Dear David Einhorn: Why are your interns doing all the cost of capital estimates (Consol Energy) ?

Just to be clear: I have nothing personally against David Einhorn. I am just wondering how he comes up with his underlying valuation assumptions these days.

I already had issues with funding cost assumptions at AerCap as well as his return assumptions for SunEdison.

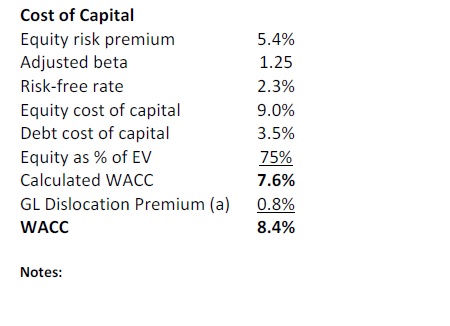

Now I came across his latest pitch for Consol Energy this week. This is the slide which explains the value of the coal business:

Without going into the other details, the question here is of course: How the hell did he come up with a WACC (Weighted Average Cost of Capital) of 8,4% ?

The WACC is supposed to be the blended total cost of capital of a company, including both, debt and equity. For Consol Energy however the obvious problem is the following: Their bonds are trading at a level of 12-15% p.a. Even if we us an after-tax figure of maybe 8-10%, even the after-tax cost of debt is higher than the assumed WACC.

As the cost of equity has to be higher than senior debt (it is more risky), there is no way in ending up with a WACC of 8,4%. Maybe some of my readers can help me out if I am missing here something, but I am pretty sure that 8,4% is not the right number for Consol’s cost of capital. He uses the same WACC later for the shale gas part of the company, so it is certainly not a typo:

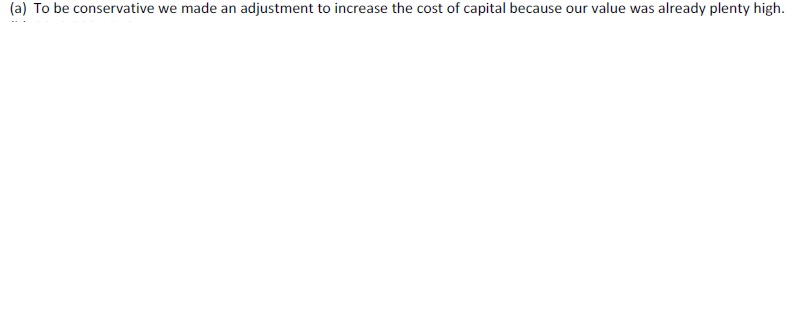

On his website he then explains how they (or his intern) came up with the WACC (slide “A-1”):

The real joke however is to be found a little bit below:

Edit: Now that I know that it was meant as a joke it reads somehow different 😉

So he somehow believes that his WACC is actually conservative.

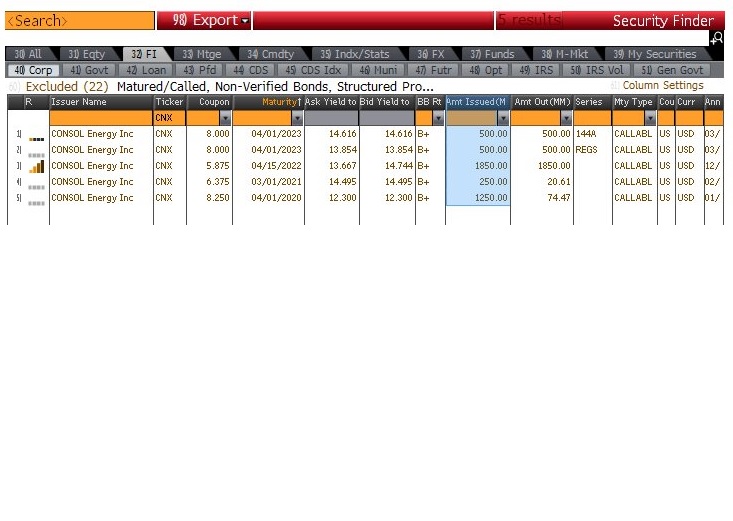

Let’s look at some “real world” data. This is the overview of Consol’s currently outstanding bonds:

The average yield based on outstanding amount of Consol’s bonds is 14,5%, a full 11% (or 1.100 basis points) higher than in Einhorn’s calculation. As I have said above, the cost of equity has to be higher than the cost of debt as thee is no protection to the downside. So if we use Einhorn’s quity risk premium of around 6%, we would get cost of equity of around 20,5%.

Based on Einhorn’s weighting, we would get a WACC of (20,5%*0,75) + (15,5%*0,65*0,25)= 17,73%, roughly speaking double the charge that Einhorn uses. You might say this is conservative but in effect it is just realistic and based on current market prices.

Even at issuance, Consol’s cheapest bond had a 5,875% coupon, far above the assumed 3,5%, so it is not even a question of current market dislocation.

Either Einhorn assumes implicitly that cost of capital goes down dramatically or he has some “secret” that I don’t know. If I look at Einhorn’s last pitches, especially AerCap, SunEdison and Consol, there seems to be a common theme: He is always pitching capital-intensive companies with significant debt where he assumes pretty low cost of capital in order to show upside.

So what he seems to do these days is effectively betting on low funding costs which, at least for SunEdison and Consol didn’t work out at all.

In my opinion, this has nothing to do with value investing. Value investing requires to make really conservative assumptions to make sure that the downside is well protected as first priority. For those leveraged, capital-intensive businesses however, the risk that you will get seriously diluted as shareholder in those cases is significant, there is no margin of safety. On the other hand I somehow admire his Chupza. Standing in front of a lot of people who paid significant fees to hear the “Hedge Fund honchos” speak and pitching such a weak case with unrealistic assumptions is brave.

Of course a stock like Consol can always go up significantly after dropping -75% year to date, but the underlying analysis is really flawed. I would actually like to ask him if he really believes in those assumptions or if he just didn’t pay any attention to the details. This would be really interesting.

Maybe a final word on this: I am always criticising David Einhorn on his assumptions. Which is easy because he actually is very transparent about them. Many other Hedge Fund managers just tell nice stories. I am pretty sure that in many cases the assumptions behind those cases are not much better.

Thanks a lot for the great article an discussion. This really helped me to understand things better!

If you look at the presentation he cross references his DCF to Earnings before tax (after interest) and gets a multiple of 11 or something, which is reasonable.

WACC/DCF is only one tool. Plus the WACC of 8.4% is essentially a PE of ~12. Your WACC of 17% is a PE 5.

You could argue their coal business should get a PE of 5 (but PE seems way too low for a low cost producer). But for the gas business a 12 PE is very reasonable.

His WACC aint out of WACK.

No, WACC of 8,4% does not mean a P/E of 12. If the bonds yield 14% or a “P/E” of 7, then the equity needs to be cheaper. Don’t mix up different concepts (WACC and P/E)

Geez…….The PE is an approximation of WACC. A WACC % of 10 is APPROXIMATELY 10 times cash flow.

Net income is an approximation of cash flow. So a the PE equivalent of WACC will get you similar results.

I do this for a living, with my own money, you are stubborn and you are clueless. Most of your analysis is based on University finance class efficient mkt hypothesis.

You are confused and focus on little issues that have very little bearing on the overall outcome of the investment.

I read the Einhorn presentation and invested in CNX, the fact that you chose to nitpick on the WACC issue, shows how clueless you are.

hmm, I think you don’t rallyknowwhat WACC means, so I think further discussion is unnecessary. Good luck with the CNX investment.

Edit: Maybe I should waste my time with an explanation: The Wacc is only equivalent to the Cost of Equity (and a P/E) if there is no debt. A bank for instance has a lot of debt and a low WACC. Deutsche Bank for instance has a WACC of around 2%, that doesn’t mean that their “fair” P/E is 50. Themore debt the higher the cost of equity and the lower the P/E.

If you are going to delete my posts delete all of them, mr clueless

NM i thought you deleted my posts…I am slow….but you are still clueless though.

Sorry that you had to read my post and wasted your precious time. Do me a favour and don’t read my blog in the future. Just stick with those guys who like your investments, that is the best solution for both of us.

Since aggregate WACC is not observable and difficult to predict, it’s important to conceptualize it as a distribution. “Normally” summarizinf the distribution with a point estimate for bell shaped distributions is workable. CNX’s WACC is more complex because the probability and severity of a credit event is very different under a reasonable range of commodity price scenarios. Visually, if realized price is the X-axis and credit impact is the Y-axis, it would be the sum of bell distribution centered at about 8.5% and a horizontal line intersecting the right hand side of a second bell at the level of total loss.

Sounds quite sophisticated but in my opinion a little bit too complicated

>>On the other hand I somehow admire his Chupza…speak and pitching such a weak case with unrealistic assumptions is brave

Nice Observation.. David Einhorn is an excellent salesman than an investor!

Your comment is tongue-in-cheek, right?

Salesmanship is necessary but not sufficient explaination for Einhorn’s incredible commercial success and mostly irrelevant to his investment skill.

It’s dead obvious he only presented part of his CNX analysis. He has a great track record give Greenlight’s scale and plays poker. Do you seriously think he hasn’t worked out his downside?

Spend a few minutes working out a rough probability-weighted value for three commodity price scenarios and the likelihood of a credit event for each. You’ll probably end up somewhere between $15-$50 a share.

Well, the commodity price scenario “as is” most likely justifies the current price.

No, it’s not. I consider him to be a good investor, but even a better Salesman than an investor.

David Einhorn is no doubt a gem of a person, however this is not a personality contest. He could have a stellar record, but I haven’t seen or verified it, have you? Or its just what you hear the media say and believe it?

Here’s an example

http://www.businessinsider.com/einhorn-st-joe-short-gets-shout-out-from-the-sec-2015-10

The author has done a poor research and on top calls this ultimate victory!

According to HFR, Greenlight returned 8% in 2014 vs. 3% equity hedge fund average. In its first decade of operation, Greenlight’s annual return was 29% versus 12% hedge fund average. Over the past five years, Greenlight’s 12% compares with 4.7% hedge fund average.

@hubriskills, And based on that you made assumption of investment success ? If others perform bad and my performance is average, that doesn’t make me a genius.

Check against the S&P500 and you will understand why I mentioned better “salesman”

This is from one of the sites, which doesn’t even include the awful 2015 performance Greenlight is having. I wish them nothing but good luck going forward!

http://www.gurufocus.com/profile/David+Einhorn

scroll down to “Performance of Greenlight Re” section

Paraphrasing Rumsfeld and Socrates, you don’t even know what you don’t know. (If I were speaking, the inflection would be friendly, not harsh.)

No doubt Einhorn must be an excellent salesman.

No doubt Greenlight’s investment CAGR crushed SPY. *

No doubt Greenlight underperformed SPY over short time frames.

No doubt Greenlight fees are higher than SPY.

No doubt Greenlight’s fees were worth paying.**

No certainty Greenlight’s CAGR will continue to outpace SPY, either in absolute terms or on a risk adjusted basis.

No certainty fees will continue to be justified by performance.

No doubt many of Greenlight’s investments were clinkers.

No certainty Einhorn’s CNX pitch at Robinhood comprehensively presents his thesis.

No certainty CNX is a good idea.

* Greenlight’s investment CAGR was approximately 16% since inception in 1996.

* S&P 500’s CAGR was about 4.4% over the same period.

* Before fees and tax, $1 invested in the index is now about $2.4. One dollars in Greenlight is now more than $9.

* Net of fees, SPY returned about 4% growing $1 to $2.2.

* Net of fees, Greenlight returned approximately 10% growing $1 to about $7.5, assuming 2/25 with a highwater mark.

* In very rough terms, Greenlight’s Sharpe ratio was 0.90 versus SPY’s 0.22. For convenience I used 10.7% or 2/3 US equities standard deviation of about 16%. That’s a bit higher than the 350bp spread in 2008 net drawdowns.

* The estimated returns are based on annualized results supplied by reliable hedge fund manager research firms as reported in the press, with the following exceptions:

* Greenlight’s annual returns were positive every year except 2008 (-22%).

* YTD 2015 is on track for another negative year, I used -15% as reported in the press.

* I don’t have a return for 2007 and assumed 1% for convenience.

>>If I were speaking, the inflection would be friendly, not harsh

Listening to Socrates is fine, but tossing in Rumsfeld? you lose credibility!.. .. I have no verified/audited results yet I throw phrases of others not knowing what they don’t know… lol

Even if harsh, should be ok, as long as we get to learn/share.

5~7 years maybe be a short period for you, not for me (and am sure not for many others). Think about it, those accredited investors who went with Green light in ’07~’08; they are paying 1.5~2/20~25 in fees, not even beating S&P, getting K1’s (for the year) and yet with Greenlight ( some might have left), don’t you call that excellent salesmanship?

While we are at it, don’t forget to take a peak at NASDAQ:GLRE, (-16.51%) since it went public in 2007

Not sure if you heard Stanley Druckenmiller say so many times, many hedge funds are being run by incompetent/average people, ( of course not implying Greenlight is incompetent or average) which makes this Hedge Fund Average sort of useless. And the returns you brag about since inception and going forward, listen to him again and understand why he says were achievable before and now difficult to come by.

Don’t think G-pa is idiot to bet $1 mill on hedge funds not beating SP500.

Of course there are funds that will beat the SP500 time and again, but that’s some other topic.

Hi This is David Einhorn

Really.

First, I want to thank you for writing this blog. One of the purposes of these presentations is to create dialogue and receive feedback. I find your writing to be excellent and I don’t mind your disagreeing with me at all. You very well may be right.

Second, regarding the substance. Calculating at DCF and a WACC is a theoretical construct. It can also be reverse engineered to estimate an implied WACC and the Cost of Equity embedded in the current share price. So, I asked my “intern” to do just that.

Our analysis implies a WACC for the entire company of 17.7%. If you assume the bank debt has a cost of its coupon, the bonds have a cost equal to their trading price, the implied cost of equity at the current share price is 36.0%. My thesis is that the market has this company wrong and that those prices represent bargain on a risk-reward basis.

Of course, you or others might feel that this company should have a cost of equity of 36% (or that my projections are too high). If you do, then don’t buy the stock. That’s what makes the market.

Again, I do thank you for taking the time to analyze my work and provide this feedback. I find it both valuable and constructive.

Best,

de

P.S. The footnote that you highlighted was written tongue-in-cheek. That’s just my sense of humor. I apologize if you took exception to it.

Hi David,

thank you very much for the quick and direct response. I have to admit, I didn’t get the joke with the footnote. Maybe it’s because I am German ? 😉

To be honest, I don’t know that much about coal in the US and if and when Natural Gas prices will trade up to their forward prices. Those low energy prices seemed to have surprised everyone except that one guy from Citigroup.

36% as the implied cost of equity looks quite rich and mabye worth a look if these kind of high return/risk stocks are within one’s area of investment. For me, fortunately or unfortunately, they are not, I try to stay away from equity in distressed companies. As a large shareholder who might get heard by management this might be different.

Good luck with the investment and greetings to your “intern”,

mmi

After googling ‘tounge-in-cheek’, I now get the joke too :-). Thanks for clarification, David.

@ mmi: I guess the fact that David thinks it’s worth commenting here is a consequence of the quality of your blog. So, thanks for your blogging.

Tom

Great discovery and analysis! I am very happy that I clicked through from AR.

Common sense tells you that both cost of equity and cost of debt in Einhorn’s valuation are way too optimistic, regardless of the current bond yield or stock beta.

The footnote tells you all you need to know: WACC and all the other valuation assumptions were very likely reverse engineered to arrive at a specific price target.

Chris

Thanks for the comment and welcome !!

Yes, reverse engineering is always an issue. With Consol, you can’t du much with growth rates, so you have to play with the discount rate.

thanks for this.

a few quick typos: there spelled as “thee” and assumptions spelled “assumtptions”

thanks. My long time readers know that spelling is not my strength and/or priority….

I guess you’re touching one of the weakest spots of a DCF calculation (and there are many). In the basic formula WACC = Cost of Debt x Debt/(Debt+Equity) x (1 – tax rate) + Cost of Equity x Equity/(Equity+Debt), where Cost of Equity is, at least according to CAPM, risk Cost of Equity = Risk Free rate + Beta * Equity Risk Premium.

Already this calculation is full of issues with, as far as I know, no real answers for, just to name a few:

Cost of Debt (basically start of the discussion): What to take? Median of company bond coupons? Most current coupon? For long term or short term bonds? What about bank loans? Maybe a sector average? Or a long time average of the company? What about the relation between leverage and income situation with regards to bond prices?

Debt: Typically the market value of debt. So leverage actually decreases when a company’s bonds get lower prices due to bad market sentiment in the company. As an extreme case, the leverage would be zero once the company defaults (debt market price equals zero). What about bank loans? Adjust for market price or simply take book values? What about uncovered pensions and operating leases? They are similar to debt but what market price will you set in your calculation?

Tax rate: Which tax rate? The current tax rate? That gets lower the worse the company’s business goes. An average of the past x-years, 5-10 maybe? Or simply take the countries company tax rate? As you already mentioned, there actually is no tax benefit for a company that has no income.

Cost of Equity: What risk free rate and market risk premium to take? From the country of origin or global average? Or where the companies operations are concentrated in (wish you fun calculating that!)? A long time average? For which index? Dow Jones back 100 years? S&P 500, or should you take an index the company is part of (if any)?

What about the beta? Take the sector average? Adjust for leverage? Or take the companies beta, which in most cases varies a lot over time? If using a sector average, for what time period? What about the correlation between leverage and beta? If the company has no income and leverage is high, the beta must increase as well, so there’s a link between the two.

What about market value of equity? I want to know the intrinsic value, so current market values of equity (= market capitalization) can’t be used (circularity issue, also already mentioned in the comments).

To make it short: A DCF is filled with assumptions, even for the starting point of determining WACC. In my opinion, it doesn’t make sense to try and get an exact value for the company. It doesn’t exist anyway. A DCF is just a way to get a fair market price for a company with regards to your assumptions, that’s all. It’s just a very rough estimate after all, but maybe the only way to get it so I think it is worth doing it. In the end, though, your assumptions must be correct, which is the much harder part of it.

So, coming back to the initial question: Are WACC of 8.4% for Consol sensible? Personally (!), I don’t think so and would expect it in the range between 15-20%.

Dan,

thank you very much for your great comments. Fully supported on every single point. I agree that DCF is a very crude tool there aren’t that many alternatives. Nevertheless one should always start conservatively and then explicitly take into account what assumptions lead to lower discount rates (and higher values). Only if one does this explictly, it can be verified later.

And yes, I agree that a WACC of 15-20% is a realistic number in the current market environment.

mmi

You look at ABN Amro at all?

yes briefly. But it Looks expensive from the outside.

While I also think a WACC of 8 something is too low for highly cyclical business with a questionable future, it is misleading to use the current yield on the bonds as an indicator, as it is a function of the specific capital strucure of the company – which is overlevered. This is the wrong perspective in my view

If you want to value the asset “objectively” it makes more sense to use the figures for a sustainable capital structure, i.e. the price a non distressed buyer would be willing to pay – he probably would not have to pay 15 percent to take over the debt….

It depends on the circumstances which view is correct – this being an art not a science….

hmm, i think ignoring the capital structure in valueing a company is not a very good idea. You are not buying the asset but the stock and the bonds have priority on any cashflow from those assets. Any “secure” asset can become a risky equity if you add enough debt.

But you can sell the asset (I assume there is a market for coal and gas reserves, albeit depressed) to a strategic buyer with a strong balance sheet…he looks at the world differently. Immagine Exxon buying the whole thing in order to show “growth”….

Of course, they would figure that your bargaining power is weak as you are in distress, but if the assets are attractive (no opinon on that) you might have several buyers to choose from to mitigate that.

If EInhorn finds such a buyer and can convince them it is attractive and conserviative, it might make sense.. The more “liquid” the asset, the less your debt structure matters-relatively speaking.

Again, it depends on the perspective – there is no right or wrong…

By the way, the bonds could be attractive…

A few comments on the asset sales: I am not an expert but in the current market, buyers will require more than 8,4% p.a. for coal and shale gas assets, especially if they are not even profitable at current prices. Einhorn’s case assumes increasing prices for natural gas which again is not really conservative.

Additionally, the issued bonds contain some codenants especially with regard to asset sales. Plus there is a change of control clause, a full take over will give the bondholders a put at 101%…..so the debt structure matters uuite a lot 😉

Clearly you can speculate on a take over but again, this is a speculation and not a value investment. Different investmetn case.

I think Munger is right, as usual: “I’ve never heard an intelligent cost of capital discussion. Warren’s way of having every dollar retained having to produce at least a dollar of market value is the best way to describe our cost of capital. But that’s not what people mean when they say it, especially in business schools. But it’s simple; our way is right and their’s is wrong.”

I agree that cost of capital is not an ideal decision making tool. Therefore you rarerly see me using this in my cases. I find it more intuitive to think along this lines:

I define what I want to earn on an investment first and then look at what has to happen. That doesn’t look so sophisticated as a DCF model but is more transaparent. For me, somthing like Consol would need to earn 20-25% in order to justify to even think about an investment if at all.

Great article on a very interesting but grey topic in discount rates. How do you view Buffett’s way of discounting all ideas with the 30yr?

http://25iq.com/2015/11/21/why-and-how-do-munger-and-buffett-discount-the-future-cash-flows-at-the-30-year-u-s-treasury-rate/

I will actually write a post on that. The short answer: Buffett is a genius, he doesn’t need to think about it. Most other investors aren’t geniuses.

Einhorn uses normalized figures for both the cost of debt and equity. In every valuation you have to use your assumptions on growth, cost of equity etc. because otherwise you can just invest passively. To be honest one can’t even calculate beta without assumptions. Everyone who thinks otherwise is a nice counterparty 🙂 Of course Einhorn is deviating heavily from what the market implies here…

If I remeber correctly you have yourself invested in distressed bank bonds in the past. If you think about that and take the past extreme YTM, you should have shorted the equity. But you did not do it. Because you thought the bondmarket was wrong.

As you pointed out by assuming reversion to the mean every “distressed” situation looks attractive. The question really is whether Mr Einhorn is right on his mean reversion assumptions or if there is a terminal decline and current prices are the new normal. I can just say: I don’t know. Maybe Einhorn is just nearer to the truth than the market.

If you look at the full slide deck, Einhorn assumes a lot of other stuff, like increasing prices for natural gas (he is pricing on the forward curve etc.).

And yes, I invested in subordinated bank bonds, because they had an appropriate upside for the risk. Back then I think the bonds were correctly priced for the risk (this was not risk free) but the shares were way overvalued. I din’t think the bond market was wrong, I thought the stock market was wrong, overvaluing bank equity.

Einhorn’s WACC estimate is pretty similar to the consolidated WACC figure provided by Consol Energy. You can find it on slide 170 of the analyst day presentation, 2014. The transcript provides some more color on the topic.

http://phx.corporate-ir.net/phoenix.zhtml?c=66439&p=irol-presentations

Ok, I saw the slide. But just because they say that the cost of capital is low doesn’t mean that it really is. Bond prices speak for themselves. Looking at coal and energy prices in general: I guess no bank is handing over money for 3.5% – way below the last bond refinancing round (5.875% according to the slide). So the 3.5% Einhorn used seem a little optimistic.

But then, Einhorn is a hedge fonds star…

Tom

The 5,875 percent was pre-tax. You have to use a post-tax figure. I don`t know the tax laws in the US that well, but as far as I know the total corporate tax over there is somewhat higher than it usually is in Europe. So it comes close to the 3,5 percent if you first of all assume full tax deductability and also that they could get refinancing with somewhat similar conditions. To be clear: I don`t know if these are justified assumptions.

This point goes to you 😉

Well, assuming post tax only makes sense if you actually make profits and you actually pay taxes. Consol made losses in 2015 and will make losses in 2016.

Assuming full deductability of interest agains taxes is by the way one of the most common systematic mistakes when looking at distressed companies. More on that here (slightly “wonkish” but very relvant:

Click to access 2009_cost_cap_distressed.pdf

Page 49ff.

That`s true. But obviously Einhorn expects the company to generate basically taxable income soon, otherwise it really would make no sense to buy the equity. Off course you can argue that it would be more conservative not to assume full deductability. I would be totally ok with that.

But on the other hand, if the company could save tax-loss carry forwards in the future, you could also take that into account. Again that depends on the acual tax laws, which I am not familiar with.

By the way: did they post tax relevant losses and will that continue in 2016?

yes, ~600 mn taxable loss for the first 9 months in 2015. And no, I don’t know if this will continue. You have to ask Einhorn for this 😉

Since I am just another unknown blogger, that will not work out 🙂

If he’s saying the WACC is 8% and the debt is selling for 14%, then it would be a value-add transaction to sell equity to pay off the debt. They could lock in an instant profit doing this, according to Mr. Einhorn’s assumptions.

i think his reasoning is probably this: asset sales will alleviate debt -> bond trades back at par -> low discount rate justified. obviously the credit market disagrees.

The credit market is often more realistic than the equity market….

Yeah often times this is true. But looking into their balance sheet, do you really think they would have to offer 13 or 14 percent on newly issued debt? Just in your common sense…

By the way I dont think it is correct to add the whole equity risk premium on top of the (already risk bearing) debt cost.

I think it is correct. This is clearly aditresed situation. If the company goes bankrupt, equity holders will get nithing, the bondholders will be the new owners of the company. Perosnally I think the equity risk premium should be even higher. If I would invest in such a situation I would like to earn at least 25% p.a. as a shareholder to compensate for the risk.

Well,thy would have to offer even more. New Bonds are always priced based on the yield of the outstanding bonds. Additionally investors would demand a “new issuance” premium. Why should investors buy a new bond for less than the oldbonds are trading ?

First of all, you cant just add back the whole equity risk premium, which another investor has assumed, on top of the yield of the bonds. The equity risk premium is the difference between risk free rate and the cost of equity. Since the bonds themselves are already yielding more than the risk free rate is, they are basically “covering” some of the risk. Off course you can assume a higher equity risk premium, even such a high one that you get your 25% as a shareholder. I am totally ok with that, if you think, that they are in real trouble. But in my way of looking at it it`s myopic to assume that they are in trouble, just because the bond yields are so high at the moment. Often times the bond markets are more rational, thats true. But some times they are just as way off the line as equity markets. You have to get to such a conclusion by looking at their balance sheet and their prospects, and not by just looking up what the bond market is thinking about them. Otherwise you are letting the market tell you how to think about the company, and thats also not what value investing is about.

Well, it certainly can be that the bond market is wrong and evrything is going back to normal. But on the other hand, not using this as a starting point is in my opinion stupid. Einhorn presented the case as an “asset Play” where he Claims to use conservative assumptions to come up with an intrinsic value which is much higher than the current share Price.

I think we can agree that his assumptions are not conservative but already assume significant mean Reversion to the upside. Assuming this in my opinion, is for me a “bet” and not a vlaue Investment. I am wondering why EInhorn is not buying bonds like crazy.

I can`t agree on that Einhorn isn`t conservative in his assumptions, because I haven`t deeply looked into Consols Assets. Maybe he is just plain wrong, and you are right with your assumption. So please don`t get me wrong that I am here to defend Einhorns investment case. And bond yields are something, that you clearly have to look at, no doubt. But I don`t buy the absolute conclusion, that he is not conservatively “doing” his Analysis, just because he assumes a lower cost of capital than the bond markets suggest. Thats all.

Point taken, but I still believe that assuming a 8,4% “WACC” against the Market’s 14% for debt is aggressive. On top of that I think his beta estimate is way off too….

I don`t think the Beta (however it is “adjusted”) is an appropriate risk measure for an energy and ressources company these days at all ^^

also, the 75% equity/ev is not what is today. it’s probably a circular reasoning – they arrived at their total ev first and then calculated the 75%.

No thats methodically correct. The proportions in the WACC are calculated by using the market value of debt and the value of equity in terms of fair equity value. So you weigh the equity part with what you think that the equity is worth. That creates a circularity problem which has to be solved via iteration.

Thanks for your thoughts. Always great to hear one great manager taking another manager’s idea’s apart.

Thanks for the comment 😉 but I am only an unknown blogger and EInhorn is a Billionaire…..

Don’t let that fool you, the only difference I see is, he is a better salesman than you (at this point) 🙂

Thanks.

I have the feeling that everybody is lowering discount rates (or WACC for that matter) to justify investments these days. Sometimes I think I’m really stupid for not doing this.

Feels good to recognize that I’m not the only one wondering…

Tom