Energiedienst Holding AG (ISIN CH0039651184) and German electricity prices

I started my small 2013 utilites project with E.On 2 weeks ago. Instead of working through the list of German utilities I wanted to focus on Swiss listed Energiedienst Holding AG first.

Energiedienst is a slightly unusual stock. It is listed on the Swiss stock exchange, but its balance sheet is in EUR. The company basically runs a number of big Hydro power plants along the Rhine River plus some smaller Hydro Power plants in Southern Germany and Switzerland as this map shows:

Market cap: 1.3 bn Swiss Francs

P/B 1.1

P/E 12.0

EV/EBITDA 7.1

Dividend yield 2.3%

From a simple valuation point of view, Energiedienst does not look overly attractive, however one should mention that they do have net cash which is quite uncommon for utilities.

The company is majority owned by German ENBW (67%) plus a company called “Services Industriels de Genève (SIG)” which bought a 15% stake in 2011 from ENBW (remark: ENBW itself is in quite big trouble because of the Nuclear exit in Germany).

Business model

In addition to the Hydro plants, Energiedienst owns a distribution network with around 750 tsd clients in Switzerland and Southwestern Germany. The focus is clearly Germany with more than 80% of sales there. Energiedienst produces around 25% of its energy itself, the rest is bought in the market.

The interesting point is that their own electricity production is almost 100% Hydro power. Hydro power, in contrast to power from fossil fuel, is more or less a pure fixed cost business. You build the hydro plant, depreciate and that’s it. If electricity prices go up, you earn more, if they go down you earn less. You don’t have to worry about oil or coal prices. On the flip side, hydro power depends on the amount of water available, so in dry years you can produce less or more in wet years which introduces some uncertainty.

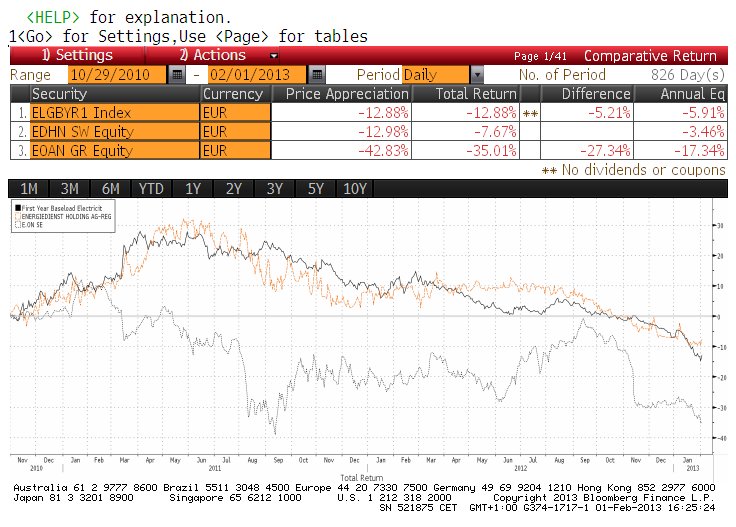

But in any case, a Hydro Power “pure play” is more or less a “bet” on electricity prices. In order to check this theory, I let’s look at EDHN’s share price (in EUR) against 1 year forward prices for German electricity (as a comparison, I plotted E.on as well):

I find it fascinating that over the past 2.5 years, Energiedienst more or less directly followed German power prices. We can see that E.on is much more volatile and most likely exposed to general stock market fluctuations.

Just for the complete picture a history of German wholesale electricity prices since 2007:

It is interesting to see that German power prices seem to be at the lowest level since the beginning of this time series in 2007. After the surprise phase out of nuclear power after Fukushima and the corresponding propaganda from E.on & Co, one might have expected exploding electricity prices. But it looks like that the new supply of alternative energy plus maybe reduction in consumption led to a dramatic decrease in electricity prices.

Digging deeper, I found for instance this German publication from 2011 which confirms the point, that the subsidized renewable energy will lower electricity prices in general. So for a renewable hydro player like Energiedienst, the subsidies to solar and wind have the “perverse” effect of lowering the profit of this very cheap type of electricity significantly.

The “trick” is that the electricity distributors have to buy the renewable electricity at fixed subsidized prices, but have to sell it at current market prices into the German electricity exchanges. The difference then gets charged to consumers. According to the paper, the electricity price clears at the level of the most expensive supplier. The mechanism for the renewable providers however introduces practically a big source of potentially extremely cheap electricity as it gets sold at market prices no matter how low they might be and “unelastic” to the actual demand.

Due to the low interest rates, subsidized wind parks and solar plants are still attractive investments despite the price for electricity being at multi year lows and demand being rather weak.

So the low prices are not a result of low demand, but mostly of subsidized renewable energy which will be sold as long as the price is higher than zero.

Zero hedge just had a post in its usual style, claiming that the falling energy prices are a harbinger for falling stock prices. That is correct for utilities but other than that it is just a result of the mechanism described above.

Summary:

The current system for renewable energy in Germany (selling renewable electricity into the market at any price with the consumer paying the difference) is hell for “traditional” utilities including hydro power.

The German utilities have maybe underestimated the extent of renewable production, otherwise they could have done the exactly same thing themselves. Now howver, the are in a kind of “death grip” between having to run their expensive black coal and gas plants for peaks and the articificially low electricity prices. Combined with unfavourable natural gas delivery contracts, especially for E.on the air will remain quite thin.

So unless something changes significantly, German utilities (including Energiedienst) will need a long long time to adjust capacity and change their business models.

Warren Buffet seems to be much more clever: If you can’t beat them, join them. I think this is the reason why his US utility is investing so much into Solar and Wind.