From the archive: Emak Spa, Sol Spa, Piquadro – The Italian update

From time to time I check on previous investments how they performed and if they might be interesting again. I find this a very efficient way to create potential (re)investment ideas as only relatively little effort is needed to get up to speed.

EMAK SpA

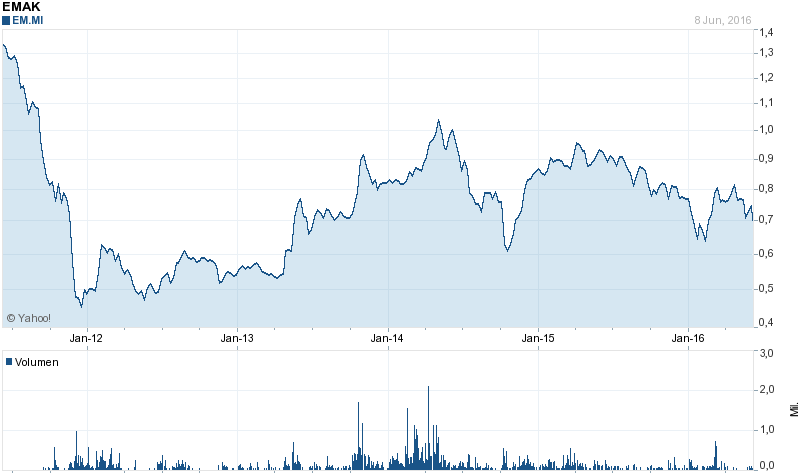

EMAK SpA was an Italian “special situation” investment I made in 2011 following an “italian style” capital increase in 2011 and then sold end of 2013 and early 2014 for a decent profit. Looking at the chart we can see that the timing of the sale was not that bad, as after a peak of around 1 EUR in early 2014, the stock is now trading ~30% below that price:

Optically, EMAK looks very cheap now:

P/E 12,8

P/B 0,7

EV/EBITDA 7,0

The problem however shows clearly if we look at these numbers:

| EPS | BV/Share | FCF/Share | ROIC | Operating Margin | |

|---|---|---|---|---|---|

| 30.12.2011 | 0,035 | 0,846 | -0,050 | 5,1% | 4,6% |

| 28.12.2012 | 0,051 | 0,876 | 0,093 | 4,7% | 6,0% |

| 31.12.2013 | 0,063 | 0,911 | 0,167 | 6,3% | 7,1% |

| 31.12.2014 | 0,064 | 0,969 | 0,021 | 5,6% | 6,8% |

| 31.12.2015 | 0,054 | 1,021 | 0,055 | 6,1% | 5,4% |

| 2001-2010 avg | 10,5% | 9,9% |

For some reason, EMAK never achieved their old margins and old returns on capital. It is also clearly that they need more and more capital just to keep their earnings stable.

Last year, EMAK made a rather large acquisition in Brazil. This is clearly a risky move, one needs to look if this plays out for them. In any case, despite the cheap valuation, I don’t think that EMAK is fundamentally an attractive investment.

SIAS SpA

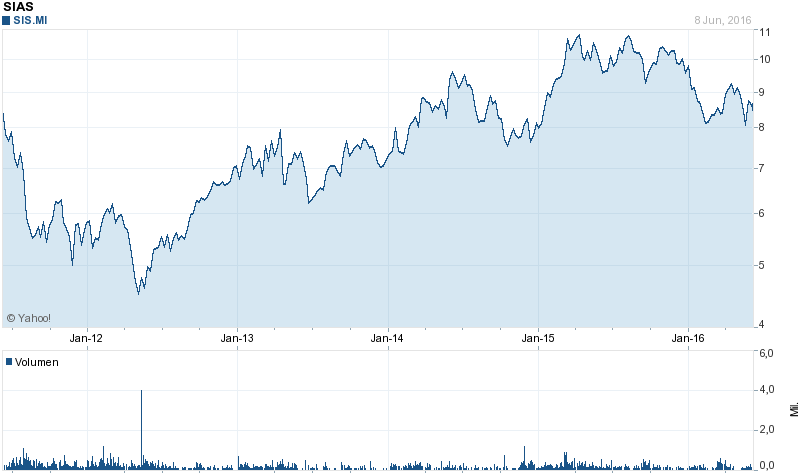

SIAS Spa, the Italian toll road operator was another “Special situation” investment I sold in early 2014, after the “catalyst” had taken effect.

The stock chart looks slightly better than EMAK but not much: The stock trades almost exactly where I sold it more than 2 years ago:

If we look at the same data as in EMAK’s case, we can see however that (with the exception of the on-offs), margins and returns have slightly recovered.

| EPS | BV/Share | FCF/Share | ROIC | Operating Margin | |

|---|---|---|---|---|---|

| 30.12.2011 | 0,671 | 6,094 | 0,517 | 5,8% | 26,1% |

| 28.12.2012 | 2,181 | 7,580 | 0,198 | 6,7% | 25,9% |

| 31.12.2013 | 0,610 | 7,377 | 0,356 | 4,8% | 24,3% |

| 31.12.2014 | 0,629 | 7,342 | 0,856 | 4,6% | 25,2% |

| 31.12.2015 | 0,706 | 7,761 | 0,770 | 4,9% | 26,7% |

| 2001-2010 avg | 7,2% | 34,0% |

Profitability is still lower than before the EUR crisis, but at least it looks like that they go into the right direction.

Interestingly, like EMAK, SIAS acquired in Brazil, too. They do have a quite detailed presentation on their website. The acquisition is interesting as they do have a good track record in South America, one of the reasons I bought back then was the fact that their Chilean assets were clearly not sufficiently valued in the then prevailing stock price.

The target is interestingly a listed Brazilian company and SIAS would own 20% of this entity, so it should be quite easy to track the success of this investment.

I do think that SIAS is on a good way. It should clearly benefit going forward from low interest rates as well. So I will put them back on my watch list. At prices below 8 EUR this could be interesting again.

Sol Spa

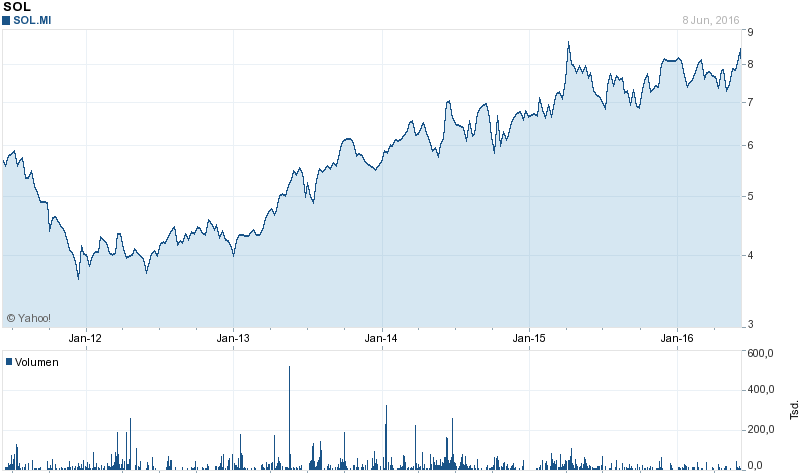

Sol Spa was a “normal” Value investment also sold in early 2014 at around 6 EUR per share.

In contrast to EMAK and SIAS, Sol however kept going up nicely:

Looking again at the numbers, at first sight it is not clear why Sol performed so much better and is trading at a 23x trailing P/E and 1.7 times book value:

| EPS | BV/Share | FCF/Share | ROIC | Operating Margin | |

|---|---|---|---|---|---|

| 30.12.2011 | 0,343 | 4,017 | 0,011 | 8,0% | 10,8% |

| 28.12.2012 | 0,320 | 4,171 | 0,023 | 7,1% | 9,7% |

| 31.12.2013 | 0,238 | 4,228 | 0,088 | 5,2% | 9,0% |

| 31.12.2014 | 0,322 | 4,505 | 0,307 | 5,9% | 9,7% |

| 31.12.2015 | 0,358 | 4,884 | 0,068 | 5,4% | 9,7% |

| 2001-2010 avg | 2,9% | 10,7% |

Returns on capital clearly decreased although operating margins remained quite stable.

So why is the stock doing so well ? If we look back to the first post, we can see that Sol Spa is actually a tale of 2 companies: A struggling local Italian Industrial Gas company and a rapidly expanding Pan-European healthcare player.

Back in 2010 the healthcare business had around 220 mn Sales and 31 mn operating profit, the traditional business had 331 mn sales and 29 mn OP.

In 2015 however, the technical gases had sales of 370 mn with an OP of 23 mn, whereas the Healthcare segment showed 350 mn revenues and 42 mn OP. So in 5 years the healthcare segment grew by 50% in sales and 1/3 in OP which is very remarkable.

In Sol’s case it seems that people really understand the attractiveness of this rapidly growing segment, which at some point in time will simply outgrow the “bad” business. Clearly, in Sol’s case I was not patient enough as this was not exactly a secret. At current prices I still think Sol is expensive but maybe a will do a similar post in 2 years time….

Piquadro

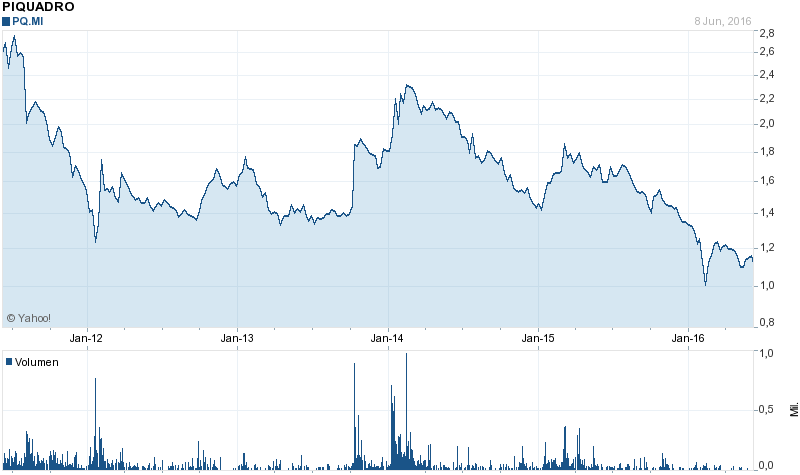

Piquadro, the manufacturer of technical bags was an investment I bought early but then sold in 2012 because I identified some structural problems, especially with regard to their wholesale sales channel and results started to deteriorate.

Since then, not much happened.. Profits dropped by -50% and pretty much stayed there. They will release figures for FY 2015/2016 in a few days, but I do not expect very positive numbers.

Looking at the stock chart it is interesting that for some reason the stock went up a lot in 2014, but now is lower than in 2012:

Overall, I think their problem is still that they are not a first tier brand and will have a very hard time to earn the margins the had under the old wholesale business model which doesn’t really work anymore.