×1. In my opinion (and here obviously is just an opinion) chances are that an agreement will be reached. Utilities will be keen on withdrawing the legal claims if comfort is provided by capping their liabilities. Moreover, chances are that contributions to the so called dismantling fund will be spread throughout several years (at least until the shut down of the last unit by 2022, enabling the companies to generate additional cash-flow to fulfill this task).

This is like a landlord that wants to get paid but by pressing harder on the lessee could certainly cause him to go bankrupt but you know what? There are no other lessees available! So we can debate whether Germany is right or the rest of the world is wrong but electricity is basic and common sense tells that both parties (Gov. and utilities) are condemned to reach an agreement. Favorable odds for having this agreement scenario are no-brainer for me. Let me recap on the legal front regarding this nuclear issue and its implications:

a. Nuclear tax: a decision is expected in Q1 (that’s why –not only BofA- but all the sell side is pushing the stocks now. For RWE would imply +3 €/share. A little bit less for E.On. Let me remind you that a local Court already gave the reason to the companies (Brussels already ruled that the tax was not against European law –which is a way to say, guys solve this issue internally- so the claim went back to the Constitutional Court that will be one last ruling on this matter. Remember that the issue here is whether or not you can tax something on a general purpose –consumption-. The chances for getting this favorably are high (I would say more than 50%) with the already positive precedent from the local Court ruling. On top, the tax per se was a result of former negotiations between the Gov. and the utilities (the tax was imposed as a consequence of the life time extension by additional 10 years). The extension was revoked but the tax was to stay? Let me refer it as dubious and morally questionable…

To sum up, as a result German utilities would have a triple benefit should the tax nuclear be revoked: (1) higher SOP; (2) a sustainability of the dividend would not be into discussion (3) higher earnings (a positive resolution would imply higher operating earnings) would allow for the use of the tax shield (lowering significantly the tax rate; i.e. RWE ca. 40% currently).

b. Nuclear shut-down: this is a win-win for the utilities. Chances for having a positive result is extremely low (on the overall claim). E.On alone disclosed more than € 8 bn claim. Nevertheless the capex already incurred and the “lucro cesante” is a reasonable claim and could be a positive for the utilities (and a much more reasonable outcome). This claim is a large impact-low probability that is certainly acting as a negotiating tool.

I am not German, but I read the political environment 100% opposite as you do: in theory, there is no urgency when it comes the issue of nuclear liabilities. But with Federal elections nearby (August-October 2017 if I am not wrong) it wouldn’t surprise me if CDU is keen to avoid any negative press around the state’s failure to deal with the potential liability for both (the shutdown and the nuclear tax). I cannot imagine the Government saying to their voters, by the way, we have lost some €10 bn because we thought it was the right thing to do (though the Judge thinks differently). That means that the Gov. may well consider capping the utilities’ liabilities in exchange for some degree of upfront funding and an amicable outcome to the court cases. The upfront funding would be obviously “sold” to the public opinion as a victory.

So in essence, you as a German taxpayer, have to congratulate yourself! Because even setting a cap on the utilities’ liabilities you are paying the lowest cost in the world associated to this concept! You would like to pay even less (I know) but I guess that when a judge sees the comparable data –let me insist-, worldwide speaking, the German utilities objections start to makes sense. The $800/GW that other reader has mentioned is an industry standard.

2. FACT: Conventional German generators are currently–again worldwide speaking- the worst remunerated. Nevertheless they are needed in the system. The market design penalizes conventional generators because of the aggressive introduction of renewables. The key point here is that at 25 €/MWh prices the generation business is hardly making money (cash-flow neutral at best and with substantial P&L losses –that E.On and RWE will certainly show in front of the regulator –one of the reasons for the spin-off-).

Having said this, generation is a liberalized activity (so Gov. cannot force you to run the power plant though is fair to say that companies cannot close the plants either). The bounce back in commodities (gas is already bouncing back while coal API2 has stabilized) together with the significant higher CO2 forecast will drive higher pool prices (more than 2 years time horizon will be needed) with CCGT replacing hard coal in the merit order. Again, this is not under discussion. That would easily lead back to 32 €/MWh prices range, more in line with other European references, though substantially lower in Germany because of the higher renewable share.

Let’s now inverse, what could drive lower pool prices lower vs. current levels? Almost nothing. Nowadays a brand new hard coal power plant setting the marginal could reach 21 €/MWh with API2 below 50 $US/Tn and 6,000 hours load factor (but there is no such capacity available in the system. There is “old” hard coal). In other words, the pool has bottomed –or is very close to bottom- at current prices. The odds of higher generation prices in Germany are highly favorable in 2-3 years time (forget about the 80€/MWh that we saw in 2008 but definitely higher prices vs. current 25 €/MWh). If the companies are neutral cash-flow at 25 €/MWh needless to say what could be the EBITDA under a 32 €/MWh pool price scenario. For RWE (which is more linked to commodities since has a higher share of the German conventional system that would imply minimum 3€/share).

More importantly, the system needs to rely on higher pool prices so that renewables premium could be more easily recovered thru the market rather than via incentives (opposite to what is happening today).

This is concerning energy term. But, what in terms of capacity? On average a healthy electricity system with such a high degree of renewable penetration will need 35-40% capacity for back-up and peak demand (in other words, higher than normal thermal back up). There is no way that you can sustain that level of back-up capacity without proper incentives when pool prices are depressed at current levels. What’s more if I recall it correctly, circa 70 hours already met negative marginal prices in 2015 and remember, the Gov. cannot force to run the thermal power plants! (although you cannot stop nuclear). This is simply insane. The higher the introduction of renewables, the higher the system will need additional investments for i.) stabilizing the grid (this is moving right and accordingly in Germany) but the companies are not ii.) investing in generation (just pure maintenance ☹ ). There is no way you can sustain the aggressive goals beyond 2020 without incentivizing capacity. There are too many examples for that (capacity payments Spain, auctions in UK, pago de confibilidad in Colombia, regulated fixed cost pass-through for the US utilities, etc etc etc). It is simply a mistake and the regulator needs to amend it accordingly (or sooner or later there will be problems at serving peak demand).

Remember that this is not secondary industrial activity. This is primary energy, basic service. According to my own calculus, aprox. €300 M/year of RWE EBITDA should come from capacity payments in the future (post 2017).

3. FACT: Growth profile is changing for the German utilities: provisions at 4.7% vs. long term cost of debt will be EPS accretive for the companies. The distribution and supply businesses are performing well while the companies will have time to adapt to the new paradigm model (distributed generation, thin film, smart grid, house back-up batteries, etc, etc).

To make short a long story please bear in mind that just the mere favorable nuclear tax resolution would cover the negative delta arising from the nuclear shut down beyond 2022 (at operational level)…

So let’s recap the main points (again, these are summarized facts):

1. The only country in the World that has decided to move away from nuclear generation while at the same time trying to reduce significantly CO2 emissions is Germany. The only free emission generation that is abundant and cheap is nuclear (>80% load factor. Large hydro is already “exhausted” in terms of new capacity –for developed countries-). This, after all, despite no known track record of tsunamis (well, there was a 4m wave in Sylt in 1858) 🙂

2. Regarding nuclear dismantling costs, the German utilities will be the largest payers (worldwide) by 5×1 difference but controversy today exists that they might need to pay more. Note: the transport of high-content radioactive material follows a strict safeguard protocol and I’m pretty sure that has been taken into consideration. (See http://www.world-nuclear.org/info/Nuclear-Fuel-Cycle/Transport/Transport-of-Radioactive-Materials/)

3. Some years after its introduction, German electricity market reform (Energiewende) needs to adjust to accommodate the growing renewable share (the elephant in the room). Correct incentives need to be in place to achieve a sustainable path (€1-2 bn/year capacity payments may sound controversial but €25 bn/year of renewable premium is perceived as “adequate”). I guess the media has played its part…

4. In the meantime, the companies should have sufficient resources (negotiation and back to fundamentals) and time (till 2022) to reshuffle their businesses. Otherwise, Government will fail to defend point 1 and 2 (while it’s fair to say that they –The Gov.- can mess around with 3 but that is a different –and longer- story/post ☺ ).

5. Besides all the above, all the financial efforts already made (by households and utilities), CO2 emissions are on the rise in Germany (see “Rising German Coal Use Imperils European Emissions Deal”, Bloomberg 2014). The energy reform has its major flaw on the fact that the ultimate purpose is becoming more and more distorted and in this sense, Energieweden is not delivering on its promises (which is posting additional threats for lignite but that is not the key point under discussion right now. Moreover because nuclear and coal cannot be, from a regulatory point of view, tackled at once). My point here is that Energiewende should not be considered as stoned-cast. It is time to consider that may it be reviewed and readjusted.

Mike Burry realized that something was terribly wrong looking at the boom in house prices (and therefore the mortgages sustaining that boom should have weak premises). You, as a German electricity consumer, have to make an objective assessment and ask yourself. How much have you paid in your last electricity bill? Household prices have moved from 19.1 ct€/kWh (2007) to more than 35 ct€/kWh (2014) and expectedly above 40 ct€/kWh in 2015 (Bdew/Agora), and the trend is upward (you are increasingly paying more the fixed component of the renewable premium, although the energy component –based on commodities- is much lower. But the sum of these two concepts will end up with you paying much more as additional renewable capacity is fed into the system).

The simple question is: is this sustainable? Before the German case, what reveals the Spanish and the British cases is the importance of Governments to make compatible support for new energy technologies with an energy cost that does not sink competitiveness and multiply cases of energy poverty (they have failed miserably in doing so).

Don’t get me wrong, the goal to reach a highly dependent system based on renewables is desirable per se (I am not against that goal) but it cannot be built on weak foundations or without hearing technical expertise on the matter (it cannot be built by politicians). Both systems (conventional and unconventional) need to coexist until the latter gets the lion share.

Please, do not take it personal. I am only sharing (with all of you) what drove my decision to be long in German utilities last summer but by no mean I am trying to convince you. I built a long position in RWE at 10 €/share and now I realize that I could complement that position by being long at Greenlight Capital RE (I admit that E.On has a longer term basis).

Always happy to hear your thoughts and open to discuss pool electricity valuation models and/or sum of the parts.

Take care and -again- please accept my apologies for this extenuating “report” but discussion will make us richer 🙂

Dave.

Dave,

thank you very much for the comment, I would say that this is the best comment I received since I started the blog.

Allow me to answer in the following way, summarizing the aruments you made and then with my comment

1. The assumed dismantling costs are actually lower than the reserves on the balance sheets

As I don’t have the Morgan Stanley study, I cannot verify this. In general however I am always sceptical of Sell side research especially when they want to “spin” investment cases.

What I found (thanks to Google) in a quick search was among others this OECD document comapring different European regimes:

Click to access nea6831-cost-estimation-decommissioning.pdf

What I found remarkbale there are 2 things:

– the cost estimation and reporting process in Germany seems to be much less regulated than in other countries

– – in other countries, additional “contingency reserves” have to be added but not in Germany

Compared to other countires, some cost elements are even missing compared to other countires (Table 1.b):

“except management of legacy waste and interim storage of spent fuel and high level waste”

Overall I am wondering: Why would E.On and RWE use higher reserves than required if the process is actually relatively “lightly” regulated ?

2. Utility negotiation stragegy vs. the Government:: we wil not sue you if you take over the liabilities

I had a post on that already 3 years ago how Buffett approaches this:

https://valueandopportunity.com/2012/12/27/utility-companies-the-warren-buffet-perspective/

Maybe in the short term they could be even succesful with this strategy, but long term, suing your regulator is not a very good strategy. In my opinion this will weaken their position in Germany further. Ok, if you speculate on a short term bounce it might work.

3. Capacity payments

This is soemthing I heard often. My question is: Who would pay for this ? Private households already pay the highest prices for electricity because of the renewable subsidies. I think it is not realistic to assume additional payments from their side. Cutting subsidies for renewables ? Also a tough one. The renewable industry has a lot of lobbying power and in the mind of the public they are the “good guys” and utilities are the bad guys. The German Government giving up on their “Energiewende” ? I don’t see it.

4. Electricity prices

I don’t want to sound too arrogant here (;-)) but I predicted falling electricity prices already 3 years ago when they were at 40EUR:

https://valueandopportunity.com/2013/02/04/energiedienst-holding-ag-isin-ch0039651184-and-german-electricity-prices/

Honestly I am surprised how far they fell. But has anything changed ? I don’t think so. Germany has too much electricity and and the supply is increasing constantly. If you look at Electricity prices “it’s all about the supply” and the supply is still growing.

If you really want to bet on increasing electricity prices, Verbund or Energiedienst as pure Hydro Power companies would be much better. With a 100% fixed cost base, any increase in electricity prices has a pretty significant impact on their bottom line.

Kind regards,

mmi

I am happy you like it!. Thank you for the compliment.

I think all the points have been already discussed and now is a question of how the political landscape evolves…

Maybe, just to mention very briefly because of its importance, the point about pool prices. Congrats for your post dated some 3 years ago about this. Not many sell side analyst wrote in anticipation by that time. The question is now that chances are that there will be a bounce back in the energy prices -low 30s- (as I mentioned before, not before 2018). Think about this. The conversion of the CO2 into variable cost for the day-ahead bidding implies that coal plants will have to internalize this cost in a proportion of 0.9 (904 gr/kWh emission factor conversion for hard coal) while CCGT (gas) will do so by 0.4 (386 gr/kWh CCGT). The forwards by 2018 are quoted at around 15 €/Tn (currently at 7 €/Tn). Ergo Coal will internalize additional 8 €/MWh while gas ca. 3€/MWh. And this is just CO2 (on top we could assume that some commodity repricing would make sense by that time). The margin for these plants will be similar to today’s (higher variable cost but coupled with higher revenue) but the zero-bid baseload technologies (hydro run of the river and –mostly- nuclear) should enjoy higher revenues. This together with the development of a capacity market ☺ should allow for the come back of the generation business (I know that for the time being Minister Gabriel has a different view regarding this capacity scheme)…

Of course I do agree with you that suing your Government is not wise thing to do. I am afraid that there was no choice but I am pretty sure it is just a tactic move and an amicable agreement will be finally met.

By the way I saw you wanted to expand your circle of competence in energy (me too). May I suggest you a company to get started or will you follow an orderly approach by sector? Although I am pretty sure you are aware of this, I think Cheniere (LNG) is becoming more and more interesting.

Having Icahn and Klarman both with a 10% stake each and Chanos shorting the share…I am already digesting the annual report… ☺

Take care.

David.

Hi Dave,

I gues you have missed it but I already discussed Cheniere 1 year ago. I thought it was too expensive at 60-70 USD per share:

https://valueandopportunity.com/2015/02/17/why-on-earth-is-seth-klarman-investing-17-bn-usd-in-cheniere-energy-lng-at-7x-pb/

😉

I feel comfortable with the bet. 🙂

he he he….let’s see…..

Hi,

I think you are overstating the nuclear risk.

The provisions look too high to me, not too small. They are wasting precious capital.

Why is that?

First, you have to look at the cost experience of a country where many plants were decommissioned in a row, like will happen in Germany. In the US, the cost is around $800m per GW. E.On has 4.3GW of capacity and €17bn of provisions.

Then it is useful to remind how decommissioning works. It is not that on the 01/01/2023, work will begin. No. The reactor will be left to cool for at least 10-15 years. Maybe a sarcophagus will be built around it.

Why? Because contaminated material decays with time. The more you wait, the less dangerous to handle it is.

After 50 years, radio-activity is so low in some pressure vessels that human can go and work on dismantling.

So essentially, what could happen is that nuclear reactors will be left to cool 50 years before being worked on seriously. This is what they are doing for the first nuclear reactors in France.

In Spain, they are doing it with another one and costs are much lower than expected – in essence, paying a few guys from Securitas for 50 years is cheaper than having special purpose robots remove contaminated steel bits from a reactor.

Provisions are set aside today for major expenses 50 years from now. Even if interest rates are low, for such a duration, you can expect these funds to at least match inflation, if not grow in real terms. Since we are compounding over very long periods, this will absorb any cost inflation.

Now it means that E.On is not a nuclear liabilities story anymore but an earnings call.

I think you can criticize the earnings outlook of EOAN but not the liabilities anymore.

Finally, if the provisions were so low, would the government not intervene? Which government wants a few extra billions of future liabilities?

Little Friday,

allow me a few comments on that:

1) Cost comparison US/Germany: Germany is a densely populated country with people being EXTREMELY sensitive about waste disposal and nature in general. The US on the other hand has vast areas where you can easily bury your waste and no one cares (Nevada, etc.). So assuming the same cost to me seems “optimistic” to put it friendly.

I think also France and Spain are not very good comparisons. It is not in the Nature of Germans to wait 50 years and hope the problem will go away by itself or solved by the next generation, this is more the “Mediteranian approach”.. But I see now where Non-Germans are coming from. Interesting.

2) “Even if interest rates are low, for such a duration, you can expect these funds to at least match inflation, if not grow in real terms. Since we are compounding over very long periods, this will absorb any cost inflation.”

It’s very interesting to assume that a long term liability discounted at 4,7% is too high in this environment. If this would be true, you would have plenty of investment opportunities in Germany, UK, basically everywhere. We just the money into some nice stocks and we are all a happy family…..

By the way, the pattern that you are describing is fully reflected in the reserving.

Finally you might have missed the point that the Governement has already intervened when E.On tried to put the Nuclear liabilities into Uniper. Would they have done so if they were happy with those reserves (and the assets covering them) ?

mmi

” I think also France and Spain are not very good comparisons. It is not in the Nature of Germans to wait 50 years and hope the problem will go away by itself or solved by the next generation, this is more the “Mediteranian approach”..

In France, Spain or Germany, half-lives of irradiated nuclear materials remain the same I am afraid.

In densely populated areas, there is even a bigger need to let things cool to avoid contamination during dismantling and transportation. Would you be comfortable knowing that trucks full of irradiated materials are taking the same road where you drive your kids to school? While waiting 30 years would lower the risk by a large risk factor?

Well, tell this to the people who live very close to 40 year old reactors….I think the time tables are pretty clear under German rules.

There was a very interesting documentation on German TV this week about the ancient Belgian reactor right at the border to Germany

(Spiegel, German: http://www.spiegel.de/wissenschaft/technik/panne-in-belgien-reaktor-muss-nach-wenigen-tagen-vom-netz-a-1069490.html)

It’s interesting to see how Germans even try to force the Belgians zu close the reactor.

With regard to transport: Yes that’s a problem, although in Germany nuclear waste was only ever transportd on rail, never on roads for longer distances (“Castor transports”). Another reason in my opinion that the final soultion will rather be more expensive then less expensive….

Honestly, I do think you underestimate the sensitivities of German voters in regard to this topic. But let’s wait and see. For teh time being I am long E.n via Greenlight Re and potentially also long Nuclear liabilities as a German Tax payer.

I am not talking about sensitivities of any nations. Just pure science. It is better for everyone to leave irradiated materials cool down as radioactivity wears off naturally with time. I am not talking about the spent fuel. More about anything that was kn contact with uranium. Better let time cool and clean it. Then you can dismantle a nuclear reactor wearing a tee-shirt and cleaning gloves (a small exageration but you get the gist).

well, I am not a scientist so I cannot judge if what your are saying is right. However, most of the voters are no scientists either.

Let me give you an example how public opinion in Germany is shaped:

Even almost 30 years after the Tchernobyl incident, every autumn just at the start of the mushroom season, people are warned that mushrooms still contain too much radioactivity and should be eaten carefully

http://www.br.de/themen/ratgeber/inhalt/ernaehrung/pilze-radioaktivitaet100.html

https://www.test.de/Wildpilze-sammeln-und-zubereiten-Tipps-fuer-den-unbeschwerten-Genuss-1163075-1163675/

The same is true for game meat:

http://www.lfu.bayern.de/strahlung/caesium_wildbret/index.htm

Unfortunately, when the Tchernobyl cloud was over Europe, it rained in Bavaria and therefore the ground is radioactively contaminated to a certain extent. Imagine now growing up with having this on the news each and every year: You are not allowed to eat something because 30 years ago somthing blowed up 3000 km away. Then maybe you understand that people would feel just very uncomfortable with living next to a nuclear reactor cooling of for 50 years or so.

But again, maybe I am biased, but I am also an “insider” here and I think I do understand German voters to a certain extent.

I was not aware of that the French did that with their old nuclear power plants. Very clever. Significantly lowered risks not only for the future dismantling but also for the population that decided/accepted to live next to those nuclear plants. Very clever. I guess the only big losers will be investors that buys land and properties expecting to make big bucks once the dismantling is done. Them, however, I do not feel sorry for.

I think the French have a very different approach to nuclear power plants than Germany. Funnily enough, in the first winter when Gemrany switched off the nuclear plants, Germany had actually to export energy to France. Because it was such a hard winter, French households had to switch on their radiators whoch overwhelmed the French nuclear genration capacity….

I remember that the utilities argued that actually Germany would be doomed but this was clearly an empty threat from the utilities….

Thanks for the article.

I have to admit I don´t know anything from the 2 german utilities other than from your articles, Einhorn comments and an investor letter (may 2015) from an spanish fund manager (unfortunately is in spanish https://s3-eu-west-1.amazonaws.com/abante-web-wp/wp-content/uploads/2015/05/201505-Abante-Pangea-Insight-XVI.pdf) that refers to RWE . Let me try to sumarize his points (apologies if there are translations errors) just to provide the long side view:

Controversial business (coal + nuclear) less than 15% ebitda,in medium term 50% ebitda from regulated and estable business. Normalised ebitda including cost cutting and asset sales to reach €3/share at PER x14 -> €42/share.

– Recovery of “nuclear tax” paid or at least no more payment since 2016.

– No compensation expected to be received for nuclear closing but can be used as leverage for other negotiations.

– Gas a the new marginal energy after coal closing that will translate in an increase in energy price from €32/Mwh.

– Cost cutting and asset disposal in 2016-2017 would support ebitda levels. FCF €2000 m on a market cap 12bn at may 2015 (€7.29 today)

– proposals against lignite and coals emissions would be offset by gas as new marginal energy.

– no minimum payout% policy by the company has created uncertainty around the sustainability of 1€/share dividend. He considers dividend is sustainable after DEA sale and 2bn FCF.

– Confusion about debt x3,5 net debt/ebitda excluding non financial debt (nuclear,mining and pensions provisions ” very long term & difficult to quantify”) translates into x1 net debt/ebitda. He considers capital increase not probable.

– 70% Ebitda cash conversion -> €3.850m cash flow to cover €2bn investments and €614m dividend.

– RWE poor performance vs DaX on relative terms.

Between Einhorn, the spanish manager and your blog, after a few years I trust more on your blog… but 6-7% dividend from an utility company (no risk assumed) in a yield starving market seems very attractive (also on terms of relative bad performance of the stock in previous year) and people like Taleb ´s turkey we don´t care about long term while we are being fed with a generous dividend until is too late (as with the Yieldcos and some oil stocks). So I guess you are right this is just a special situation position for Mr. Einhorn.

andy,

I didn’t read the RWE “insight” but my assumption is that this Spanish manager has no idea how the German electricity market works. Since the time he wrote that piece, power prices dropped 1/3 to around 24 EUR due to the massive build up of renewable capacity. The concept of the “marginal” cost does not apply in a market where you have an ever increasing supply of electrictity with 0 variable cost.

After I wrote the comment I read a RWE presentation, so the letter was outdated. Very good point your last sentence “The concept of the “marginal” cost does not apply in a market where you have an ever increasing supply of electrictity with 0 variable cost.”

Regarding your post edit “Interestingly enough in this case, US based researchers/investors seem to be much more optimistic than local ones.” this is a common bias that I have also perceived not just regarding countries (people from spain that are aware of their country risk invest in germany and viceversa) but also sectors if you have worked in a IT company you don´t invest in IT, if you work in a bank you don´t invest in bank.

Completely agree, investing in E.on is by far the most incomprehensible recent investment from David Einhorn. Like in poker, suddenly loosing big money makes your mind to come up with worse and worse ideas to recover fast.

Agree. This hot potato will be touched only after the next general election. No politician can win anything when agreeing to let them off the hook, even partially. In the meantime, they are heavily indebted and credit is tightening. Will any creditors and the russians agree to be “spun off” to uniper?

“Over the first 10 years, the utilities were not yet able to come up with a solution where nuclear waste shall be finally deposited”

Oh my god. For the utilities the solution was there all along. It’s local interests, politics and green radicals that are to blame that we don’t have a repository. And the worst is that the utilities are expected to pay for everything, even if it’s not their fault that nothing ever gets done. I personally hope that the utilities will sue and one day recover all the costs that were sunk “for nothing” because of political decisions.

“It is pretty clear at least to me that there will not be a complete transfer of all liabilities from utilities to the Government. In typical German fashion, I guess there will be a “compromise” solution.”

That seems to be the most likely outcome. One should remember that the post-Fukushima shutdown had no rational or economic justification. It was a purely emotional/hysteria-driven decision that resulted in value destruction (for utilities AND taxpayers) on an epic scale. The taxpayer can’t sue, but the utilities did – and they have good chances to be awarded damages. If the government shuts down your production plant for no good reason (and there really was no good reason at all, NOTHING had changed from one day to the other) then you can claim damages.

This is the other side of the coin.

So yes, let’s hope for a compromise – but to quote your title:

Trittin, head of the “Atomkommission”? really? c’mon…

That’s like putting Ahmadinejad in charge of a gay rights commission.

What qualifies this crazy fundamentalist for the job? How can we expect any sensible decision if this guy is in charge??

#shock,

I don’t know where you are living but I’am pretty sure you don’t want to live near a nuclear “Endlager”. And I am pretty sure you heard about the problems in the socalled “Zwischenlager” Gorleben.

In one respect I completely disaggree with you and I thought that I made that clear: The big shareholder value destruction comes from E.On’s and REW’s mangement and not the Government. The Governement didn’t force them to do 30 year fixed price contracts with Russia or to sink billions into Brazil instead of building renewable assets in Germany. For the management it is a nice excuse to blame the Governement for everything and collect nice bonuses because “its not their fault”.

Hmmm… I look forward to Davids answer to this one!

How many %-age of the total portfolio in Greenlight Re is now shares of E.On? I mean is it 1% or more 10%?

Personally I am pretty heavy into utilities and I own today E.On, RWE, Enel and CEZ. I own them simply due to that they appear to be cheap and they provide the world with a product that I consider that the use of will only increase year by year. But yeah… times are tough at the moment.

He didn’t cross the 3% threshold, so less than 500 mn EUR

One of the best posts so far. Thank you very much.

Nice post and your thesis is pretty convincing. Would you put RWE in the same boat?

Yes, to a certain extent RWE is ecen worse..