Another potentially interesting story is Easyjet, where a US investor with the name Castlelake is trying to buy Easyjet and has increased the bid price now for a fourth time.

According to some sources, the board might be willing to sell for 7 GBP.

At the time of writing, the shares trade at 5,72 GBP, a discount of more than 18% to the potential “clearing price” of 7 GBP and 12% to the last offer from Castlelake.

This is a pretty wide spread, but maybe justified because the case as such is not super easy.

For instance, in order to maintain its EU landing rights (which are essential for Easyjet), non-EU ownership is capped at 49%. To circumvent this, Castlelake seems to have teamed up with certain European individuals to restrict their ownership as US institution, put this structure will be heavily scrutinized if it comes to a bid.

What I also find interesting is that Castlelake has no track record in Private Equity. However, since 2024, they seem to be majority owned by Brookfield. But so far they have been focusing on Asset based lending, not Private Equity.

To me it is also not 100% clear which fund is sourcing this quite substantial deal.

Finally, at Easyjet, the founder is still owning 15% and he might have a lot of influence if and how this company gets sold.

Looking at the long term chart we can also see that as many other airline stocks, it was not such a great long term investment after all:

So overall, at least for me it is really difficult to “handicap” the risk of the deal not happening. Therefore I will stay away from this one despite the rather “juicy” spread.

Nagarro

Nagarro is a company I followed loosely over the years. It is a spin-off from German IT services company Allgeier and mostly considered to be a “Indian IT Outsourcing” shop.

Initially, the company became a “spin-off superstar” and went up to almost 200 EUR per share in 2022, before trending down the last 4 years to around 33 EUR:

There wer always some questions around the company and those outsourcing business models these days seem to be vulnerable to Ai Agentic coding.

For instance, the share price already increased by +20% on Friday, so it seems that some insiders were already front running the news.

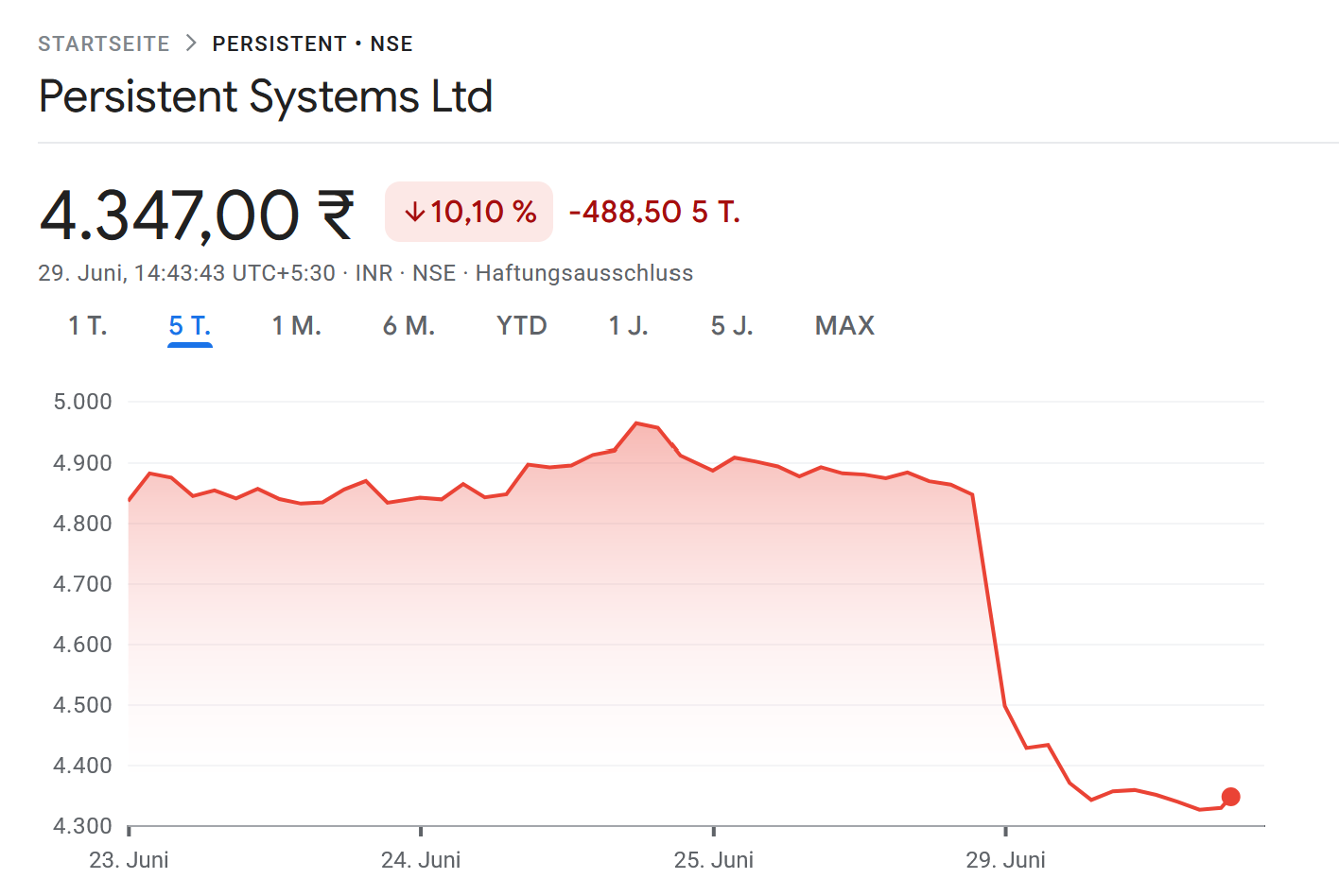

I also find it quite curious that the take over premium is so high. The bidder, Persistent Systems which is listed in India dropped by -10% today:

At the current price of 77 EUR, the discount is only 5%. There will be a dividend on July 2 nd of 1 EUR and record day is tomorrow, so this could be added to the discount, but still, something does not feel 100% right here from my perspective.

BioNTech:

Tomorrow is the day when BioNTech is supposed to announce how the separation between the founders and the company will look like.

There was a lot of noise around Berkshire’s 10 bn participation in the Alphabet capital increase. However, at the Berkshire AGM, Greg Able mostly singled out the investment of Berkshire into Japanese Insurer Tokio Marine as a great investment.

Therefore “Hello Japan” for the first time on the blog.

Interestingly, I was not able to find any real write-ups on Substack, just a few very “light” ones mentioning the Berkshire partnership. The “Buffetologists” have ignored that one so far.

Strategic Investment: NICO acquired a 2.49% stake in Tokio Marine Holdings for approximately $1.8 billion, with options to increase its holding up to 9.9%. To my understanding, Tokio Marine sold Treasury shares to Berkshire.

Reinsurance Agreement: Berkshire entered a whole-account quota-share reinsurance arrangement, absorbing a portion of Tokio Marine’s globally diversified portfolio to help the Japanese insurer mitigate natural catastrophe and underwriting volatility. M&A Collaboration: Both companies plan to collaborate on global M&A and strategic investment opportunities.

Technically, the investment is done by NICO (National Indemnity), not Berkshire. The third part is really interesting and unique. It will be interesting to see how this would look in practice.

Tokio Marine overview

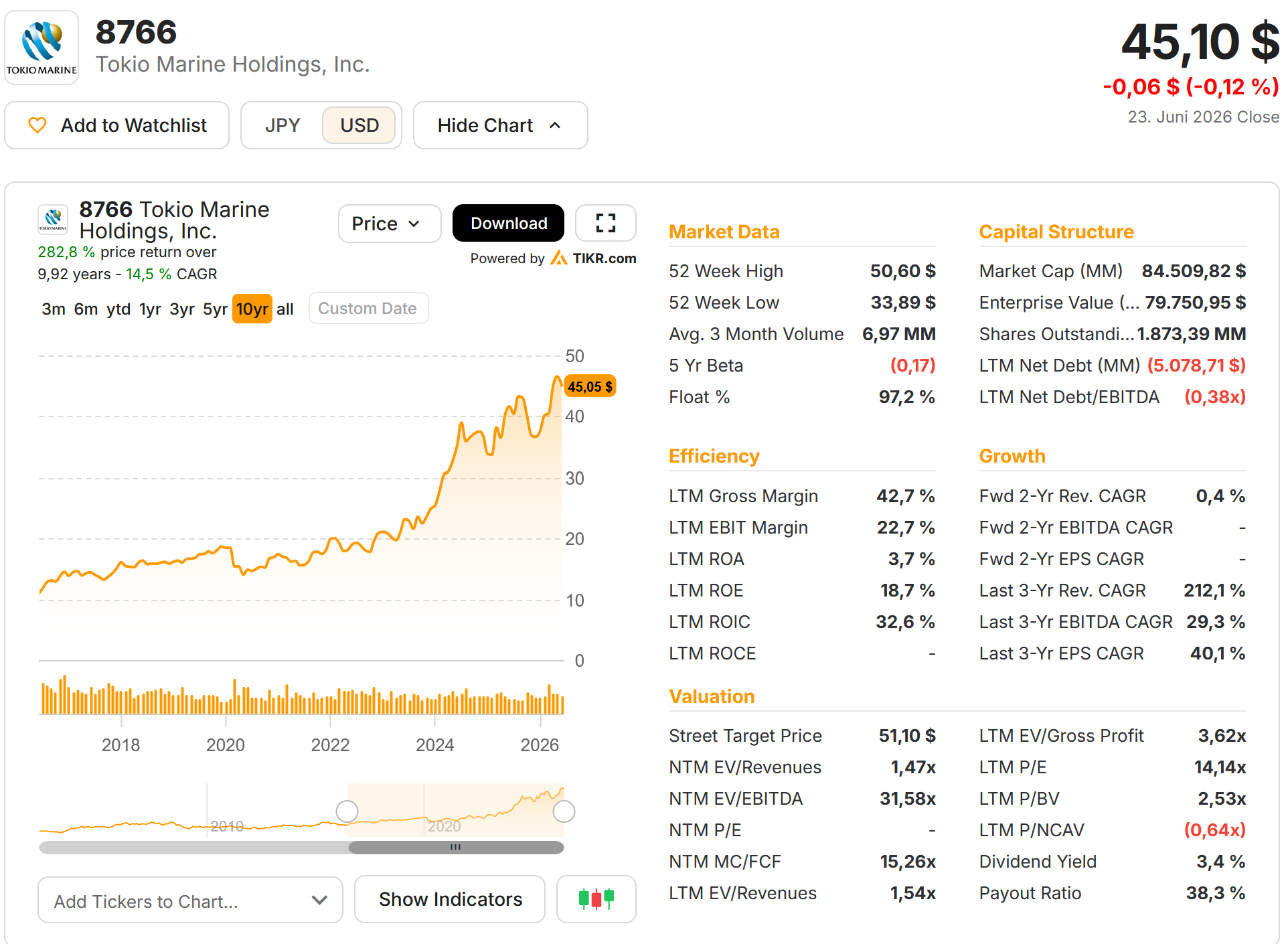

Looking at the TIKR overview, we can see that Tokio Marine has a market cap of around 85 bn USD, is quite profitable and trades at 14x LTM P/E. The 3% dividend yield is quite high for Japanese standards.

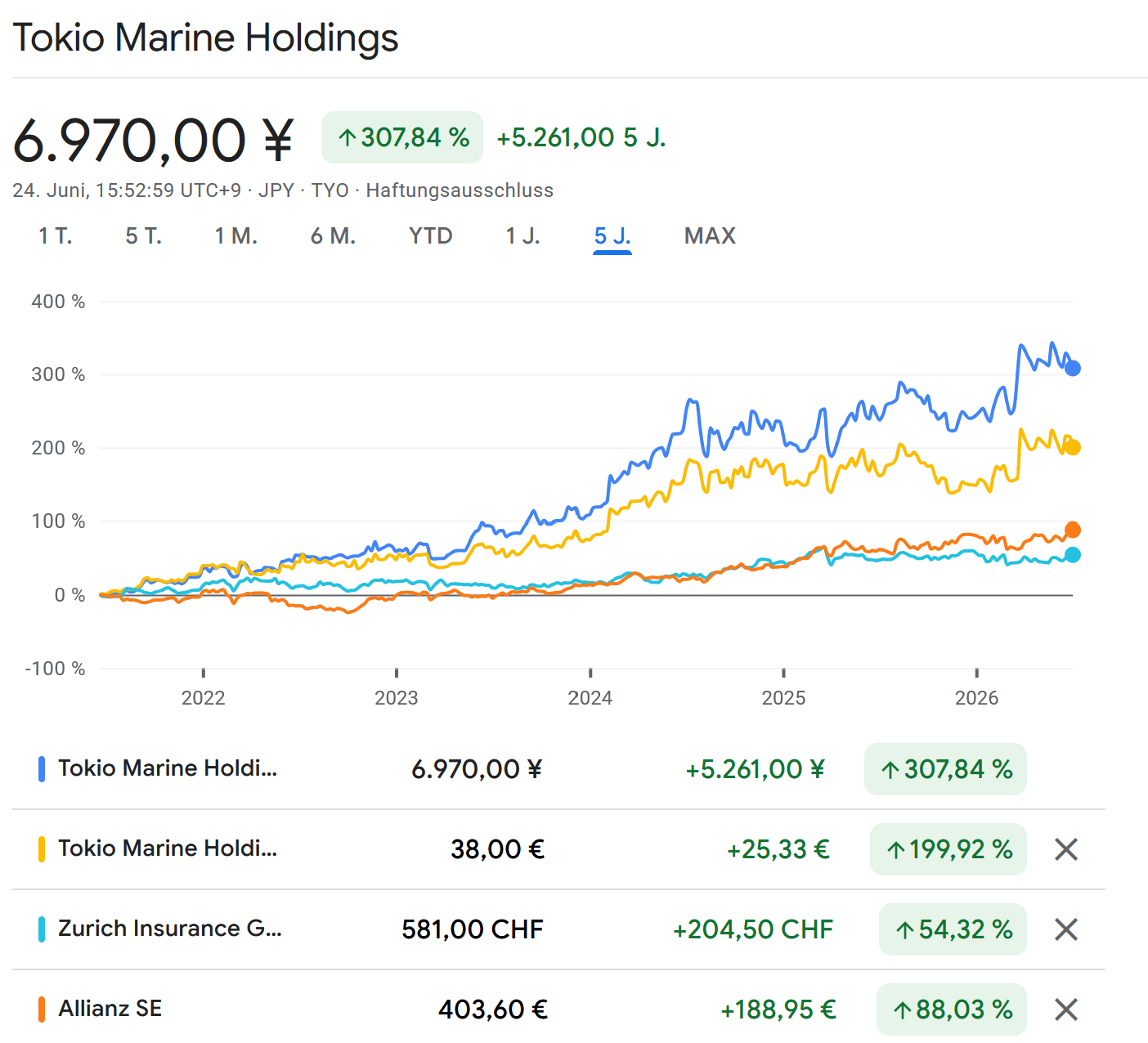

The share price has done very well in Yen. Although as this chart shows, part of the more recent performance is also due to the very weak yen. But the company still easily outperformed the European peers Zurich and Allianz by a wide margin over the past 5 years:

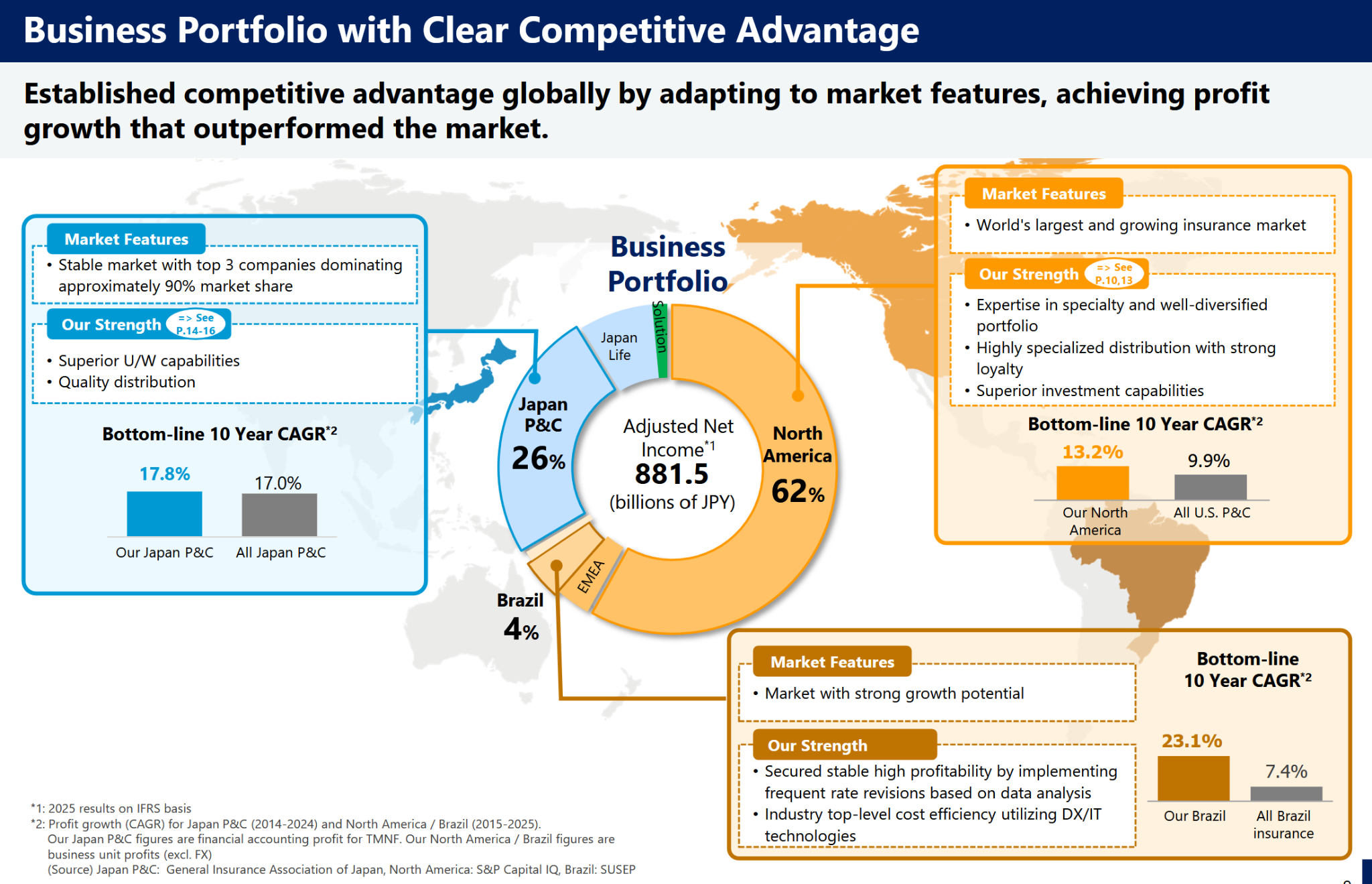

One aspect that really surprised me is that their business seems to be by majority in the US (measured by “adjusted net income”) as this chart shows:

So essentially, Tokio MArine is a US Specialty Insurer with a Japanese business. Looking at the mixed track record of Japanese acquisitions in the US, this looks rather smart in comparison.

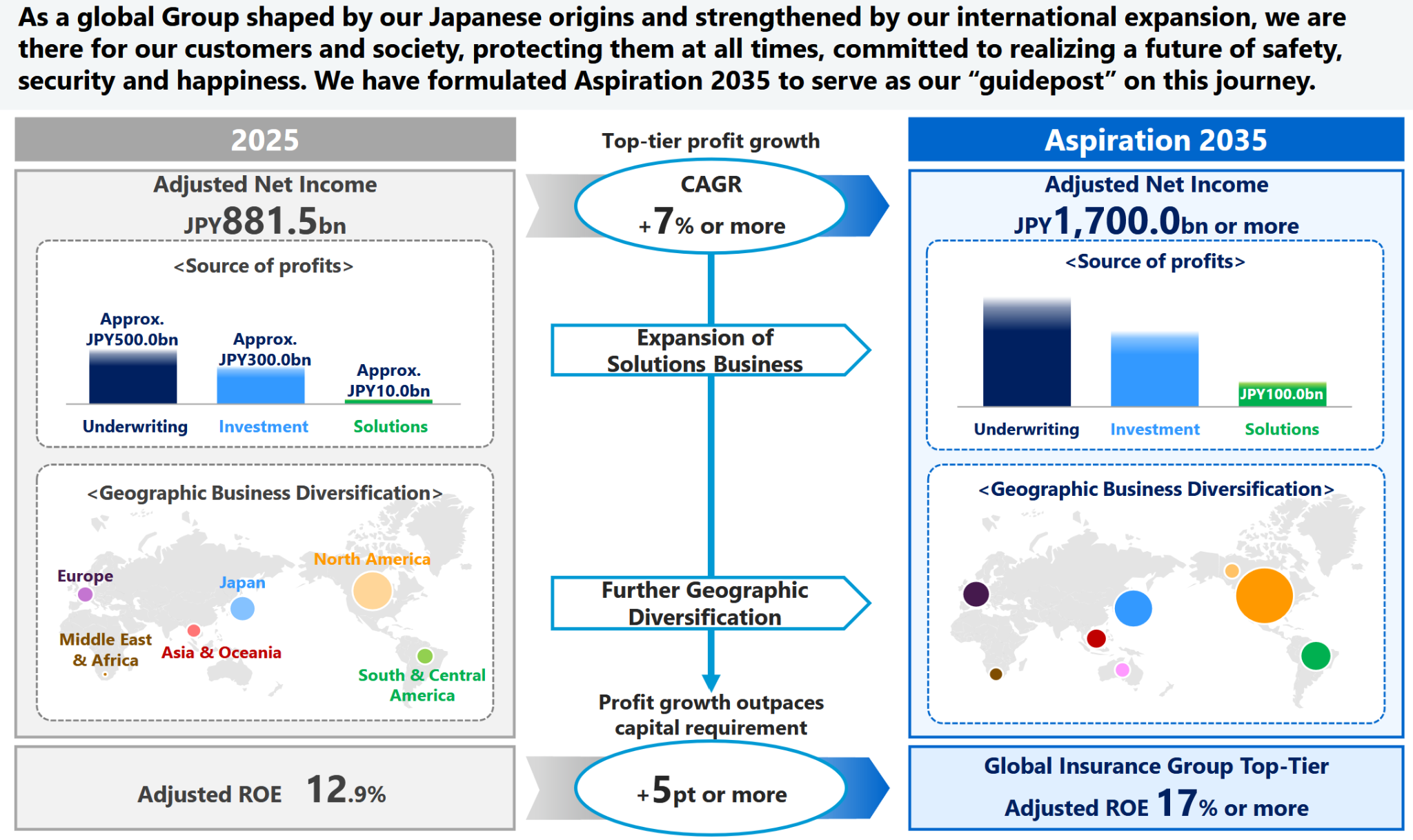

Business plan:

Their plan is to double Net income by 2035:

This is some more detail:

Of course, as insurance is not always predictable, this should be taken with a grain of salt, but putting out a 10 year plan is nevertheless a very positive aspect.

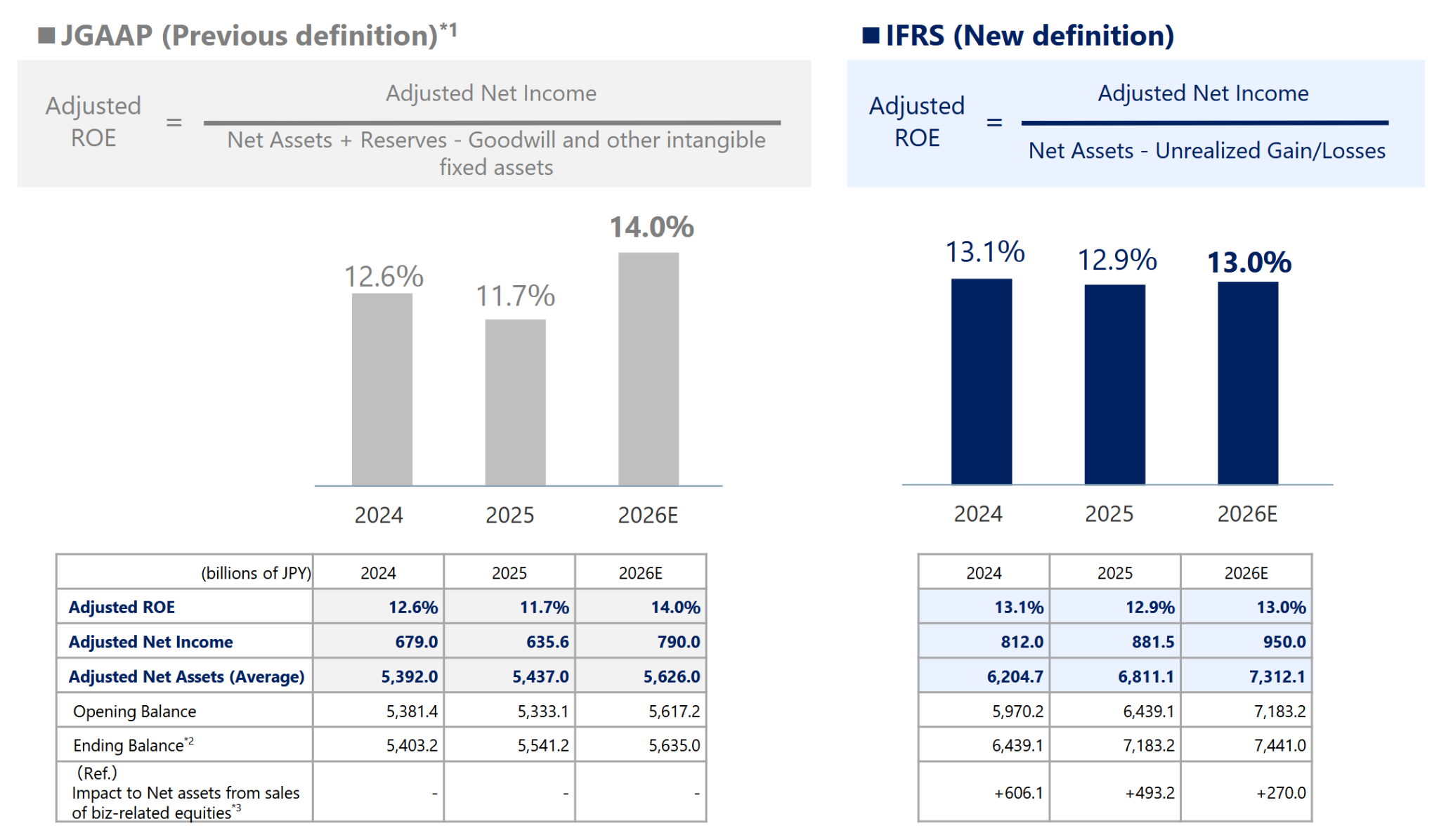

Switch from Japanese GAAP to IFRS

What makes things a little bit more complicated to analyze is the fact, that according to the presentation, Tokio Marine is switching from Japanese GAAP to IFRS in 2026.

They have this table which seems to indicate that IFRS profits are higher, but ROE lower, as net assets (Equity) is jumping after the switch:

Overall; Tokio Marine estimates that profits on an adjusted basis will be higher and less volatile compared to JGAAP.

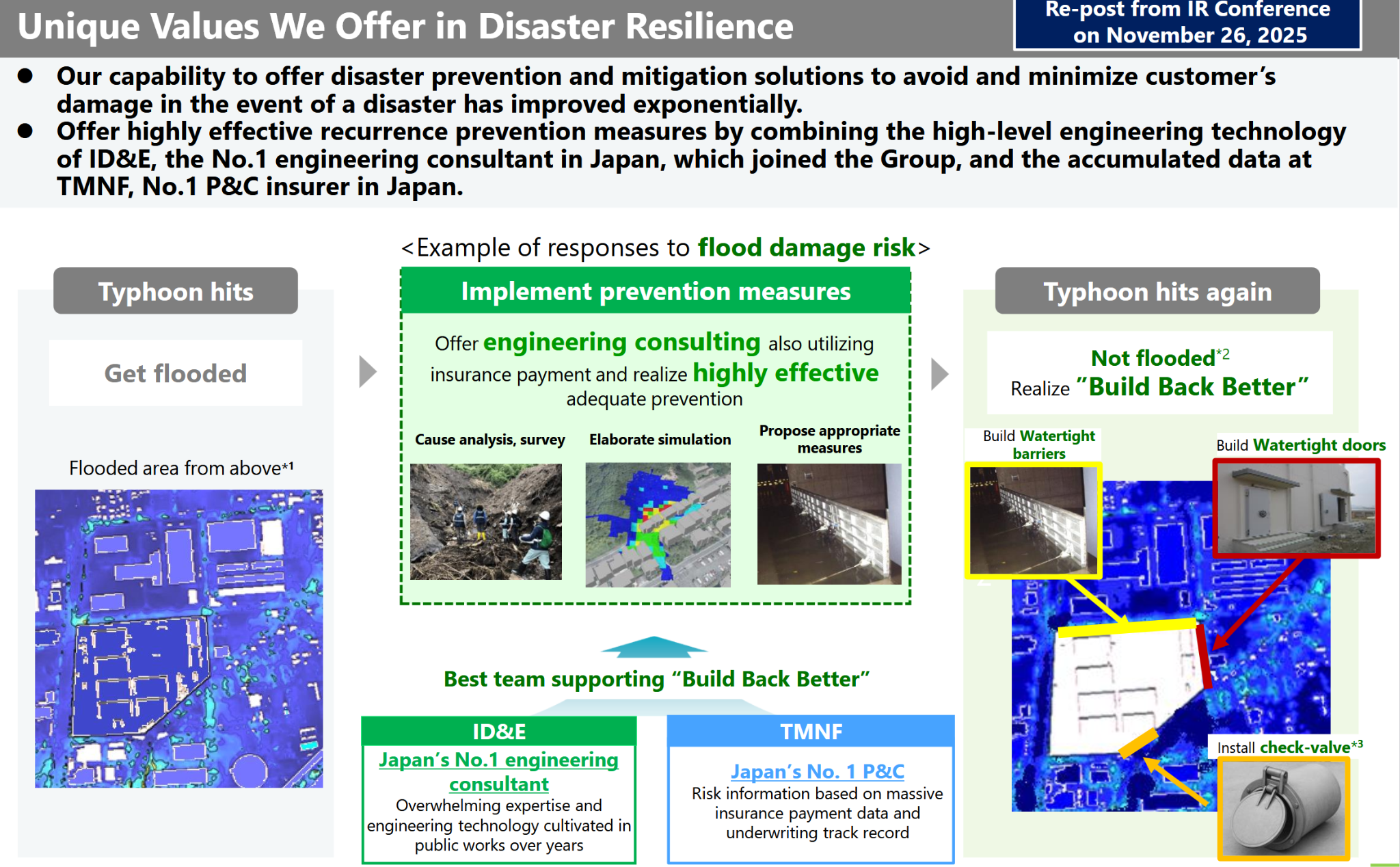

Buying an Engineering design company

One pretty unique transaction was their purchase of an Engineering design company in 2025. That’s pretty unique among insurers.

I am really curious if and how this will actually develop in the next 2-3 years.

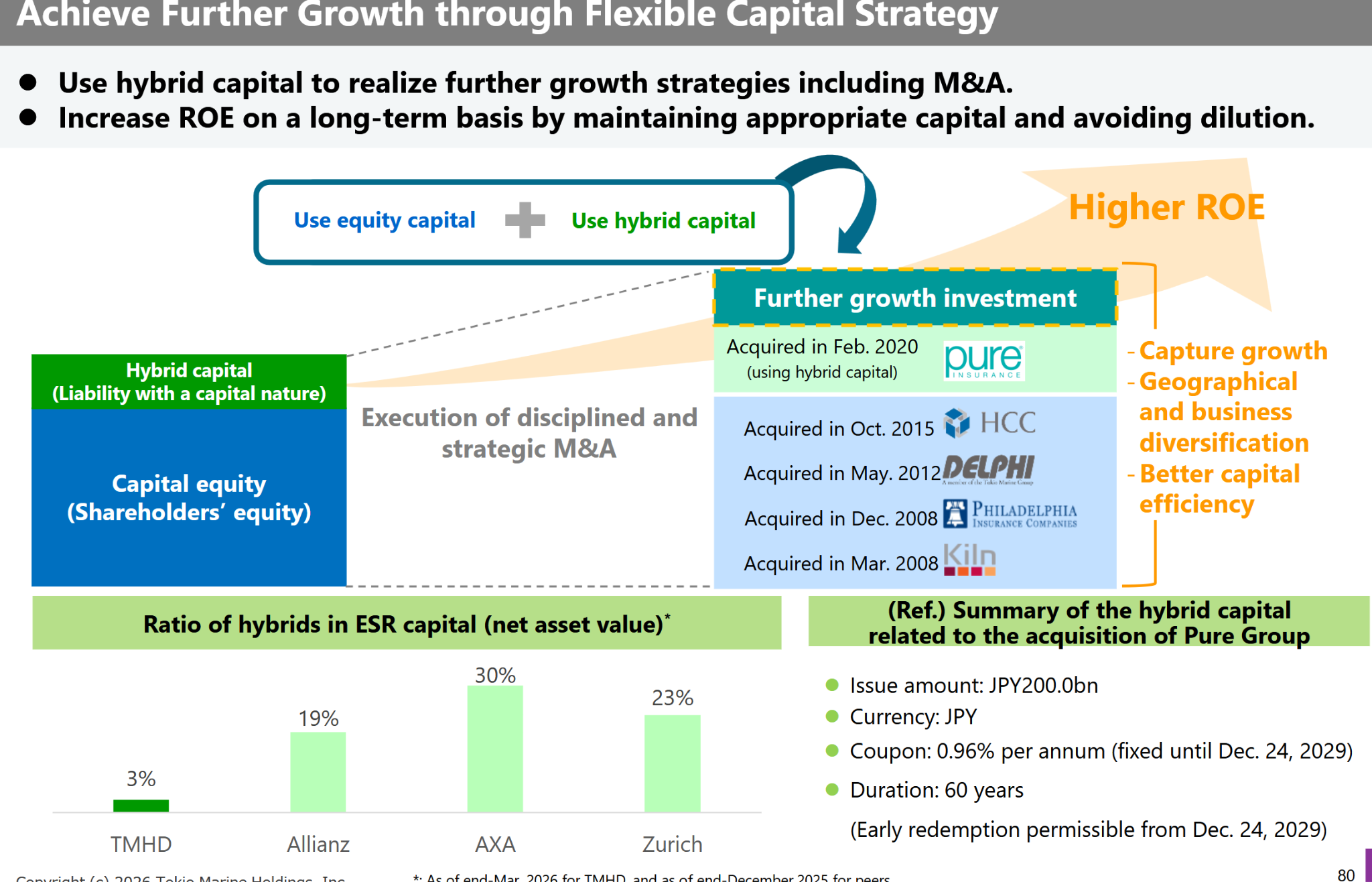

Capital optimisation

One of the “dirty secrets” of Insurance stocks is that a significant part of the Big Insurer’s capital base consists of bonds, so called “hybrid bonds”. Those are significantly cheaper than equity. This is Tokio Marine’s slide that shows that they have made little use of that so far:

Just getting to their competitor’s levels gives them a lot of flexibility with regard to M&A and/or share buybacks.

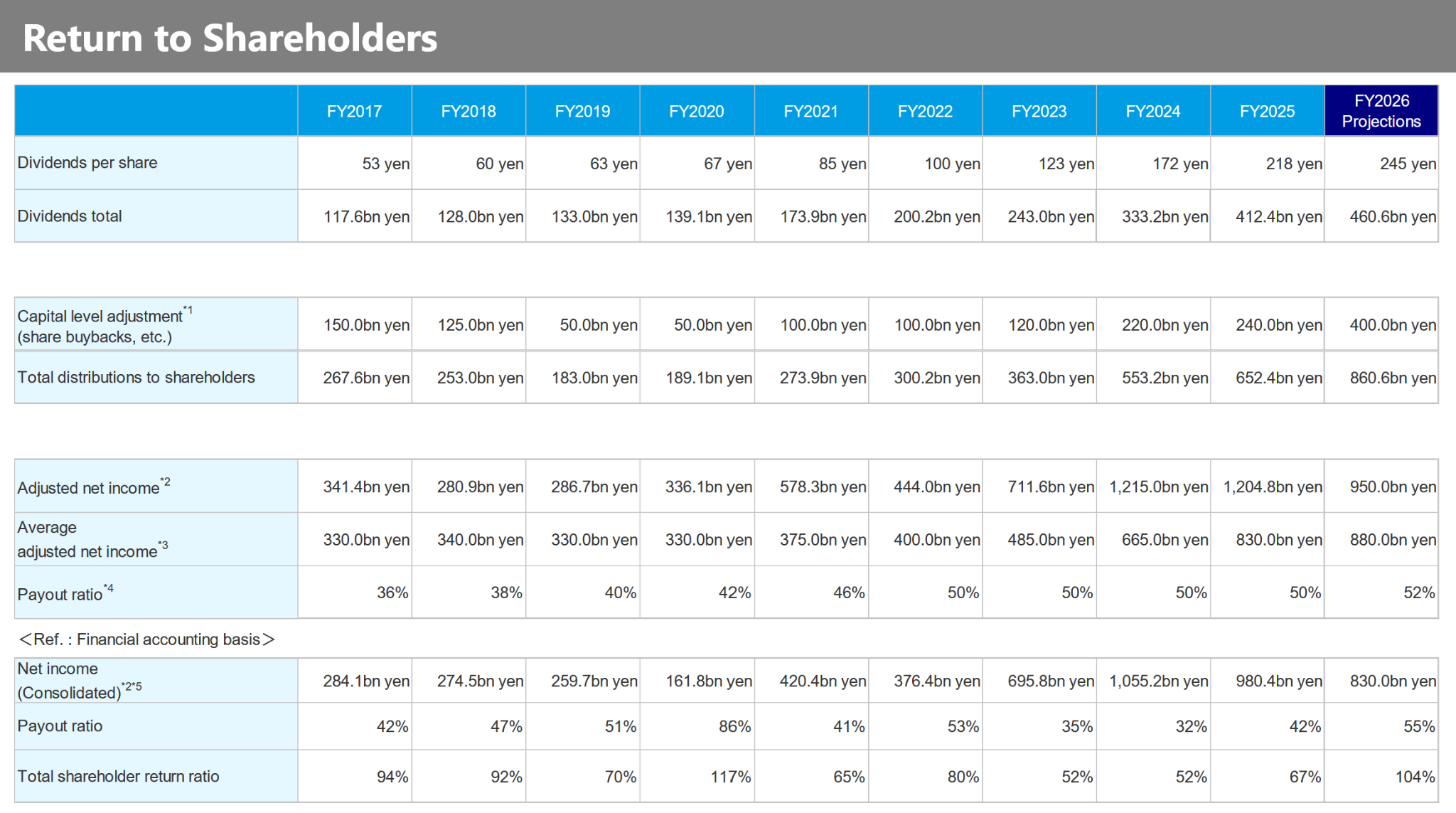

What’s interesting is clearly also how Tokio Marine has increased dividends and share buybacks over the past 10 years which can be seen in this table:

Return expectation:

A simplified return expectation for Tokio MArine would look like this:

Dividend yield + Buyback yield + growth rate

Taking Tokio Marine’s numbers this would result in:

3,1% + 1,5-2% + 7% = 11,6-12,1% p.a. without assuming any multiple expansion

This is not bad, but to be honest, also not super great.

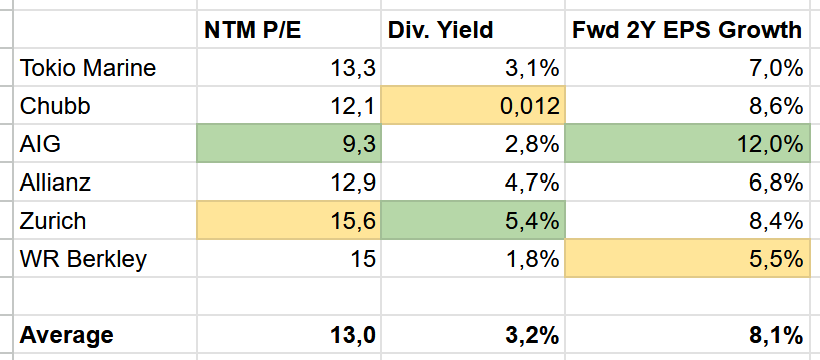

Here is a quick Peer Group table which shows that Tokio Marine enjoys an absolute average valuation in my subjective Peer Group:

The question or upside would be if Tokio Marine is really an “above average” player, then maybe they would deserve an above average multiple. Based on their very conservative capital structure, they should (in theory) be able to grow more than competitors.

To be honest, based on this quick check, I am not yet ready to give them an “above average” rating despite Ajit’s endorsement.

Pro’s/Con’s

As always, a quick summary of Pro’s and Con’s

Ajit generally knows what he is doing & Berkshire Cooperation

+/- not super cheap, expected return below my hurdle rate +/- Japan GAAP to IFRS transition +/- complex business

+/- USD/JPY risk (as EUR investor)

General Nat Cat exposure (famous Japanese Earthquake)

Summary:

Tokio Marine looks kind of interesting. Especially the fact that the majority of its profit comes form the US is a big surprise to me.

However, after the Berkshire announcement, the stock is not so cheap anymore.

So for the time being I will put it onto my “focus watch list” but not invest. I think it will be interesting to see how IFRS results will look like in 2026.

In any case, this shift from JGAAP to IFRS seems to be a very interesting item for Japanese insurers.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

Publishing research is a good way to get constructive feedback. With regard to my Norma Group Special situation post from earlier this day, one friendly person reminded me that there were at least two cases in Germany of big Buy back tenders in the past which had separable tender rights. I didn’t remember them, neither did Gemini.The two cases were:

In both cases, for every share you owned, you “only” got a “partial” tender right, i.e. for Rocket, every share got a right to tender only ¼ of a share. The Rocket internet case was very special, as Oliver Samwer “gifted” his tender rights to activist investor Elliott.

But the principle is clear: In order to tender more than your relative share, you had to buy additional tender rights. You canot just hope that someone doesn’t tender and you will then benefit.

So far, with Norma we don’t know if and how they will offer these separable rights, but this could change and require more active involvement especially when the tender rights are trading.

I just wanted to put this out. I have not sold or bought any shares because of this. I need to research the two cases and potential other cases more closely.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

Executive Summary:

Norma Group, a previously PE owned German manufacturer of small connector parts, is planning to use part of the cash it received from selling a division to buy back a significant percentage (>30%) of its outstanding shares via a tender offer at a premium of up to 20% compared to the current share price.

Although there are some moving parts and the overall case turned out to be more complicated than I thought initially, this represents a potential uncorrelated special situation for 3-4 months with an expected (probability) return of around 13% based on my assumptions.

Norma Group Background/Introduction

Norma Group has clearly seen better days. IPOed in 2011 as a previously PE held company (3I), the stock price did well until 2019 before then losing -80% when the stock price reached a low of below 10 EUR per share in early 2025:

Interestingly, according to TIKR, Operating margins had been on a downtrend since the IPO date and EPS peaked in 2017, but until 2019 no one bothered too much:

Norma was active in what they called “joining technology”, mainly connectors and other small parts out of metal and plastics for industrial applications, the car industry and “water applications”. Here a sample picture:

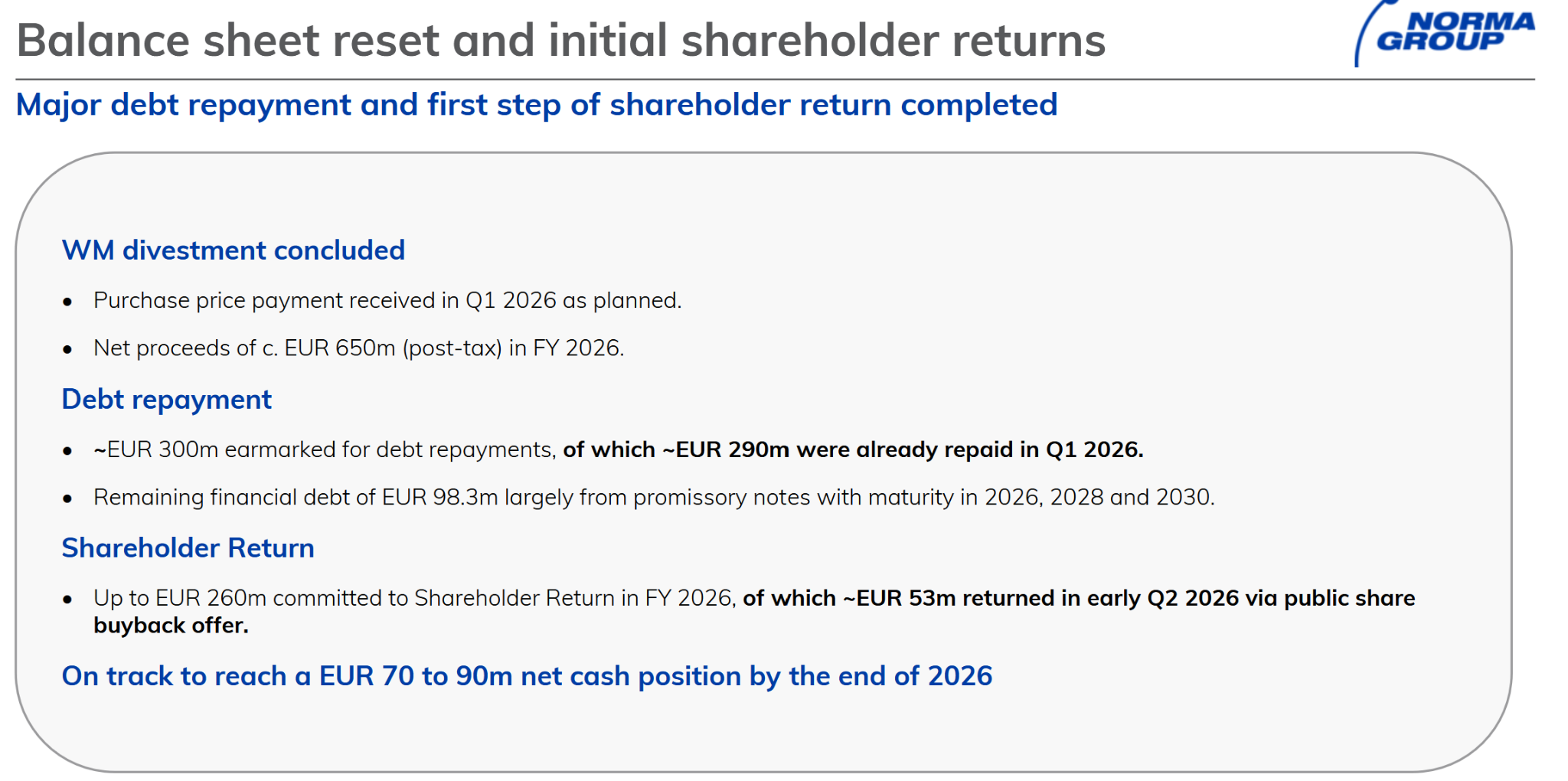

Norma said that they already paid back most of their debt and will keep 70 mn for investments into the remaining business and use the rest to buy back shares.

However, that only partially resolved the Excess Cash problem which leads us to this

The special situation: A 30% (plus) buy-back tender at a (up to) 30% premium

Three weeks ago, Norma announced a 208 mn EUR share repurchase tender at a premium of “10% to 30%” to a certain reference price.

Under German corporate law, in this case the AGM has to approve this decision before the board can formally issue a tender offer. The AGM will take place on July 1st in Frankfurt.

The long stop date for both, the acquisition and the cancellation of the shares is February 27th 2027

The buy back premium will be between 10% and 30% (the management board has signaled that they are going for 30%) compared to a certain “reference price”

The total amount that will be spent is 208 mn EUR in any case

Shareholders will receive a dividend of 0,14 EUR after the AGM in any case

That reference price is defined as follows

Initially I thought that this was referring to the date of the initial board resolution,which would have translated into a reference price of 15,62 EUR, but after an in-depth discussion with Gemini, I think it is the 90 day period prior to actually publishing the offer.

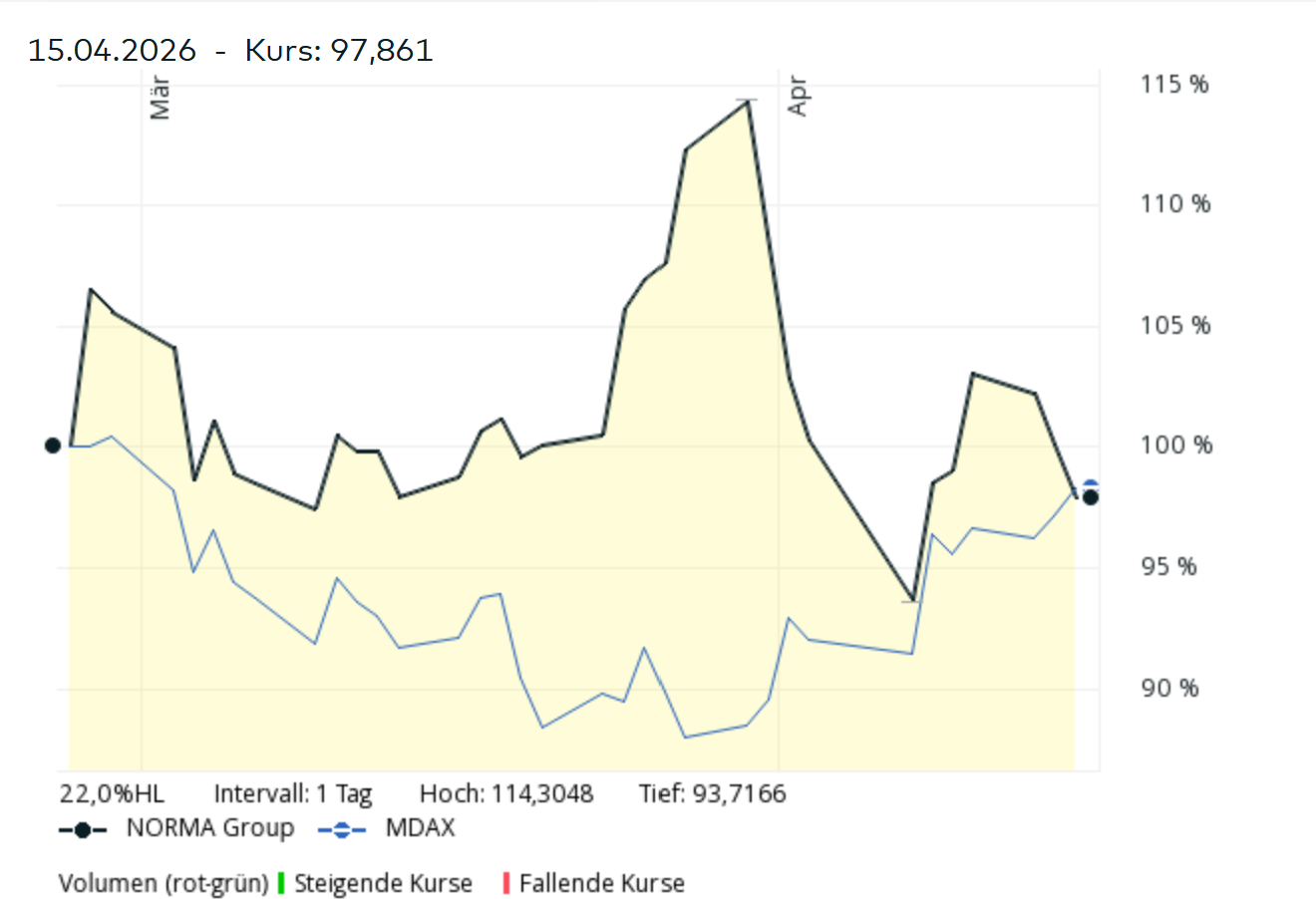

At the time of writing, the current 90 day average of Xetra closes is 16,09 EUR and increasing as long as the share price is at the current 17 EUR as we can see in this chart:

That the upper cap of the buy-back price is 20,87 EUR which is a “fair value” estimate by the Management

This is how this has been derived:

The Management Board has therefore, in preparation for the Capital Reduction proposed to the Annual General Meeting, commissioned a valuation of the Company in accordance with the IDW S1 standard as at 31 March 2026. This valuation resulted in an average value of EUR 20.87 per NORMA Group Share as at that date.

Looking back: How did the first tender offer in March work out ?

In March, Norma made a buyback tender for 16,59 EUR per share for up to 10% of the total share capital.

This was released on February 26th 2026. The closing price the day before was 14,92 EUR per share, so ~10% premium. The offer period ran from Feb 27th to March 27th.

Interestingly, 18,1 mn shares or around 57% of all shares were tendered, which is a lot for such a small tender with a relatively small premium. As only 10% of the shares were available, only 17,6% of the tendered shares were bought back. We will look at this later once again.

Interestingly, as we can see in the chart, the share price reached a high of 17,10 EUR on the day after the end of the tender period. One week later, on April 7th, the share price reached a low of 13,78 EUR, around -20% vs. the tender offer price:

Maybe that had to do with the release of the 2025 numbers on March 31st and the news that the CEO would step down.

The current Tender: What we don’t know

As I have outlined above, we know certain things about the tender already, but not everything. The main variables that we don’t know are as follows:

What will be the ultimate premium & share price at which the tender will take place ?

Although they state that the buyback will happen at a range of between 10-30% above the reference price, certain wordings indicate that they will go towards the high end. The most telling sign is the wording in the supplement to the AGM invitation

“The price clause described in section 2.2 enables the Management Board to offer shareholders a repurchase price closer to the intrinsic value of the share.”

For me, this is a very strong indication, supported by their largest shareholder, which will join the Supervisory board, that they will aim for the upper end of the range or close to their “fair value”.

Just to show the numbers:

With 16,09 as reference price, the low end of the range would be 17,70 EUR per share, whereas at the high end would be 20,87 (capped by the “Fair value”).

What will be the acceptance rate of the tender ?

If we assume the 20,87 as the ultimate tender price, this would translate into 208 mn/20,87 EUR = 9,97 mn shares which represents 31% of all shares or ~35% of all shares ex current treasury shares.

So if all shareholders tender fully, the minimum acceptance rate for every shareholder should be 35% (around 2x the acceptance rate from the first offer)

Another assumption is that Teleios, the 17,15% shareholder, will not want to lower their stake when they simultaneously join the board. So if we assume that they tender only 35% of their shares, we can assume that another 17,15-(0,35*17,15%)=11,2% of shares will not be tendered for sure.

This translates into a “worst case” acceptance rate of around 40% for the scenario with the maximum purchase price.

On the other hand, it is also very likely in such cases that not everyone tenders. I will solve this issue by creating several scenarios and weighting them with my subjective probabilities. More on this later.

At what price will one be able to sell the shares that are not accepted in the tender

This is clearly a tricky one, but it is also necessary to assume that one in order to be able to calculate an expected return for this special situation.

My assumption here is that one should at least get the current reference price of 16,09 EUR per share. I will share some thoughts on the potential value of the “stub” at the end of this post.

Actual timing of the offer

To be honest, I am not 100% sure how fast they can execute after the AGM approval. There might be some regulatory requirements (entry into the company registry) or maybe some of the usual suspects will try to blackmail the company with legal challenges.

But my assumption would be that the tender offer period starts in August and will be concluded in September. So from today, the time required for this to fully play out will be 3,5 to 4 months.

AI excursion: Analyzing the potential tender rate and resulting Acceptance rate

One main element that one needs to estimate is the percentage of shares that will actually be tendered. I have mentioned in the beginning, that in the first tender, 57% had been tendered with only 10% available, resulting in a relatively small acceptance percentage of 17,6%.

Based on empirical evidence, a higher premium increases the tender rate, but a bigger tender size relative to the outstanding shares increases the acceptance rate.

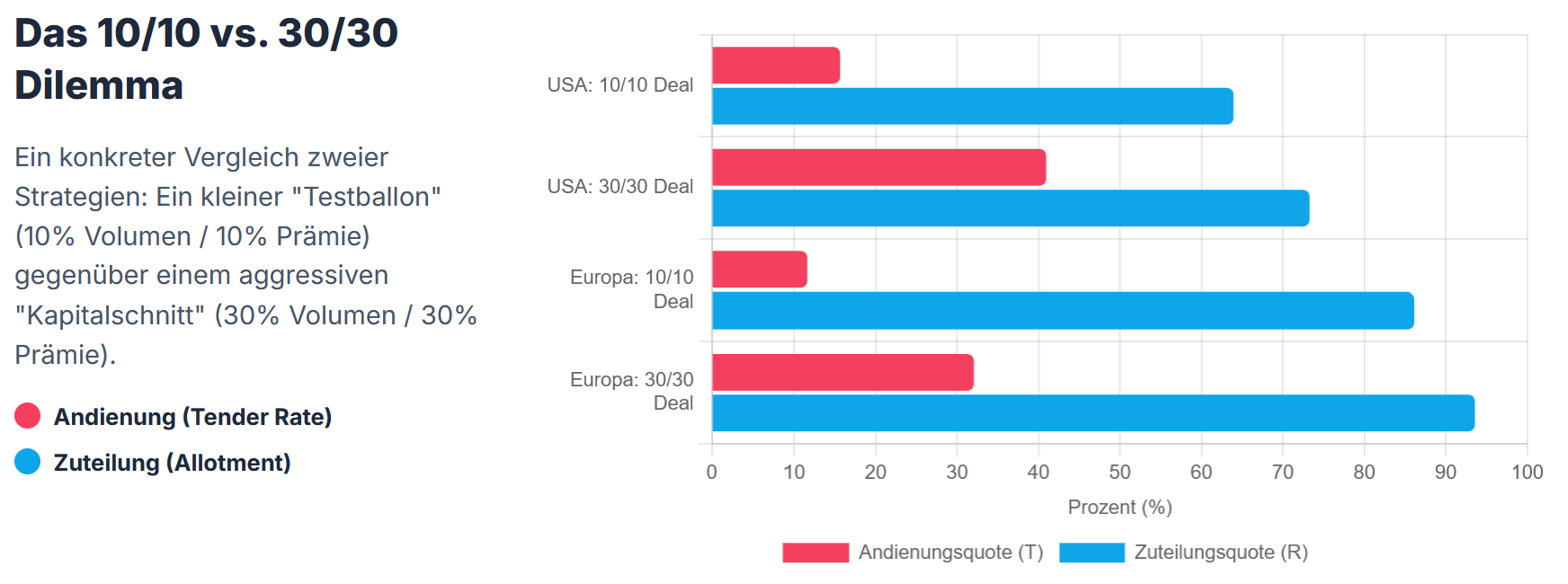

I asked Gemini to analyze tenders from the past years and estimate a regression. Interestingly, tender ratios are often quite low and acceptance rates much higher than one would normally think.

This is what Gemini estimated for a 30% Tender with a 30% Premium vs. a 10% Tender with a 10% premium both, in the US and Europe:

According to their regression, a 90% Acceptance/Allotment should be expected and only 30% of shareholders would tender. Now this sounds to good to be true and the first tender of Norma earlier seems to have been already a clear outlier.

So looking at historical data clearly helps but in any case one has to make one’s own assumptions for this case.

Overall; I do like to use AI models as a sparring partner especially in these Special Situations. Although one needs to get used to its “cocky” behaviour, I do think the discussions and additional analysis improve the process and hopefully, in the long run over many transactions, the outcome.

Return estimation based on a 30% premium to the reference price:

So now we have everything to estimate an overall expected return, of course based on all the assumptions I described above.

Here is my return estimate based on the 30% premium (capped at 20,87 EUR) and on a current share price of 17 EUR (including the dividend and 16,09 selling price for not tendered shares):

So 13,3% “expected return” over 3,5-4 months is not too bad given the current 2,25% short term interest rate in EUR.

Of course this is based on my assumptions that I have laid out above and different assumptions lead to different results.

Many of the uncertainties will go away over time such as:

The AGM will take place on July 1st. After the AGM we will know if someone wants to play games with the tender offer or not and how a realistic time table will look like

Once, the legal requirements are met, the management will formalize the offer and we will then know the actual premium

Finally, after the end of the tender period, we will know the final acceptance rate and then also the share price for the shares that can not be tendered

What happens at the low end, a 10% premium ?

This would of course be less attractive but one needs to consider the following: Norma intends to spend the full 208 mn, so the assumption here would be that they buy back more shares and the acceptance ratio will go up. The minimum acceptance would be 47%.

Also, there would be more value for the stub, but I will stick with the 16,09 EUR as selling price for the non-tendered shares. The probability of the acceptance rates also needs to be adjusted upwards.

Based on these assumptions. my return expectation looks as follows:

So at the low end which is basically almost the worst case, I would have a return of ~2% based on a current share price of 17 EUR. Only in the worst case, when basically everyone tenders, there would be a small loss.

So based on my assumptions, the situation looks like a pretty cheap “option” on a potentially higher acceptance ratio.

Some thoughts on the “Stub”:

If we assume that the tender gets through and that the shares will go back to 16 EUR per share, we will have a company that has around 18,7 mn Shares outstanding at a market cap of 18,7*16= 300 mn EUR if they pay the 30% premium

They plan to have a net cash position of 70-90 mn EUR by the end of 2026 according to their Q1 presentation, so EV would be between 210 and 230 mn EUR.

For 2026, Norma expects 820-830 mn EUR in sales and a 2-4% “adjusted EBIT margin” which would translate into ~16-35 mn in “adjusted EBIT”. At the midpoint, this translates to 25 mn adjusted EBIT or an EV/Adjusted EBIT multiple of 8,4-9,2x.

In the case of a 10% premium and a 16 EUR share price, the market cap would be ~270 mn EUR and EV/EBIT between 7,2-8,0 x EV/EBIT.

Not “dirt cheap” but not expensive either. In the second half of 2026, they plan to present a “2028 strategy”.

I think despite the relatively unexciting business, the valuation of the stub is cheap enough that I think that from a fundamental side, the downside risk is limited to a certain extent after the execution of the tender. Of course, if there is an overall market crash, no one cares about fundamentals anyway.

One important point here: For the time being, I am not planning to bet on a turn-around.

For me this is a Special Situation investment and I will exit once the tender is settled.

Technicalities:

This is an interesting detail from the invitation to the AGM

To the extent technically possible with reasonable effort, tender rights trading (Andienungsrechtehandel) is to be established.

The shareholders’ declarations of acceptance are taken into account according to shareholdings by tendering the tender rights attributable to the shareholding as well as any additional tender rights acquired from other shareholders.

So this means that there might be a mechanism that similar to a capital increase with subscription rights, in this case the tender rights might be split of from the shares and traded separately.

I haven’t seen this before and if this is implemented, it could create a special situation in itself, if those rights might trade higher or lower than the intrinsic value. So from that perspective there might be an additional “option” to improve the outcome

Timing option

As we have seen in the example of the fist tender, during the official tender period, the shares had already approached the tender price. Depending on how this is structured, I will definitely make sense to tender rather late in order to keep the option of selling the shares at a decent price before the execution of the tender.

If we have separate tender rights, then the opportunity will be mostly in analyzing the tender rights as mentioned above.

Summary:

At the current price of 17 EUR, I do think that the upcoming tender offer of Norma Group offers a decent return to park some cash for 3-4 months at an expected (probability weighted) return of 13% (not annualized).

Even at the low end, under my assumptions one would be able to make a 2% profit and the very worse case would result in a small loss (less than 1%).

For a special situation, I think there is also a lot of additional optionality baked into this whole process which in my opinion outweighs the uncertainties.

There are still a couple of moving parts and the tender is rather complex, so my overall allocation to this is rather small at 3% of the portfolio.

I will watch this very closely and I might increase the position if the price goes down or if new positive information comes in and the price stays low.

What I do like is that the risks are very specific and not much correlated to the overall market, which makes it attractive for the “opportunity” part of the portfolio.

I guess that also the complexity of the offer creates an opportunity here.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

This is a 12,5% increase (ex dividend) from the initial offer. Less than I expected but it seems the board off DCC is already happy with this:

Having carefully evaluated the Revised Proposal together with its advisers, the Board of DCC considers that the financial terms of the Revised Proposal are at a level which the Board of DCC would be minded to recommend to DCC shareholders should a firm intention to make an offer pursuant to Rule 2.7 of the Irish Takeover Rules be announced by the Consortium on the same financial terms, and subject to the satisfactory agreement of the full terms and conditions of any offer and satisfactory agreement and execution of definitive transaction documentation.

Just to be clear here as a reader asked why the price did not directly jump to the offer price.: KKR hasn’t made a formal offer yet. This is so to say the “pre-discussion”.

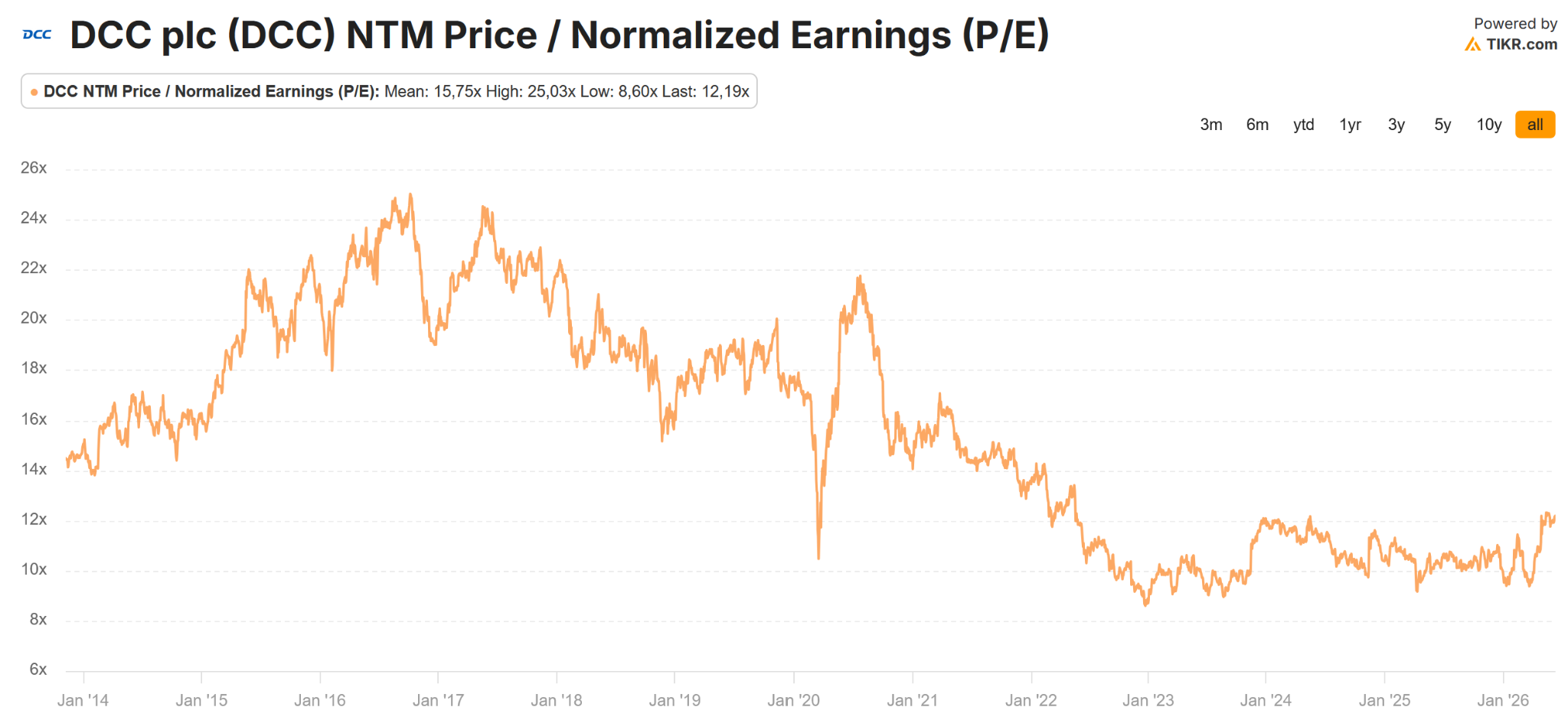

Looking at DCC’s long term share price, the offer price equates roughly the share price DCC had 10 years ago:

Looking at the historical P/E, we can also see that 2026 was the period in time when people thought that DCC is a 24x NTM P/E business:

As DCC’s board seems to have already accepted the bid, the only further upside would be now a counterbid from another PE fund or a strategic buyer.

I am not sure how probable that is, but maybe not 0% either.

Such rumours are actually not rare in these situations. Sometimes they are launched by hedge funds who might not want to wait until the offer is executed but get out close to the offer price long before that. In other cases, the rumour actually becomes true.

Wise Plc – What is the potential impact of the AML issue

I think what is important to know is that the subsidiary in Belgium is not a tiny little subsidiary but basically handling all Euro transactions for WISE. I guess this has regulatory reasons.Unfortunately, Wise doesn’t report what percentage of its volumes have one leg in EUR, but it is clearly a very significant currency.

The size of a potential fine

The question that I had and tried to solve with AI is the following: Suppose Wise is “guilty”, what would be the fine they would have to pay and what or the other consequences ?

In reality, without making this to sound harmless, these kind of AML issues are not that rare, so there are precedents.

Here is what Gemini is saying:

the maximum charge from a criminal perspective (if guilty) in Belgium is “only” 1,6 mn EUR

the maximum penalty from an administrative side could be up to 10% of sales or in Wise’s case around 190 mn EUR

In practice, the fines often seem to be a level of 1% of the volume. So overall, Gemini estimates the fine to be in the range 5-10 mn EUR. Which would be not so much.

Indirect costs: More compliance

The more critical part could be cost increases through additionally required Compliance functions. Gemini estimated that total compliance costs (which the estimate at 260 mn GBP at Wise) could increase by 30%, which would be around 80 mn GBP/100 mn EUR per year, which would be quite significant.

I think that is maybe an over-estimation, as so far, this only concerns the European operations. but still, 10-30 mn EUR per year could be realistic.

A further risk is that more compliance also maybe means less customer satisfaction and slower growth.

If we take May 29th as a reference, where the share price was at 9,35 GBP, as of the time of writing, the share price is down ~1,15 GBP or -12%. In monetary terms, Wise lost more than 1 bn GBP in market cap.

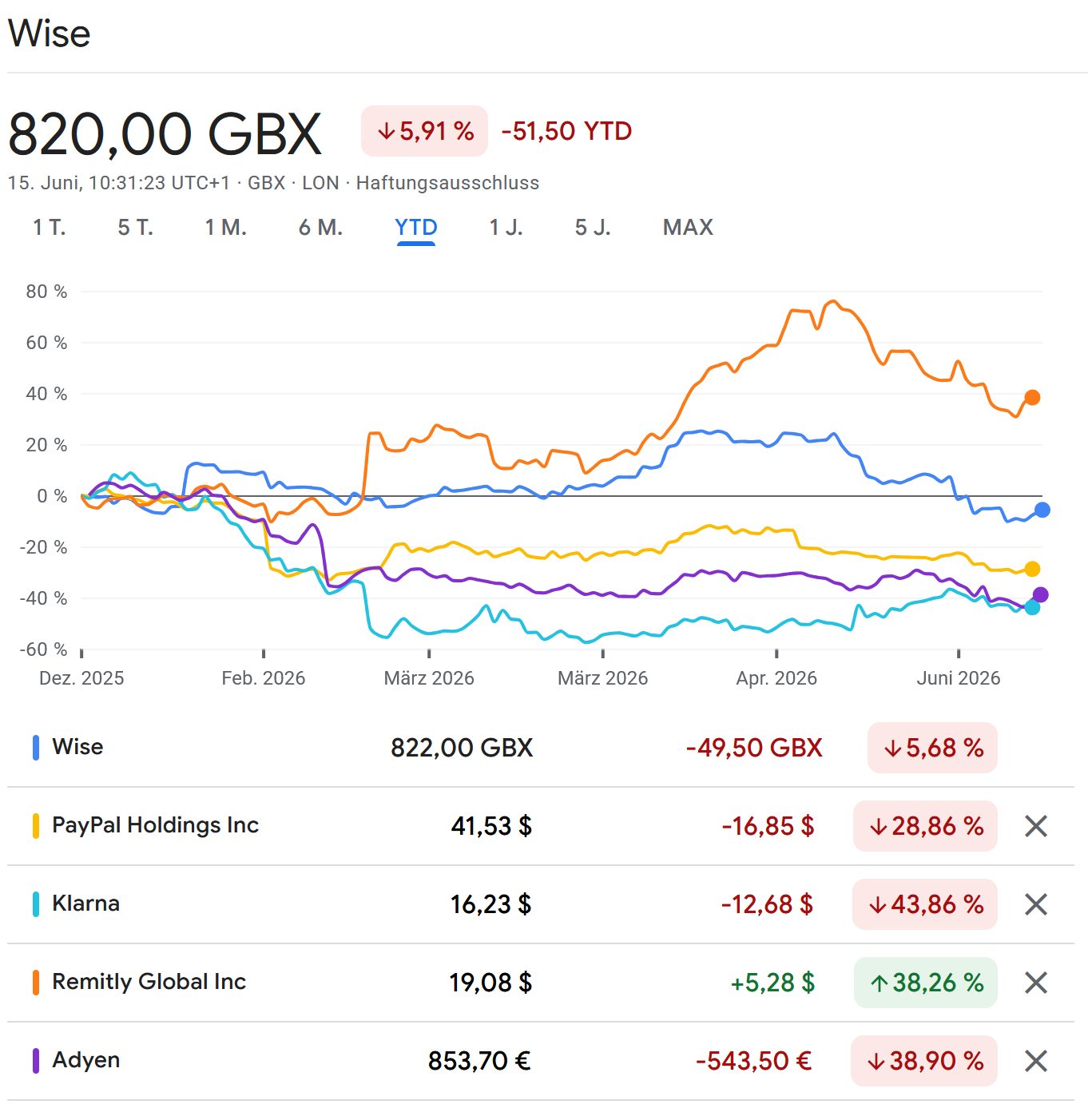

Payment in general has a difficult time in 2026

Another aspect is that payments in general are not doing that well in 2026. I have collected a small peer group here where Wise is still one of the better performers:

So where does that leave us with Wise:

For me, it is currently too early to say if and how this could impact Wise in the future. The share price drop clearly prices some pain and AML is always a risk for money transfer businesses, but I am not 100% sure if now is the time to increase the position. So I personally will wait for the next 2 or 3 quarters to see if growth keeps up and maybe add then.

If the share price falls significantly from here, I would rather sell and watch.

Last week I mentioned in the comments on the blog and on Twix that I got some “bad vibes” and decided to liquidate my Rocket Internet position even before the planned SpaceX IPO next week.

There were overall 3 things that kind of spooked me and let me to take the profit (+30%) instead of waiting the one more week. Here are the 3 items:

I mentioned initially, although it was not part of my investment thesis, that there might be a chance of a special dividend. Now it has become clear that there will be no special dividend. However, it also became clear that Rocket Internet intends to limit information flow to shareholders even more in the future which is clearly not positive

SpaceX: Another news item that spooked me was that SpaceX is aggressively pitching via German brokers for German retail investors. German investors had never access to US IPOs before. Some might find this positive, I find that rather “surprising” and potentially a hint that demand is not high enough for Elon’s appetite.

Another surprising event was the “surprise Capital increase” from Alphabet/Google. Interestingly, this represented the largest capital increase of all time at 85 bn USD but there was only very limited coverage about it in the financial news and mostly about Berkshire’s participation. But more on this later

Overall, I decided that the “easy money” was now made with Rocket internet and I was able to sell at around 25,80 EUR per share, netting a profit of 30% within 5 months, which is clearly one of my better “Special situations” investments.

I am not 100% sure that the share price increase was driven by SpaceX, maybe the rapid increase in the value of the Kalshi stake helped as well. I am not sure if there are a lot of other “plays” to benefit from KalshI’s incredible growth.

One could argue that I left some upside on the table here but the success of this investment is almost 100% depending for some time on someone else paying me more for the shares that I paid for, which is something I don’t feel too comfortable for a special situation investment.

Overall, I was clearly lucky with the timing on this one.

2. More SpaceX thoughts: Hyperliquid Perps and Damodaran

As mentioned above, we now know that Elon loves Germany so much that at the time of writing, German retail investors can now access this IPO via 8 or 10 different retail brokers.

According to some sources, in order to compare apples to apples, one would need to discount the price by 10% to make it comparable to the actual SpaceX shares. That means on this “grey market”, a synthetic SpaceX share only trades at ~153 USD, above the 135 USD “sticker price” but inside the 135-162 USD bookbuilding range.

Although no one knows for sure if this has any relevance, it is at least a reference point and it seems to be traded quite liquid.

Another interesting source is the attempt of a valuation by Prof. Damodaran. What I like about Damodaran is that he at leasts tries to put values on these kind of situations and is very transparent with his assumptions. I know most tech bros laugh about these attempts but I think avery serious investor should read what Damodaran writes because there is always a lot to learn.

In a nutshell, Damodaran values SpaceX at about 100 USD per share. The ain changes to his initial, pre prospectus valuation is that he increased the margins for the Space and Starlink business, but significantly decreased the expected margins for the AI business.

“My biggest shift is in my estimated target margin is for the AI business, where the dynamics that are pushing gross margins down, i.e., increased competition and high costs of delivering AI services, will persist; my estimated operating margin drops from 45% to 25%. “

Damodaran is also smart enough to mention that in the first days after the IPO, valuation clearly doesn’t matter at all. But within the first 12 months or so, even for SpaceX, reality will need to be met somehow.

For me however the main take away is the significantly reduced margins for the AI business which leads me to the:

Surprising 85 bn USD Capital increase of Alphabet

Being a Corporate Finance/Treasury guy by training, the news that Alphabet is raising 85 bn USD via a capital increase really surprised me.

According to the FT, this is the largest capital increase in the history of capital markets, the second largest was Petrobras in 2010 at around 70bn.

The financial press focused mainly on the 10 bn stake that Berkshire Hathaway took as part of the package. To be honest, this is a very small amount of money for Berkshire’s current size. It is also hard to really judge how good of an investor Greg Abel actually is.

The interesting thing about this capital increase is that so far, at least in the ~40 years that I follow stock markets, capital increases in size only occurred in the following situations:

Primary share portion in an IPO

Emergency capital raising in a crisis ( e.g. Banks in the GFC)

Major M&A transaction where the acquiring company pays with new shares (Paramount)

In Google’s case, clearly none of the three situations applies. According to TIKR, Alphabet still has net cash despite ~100 bn in bonds outstanding. So in theory they could issue a lot more debt.

I heard the argument that Equity is “cheaper” than debt as the interest rate on a debt offering would be 5% whereas the “earnings yield” at the current 30x P/E is “only” 3,3%. However this does not reflect the tax shield from interest and especially not the fact that Alphabet’s earnings will most likely increase for the foreseeable future and that very soon that “earnings yield” for the issued shares will be much higher than the current 3,3%.

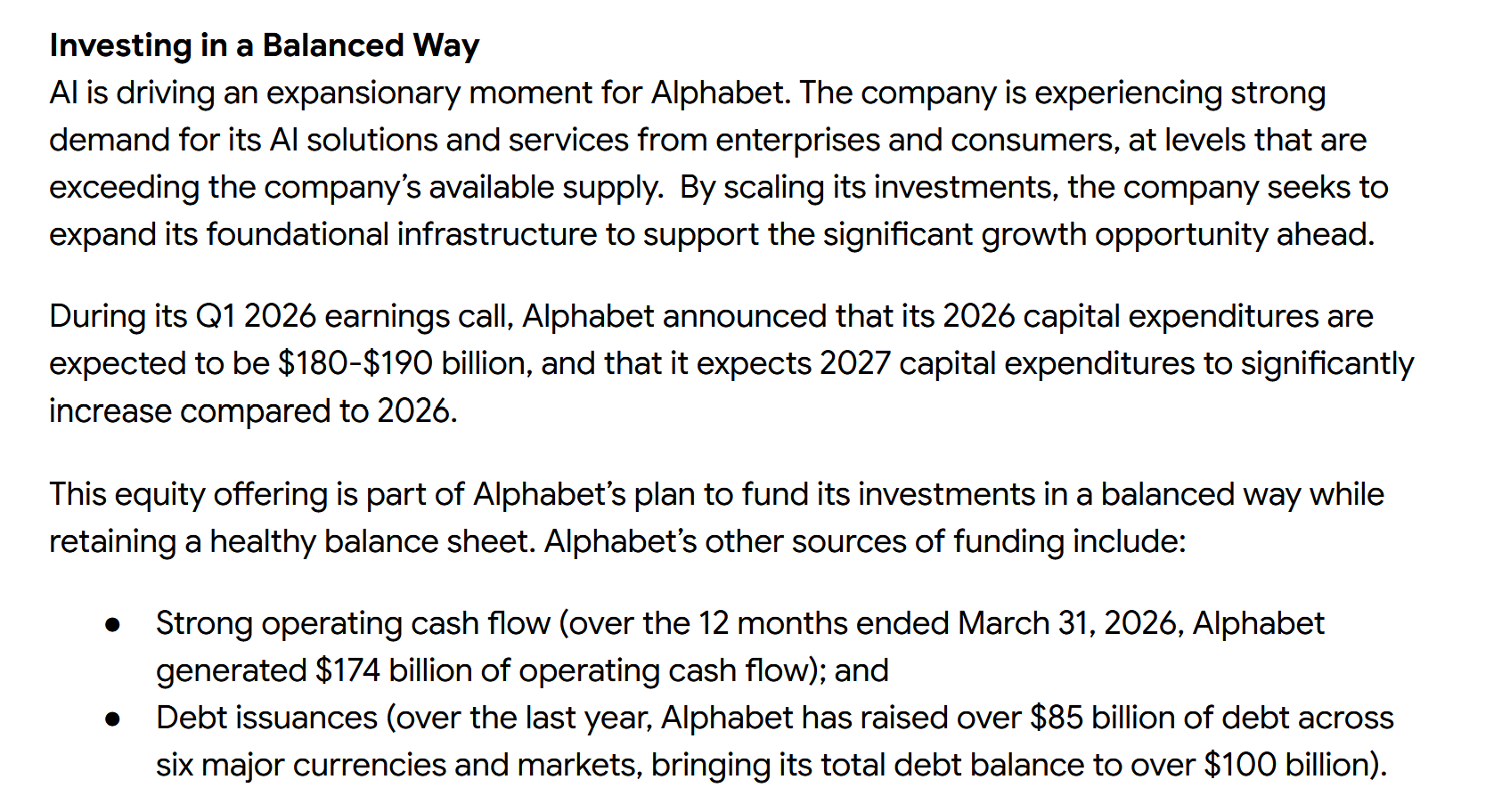

This is the main “justification” of Alphabet for the capital raise besides a 30 bn additional tax bill:

If you read this carefully, it is clear that they could still fund the 2026 Capex more or less with operating cashflow, but already in 2027, they plan to spend much more than that.

The really interesting thing is clearly: What are their plans beyond 2027 ? My best guess is that they plan with even larger investments that are not offset by operating cash flow.

But even so, why not wait until 2027 or so when they have a clearer point of view ? And I think here comes something into play which in my old Corporate Finance days was the golden rule of financing: “Raise when you can, not when you must”.

I think the Alphabet guys might have seen SpaceX’s announcement, they know that OpenAI filed for an IPO and that Anthropic will come to the capital markets as well.

As large as the listed capital markets are, there is only so much appetite for capital increases. Maybe they even fear a significant market correction which would require them to issue a much larger number of shares for the same amount of money.

Funnily enough, there were rumours that even Meta seems to think about raising large amounts of capital to fund their AI Capex programs.

One other factor that might also play a role here is that both, Private Credit and Private Equity which have been offering significant amounts of capital so far fight with redemptions themselves and are potentially overallocated to data centres already.

To me it is pretty unclear where all this is going. However one thing now is clearer to me:

The capital required to scale up this technology is larger than even the latest and best funded players like Google expected.

In my opinion, this means that it is very unlikely that we see 5 companies scaling this in parallel on their own (Alphabet, Meta, OpenAi, Anthropic & SpaceX). 1,2 or even 3 of those players might fold at some point in time or would need to collaborate really closely with someone like Microsoft or Apple to stay in the race. Or get help from the Orange guy in some sort.

Scrutinizing Data Centre Infrastructure orderbooks

For ordinary investors this might also mean to better scrutinize order books of companies that are supposed to profit from a further AI build out and trade at high multiples themselves.

At the moment, it is enough if a company releases “AI data centre” contracts to justify sky high multiples. I guess going forward, maybe even sooner than later, one really needs to understand from which counterparts those contracts are. Because not all of them might be actually turn out to be valuable.

In any case, as someone who loves capital markets, this is a great time to be alive and witness what is going on at the moment.