Operating Cash Flow and interest expenses – (ThyssenKrupp vs. Kabel Deutschland, IFRS vs. US GAAP)

In my recent post to Kabel Deutschland, I made the following remark:

Interestingly, the “operating cashflow” does not include interest charges. In my opinion, interest charges are operating, as they have to be paid regularly and there is no discretion like dividends. So in my view Kabel Deutschland currently runs free cashflow negative and dividends are paid out from the increase in debt.

After some discussions, I was less sure about this myself so I thought it might be a good thing to look at this more closely.

Before jumping into “definitions” of how to calculate and report different cash flow definitions, one should take one step back and ask oneself:

What is “free Cash Flow” supposed to mean anyway ?

The current mantra for most “sophisticated” investors is that you should more or less forget earnings and concentrate on “free Cash flow” as this is the most important metric for determining the value of any (non financial) company.

“Free Cash Flow” in plain English should quantify the amount of money which is generated by a company over a certain period of time (usually 1 year) which can be used in a discretionary fashion to either grow the company, pay dividends, buy back shares etc.

In order to calculate this number, you normally start with operating cash flow, which in theory should contain all cashflows to operate the business on a going concern basis and then deduct cash out for normal Capex, i.e. investments required to ensure the “status quo” of the company.

Further one has to distinguish between two perspectives when deciding how to calculate Free Cash flow:

Free Cash flow to the firm vs. Free cashflow to equity

The single most difference between Firm/equity perspective is that in the “firm perspective” one assumes that the financing structure is discretionary. One wants to evaluate the whole value of the firm based on the firm wide discretionary cashflow.

However, with free cash flow to equity, I have to take the current financing structure as given and one has to calculate how much of discretionary cash flow is left for the shareholder. This of course implies, that interest charges are not discretionary for a shareholder but have to be subtracted from Free cash flow to equity.

This is especially important for highly leveraged companies where interest expenses can “eat away” a lot of discretionary cashflow.

The problem:

So far so good, where is the problem ? The problem is that different companies report cashflow differently.

Let’s look at Thyssenkrupp for instance:

They start with Net income and adjust for depreciation etc. but not for interest expense. Interest expense ist therefore shown within Operating Cashflow (net finance expense was 168mn, maybe they didn’t bother with -1.3 bn operating cashflow.

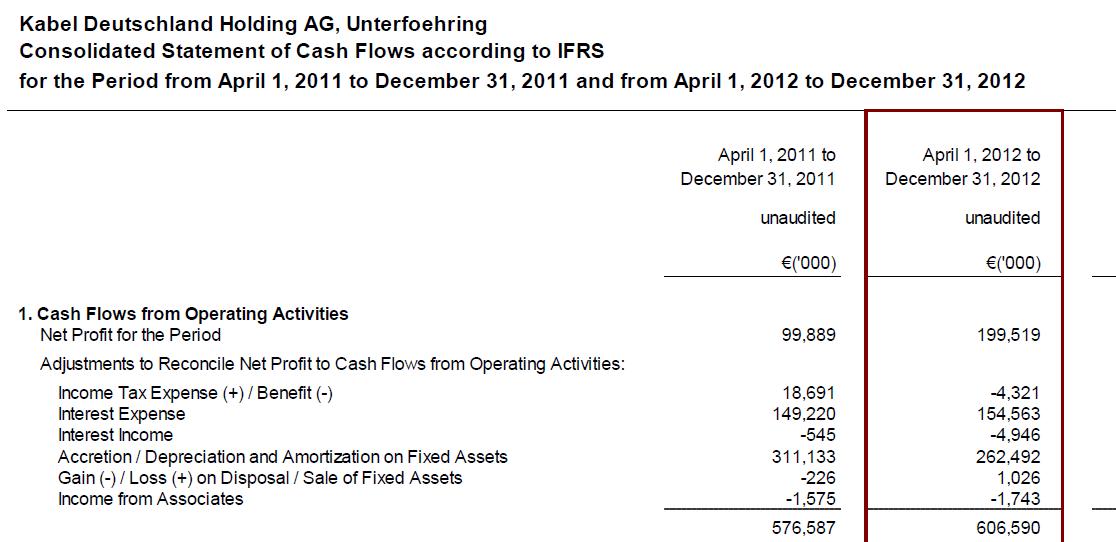

Now let’s look at the 9M Kabel Deutschland Cashflow report:

We can see that other than Thyssen Krupp, Kabel Deutschland adds back interest expense to Operating CF.

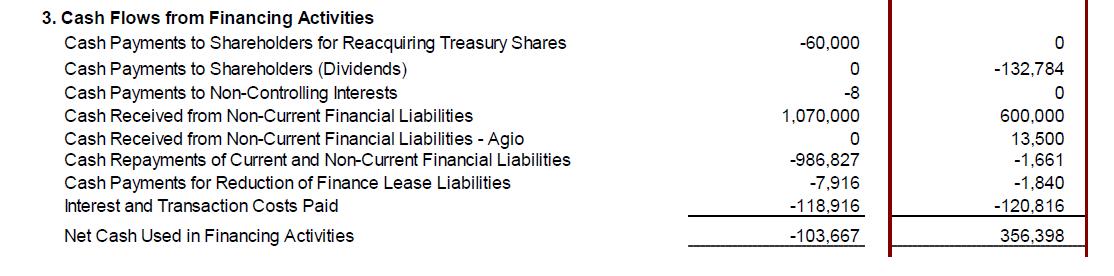

Later on, we can see interest expense under Financing Cashflow:

Accounting view

Under US GAAP it is clear: Interest expense belongs to the Operating cashflow statement. Under IFRS however a company can can choose between Operating and Investing Cashflow (see here, 7.15)

So we can see, there is nothing explictly wrong with Kabel Deutschland from a reporting point of view, they just have chosen to report interest expenses under Financing cashflow.

There is an interesting paper to be found here which makes the following observations:

We find that firms with greater likelihood of financial distress and a greater probability of default make OCF-increasing classification choices. We further show that firms accessing equity markets more frequently and those with greater contracting concerns are also more likely to make OCF-increasing classification choices. Firms with negative OCF are less likely to make OCF-increasing classification choices.

So that is no surprise that a PE “boot strapped” company like Kabel wants to show higher OCF and FCF and opts for Financing Cashflow.

What to do & Summary?

In my opinion, you have to make sure first that you compare apples to apples if you look at two different companies and compare free cashflows. Make sure that you treat this consistently. I am not sure if all the US investors which hold the largest stakes in Kabel know about this small but important reporting difference.

Secondly, I personally think that interest expenses always should be deducted from Operating Expenses and therefore Free Cash Flow in any equity valuation exercise.

Imagine for instance a company which rents its building against a company which takes out a loan to buy the exact same building. In the first building, you would subtract the rent clearly from operating profit, so why would you not subtract the interest on the mortgage for the second company ?

Hi MMI, and sorry for going back to an old post.

You say:

“Imagine for instance a company which rents its building against a company which takes out a loan to buy the exact same building. In the first building, you would subtract the rent clearly from operating profit, so why would you not subtract the interest on the mortgage for the second company ?”

In my opinion, the thing is that the rent you DON’T pay if you own the building goes out in “Depreciation” (if you pay rent because you don’t own it, you don’t depreciate the building; it is the owner who does). Since the building depreciates with time, you have to compensate somehow for that decrease in value or else you will see yourself with a useless building at the end of its useful life. That compensation is maintenance capex, which is a component of Free Cash Flow.

Your way, what you are doing is double counting.

I think interest expense should be a financing cost, as it comes from a financial obligation. What I like to do is adjust UP the discount rate for companies with lots of debt (adjust higher, contrary to what modern finance theory tells you), as the risk with this type of companies is higher. By how much do I adjust it? Well, subjective answer depending on the company in question…

This way I can compare business models, out of cash flows, irrespective of their capital structure.

JD,

thanks for the comment. No I don’t think that I am double counting, as the post was about Operating Cashflow and depriciation is a non-cash expense which is eliminated within the OpCF calculation . How you the calculate Free Cashflow is a different story. But again, anyone can adjust whatever he/she likes. I am not a professor who wants to teach something to university students, I just wanted to show that in IFRS statements, interest can either shjow up in OP CF or in Financing CF and I think that is more appropriate in the OpCF section.

I screwed up the format, I apologize. I’m posting it again (maybe erase last comment?). So sorry.

———————

Hi again,

Sorry if I didn’t express myself correctly.

EBIT

+ A&D <——— added back

– Tax

– WC

OpCF

-Mant. Capex Capex, the asset base decreases, which, assuming same turnover, means decreased sales. And vice-versa. Assuming no efficiency, utilization nor price increases, the only way to increase turnover (that I can think of right now) is through off-balance sheet assets (debt). Therefore, rent would replace manteinance (or growth) capex, not interest expense. In my opinion, higher financial expense would be a consequence of higher financing needs, due to a more financially (and operationally) levered business model. Therefore, I would subtract the FV of all on- and off-balance sheet liabilities from my discounted cash flows to arrive at my IV.

EBIT

+ A&D <——— added back

– Tax

– WC

– Interest exp <———- removed

OpCF

-Mant. Capex <———- removed

-Growth Capex

FCF

In other words, assuming a business was to transition to an off-balance sheet model, you'd have to lower future capex needs while adjusting for higher interest expense.

So, going back to the question you leave open in your post: "Imagine for instance a company which rents its building against a company which takes out a loan to buy the exact same building. In the first building, you would subtract the rent clearly from operating profit, so why would you not subtract the interest on the mortgage for the second company ?”

My answer: because the maintenance capex needs of the company just went up – you sub-tract the new capex needs from OpCF.

Rent is more opex intensive, ownership is more capital intensive.

In terms of cash flows, how would you compare two businesses from the same sector, one highly levered, not so the other one?

well, I think it is not the same. If you pay rent, you have to pay rent.

If you own the building but you financed it via a mortgage, you have to pay the interest. The Capex you mentioned however is not fixed. You can decide to do it earlier or not at all (which in the long term of course then creates bigger problemw).

For me, oeprating CFs are those cashflows that you have to pay no matter what. Not paying interest or not paying rent will lead most likely to default.

Saving on maintenance capex is much more discretionary and is therefore less “operating” in my opinion. This is actually one of the “dirty secrets” of Private Equity: In many cases, they simply reduce maintenance capex to the very minimum in order to generate cash for paying the interest on the leverage.

If you create “short term free cashflow”, you can actually let Capex out of the picture. Clearly in the long term, depriciation is a real Cash expense.

So coming back to your final question: All other things equal i always would go for the company with less (adjusted) leverage because it is less risky.

Do you think that it matters on the type of company? For instance, what if the debt is chosen to serve as a tax shield, not due to necessity? In this case, should you include Interest payments in CFO, for say, valuation purposes?

One example I would give is Vodafone. Of the 115bn in EV, only 20bn is Debt and 1.6bn in Interest payments compared to Adjusted FCF of 5bn. In this instance, I’m debating whether to include Interest payments in CFO and the reason is that a large company like Vodafone can easily retire that Debt and replace it with Equity.

Do you agree that it depends on the need for Debt or do you always treat Interest as CFO?

Thanks

thanks for the comment. No,I don’t think it depends on the type of debt. If Vodafone for instance tries to retire debt and replace it via equity, I dOn#t think shareholder will like this very much….

mmi

Yes, I’m always forced to make a mental adjustment when I switch from US to non-US cashflow statements – quite annoying! I tend to prefer the IFRS version – especially UK cashflow statements (so maybe it’s whatever is most familiar!). But I think I have a good reason:

It’s often true that acquiring companies may have a v different capital & tax situation than their targets. Net income, or free cashflow, isn’t (necessarily) something they focus on, but I think Operating FCF is v important to them. [Which I define as Operating Cash Generated from Operations (exc. Tax & Net Interest) – Net Capex/Investment in Intangibles]. So a breakout of Taxes & Interest in the cashflow is v relevant & useful to evaluating the intrinsic/M&A value of a company.

I find this a v useful figure to focus on in my analyses, and a great way to endorse the operating profit margin in the P&L (of course, Op FCF should, on average, be equivalent to Op Profit). I also tend to find companies where Op FCF is meaningfully higher/lower than Op Profit are often significantly mis-valued.

And if a company’s distressed, I will ignore the P&L, and rely much more rigorously & conservatively on the cashflow statement (which, in those circumstances, usually looks far worse). I do think actual FCF (after interest & taxes) is important though with distressed co’s as you’re evaluating their ability to actually fund their obligations & survive (the P&L will probably be completely misleading in this regard).

a) [Free Cash flow to the firm] discounted by [cost of capital] minus [market value of debt] plus [non-cashflow net assets]

b) [Free cashflow to equity] discounted by [cost of equity] plus [non-cashflow net assets]

Bot should yield the same value of equity.

As a quick proxy I compare ev/ebit, where ebit ~ operating cashflow. This is an assumption, but I don’t know a quick better way. Then I adjust ev for things like pension deficits and ebit for one-offs, discontinued etc.

I don’t understand why it should make sense to give companies choice in this matter with IFRS. Why not force them like gaap does?