Old Mutual Plc (ISIN GB00B77J0862): Buy one, get four ?

In the blog I looked in the past at a couple of “sum of parts” situations (Alstom, Viel, CIR SpA but I never invested in one. Why ? Because if nothing happens, a perceived discount can remain for a long time. So for a sum-of-part investment, a “catalyst” has to be on the horizon.

Old Mutual

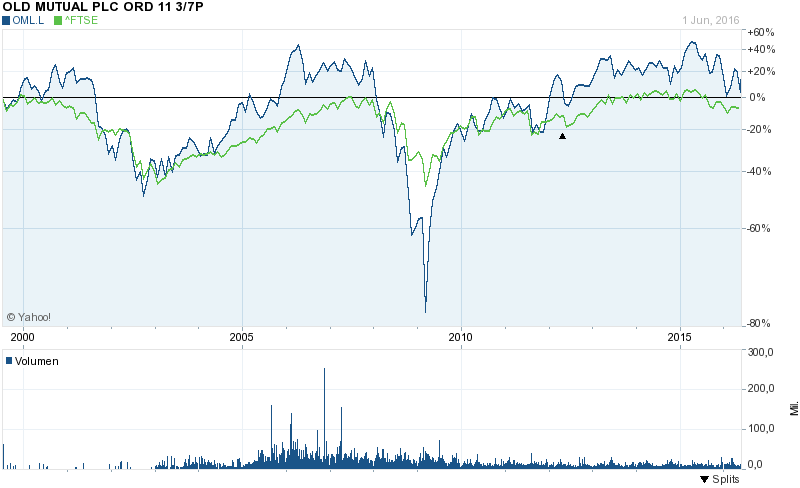

As many other Emerging Market exposed financial companies, Old Mutual did not create a lot of shareholder value over the last couple of years as the chart clearly shows, although they performed better than the overall index:

.

.

The business

Old Mutual is a combination of 4 major businesses:

1. A majority stake in listed South African Nedbank

2. A non-listed but quite succesful UK private wealth management

3. A majority stake in a listed US Asset manager (OM Asset Management)

4. An Emerging market insurance company headquartered in South Africa

Just by looking at this combination, it becomes pretty clear that with the Brexit discussion and recent Emerging MArket performance, Old Mutual is not a favourite with analysts in its current form. Luckily, the new CEO Bruce Hemphill clearly seems to recognized this.

Just a few months after taking office, Old Mutual announced in MArch that they will break themselves up and or sell major parts of the business.

The plan so far looks that they want to:

1. Sell down the Nedbank Stake to a minority position

2. IPO/spin-off or sell the UK Wealth management

3. Sell the US Asset management

4. Keep and concentrate on EM Insurance business

They want to achieve this by 2018, so a quite short period of time.

At first sight, Old Mutual doesn’t look that so attractive for a financial company:

Market Cap: 8,7 bn GBP

P/E (2015): 13,3

P/B 1,23

Div. Yield 5%

Sum-of-parts valuation

2 of the 4 businesses are listed stock are listed. For a sum of parts valuation, one could take the market value of the stake as base case. In a negative case one could make a 10% “discount”, the upside case would be that an acquirer pays ~30% control premium.

That leaves us to estimate the value of the 2 other businesses plus deducting any kind of financial debt.

UK Wealth management business:

In the press there was a rumour that Private Equity companies would bid something between 3-4 bn GBP for that business. If one takes the multiple of a very similar company, St. James Place, an ever higher valuation could be justified in an optimistic case.

Emerging market Insurance company

Personally, I find the emerging Market insurer very interesting. Growth is scarce in the insurance world and growth trades at significant premium. I would use a 12x multiple on profit in a negative case, 15 as mid-case and 20 as optimistic (i.e. including control premium).

Deduction: External debt, internal debt

According to the segment balance sheet of the annual report, Old Mutual had ~1,37 bn GBP external debt at Holding level plus 900 mn GBP internal debt, which need to be deducted. Against that we have 750 mn GBP cash at the HoldCo which we need to add.

Interestingly, the pension liabilities seem to be no problem in contrast to many other UK companies. They are relatively small and ~20% over funded based on IFRS, this means economically they should be more or less OK.

Special case: Sum-of-parts Insurance companies

When looking at Insurance companies, it is important to know that you cannot simply add reported equity stakes up. Although Warren Buffett calls insurance reserves “float”, in reality those liabilities are still debt. Whatever assets are financed by the insurance liability can therefore not be added to a sum-of-parts valuation because if you sell them, the cash has to remain within the insurance company to cover those reserves.

On Old Mutual’s case, Bloomberg reports that of the 52% stake in Nedbank, actually 15,66% are held by Old Mutual Life Insurance company. So one should deduct this stake from the sum of parts valuation.

Let’s look at the numbers:

So we can see that the base case shows a value of ~1,96 GBP per share. In an optimistic case there would be a nice upside of more than 50%, pessimistically the stock looks slightly overvalued. In the sheet I have assumed 50% probability for the base case and 25% for the optimistic and pessimistic case.

That results in expected upside of ~18%. According to what they say, the split should be executed by 2018. So this would be (incl. 2 dividends) a return of ~14% p.a. which might be a little bit to low in my opinion if we consider the risks (see below). Personally I think I would want to earn rather something like 15-20% p.a. on this one.

S0 based on my analysis, Old Mutual should trade at least ~10% lower than currently, or there would need to be clear prove that the positive case is more likely

Other considerations

One of the biggest risk of a break up situation is that management doesn’t execute or it executes too fast.

In old Mutual case, there seems to be a proposal on the table that generates a nice payout for the CEO if he completes the break up until 2018. A quick look into the details shows that the incentive is share based, so I do think this should align shareholders and management to a large extent.

Clearly, even if the break up is done in 2018, there is no guarantee that we will actually have my assumed values realized. The chances for a revaluation clearly increase but there is no certainty.

Brexit

I have no view on the Brexit, in the case of Old Mutual I do think that their business is only slightly impacted by a potential “Brexit” whatever that would mean.

Actually, any downside volatility might offer interesting entry points for this potentially interesting special situation.

South Africa

Last Friday, S&P did not downgrade South Africa to junk, but clearly at the current level of commodity pricing, South Africa is struggling. However in my opinion there is a lot of bad news already priced in so I would not feel uncomfortable with that risk, at the right price of course.

Why do they do it ? —> Solvency II

The big question is of course: Why do they do it ? Just being nice to shareholders ? The solution in my opinion can be found in the annual report on page 71 & 72.

They present a variety of Solvency figures, but the most important one, the Solvency II ratio was 135% at year-end 2015 which is very low if you compare this to competitors. Why is it so low ? Mainly because majority stakes in other financial companies such as Banks or Asset Managers are not taken into account under Solvency II to avoid “double gearing”. Under the old rules this was possible, under Solvency II, “financial Supermarkets” do have a problem.

For Old Mutual, this is even more an issue, as their main business is not even within “Solvency II land”. So if you want to grow strongly in a region where your competitors are not subject to Solvency II, you are at a disadvantage.

Strategically I find this a very good move, the alternative would heave been to cut dividends and/or increase capital.

Summary:

Overall, I do find the Old Mutual break up a very interesting situation. However at the current price, the expected return doesn’t fully cover my return requirements.

I will keep Old Mutual on my watch list, as their might be a chance to buy cheaper before or after the Brexit vote. Also I think along the way there might be more opportunities to benefit from this rather shareholder friendly break up plan (spin-off of UK Wealth management, remaining EM Insurer).

–

MMI Good analysis. I also like the break up but have to date not had the time to look at the numbers. Thanks for giving me a good base to work from.

HI, I like you blog very much, it’s always pleasure to read it. Thank you.

I noticed that you calculate total expected upside as sum of all expected returns, I think it should be weighted average of probabilities.

If you look at the table, you can see that I multiplied the expected returns with the probabilities first. Then you can just sum them up.

mmi

HI, Total expected upside should be weighted average of probabilities. Not just the sum of all uneaqual in probabilities expected returns.