DCC Plc (ISIN IE0002424939) – Extremely unsexy Business meets sexy Track Record at a super sexy Valuation

Disclaimer: This is not investment advice. PLEASE DO YOUR ON RESEARCH !!

As this post has become quite long, here is the Elevator pitch:

DCC Ltd, a 4,3 bn market cap UK listed, Ireland based company at a first look like a very boring, unremarkable collection of very boring distribution businesses. A second (or third) glance however, reveals a very stable , well managed distribution company that has been compounding EPS at double digit growth rates for the last 28 years and can be bought for a very modest valuation of ~10x earnings. The company clearly faces some challenges but this might be more than outweighed by very good capital allocation, company culture and growth opportunities.

- History

DCC has a very interesting history. It was founded actually as some kind of Venture Capital company in 1976 in Ireland and was led for 32 ears by founder Jim Flavin. After turning into an operating company, DCC went public in 1994. Over the years they acquired a lot of businesses, many of those where distribution businesses from oil majors but also in other areas such as health care and technology components.

What I find extremely impressive is their track record since they listed in 1994 and is available in each annual report:

So at least for the last 28 years since listing, they have compounded at a very decent rate.

2. Business model

DCC’s main businesses are distribution businesses. In my portfolio I have a couple of distribution companies among them are Thermador, Solar and Meier Tobler. Here are a few points with regard to distribution that are maybe worth mentioning:

- Distribution is adding the most value if there are a lot of suppliers and a lot of customers

- Speed and availability are at least as important as price

- outsourcing of Working capital requirements: If a customer knows that he can get the required items quickly, there is less need to hold large volumes of inventory

- to a certain extent it is also an “infrastructure” play, as you need to build physical infrastructure such as warehouses etc.

- Returns on capital Employed are usually good but not super great as “hard assets” such as warehouses and inventory need to be financed

- Gross margins are normally quite low, but stable

- Customer relationships are quite stable if the distributor adds value for the customer. Typical Distributors do not spend that much on marketing

Business lines:

In their annual report, DCC has a great overview over their business lines:

Energy business

The energy distribution business consists of 2 business lines:

- Mobility

This is the smaller segment is here they are basically running a chain of filling stations and deliver heating oil to consumers. The mobility business is actually quite comparable with Alimentation Couche-Tard with the addition of providing heating oil to households. Usually they get paid per liter in that business and do not bear and oil price risk - Energy solutions

In this segment, they are offering LPG mostly to commercial customers. LPG is actually a quite interesting business, especially now with the lack of Natural gas. Again, to my understanding they only have volume risk but no price risk.

The LPG business is a very interesting business in my opinion. In a first attempt to use ChatGPT, this is was the AI provided on the uses of LPG gas:

LPG is normally a very stable business and right now a pretty “hot commodity” and distributing it should be a good business. For instance I found this example of large German industrial Glass producer Schott building large Propane (LPG) tanks as a fallback for Natural Gas shortages. Up to a certain extent, LPG can be used to replace Natural gas especially to generate heat.

Healthcare:

Healthcare comprises a few major businesses. DCC Vital is a classic distributor, distributing medical products to hospitals, doctors and other primary care providers. DCC Health and Beauty is rather an outsourced manufacturing business that produces pills, capsules, gels etc. in the areas of nutrition (health supplements) and beauty products for Brand companies. A few months ago they made an interesting acquisition in the Healthcare Sector with MediGlobe that seems to fit well with DCC Vital. Overall DCC Healthcare grows nicely and has above average margins and ROCE’s.

Technology

DCC Technology comprises several businesses that distribute “technological” products primarily in North Amercia. The most recent acquisition was a business called Almo which as really significant with an EV of 610 mn and EBIT of 70 mn. Almo seems to distribute kitchen appliances, consumer electronics. audio equipment from manufacturers such as Samsung, Jabra, Electrolux or Liebherr via a number of distribution centers in the US. So far, margins and ROCE in that segment was below average but the Almo acquisition could change this. And the CEO of Almo has an interesting first name: Warren. Of the three segment, this is the one where I maybe understand the least what are the main drivers.

One interesting aspect: I would have thought that they have a much higher UK share but it is “only” 24% of profits.

Why is the stock cheap ?

Looking at the share price, we can see that the stock almost “exploded” between 2013 and 2017 and since then has been more or less trading sideways and then downwards. At the time of writing, the stock actually trades at 7 year lows:

As we can see below, this is mostly driven by a very severe contraction in multiples as we can see in this chart:

In 2016 and 2017, investors thought that a fair forward P/E was considered to be 25x, at the moment, the consensus is only 9-10x. Despite Covid etc. GAAP EPS will increase from 2,69 in 2016/2017 to an expected 3,73 GBP for the current year. Maybe 25x was too rich, but 10x looks cheap for a company that is able to grow earnings so consistently.

Interestingly, the peak in multiple and share price correlates with the last change in the CEO role in 2017. Part of the meteoric rise of the valuation multiple could maybe explained by the relisting of DCC from the thinly traded Irish stock Exchange to London in 2014 and joining the FTSE 100 in 2015.

The oil and gas business is the old core business of DCC and could be also part of the current problem: With the advance of Electric vehicles and the Energy transition, one can clearly argue that this business can only shrink over the next 10-20 years. In addition, “ESG” oriented investors might not want to put DCC into their portfolio.

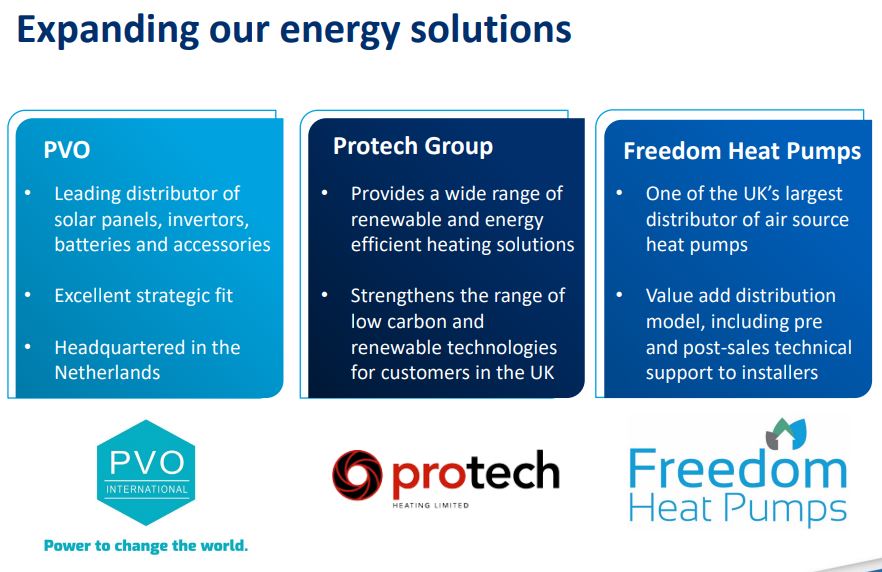

However what I find really interesting is that DCC has already reacted and formulated a new strategy for the energy division in May 2022. In a nutshell, what DDC tries to achieve is that they want to help their customers to transition to an energy mix with a much lower Carbon impact.

How do the want to do this ? Simply by offering their customers lower carbon alternatives such as biofuels, heat pumps etc. Already in November last year, they showed in an interesting Presentation how this works in practice: Offering solar rooftop installation in France, Sustainable Aviation Fuel in Denmark and EV charging posts for their gas station network. They also acquired a few companies in order to expand their offerings to customers:

My assessment is that there is clearly a risk but also a significant opportunity in the energy business of DCC. In order to reflect the risk, a slightly higher return should be required.

One more aspect to mention is that currently cash conversion of DCC’s business is significantly below the historical mean of close to 100%, mainly due to inflationary pressure. As a distributor, DCC is, like it’s peer hit by inflation directly as more expensive products mean higher working capital needs. If you need to have 100 items of item x available and the price increases 30%, this translates very quickly into a 30% higher working capital requirement.

On the other hand, their value proposition of outsourcing working capital gets even more attractive, so pricing power is actually there which should allow better cash conversion going forward.

Overall, I do think that there are clearly some factors that can explain the current low valuation, but I think that this does not justify it, which for me is the typical definition of an investment opportunity.

Management Incentives

As DCC is a company that is not Founder/family owned/run, a closer look at the incentives is important in order to understand potential conflicts in alignment.

The CEO Donal Murphy has been with DCC since 1998 and is CEO since 2017. He earns a “decent” salary of around 3,5 mn GBP, but also owns shares in a value of ~12x his salary. Kevin Lucey, the CFO only owns 2x his salary in shares but has been appointed only in 2020. There are requirements for the top level management to hold shares as a multiple of their salary. In addition there is a performance related bonus plan as well as a long term incentive plan:

Bonuses

The executive Directors will continue to participate in the bonus plan for the year ending 31 March 2023, consistent with the Remuneration Policy, with bonuses based 70% on growth in Group adjusted EPS and 30% on strategic objectives; the maximum award opportunity for the year will be 200% of salary for the CEO (the maximum opportunity

LTIP

The executive Directors will be granted LTIP awards in the year ending 31 March 2023 consistent with the Remuneration Policy. The performance conditions will continue to be based on ROCE, EPS and TSR performance over three years. The grant value will be consistent with that in the year ended 31 March 2022 at up to 200% of salary for the CEO and CFO.

Overall I think the incentive scheme is above average with very reasonable KPIs (EPS, growth, ROCE, share performance) that should align shareholders and management reasonably well. What I also like that they are very transparent in their reporting. a very simple overview like this chart from the previous annual report should be in any report but unfortunately isn’t.

The only negative aspect that I found is that for the 2019 LTIP, the retroactively adjusted one of the criteria leading to a higher award, both, for the CEO and CFO. Initially, UK inflation was the benchmark for EPS growth and they would have missed this with the skyrocketing 2022 inflation numbers. So they retroactively changed it to the more recent LTIP schemes which defines a corridor of 3-9% EPS growth. Not great but Ok if they don’t repeat this.

Capital allocation & Corporate culture

In a diverse business like DCC’s capital allocation is very important. From what I have seen so far, what they do seems to be very disciplined. They allocate based on their cost of capital across their 3 platforms. They have done a few larger acquisitions over the last 12 months and it needs to be seen how they develop, but for instance they are always releasing decent information about each acquisition including purchase price and EBIT on top of the strategic rational. The large US acquisition for instance looks very attractive at an EV/EBIT of 7 and management staying on board. So far they also did’t have to make large write-offs on any acquisition.

At the moment, “Serial acquirers” are not that popular anymore but I think that they are a very decent “serial acquirer”.

With regard to culture, from what one can see from the outside, the organization looks like an entrepreneurial, decentralized model which is maybe the only way to run such a business. Glassdoor reviews are surprisingly good for such an unsexy business.

Overall I would rate both, capital allocation and corporate culture as very high.

Valuation:

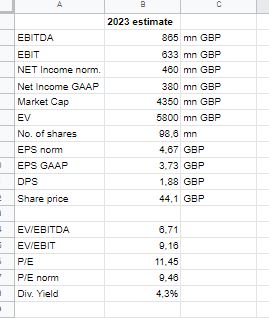

For the current business year, estimates are as follows (Source: TIKR):

One aspect worth mentioning here is that DCC shows both, GAAP earnings and “normalized” earnings. They do this quite transparent:

The “exceptionals” mostly comprises M&A related expenses, such as earn outs and m&A costs. Here I would hesitate to normalize as M&A is aprt of DCC’s business models.

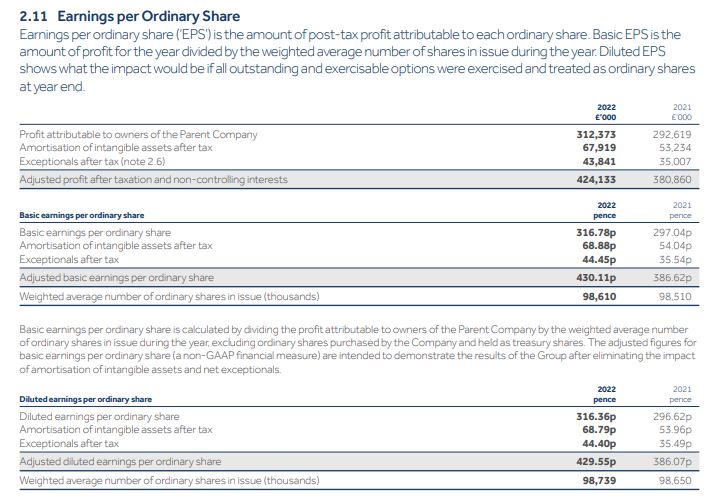

However the amortization of Intangibles is something that I would indeed neutralize as this is at the end of the day a pure accounting entry. So for me the “Correct” level of earnings would be 385 pence for 2021/2022 but not the 429 pence.

For the first 6 months of the year, EPS growth has been around +9%, so assuming “my adjusted” EPS for the current years of 400-420 Pence would be realistic which in turn gives us a very modest P/E of around 10.

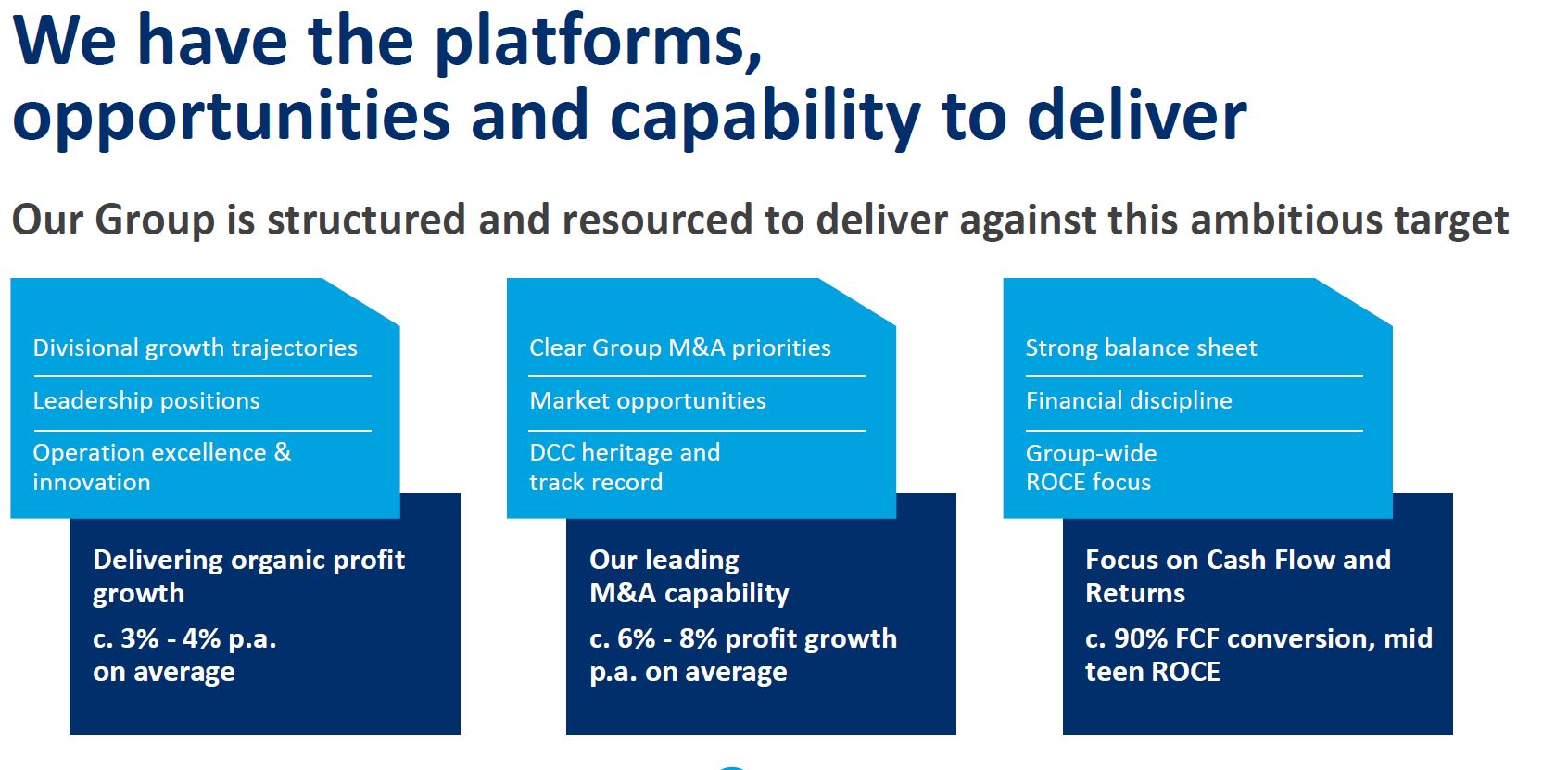

In order to value the share, we need to make an assumption of the future growth rate. Historically, DCC managed to grow by ~12% for the last 28 years. Going forward, Management targets double digit rates as can be seen in this graph with 3-4% coming from organic growth and the rest from M&A:

Interestingly, as mentioned before, the bonus plans of DCC’s management target a EPS growth rate of 3-9%, meaning that the maximum bonus is reached at 9% EPS growth which would be at the lower end of the stated targets above. Therefore I think that a growth rate of something between 7-9% is maybe more realistic in the mid- to long run.

At the current estimated dividend yield of ~4,5%, this would mean an expected return of of between 11,5% to 13,5% in the long term, assuming no change in valuation multiple which I would find extremely attractive.

My price target for a 3-5 year holding period would be between ~58 GBP (3 years 7% growth, constant exit multiple, including dividends) and 95 GBP per share (5 years, 9% growth, 13x Exit P/E).

Other investors

The investor base is almost exclusively made up of large institutional investors (Blackrock, Invesco, Vanguard etc.) which is one of the main weaknesses. So far Governance seems to be OK, but having at least some “strong hands” would be preferable. On the other hand, this would also be an invitation for a Private Equity take over bid. Which to a certain extent is a risk because this could cap the upside for investors if they would come in at the current price level with the usual premium of 30-40%.

Pro’s and Con’s

As always, before coming to a conclusion, lets look at a list of Pro’s and COn’s for DCC as a potential investment:

Pros

+ great 28 track record

+ Useful metrics (ROCE) for management incentives

+ very good reporting

+ interesting company culture with decentralized decision making

+ very reasonable valuation

+ decent growth opportunities

+ low beta, historically stable business model

Neutral

+/- growth driven by m&A

+/- OK returns on capital/ low “headline” margins

+/- not an obvious “ESG friendly” business model

+/- very diverse businesses

Cons

- slightly elevated leverage at the start of a potential recession

- Working capital increase due to inflation

- Relatively large amount of goodwill/Intangibles due to acquisitions

- Retail Energy business needs to transform

- no family/Founder/large shareholder

- ugly share price development over the past 7 years

Summary:

I have been looking at DCC several times within the past few years. I have been introduced to the company by my friend Mathias a few years ago, he has a nice summary in his 6M 2020 report (German).

DCC ticks many of the boxes that I am looking for: An unsexy business model that is very well executed, a company with a great culture and at a very decent valuation with decent growth outlook and a great track record. There are clearly challenges and of course I would prefer a higher ownership from Management, but overall I find the risk/return profile extremely attractive.

Timing wise, it might be a little bit too early as the stock chart doesn’t look good (7 year low as mentioned) but as a rule I tend to ignore this. What I find very attractive here is that DCC is not a Contrarian stock but rather a neglected one.

Therefor I allocated ~5% of the portfolio to DCC at a price of around 43 GBP per share. I financed this mostly by selling the remaining 3U position and selling a little TFF.

Disclaimer: This is not investment advice. PLEASE DO YOUR ON RESEARCH !!

Thank you for this write-up.

Something I find ambiguous about their strategy is that they kept increasing their retail petrol businesses (basically making a contrarian bet vs the ESG trend) while simultaneously making small acquisitions in the alternative energy sector.

While calculating their free cash flow, would you exclude the repayment of lease creditors?

Thank you

think mgmt faces a dilemma regarding future capital allocation.

the returns they can make investing in LPG in the US are very attractive. There is plenty of white space in rural US midwest, which will likely be buying propane for decades to come. however their ESG investor base does not want them to pursue this

on the other hand they have more „sexy“ sounding plans to invest in solar, EV charging stations etc. returns here seem very poor, markets are crowded, and DCC has no edge/competitive advantage.

if you owned 100% of this business privately, you would go all in on US LPG and capture the 20% ROCEs. But as a public company they have to be wary of their PE multiple, and therefore pay lip-service to the ESG stuff. This company should be taken private asap.

I hope they only get taken private agter the share price has recovered (a lot). Personally I think investing into solar/ heat pump/ev distribution could be very interesting.

you can see it from a top down level (incremental returns on invested capital have been declining), bottom up level (they implied at the last results that their largest recent deal Almo was underperforming expectations). and it makes sense from first principles – lots of dumb money flooding into the renewables space and DCC have no unique competency which would justify an unusual return vs competitors. lots of renewables investors do not have high hurdle rates and have billions of PE capital to deploy

i think stock will struggle to return to the old days from multiple perspective unless they abandon LPG. and they will struggle to compound at the returns required to justify a high multiple unless the increase LPG. so they are caught between two opposing forces which can only be resolved by going private

With regard to core competency in energy i would disagree. DCC has a large customer base who depend on DCC to provide them with energy. Dcc knows their needs and can help them to decarbonize by distributing alternatives. To me this sounds like a very logical way to develop the business and this is part of my investment case. But of course one can interpret this differently. We will see.

dividend CAGR of 13.7% over 28 years is flattered by increased payout ratio. adjusted operating profit cagr of 14.1% does not adjust for dilution, does it? I don’t like this promotional reporting by management.

LPG for heating with low end temperatures (e.g. heating buldings) makes only sense vs heat pumps, if you have no connection to the power grid. Of course there are industrial use cases nevertheless. I cannot answer: What is the split between sustainable operating profit and dying part of business for the LPG side of the business? Could be meaningful.

Selling heatpumps is more one-off vs. supplying LPG. I don’t think heatpump/solar can compensate the loss of business.

As they are also showing EPS growth, I don’t think that their reporting is overly promotional. For me the 11,8% EPS growth is the relevant statistic.

With regard to LPG and the retail business: As I mentioned, this is clearly the big question. LPG has quite a lot of uses. E.g. heating in areas where there is no grid connection and cold weather (mountain cabins etc.).

I do think that they are able to adjust their business accordingly but it is clearly a risk.

For the next 2-3 years, I expect the LPG business to sognificantly outperform expectations.

Otherwise a company with that track record wouldn’t trade at a single digit P/E.

Nice write-up, and details on the incentives. I find the growth pre-COVID (2013-2020) quite paltry given the amounts not paid out and the share issuance, reflected in the drop in ROE (10% from 25%). Looking forward to see the development of this one though!

Indeed the growth story is not 100% perfect. Otherwise I guess they would not trade at a single digit P/E. As mentioned, I think the srtock is attractive in relation to its current price. This is not an “attractive at any price” business for sure.

So their future growth will come from m and a, because even though their current business is probably quite resilient given their track record, it’s a bit unclear to me.

They expect 3-4% organic growth and the rest via M&A. I expect slightly lower overall growth.

So their future growth would essentially come from m and a, because even though their current business may be resilient given their track record, it’s not very clear to me.

Think the valuation deserves a conglomerate discount. Never understood why their profit margins / ROC aren’t higher. Prefer the IT distributors for that reason.

I have to admit that I don’t understand the IT distributors, however, I guess that concentration on the supplier side is quite large (Microsoft, amaton etc.). The reason that margins are so “low” is that as mentioned, they just get a small amount per liter and pass through the price without any commodity price. Very similar to Alimentation Couche-Tard. Yes, it doesn’t look very attractive at first glance but it is very stable. Nothing to brag about in a cocktail party.

The company definition of ROCE (used to gauge the attractiveness of potential targets) uses as numerator Adjusted Operating Profits (which is actually EBITA) and the denominator is also adjusted to exclude some items, for example right-of-use assets / liabilities (not marginal for this business).

This is technically not “wrong”, but it overstates the real underlying returns: first of all because it’s pre-tax, and second because it excludes too many items.

As such, “real” ROIC and margins are lower than what the company reports. And incremental ROIC from acquisitions is also only 6%-7%.

https://mrmarketmiscalculates.substack.com/p/dcc-plc

Adjusting goodwill amortizations is Ok in my opinion. As I mentioned, stand-alone returns on capital are not great but they managed to grow very consistently.

That’s one big allocation!