All Swiss Shares Part 8 – Nr. 71-80

And another 10 randomly selected Swiss stocks. Again, I found a couple of high quality businesses that are unfortunately very expensive. However, I did find one candidate to “watch” and actually bought one 1% position in one stock that I liked.

71. Klingelnberg AG

Klingelnberg is a 180 mn CHF market cap company that manufactures machinery for the Automobile and Mining industry. The company was IPOed in 2018 at CHF 53/share. As the chart shows, the IPO was not a big success ,losing more than -50%.

Looking back they optimally timed the IPO as fundamentally things went south from then. Sales almost halved from the 2018/2019 FY and results went from +10% EBIT margin to deep losses.

So overall this looks like a very cyclical play and I am not sure that this is an area where I am mentally equipped to invest. “Pass”.

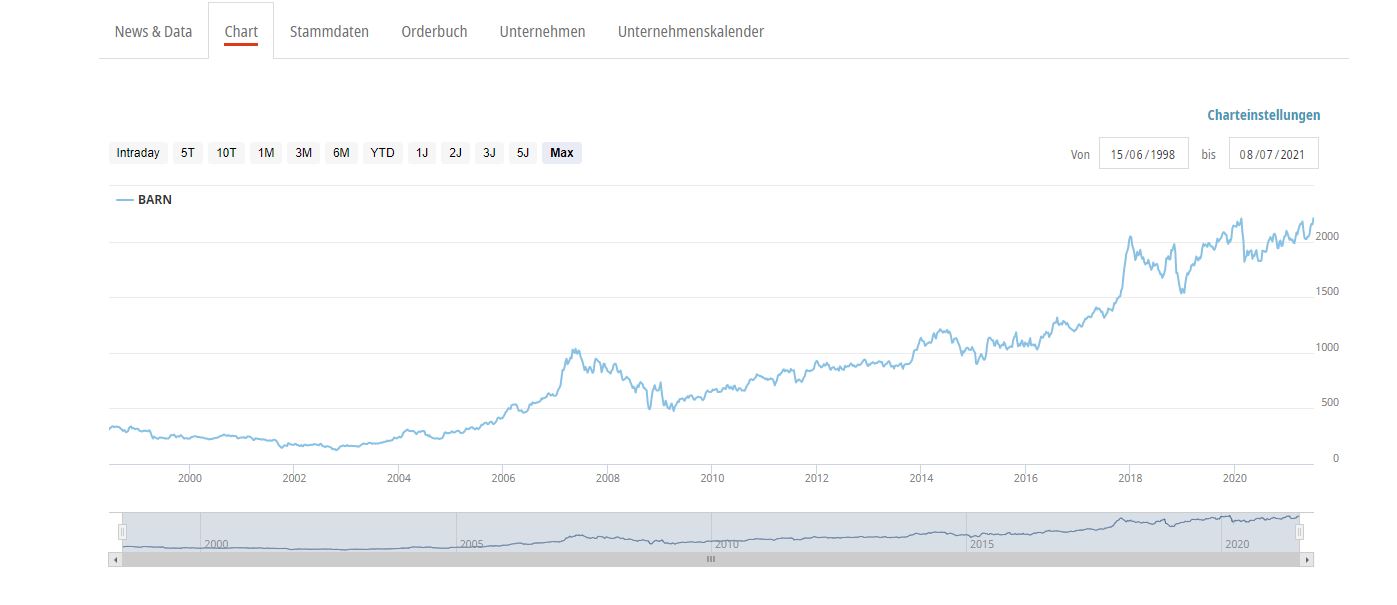

72. Barry Callebaut

Barry Callebaut is a 12,1 bn CHF market cap global leader in cocoa and chocolate trading and manufacturing. The business at a first glance looks decent (9% EBIT margins, 15% ROIC). The share price has been performing well for some time now in a very steady fashion:

With a P/E of 27, the stock is “relatively cheap” for a Swiss stock. However I am somehow not really convinced that the current stock price offers a compelling entry. In addition, Callebaut employs quite some debt and reduces the net debt number quite creatively by subtracting Cocoa inventory. Therefore I’ll “pass”.

73. Banque Cantonale Geneve

Another of the “Kantonalbanken”, this time from the Kanton Genf. The bank has a market cap of around 1,2 bn CHFs. The stock looks relatively cheap (PE of 11,5), but results have been stagnating over the last 5 years. As the balance sheet has expanded, profitability has declined. Nothing to see here, “Pass”.

74. PSP Swiss Property

PSP is a 5,6 bn CHF market cap property company. They own Commercial property in Switzerland. The stock seems to trade around NAV. “pass”.

75. Mikron Holding

Mikron is a 110 mn CHF market cap company that manufactures machinery and automation equipement for the Automobile, Pharma and Watch industry.

Not surprisingly, business has been on the decline already in 2019 bevor Covid-19 hit. In 2020, they had to take a 22mn CHF loss. The stock is trading below book value, The company has net cash, so the downside risks is to a certain amount limited.

The stock has been recovering a little bit from the low last year but theoretically there could be still some upside:

However, timing such cyclical stocks is not really my strength, therefore I’ll “pass”.

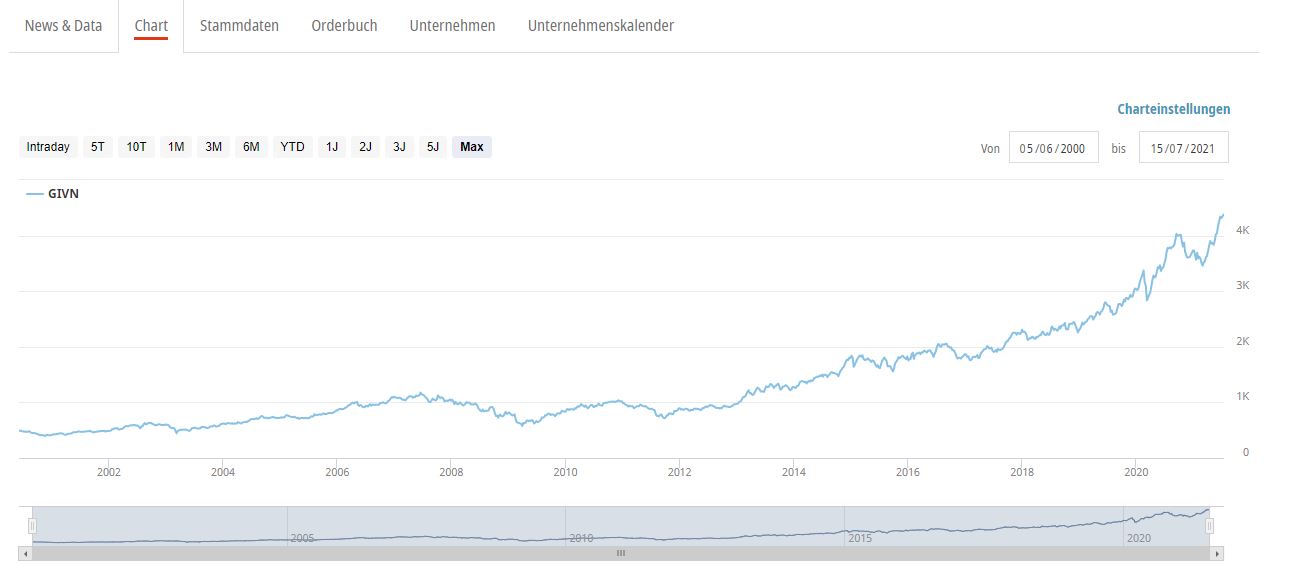

76. Givaudan

Givaudan is a 40.3 bn large cap global leader in the areas of fragrances and (artificial) flavours. The company and the business are clearly in the “High quality” area, with nice margins (22% EBITDA, 12% NI margins) and steady single digit growth even in 2020. Clearly this has not gone unnoticed by the stock market:

With a 2020 PE of 57 and P/S of around 7x the company is clearly outside my comfort zone with regard to valuation. Therefore “Pass”. I had a brief look at Symrise, the German competitor back in January 2020 which I found too expensive at a P/E of 40. Now Symrise is trading at a P/E of 54….

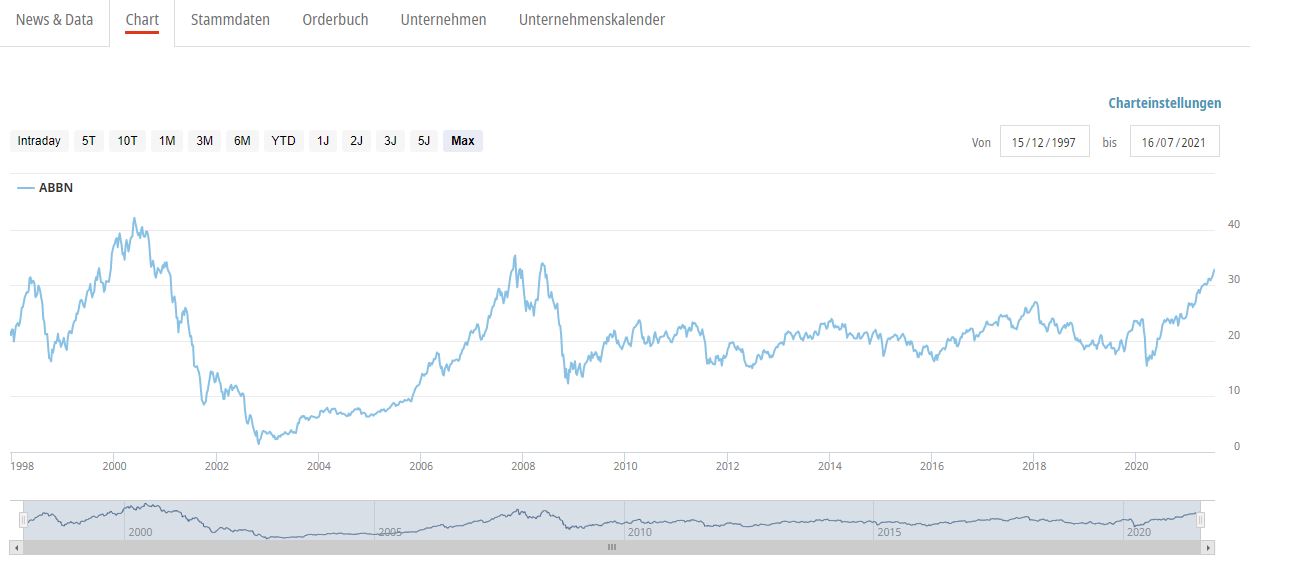

77. ABB AG

ABB is a 67 bn CHF market cap Swiss/Swedish global industrial conglomerate who is active in “Electrification, Robotics and Automation” according to its website.

Looking at the share price, one can see that the share did very little over the last 10-12 years before starting to climb towards historical levels over the past few months.

My assumption is that ABB is, especially for large cap investors an “electrification play”, as around 50% of sales and profits come from that sector. Interestingly, they sold their bread and butter transformator business to Hitachi which has been doing equally good in terms of stock market performance.

2020 was not an easy year, on an operational they earned ~1 USD per share. In their Q1 report they were quite optimistic on the next 2 years. I assume that for 2021, the share trades at around 25-30 earnings.

A few days ago, ABB issued very strong 6M numbers. Interestingly, ABB seems to intend to IPO or spin-off its Electro-mobility division, which is very interesting as they seem to do very well in providing essential equipment for EV charging.

Overall, I find ABB so interesting, that I’ll buy a 1% position for my “electrification” basket at around 33,50 CHF/Share..

78. Zuger Kantonalbank

Zuger is one of several regional banks with a market cap of 2 bn CHF. The chart shows a slow and steady increase over the last 20 years or so:

The stock trades at around 30x PE and the main attraction seems to be the ~3,5% dividend yield. However nothing to see for me, therefore “pass”.

The stock trades at around 30x PE and the main attraction seems to be the ~3,5% dividend yield. However nothing to see for me, therefore “pass”.

79. SGS AG

SGS is a 21,9 bn CHF market cap company that claims to be the leader in worldwide testing, inspection and certification. Even in a difficult year like 2020, SGS made around 16% in operating (EBIT adj) margins, 9& net income margin and 16,5% ROIC.

The share price is on a steady march upwards for many years, having increased by ~15x over the last 20 years although since 2013 the share price had been stagnating a little bit:

Free cash flow generation seems to be strong. The headline P/E of 46 seems to be quite high, However based on 2019, this would go down to 34x.

Free cash flow generation seems to be strong. The headline P/E of 46 seems to be quite high, However based on 2019, this would go down to 34x.

The business seems to be a very decent one, among others they seem to run on slightly negative working capital. The company targets double digit operating profit growth until 2023.

Overall, the stock seems to be fully valued, but I will still put it on “watch” if there will be some weakness in the stock markets in the coming months.

80. The Native SA

The Native is a 9 mn CHF nano cap that seems to have re-branded themselves as “The Youngtimers”. interestingly the company is listed since 2001 but never seems to have any revenues. “Pass”.

Added to ABB, +1% of portfolio value at 33,75 CHF. Reason: More clarity on EV Charging Listing and profit targets.

Pingback: Todas las acciones suizas Parte 8 – Nr. 71-80 - Last News

Dear Memyselfandi007

Thank you for your interesting articles, I love to read them.

I think the company ams ag (Now ams-Osram), would be also an interesting swiss stock to look at, strong Cashflows and good future opinions. The company is headquartered in Austria and produces semiconductors/sensors, but is traded Switzerland. I am wondering, if you know the company, what your opinion is on ams ag? 🙂

Hi, i have never looked deep into them. The Osram take over was super aggressive. Not really my kind of company/stock.

Everything in CH is crazy expensive. Why shouldn’t swiss stocks be ? x-D

But many things in CH are very high quality 😉

For example?

Chocolate, railway system, cheese, Fondue, tax advice, particle accelerators, tunnels, roads ….

Everything out there seems quite expensive lately (: