All German shares Part 12 (Nr. 201-225)

The next 25 randomly selected company in my “Grand Tour Germany” project with 6 of them going onto my watch list. Enjoy !!

201. TTL Beteiligungs- und Grundbesitz AG

A 67 mn EUR market cap company that started as tech company in the dot.com boom, went bust and then reemerged as real estate company a few years ago. The company invests into real estate and real estate companies. As mentioned several times, not an area that I am much interested in. “Pass”.

202. FinLab AG

Finlab AG is a 78 mn EUR market cap “Fintech investor”. The company invests in Fintech company and owns among others a 45% stake in listed Heliad Equity Partners KgAA. Although this is an interesting area and they have some interesting assets (Deposit solutions), the companies’ reporting is not very transparent. For instance their claim that Deposit Solutions has reached Unicorn status is highly debated within start-up circles.

Nevertheless a candidate to “watch” but mainly out of curiosity.

203. Allgeier AG

Allgeier AG is a 310 mn market cap IT consulting company. Currently the company shows good growth but EBIT margins are at around 4-5%. Interestingly, Allgeier seems to separate /spin-off its software business in 2020.

The company however created significant value over the last years although the stock price was extremely volatile in 2019:

A stock to watch, especially regarding the upcoming spin-off.

204. LEG Immobilien AG

LEG is a 6.9 bn EUR residential property company focusing on objects in NRW. The company trades at the calculated NAV which is around 1.5 bn higher than stated equity, earnings are mostly driven by revaluations. Not my area of interst. “pass”.

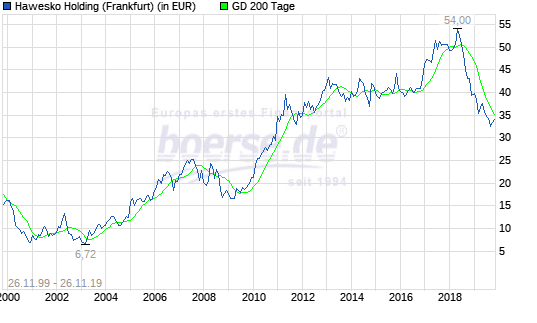

205. Hawesko AG

Hawesko is a 306 ,m EUR market cap wine retailing company, kind of the “Majestic Wine” of Germany. Fortunately, Germany is not leaving the EU, so HAwesko is still doing relatively well with nice top line growth. Bottom line however, things look not so great. A newly acquired subsidiary and a new logistics centre have negatively impacted the 2019 Q3 results.

Despite the recent drop in the shareprice, the stock is not cheap:

Nevrtheless it is a “watch” list stock for me as long as I own Naked Wines.

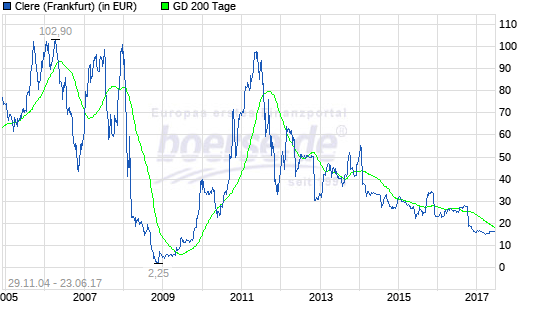

206. Clere AG (ex Balda)

Clere AG, the 67 mn EUR market cap has an interesting history. Initially named Balda AG, the company was on a wild ride especially in the years 2007-2009:

From superstar stock as supplier of Apple Iphone displays to almost bankrupt back to superstar. At some point in time however it became clear that the main shareholders didn’t really want to share the remaining assets with minorities and the company officially delisted in a strange transaction in 2017, taking advantage of Germany’s week protection against delistings. The stock is now only listed OTC in Hamburg and doesn’t publish reports anymore. “Pass”

207. Halloren Schokoladenfabrik AG

Halloren is as the name says, a 20 mn EUR market cap chocolate producer. Similar to Clere AG, the company took advantage of the lax delisting rules in Germany and delisted in 2016. The company still issues an annual report but for me the stock is a clear “pass” due to Governance issues.

208. RIB Software AG

RIB Software is a 1.24 bn EUR market cap Software company. According to its 9 month report, business is going well. 9 months sales increased by +59% (!!). Profit margin has been decreasing but a 15,6% pre tax margin still looks Ok. Part of that growth seems to come from acquisitions but somewhere they mention that organic growth has been around 25%

RIB specializes on Software around the construction sector, from architects to construction companies.

With an annualized run rate of ~50 mn EBITDA and net cash, RIB’s valuation (~20x EV/EBITDA) seems neither cheap nor expensive considering the growth rate.

On the other hand, the company does really strange capital increases and the ratio of shares sold short compared to free float is quite high. It is also interesting, that Ennismore, the guys who identified the Globo Fraud early on, have this as their largest short position. “Pass”.

209. DMG MORI AKTIENGESELLSCHAFT (ehemals Gildemeister AG)

DMG Mori is a 3.3 bn specialty machinery manufacturer that used to be named Gildemeister AG but is majority owned by Japanese DMG Mori Seiki since 2015.

Interestingly, DMG Mori as 52% shareholder is only valued at 2 bn EUR market cap. The company is doing relatively well although growth rates are decreasing, hwoever I do think that with 200 mn planned BEIT, the valuation of 16xEBIT is quite high for such a cyclical business. “pass”

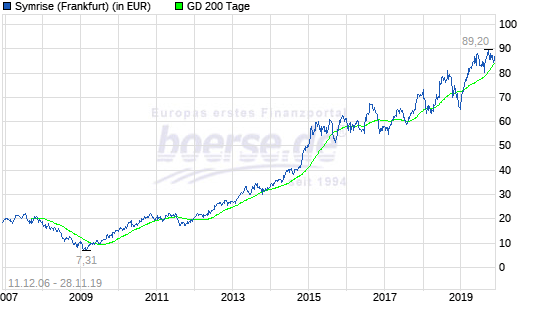

210. Symrise AG

Symrise is a 12.9 bn specialty chemical company with a dominating position a fragrances. Longterm shareholders have done very well as the stock chart shows:

The company is a constant grower, currently with around 5-7% p.a. organically plus M&A. With EBIT margins of 14%, the business seems to be very attractive, however a P/E of >40 shows that this is clearly not a secret. Nevertheless a clear candiddate for my (long term) watch list.

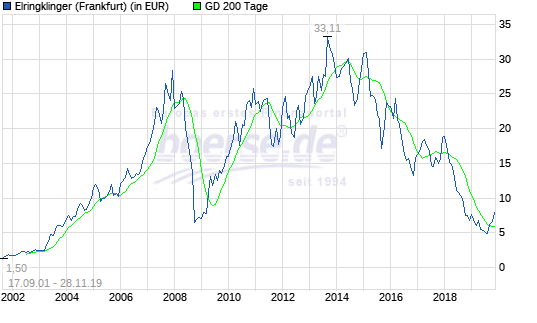

211. ElringKlinger AG

ElringKlinger is a 500 mn market cap supplier for the automobile industry. From the whole sector, ElringKlinger is maybe the most dependent company on combustion engines. The company is the most important cylinder head gasket globally, with a market share of 80%. However, electric vehicles have no need for these parts. As Elringlingers revenue still depend mostly on these products it is no wonder that the share price has tanked to a 15 year low after a long climb:

The company itself is clearly trying to establish new product lines in order to lower the dependency on combustion engines as the last investor presentation shows. One of the issues however is the large amount of debt (~900 mn gross) that the company has accumulated. Nvertheless, Elring Klinger for me is an interesting candidate to “watch”.

212. Vita34 AG

Vita34 is a 55 mn EUR market cap company that stores umbilical cord blood of neborn babies. The stemm cells in the blood are supposed to enable therapies that will help better against illnesses, although to my knowledge, currently not many therapies exist. The business model in principal would be interesting (storing is nice recurring business) but organic growth is low and bottom line profitability is weak. “pass”.

213. Fuchs Petrolub SE

Fuchs, the 5.5 bn lubrication oil specialist, is clearly one of the biggest success stories within the German small cap universe over the last 2 decades or so.

The chart doesn’t really show it but Fuchs increased around 50x over the last 20 years or so (I owned the stock several times in the past but always sold quickly after some minor gains….):

Since the peak in 2018 at around 50 EUR/share the stock is however struggling. In 2019, slaes are stagnating and profit is down -17% yoy. Although EBIT margins are still decent (~12,6%), the current P/E of >25 looks rich. Nevertheless clearly a quality company to “watch”.

214. Axel Springer SE

Axel Springer, a 6.9 bn media company is most famous through its Tabloid “Bild” which still dominates the German daily press. Although Spinger started early with Digital offers, the company is struggling. For the first 9 months, sales were more or less unchanged, but EBITDA dropped by -19%. EBIT dropped even more by -29%.

However Springer surprised the market this year by teaming up with PE shop KKR. KKR made a voluntary offer to the minority shareholders and ended up with around 28% of the shares. In part this was a defensive move as some of the Springer family seemed to have willing to sell anyway and the major shareholders seem to think that partnering with KKR is the lesser evil.

It wil lbe interesting to see how and if the decline in print media can be compensated by online offers, but in my opinion Springer doesn’t have many top online assets. For me Springer at the moment is a “pass”.

215. The Naga Group

28 mn EUR market cap “Crypto Shit show” that I wrote about 2 years ago. The only surprise here is, that the market cap is still >0. “Pass”.

216. Vereinigte Filzfabriken AG

19 mn market cap felt manufacturer. Stock trades rarely and business is struggling operationally. “Pass”.

217. Allianz SE

91 bn EUR market cap insurance giant. For me too complex to analyze, therefore “pass”.

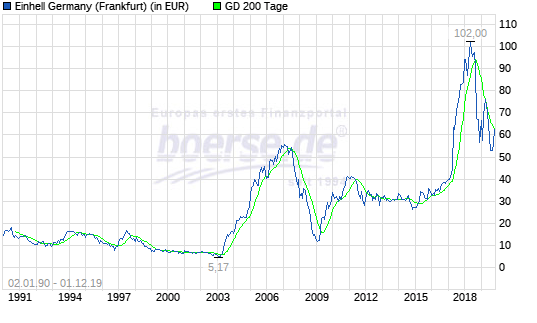

218. Einhell AG

235 mn EUR market cap company that specializes in importing and distributing mostly DIY tools and materials. Its products are offered mostly in the lower price range. I have looked at and owned Einhell several times in the past as it always looks cheap.

The stock chart looks pretty crazy with wild multi year swings:

In the past they always managed to have good periods and then got hammered either by internationl expansion gone wrong or trying to create a premium brand. The business model as such doesn’t look very attractive but in perfect hindsight one would say that Einhell seems to execute very well in that sector. I am not 100% sure why the stock price exploded as it did in 2018. One thing is interesting: At least in 2017 and 2018 according to the annual report, cash generation was really poor, with operating cashflow negative despite the nice increase in profits. Working capital management looks poor. FOr me still a “pass”.

219. Evotec AG

Evotex is an interesting company at least for me. Although it has a market cap of 3,2 bn EUR I never ever looked at he company. It seems to be a kinfd of R&D service provider for the pharmaceutical industry. After reading one of the latest IR presentations, I do not really understand what these guys are doing. However the company is growing quite fast (3x increase Topline from 2015-2018). With an EBIT run rate of around 50 mn and an EV of around 3.6bn, the company trades at ~70xEBIT which might be justified but I am not the one to challenge this. “too hard” and “pass”.

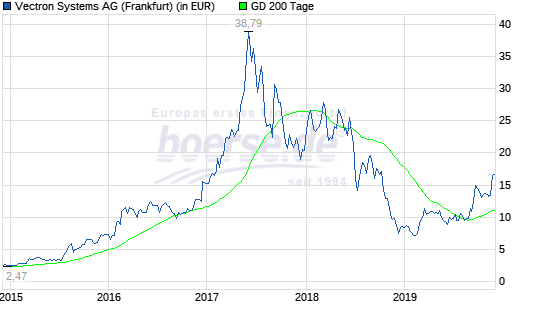

220. Vectron Systems AG

Vectron is a 125 mn EUR specialist in Point of Sale (POS) and cash register solutions. Fundamentally, the first 6M 2019 didn’t go well with lower sales and a higher loss plus a capital increase in Q1 2019. However the stock price increased signficantly over the last few months:

The upside case seems to be a change in regualtion for businesses from Jan. 1st 2020 that might trigger a huge wave of orders for them. Too speculative for me, “pass”.

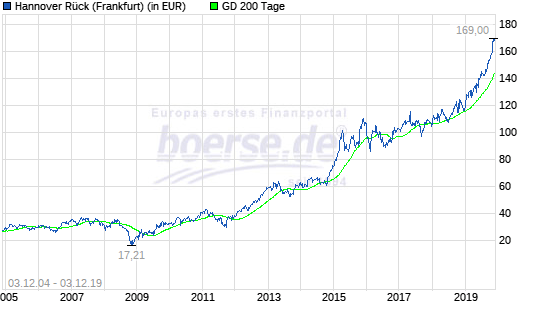

221. Hannover Rück

Hannover Rück is the no. 4 Reinsurar globally. For some strange reason I never looked at the company. The 20 bn market cap company has shown an incredible run and is clearly one of the best performing insurance stocks globally:

In the past I had avoidded the company because the overall structure is to put it mildly, complex. Hannover is part of the HDI group and its sister company Talanx is also listed. It is pretty hard to understand how the overall group looks like which is key for assesing any financial company. Nevertheless, the company is a clear “watch” candidate.

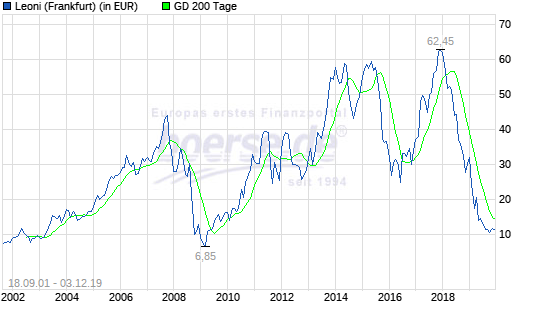

222. Leoni AG

Leoni AG is a 374 mn EUR market cap automobile supplier who clearly has seen better days looking at the stock chart:

Before 2009, Leoni “conquered” the world, expanding globally together with the big German OEMs. After 2009, the company recovered quickly before then in 2018 hitting the “brick wall”. Some early signs were visible: The fact that a Romanian subsidiary was able to transfer 40 mn EUR onto a fraudulent account in 2016 was clearly a warning sign that somehow controls within Leoni were not so great.

Looking at the most recent investor presentation provides a pretty depressing picture: Financial debt goes up, cash and still open credit lines go down, losses increase and sales tumble. The company looks very vulnerable to any economic shock, however the stock also looks cheap. The company plans additionally a spin-off/carve out of its cable business, now for 2020. For my taste that is maybe not the smartest idea as their resources might be needed elsewher. Nevertheless for me it is a “pass”.

223. Trade & Value AG

0.9 mn market cap Nano cap. Pass.

224. Ymos AG

Insolvent company with 6,5 mn EUR market cap. “pass”.

225. Pearl Gold AG

Super strange company that claimed to have a 25% interest in a gold mine in Africa. Bankruptcy in 2016, CEO seems to be a fraudster. For some reason 6 mn EUR market cap. “pass”.

Vita 34 is actually a really quite interesting case at the moment in my opinion.

Active Ownership Capital is trying to consolidate the market by merging “Vita 34” with the larger polish blood bank “Polski Bank Komórek Macierzystych” – this would form an undisputed European champion.

Due to the historically low presences at the General Meetings, they should be close already – as they had convinced the biggest shareholders to sell their stake in Vita 34 and receive stock in the new HoldCo instead. This triggered a mandatory takeover offer, which AOC lowballed by offering the legal minimum which is well below the pre-Covid stock price.(It’s here, I quite like the official name: https://vampire-offer.com/ )

Let’s wait and see what happens, I like the business modell (recurring revenues, cash-strong and high barriers to entry), I can imagine some merger-synergies for marketing, storage and regulative costs and as research progresses, this could potentially be a home-run. Especially if somebody decides to buy some more stock to block/secure the merger, it’s now IMHO more attractive to be in the Vita 34 stock than PBKM, but what do I know. This might to worth to look into a little more.

Yes, an interesting case. As you will see now, I am already indirectly invested 😉

EVOTEC ag On is a fairly big German Biotech (service oriented with 3000 employees)which partners among others with French Giant Pharmaceutical company Sanofi.

Actually Sanofi has transfered all its anti infection Research & Development to Evotec in order to combat infectious diseases..

Evotec also partners with Bayer in discovery,pre-clinical and clinical development.

Schneider Electric wants to take over RIB Software for 29 €. Crazy days…

Wacker Neuson is interesting but also compelling because of profitwarning. The CEO wants to cut costs for approval. 50 million euro’s.

But last days stockprice is rising. I am not sure if this stock can go down again.

Hi, I enjoy reading your blog for many years already. Great job, and keep it going! I have been looking at Wacker Neuson SE last few days. Share price has come down significantly. I really like that it is a family owned business, that usually helps with long term perspective. Also, revenue growth seems encouraging and the size of the company is rather modest, so still room to grow. I came to your blog to find if you had already done an analysis, I don’t think so. If you have an opportunity, would please take a look at it?

I’ll have a look once the random number generator selects the stock.