DCC – Interesting “Special Situation” following KKR potential buyout offer at 58 GBP ?

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!!

DCC is an investment I made back in December 2022. The investment thesis back then was that it was a successful compounder/serial acquirer that had the opportunity to grow further through its 3 platforms (Energy, Healthcare, Technology).

In the meantime, a lot of unexpected things happened. After issues in the non-Energy segments, DCC is currently transforming itself back into the original Energy distributor and sold already a significant part of its non.Energy businesses. The transformation has progressed well including a share buy back tender but is not finished yet.

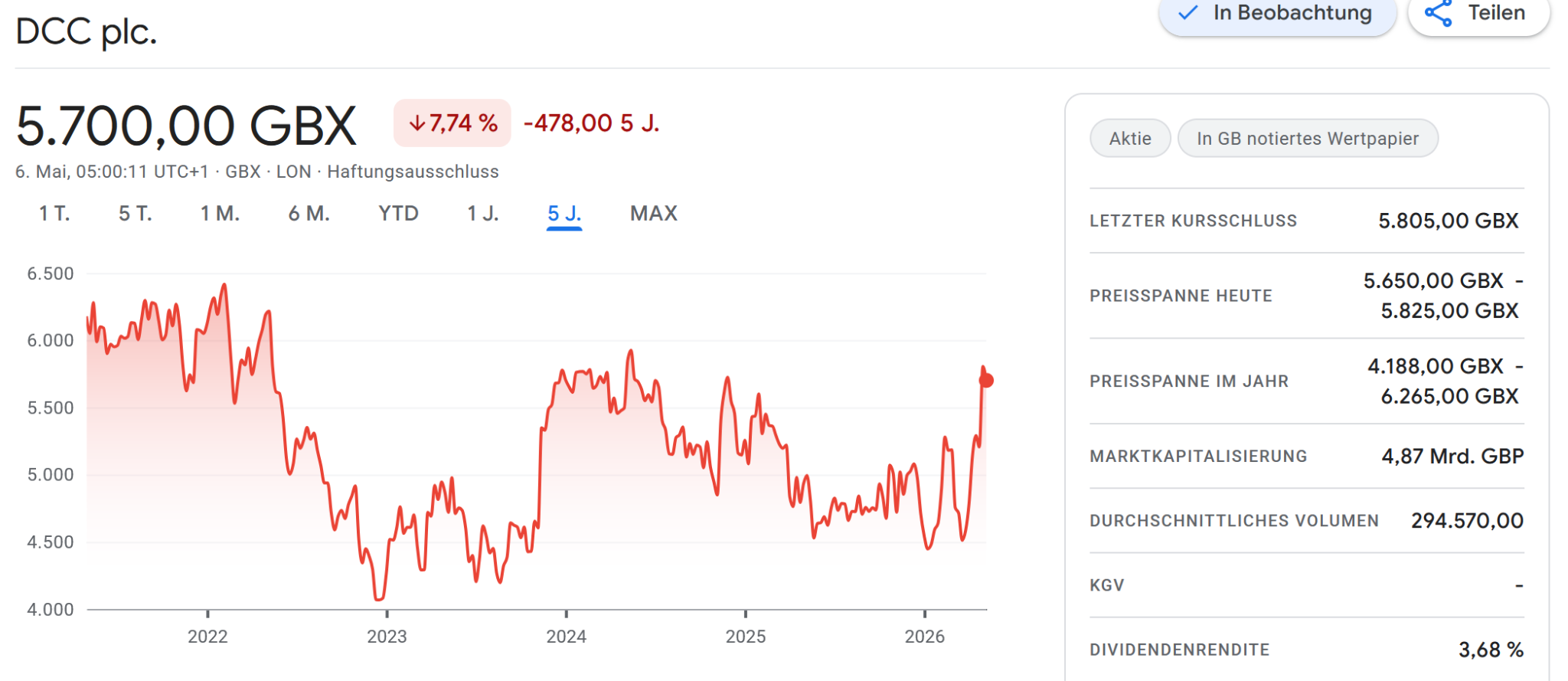

Looking at the share price, we can see that not much happened over the last 5 years but that the timing for buying into DCC in Dec 2022 retrospect was quite lucky:

After the recent jump to 58 GBP, I am up 42% in total (in EUR, including dividends) which is not spectacular and rather at the lower end of my expected outcome. However, given the “Pivot” it is still a decent result and mostly attributable to the low entry point and the relevant dividends.

Now fast forward to last week:

Private Equity behemoth KKR and another energy focused PE called Energy Capital Partners approached DCC and seem to have informally offered to take over DCC at 58 GPB per share which only represents a 15% premium over the average share price for the last few months.

DCC immediately declined the offer as “too low”.

Energy Capital Partners is a pretty large Energy focused US PE/Infrastructure investor that owns a lot of “Energy Transition” businesses. AuM seems to be north of 40 bn USD.

Although KKR did not disclose which fund is bidding, it looks that both KKR and ECP see this as an infrastructure play which makes a lot of sense.

58 GBP per share is clearly a low ball offer and no formal offer has yet been made. Under the applicable Irish laws, KKR has time until June 10th to either submit a formal offer or walk away.

From a shareholder perspective, I assume that maybe a lot of investors have been frustrated that the stock only went sideways for the last 5 years or so and are maybe happy to exit at that level.

The “asset heavy” Infrastructure PE playbook

DCC so far has operated as a relatively capital light distributor, but I think it is relatively easy to pivot them into an Infrastructure like business that usually enjoys significantly lower cost of capital.

In contrast to “normal” Private Equity, Infrastructure Private Equity still enjoys a pretty good time. Many players have raised large funds and are eager to deploy money. Infrastructure is often considered “AI safe” these days.

So I guess there might be a chance that some other players might look very closely at this situation. DCC is a very obvious target and the timing is quite nice from a PE perspective. The refocusising on Energy at DCC is still underway and the results don’t look so “clean” at the moment,

DCCs business model, especially the LPG distribution business has a lot of potential to get easy access to many SME companies and sell them solutions.

Especially the current volatility in fossil energy prices opens up a unique selling opportunity for solutions that offer less exposure like rooftop solar etc.

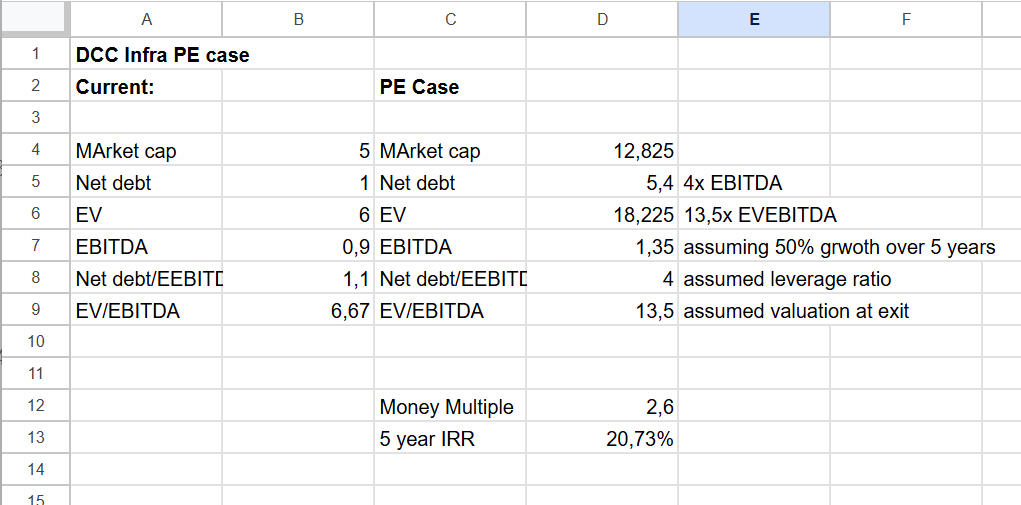

According to TIKR, DCC’s Net debt to EBITDA ratio is only around 1,2x. The company is valued at around 7xEV/EBITDA. The typical infrastructure playbook would be to make the company more “asset heavy”. Due to the low gearing, this could be financed by more leverage. A typical “asset owning” infrastructure company with longer term contracts can be easily levered 4-5x Net debt/EBITDA,

In DCC’s case, with around 900 mn in EBITDA, increasing the leverage ratio to 4x would allow them to issue almost 3 bn in debt which could finance a lot of assets. Those assets then will automatically increase EBITDA,

A stabilized infrastructure like company can then be sold at much higher multiples, usually at 12-15x EV/EBITDA. So the value creation potential for a good Infrastructure PE shop is significant.

Just for fun I did a high level calculation how that exercise would look from this perspective (I just took the current numbers from TIKR, before further disposals):

A potential IRR of above 20% p.a. is highly attractive for an Infrastructure fund and as I have written before, PE’s have some more levers to “juice up” the IRR and earn even higher performance fees.

Is DCC now an interesting special situation play ?

There is clearly the risk that DCC might reject even higher offers, but I do think the 58 GBP low ball offer provides a decent “floor” for the stock (“Anchoring effect”).

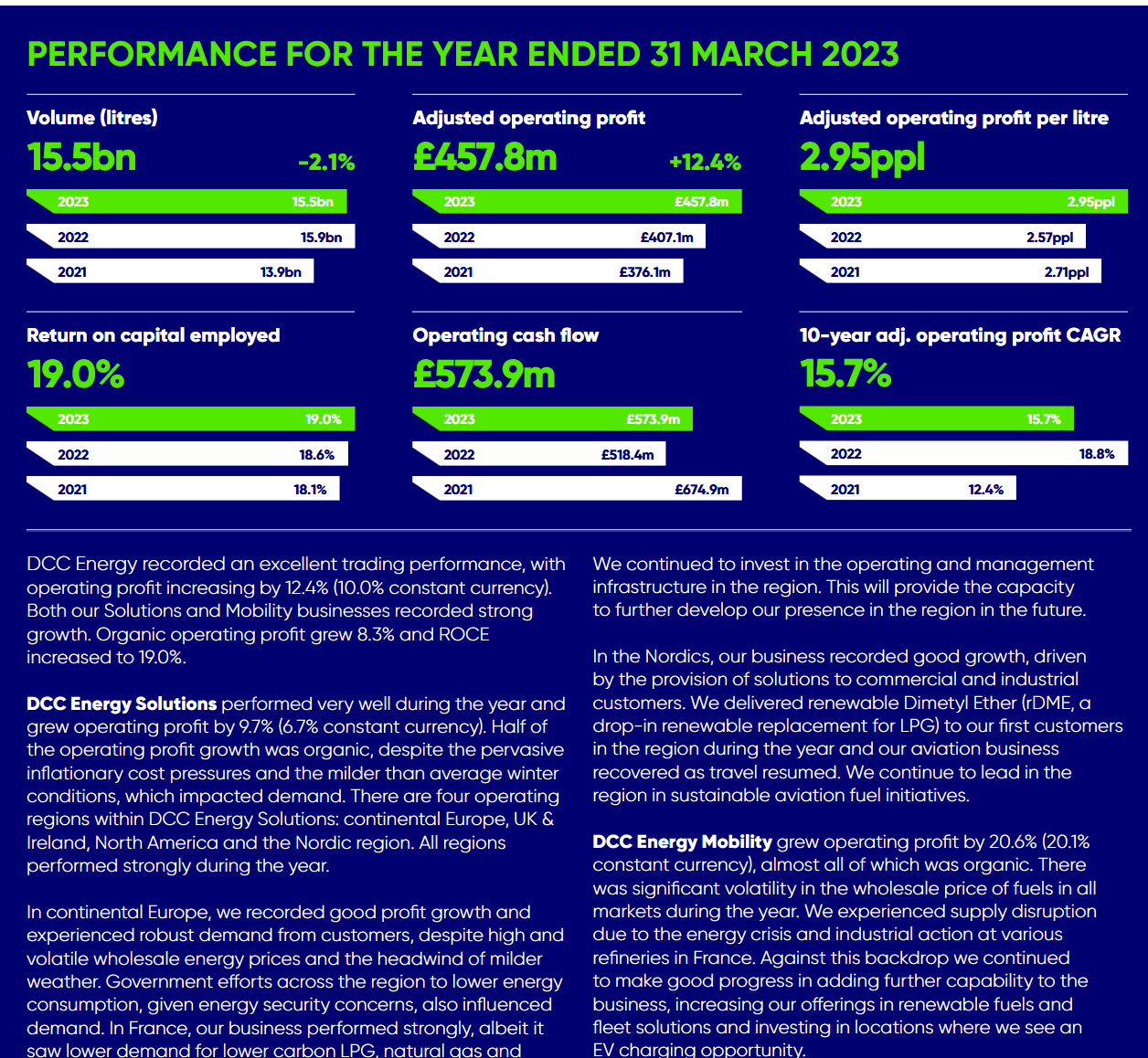

For one, DCC should expect some positive operational tailwinds. Volatile and high energy prices in the past have been good for DCC’s energy business. As we can see every day “at the pump”, distributors like normal Petrol stations immediately increase prices although they often have inventories for some weeks/months and often drop prices much slower.

Looking back to the last energy price shock in 2022, we can see that this was DCC’s best year, especially for the energy business:

Although there is no guarantee that the same will apply to 2026, there is a high likelihood that 2026 will look good for DCC from an operational perspective.

In addition, I do expect that the transformation will be more or less completed in the 2026 calendar year.

So all in all, 2026 seems to look pretty good for DCC. I think this also explains the timing of KKR and ECP, as they don’t want to wait until this improvement shows in the results of DCC.

Even in case, DCC gets sold relatively quickly at 58 GBP per share, one would still get the Dividend that will be recorded end of may.

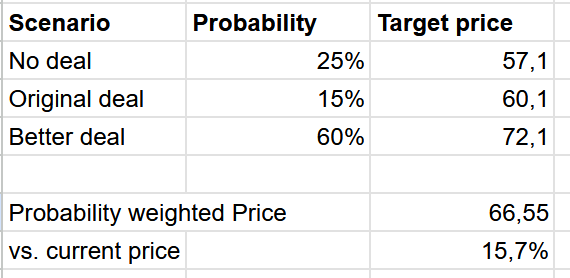

Quick handicapping exercise:

Overall, I would see the probabilities as follows until the end of the year::

25% probability of no deal with 55 GBP as the outcome (plus dividend, currently estimated at 2,10 GBP/share)

15% of a deal at 58 GBP (plus dividend)

60% probability of a better deal. My guess here would be 70 GBP plus Dividend

This is the quick and dirty calculation:

So based on my assumptions, my probability weighted expected return is around 16% until year end. This looks attractive to me, as in my opinion, the downside is very limited.

Of course, all the assumptions can be challenged and changed.

Summary:

So in total I see the following situation here:

- The bid of 58 GBP is clearly too low

- DCC’s short term operational results are supported by increasing energy prices

- in addition, the full effect of the transformation “back to energy” will materialize in the following quarter

- Other Infrastructure funds might also be interested in DCC

So even if the bid from KKR would not be successful, I do think that the share price has much more upside than downside potential at the moment.

From that perspective, I decided not to sell any DCC shares but rather increase my position by ~1,5 % of total portfolio value at around 57,50 GBP per share.