Book review: Dan Lyons “Disrupted: My Misadventure in the Startup Bubble”

The book:

“Disrupted” ist the autobiographical adventure of Dan Lyons, a journalist who lost his job at Newsweek as technology writer at age 52.

The book:

“Disrupted” ist the autobiographical adventure of Dan Lyons, a journalist who lost his job at Newsweek as technology writer at age 52.

Would you consider to invest into a company which at every occasion states the following:

AQ possesses no amazing patents or other security, we rely on having the best crew.

For a “Buffett/Munger” style value investor, this would be tough as there is clearly no moat or anything close and according to Buffett, the business economics always win in the long run, no matter how well a company is run.

Welcome to AQ Group, a Swedish “non moat” manufacturing company

Great insights how the event ticket market works (hint: You’re screwed)

Armstrong Flooring could be an interesting small cap Spin-off (h/t AR, market folly)

Is there a mattress store bubble ? Plus Jeff Mathews on Mattress Firm (MFRM)

Interesting letter from Gator Capital, a HF focused on financial services companies with an analysis of post-reorg Ambac

Jim Chanos sees big issues in online and auto lending in the US

Shipping Parties in Greece are not as much fun anymore

Reading the press and comments of market pundits lately, one might get the impression that the end is near if the British referendum next week will result in a vote for leaving the EU.

Following my Old Mutual “sum of parts” valuation I saw the following Ira Sohn presentation of Exor Spa, the Agnelli family holding (FiatChysler, CNH etc.) as a potential “Sum of part” value investment.

![]()

To summarize the presentation in my own words:

The study sees a potential upside of several times the current share price. They forecast a 150 EUR NAV per share (vs. ~50 EUR now and 30 EUR share prices), driven by a quadrupling in value of the FCA and the CNH stakes.

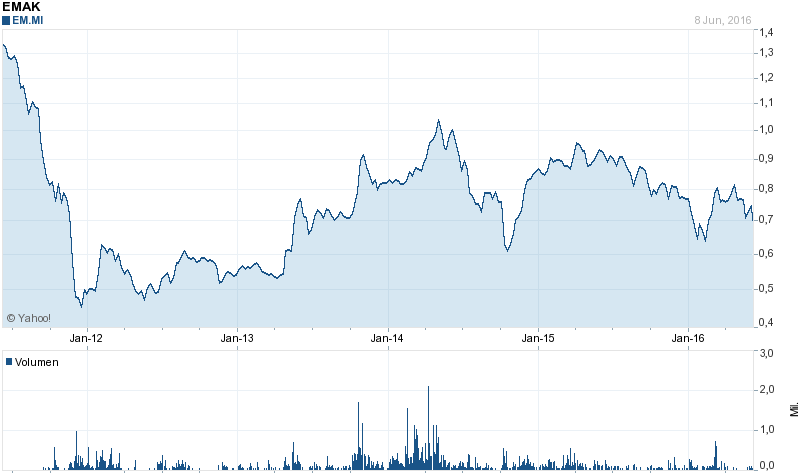

From time to time I check on previous investments how they performed and if they might be interesting again. I find this a very efficient way to create potential (re)investment ideas as only relatively little effort is needed to get up to speed.

EMAK SpA

EMAK SpA was an Italian “special situation” investment I made in 2011 following an “italian style” capital increase in 2011 and then sold end of 2013 and early 2014 for a decent profit. Looking at the chart we can see that the timing of the sale was not that bad, as after a peak of around 1 EUR in early 2014, the stock is now trading ~30% below that price:

Optically, EMAK looks very cheap now:

P/E 12,8

P/B 0,7

EV/EBITDA 7,0

In the blog I looked in the past at a couple of “sum of parts” situations (Alstom, Viel, CIR SpA but I never invested in one. Why ? Because if nothing happens, a perceived discount can remain for a long time. So for a sum-of-part investment, a “catalyst” has to be on the horizon.

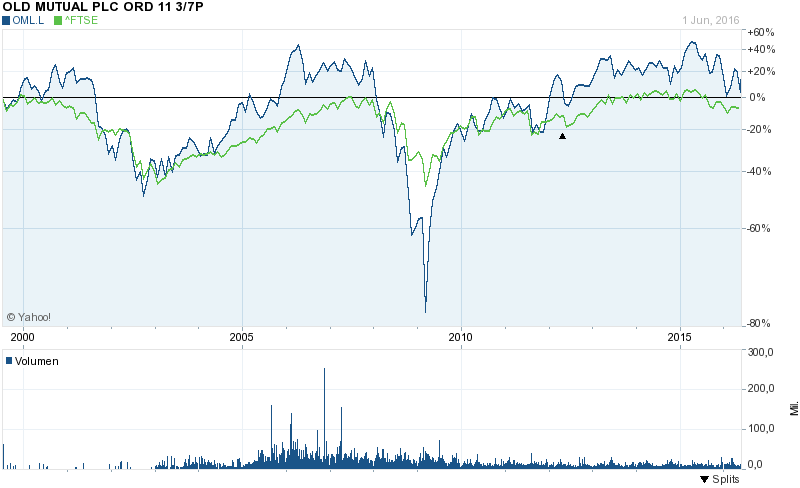

Old Mutual

As many other Emerging Market exposed financial companies, Old Mutual did not create a lot of shareholder value over the last couple of years as the chart clearly shows, although they performed better than the overall index:

.

.

“Who says Elephant’s can dance” is the book from the former CEO of IBM who took over in 1993 when IBM was struggling hard and then turned around the company until he left in 2002.

Interestingly he wrote the book himself without the help of a professional writer, which is very rare for such kind of memoirs, but makes the book very interesting.

Gerstner came to IBM from RJR Nabisco but he did spend most of his previous career ar Amex and was shocked how bureaucratic the company was. The book then describes in detail how he managed to focus the company on the then little known internet and “e-business” segment away from the focus on the traditional mainframe computers.

The most interesting chapters come towards the end of the book where he reflects on company culture and strategy.

A few of my take aways from Louis Gerstner’s insight:

At the end of the book he even gives some advice to stock analysts and proposes 5 questions to ask (and answer) when considering an investment:

Coming from a manager and not an investment guru, I think this 5 points pretty much capture everything.

Overall, I found the book one of the best “Business books” I have ever read and I can only recommend it highly.

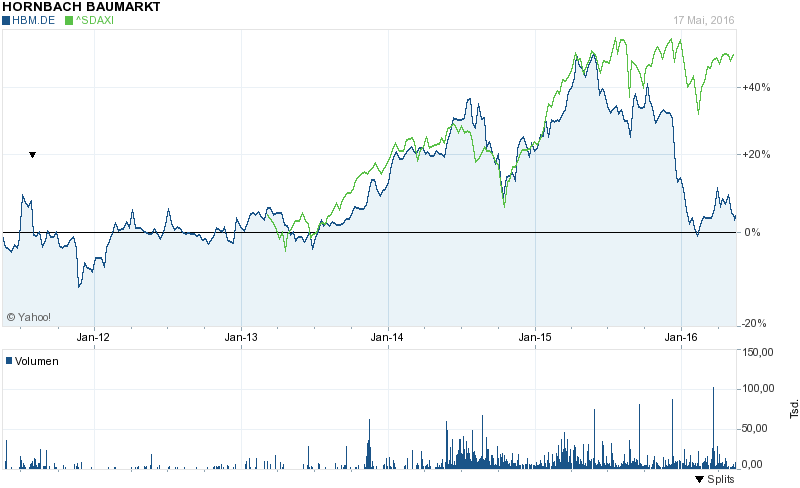

Hornbach Baumarkt is one of my few remaining initial position after almost 5 and a half years.

Looking at the stock chart we can see that compared to the German small cap index, Hornbach looks pretty lame:

At the time of writing, within my portfolio Hornbach clearly was a drag on performance with a total performance of 13,7% since 01.01.2011 vs. 109,5% for the portfolio and 73% for the SDAX.