Hornbach Baumarkt AG revisited- Where are the market share donators ?

Hornbach Baumarkt is one of my few remaining initial position after almost 5 and a half years.

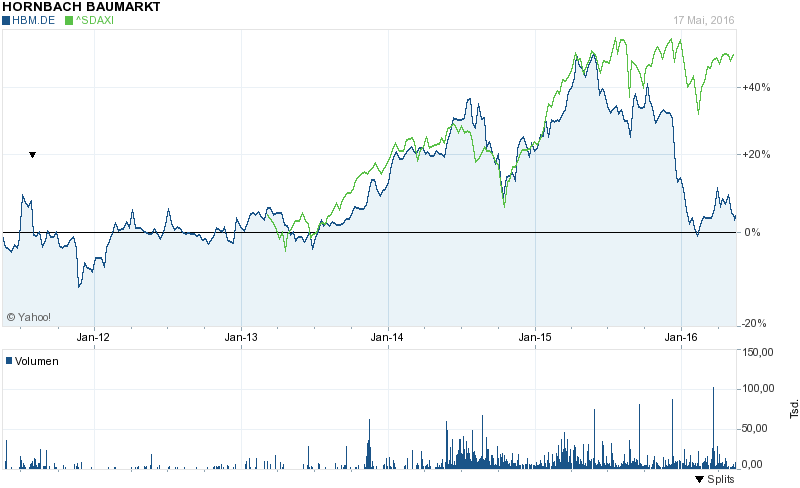

Looking at the stock chart we can see that compared to the German small cap index, Hornbach looks pretty lame:

At the time of writing, within my portfolio Hornbach clearly was a drag on performance with a total performance of 13,7% since 01.01.2011 vs. 109,5% for the portfolio and 73% for the SDAX.

What really irritates me is the fact, that despite the bankruptcy of major competitor Praktiker 2 years ago and a veritable real estate boom in Germany, Hornbach seems to struggle hard just to stand still. Yes, market share and sales increased but profitability dropped.

This leads of course to some questions. I think one can nail it down to those 3:

- Why did Hornbach perform so badly ?

- Did I make any mistakes along the way ?

- Should I keep the stock ?

- Why did Hornbach perform so badly ?

According to the just released annual report, non-German stores accounted for 73% of EBITDA and 105% of EBIT (!!!). Which means that the core German business earns close to nothing.

Germany is in a veritable building boom right now. Low interest rates and more than 1 mn refugees last year have substantially increased building activity in Germany. I would argue that fundamentally, it doesn’t get much better than that.

Hornbach itself names 3 main reasons for lower profitability in the German business

- former Praktiker stores are now run by better competitors

- aggressive “special offer” pricing of competitors

- increased costs due to “digitization”

Another reason can be found if we look at how market shares have developed in 2015 vs. 2014 in Germany’s DIY industry. The detailed table shows clearly that from the top 10 DIY chains, 9 increased their numbers of stores both in 2014 and 2015. Especially market leader OBI expanded significantly, interestingly without gaining in sales.

Basically everyone is expanding store count, there are no “market Share donators” anymore. My personal guess is that the overall positive situation in Germany combined with very low-interest rates makes it tempting for the DIY chains to expand their store base despite the fact that there are far too many DIY stores in Germany already. If the table is correct, 2016 will bring even more new stores than 2015.

Even in my own hometown one can see this easily. Market leader OBI lost 16 Franchise stores in Munich in 2013 to Hage Baumarkt, and then “of cours”e directly opened up 5 new stores in the next years.

Munich was saturated with DIY Baumarkts already before, but now there are 5 more.

So we clearly have a market where the participants are not cooperating and everyone seems to try to outgrow the others which in aggregate of course cannot work and will hit everyone hard in the next downturn. This could mean that the industry itself is really screwed for some time to come and until more than 1 of the top companies goes bankrupt.

Prize guarantees

With regard to prize competition however, Hornbach is not free of guilt. One of their cornerstone features is that they have a low price guarantee. So whenever you see something cheaper elsewhere, they will not only offer you the same item for the same price as the competitor, but they will sell it 10% cheaper than that. Other competitors offer similar guarantees for instance Hellweg , Globus and Nr. 2 Bauhaus even takes of 12% if a product is cheaper elsewhere. Interestingly the Bauhaus guarantee does not apply to internet offers whereas Hornbach even guarantees against pure internet offers. Market leader OBI doesn’t offer this kind of guarantee but maybe that has to do that around 50% of OBIs branches are franchises.

There is a lot of literature on the impact on prize guarantees on a market. I do think that the most likely outcome is the one that is mentioned here: When consumers have little hassle to compare prices (Smartphones !!!) then price guarantees will make prices very competitive which means low prices for consumer but also thin profits for companies.

I am also not sure if it is smart for Hornbach to guarantee (and deduct 10%) vs. pure internet competitors. Someone like Amazon with intelligent pricing algorithms could create a lot of issues for Hornbach.

Store format issues ?

It looks like that Hornbach rolled out a new store format: So called “Hornbach compact” stores with overall size of 1500 square meters or ~1/6 of a normal store. I have to say that this irritates me somehow. Up until now, I thought that one of Hornbach’s competitive advantages is that they always run the same “super store” concept and that different formats increase complexity. So maybe the super store concept is not the final answer.

On the one hand it makes clearly sense to try different formats, on the other hand this looks like a defensive move as the “compact” format somehow looks and sounds like the new “Screwfix” format which Kingfisher tries to roll out in Germany after selling their Hornbach stake 2 years ago. So let’s wait and see but new store formats would clearly be an additional challenge and risk especially for Hornbach with its previous “one size fits all” approach.

2. Did I make any mistakes along the way ?

Mistake 1: Forgot to update my assumptions

I think the initial investment case was not bad. A well run, family owned company in a tough market but with the biggest competitor struggling and heading for bankruptcy didn’t look so bad, especially as the stock was relatively cheap. Add on top a cheap interest rate fueled building boom and it there could have been a good outcome.

On the other hand, looking back, I should have seen earlier that not everything is great.

If I look for instance into my initial valuation, I assumed that free cash flow (before growth Capex) would be ~103 mn EUR p.a. Looking back, we can see however that actual free cashflow was close to zero in 2015/2016 and only 43 mn EUR in 2014/2015. Actually, operating CF before maintenance Capex was only around 105 mn EUR p.a.. Assuming Maintenance Capex of 30-40 mn EUR, then Free Cashflow would only be 70 mn EUR p.a. Only in the best year of my holding period, 2013/2014, Free Cashflow was near my assumed level.

If I just use those 70 mn EUR as a basis for a valuation with different cap rates, the fair value would drop from a 25-45 EUR range per share (adjusted for splits) to a range from 17-32 EUR, indicating that the shares are fairly valued.

Anchored on Book Value

Another issue is that from a book value perspective, the stock also looked cheap.Taking into account their “hidden reserves” on real estate, adjusted book value per share would be around 40 EUR or so. Stated book value increased from around 23 EUR to 30 EUR per share.

However one thing that I learned over the past 5 year is the following: If you need to invest more and more just in order to keep your profits constant, than the additional book value is not value creating.

In Hornbach’s case it is also quite unrealistic that the book value will be realised anytime soon. With the KgAA structure, there is no chance for any activist investor and I don’t expect Hornbach to change its strategy and suddenly spin-off a REIT or so.

Installux in comparison also retains profits and has relatively constant earnings, but they don’t need to reinvest. They pile up cash and if you adjust for this, returns on capital are pretty stable.

So I would argue that I was also anchored too much on book value and did not take into account the deteriorating returns enough. Interestingly enough, even my own BOSS model showed a deteriorating value starting 2 years ago which I ignored.

Other issues: Hornbach family selling stocks

The Hornbach family disposed 1 mn shares in the Holding company in October 2015 for around 70 mn EUR, a couple of weeks later Hornbach came out with a (significant) profit warning. They now own 43,75% of the holding shares but via the KgAA structure effectively control the company.

The timing of the sale at least looks “lucky” to me.

The profit warning

The profit warning in late 2015 itself has been a big riddle to me. In the annual report of the Baumarkt on page 52 they explain why they had an unplanned write down. The trigger was the IFRS rule that if the stock price is below book value, you have to test your “Cash generating units” against their book value.

What I don’t understand is the following: First, the definition of cash generating units is not carved in stone. Especially for the retail industry, there is no fixed rule how to define cash generating units. If you want to avoid write downs, a very simply alternative would have been to just combine several stores in the region and then avoid the write down. Secondly, there is always the possibility to adjust assumptions (i.e. use longer time periods, higher ultimate growth rates etc.) to avoid write downs.

Finally they mention that they haven’t actually written down only stores but also some software and other stuff.

What then really surprised me was the fact that the actual net profit for 2015/2016 was higher than the year before, despite the extra write downs. Why is that ? The tax rate in 2015/2016 is a lot lower, it seems that they had built some tax reserves in Sweden which now however needed to be released. Interestingly, the Holding had lower EPS than the year before, so at the Baumarkt, the positive tax effect over compensated the write downs. In any case, for me this is not very good communication and in connection with the stock sale even looks kind of dodgy.

Finally: Should I keep the stock ?

First I will clearly put the off my mental “do not touch” list. Secondly, I think there is no urgent requirement to sell as the downside seems to be relatively limited. On the other hand, there is not much upside either.

So Hornbach will be one of the first stocks I would sell if better opportunities come up.

As a learning experience, I think I will need to make better updates at least on an annual basis plus I will need be more critical on using book value as a measure of value and look better at industry dynamics. It doesn’t help to look for the best house in the neighbourhood, if the neighbourhood is really bad and getting worse.

Ennismore still likes Hornbach….

Click to access NL%20OEIC%20Jan%2017.pdf

Forgot to record: Sold my Hornbach Shares (to early obviously) for 25,60/per share….

These days, my decision back then looks like a good one…

Hi mmi,

I think EBIT in the German area has gone down due to their big, big investment in getting their business online. Usually companies capitalize this expense (higher intangibles) so to report higher margins (though their cash conversion will be lower); which is understandable as their assets are presumably worth more. Hornbach on the other hand chose no to capitalize this expenses so as to be more conservative. What they are saying is they don’t care about short-term performance (in the form of higher reported margins) but on long-term performance, which has several implications:

– 1) Once they have their online capabilities built up, those expenses will cease = higher margins.

– 2) That new sales channel would potentially boost sales, levered on their existing Capital Employed (their stores + warehouses) = higher asset turnover.

– 3) Accounting effect: since they didn’t capitalize those costs, their Capital Employed will be lower than peers who did.

We should see therefore a boost in EBIT + higher turnover ratios (1). These would make its profitability metrics go off-the-roof = multiple expansion (2).

This is just what comes to my mind. I haven’t decided to invest just yet, but I’m pretty close to wrapping up my investment case. What do you think? Am I missing something?

Thanks,

JuanDz.

Well, this is clearly one Scenario. I see it personally rather as a “defensive” move and therefore much more as a part of maintenace capex. If they don’t do it, they will have big issues and lose market share. Everyone else is doing it as well. It reminds me a lot of Berkshire’s decision not to invest into the new Generation of tiextile machinery. If everyone is doing it you gain no advantage, it only increases the capital intensity.

I still sell down my Hornbach Position. Could be the wrong decision, but who knows ?

Hi, this was an interesting read. Wrote an article on Hornbach myself recently, which can be found through the enclosed link if you’re interested. Thanks. http://bit.ly/timberwolfequity-hbm

Zu beachten ist bezüglich der Baumarkttochter die Entwicklung der Holding. Insbesondere die unterschiedliche Dividendenentwicklung in 2016 (0,80 auf 1,50 versus 0,60 auf 0,68) ist interessant. Gut informierte Anleger (First Eagle) haben sich in 2015 sukzessive von der Baumarkttochter verabschiedet, sind aber weiterhin in der Holding investiert

Disclaimer: Zugegeben, ich bin nach der für mich komplett überraschenden Gewinnwarnung ausgestiegen, weil sie in einem Maße der kurz zuvor kommunizierten Gewinnerwartung widersprach (und die Unterschiede nicht erklärte), dass mein Vertrauen wegbrach.

Die Jahreszeit als Ursache für Verluste vorzuschieben – hm.

[Dieses zusammen mit der Umwandlung in eine KGAA (was ich an und für sich für Familienunternehmen gut verstehen kann) könnte auf absehbare Zeit nicht wenige Investoren abschrecken.] Seit dem Ausstieg beobachte ich Honrbach eher oberflächlich.

Aber mein Eindruck war, dass Hornbach fast schon panisch Geld in den Online-Handel investiert. Dort mal eben (ohne Vorwarnung) 50 Mio in einem Jahr zu verbraten, das ist nicht ohne. Irgendwo las ich, dass der Online-Anteil im Baumarktgeschäft schon bei ca. 12,5% liegen würde, stetig und stark wachsend. Das könnte die panische Richtungsänderung erklären. (Siehe z.B. http://www.stern.de/wirtschaft/news/hornbach-baumarkt-shop-online-digital-6865926.html)

Daraus erwuchs mein (oberflächlicher) Eindruck, dass Hornbach auch in den nächsten Jahren massiv in die Online-Richtung investieren dürfte, und dass das auch einige weitere Jahresgewinne kosten könnte.

Ganz nach dem Motto “lieber in guten Zeiten auf Gewinne verzichten und tendenziell dort zuviel investieren als nachher zu spät zu kommen und abgehängt zu sein”. Wenn Online tatsächlich so stark kommt, halte ich die starke Reaktion für richtig. Je später ein Kurswechsel, desto geringer die Erfolgschancen, wie wir in anderen Punkten an Praktiker und anderen Baumarktketten sahen.

Das ist aus Sicht der Firma, der Mitarbeiter und der Familie Hornbach (für die das Lebenswerk wichtiger als der Aktienkurs sein dürfte) absolut korrekt, aber vor einer deutlichen Neubewertung (=Kurssenkung) sehe ich vorerst wenig Argumente, Hornbach-Aktien zu halten.

Apropos Buchwert: Bei Retailern schätze ich einen anständigen Buchwert als Schutz gegen schlechte Zeiten. Aber so lange die Geschäfte solide laufen, ist der Buchwert m.E. eher eine value trap, denn die Immobilien werden eh nicht verkauft. Und wenn die Geschäfte schlecht laufen, hilft der Buchwert, eine Zeitlang schlechte Zeiten zu überstehen – aber du erwähnst ja selber regelmäßig, wie schwer ein Turn Around bei Retailern ist und wie selten er gelingt. Daher würde ich mich bei der Bewertung eher an der Marktstellung (sehr stark) und den an Gewinnerwartungen (mäßig) orientieren als am Buchwert.

Das Kopieren des Screwfix-Konzeptes finde ich hingegen sehr spannend. Screwfix scheint in ungewöhnlich gutem Maß eine Verknüpfung von Online- und Brickstores im Baumarktbereich gefunden zu haben. Es spricht für Hornbach, die anscheinend besten Ideen in der Branche auszuprobieren und nachzuahmen.

Ich halte Hornbach nach wie vor für die stärkste Marke im Baumarktsegment. Trotzdem muss ich die Aktie zu den aktuellen Kursen nicht haben.

Why would the Holding need to pay any transfer taxes? They already own 76% of the Baumarkt shares and consolidate the whole Baumarkt group.

The transfer tax is based on legal entity level. Vonovia owns 93% of Gagfah and still would need to pay the tax if they merge Gafgfah into Vonovia. The threshold is 95%.

I think if they hold 94.9 per cent for more than 6 years they can buy the remaining 5.1 per cent without tax.

Market value: since the real estate should be worth more than stated in the books, you can’t take book values, of course.

Thank you very much!

Tom

this should have been a reply to your last comment below, of course

the market value can be found in the Hornbach Holding report. For some reason it is not in the Baumarkt annual report.

This was an eye-lifterer for me!

I have never even thought about the fact that even if a competitor dies… If the company that I as an investor own does not fill the gap then someone else will and it will lead to even worse competition than before.

Investing is complicated.

I wouldn’t say investing is complicated. It is actually simple but it is not easy.

Thanks for the update, I’ve got Hornbach Baumarkt shares too. But I don’t feel uncomfortable owning them and still believe it’s a good position to own. Me, and all the DIYers I know, feel that Hornbach markets typically offer the best price to value proposition for customers compared to competitors, which is a nice LT argument (although that’s only a feeling, not a fact). Higher costs due to digitization is not nice, but it could/should still play out over time.

However: do you think that, after the reorganization at the holding, there could be an attempt to reorganize further – that the holding makes an attempt to, in which way ever, take over the minority stakes (us) in the Baumarkt shares?

Somehow I have the feeling that this is the logical next step…

Tom

I am not so sure about a merger. This could trigger signifcant real estate transfer tax issues.

Interesting, I did not think about that. I guess it is almost impossible to estimate in advance how large such a tax issue could be?

no it is easy. The potential issue is Market value of real estate multiplied by real estate transfer tax. I think 5% on average should be realistic. There are ways around it, but the Gemran Government just closed some exsiting loop holes. That is one of the reasons why for instance Gagfah has not been merged with Vonovia yet.

Are you sure about that transfer tax? After all, the Holding already owns 76% of the Baumarkt and consolidates its earnings. So a case could be made that the Holding already owns the Baumarkt real estate portfolio.

Are you sure about that transfer tax? The Holding already owns 76% of the Baumarkt stock and consolidates its earnings, so a case could be made that the Holding already owns the Baumarkt real estate – or at least 3/4 of it.

yes, I am pretty sure about the real estate transfer tax.

The tax effect would be a one time thing. In contrast, how much does it cost (annually) that the Baumarkt is listed as a separate entity on the stock exchange?