DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

Publishing research is a good way to get constructive feedback. With regard to my Norma Group Special situation post from earlier this day, one friendly person reminded me that there were at least two cases in Germany of big Buy back tenders in the past which had separable tender rights. I didn’t remember them, neither did Gemini.The two cases were:

In both cases, for every share you owned, you “only” got a “partial” tender right, i.e. for Rocket, every share got a right to tender only ¼ of a share. The Rocket internet case was very special, as Oliver Samwer “gifted” his tender rights to activist investor Elliott.

But the principle is clear: In order to tender more than your relative share, you had to buy additional tender rights. You canot just hope that someone doesn’t tender and you will then benefit.

So far, with Norma we don’t know if and how they will offer these separable rights, but this could change and require more active involvement especially when the tender rights are trading.

I just wanted to put this out. I have not sold or bought any shares because of this. I need to research the two cases and potential other cases more closely.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

Executive Summary:

Norma Group, a previously PE owned German manufacturer of small connector parts, is planning to use part of the cash it received from selling a division to buy back a significant percentage (>30%) of its outstanding shares via a tender offer at a premium of up to 20% compared to the current share price.

Although there are some moving parts and the overall case turned out to be more complicated than I thought initially, this represents a potential uncorrelated special situation for 3-4 months with an expected (probability) return of around 13% based on my assumptions.

Norma Group Background/Introduction

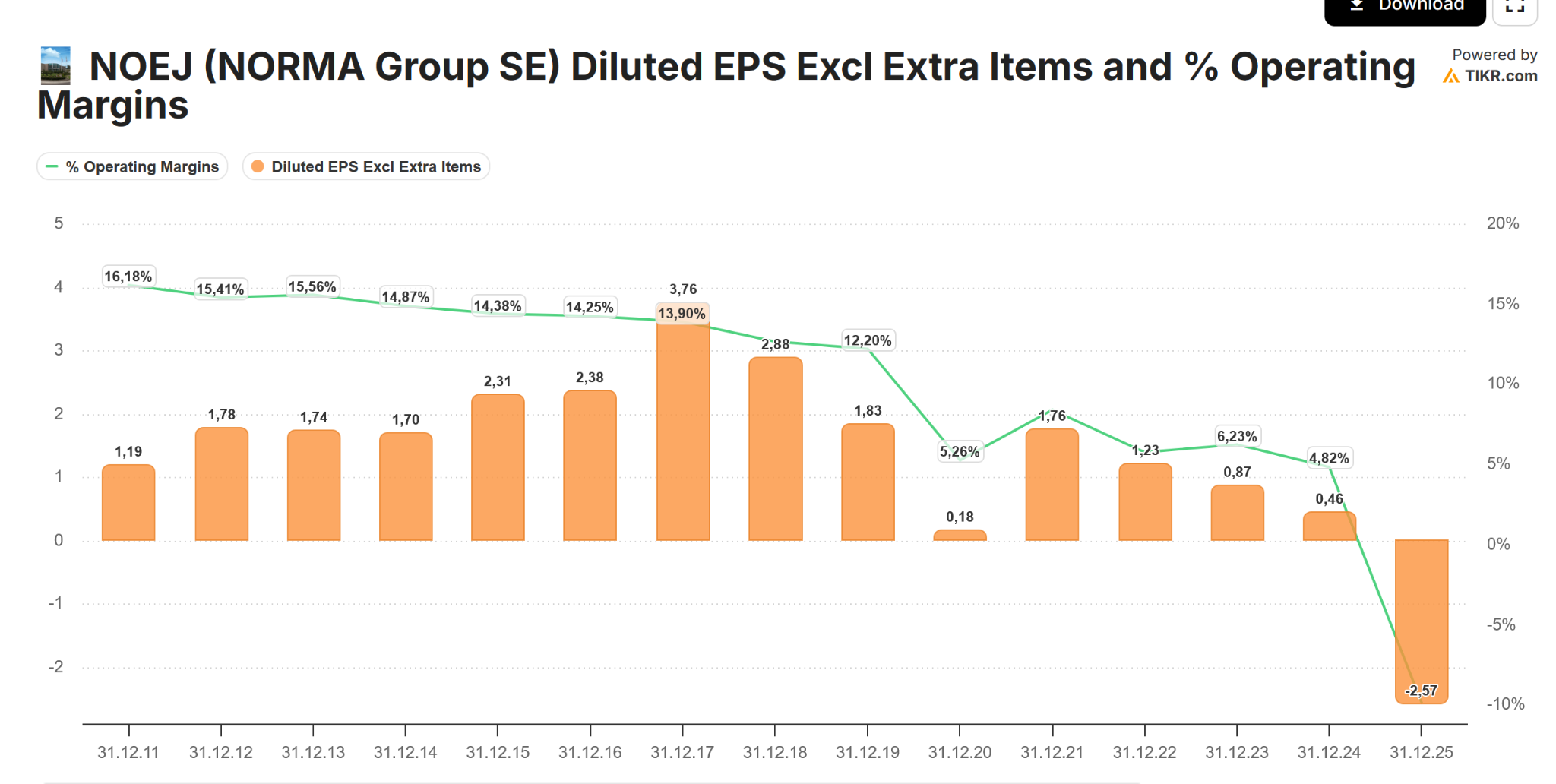

Norma Group has clearly seen better days. IPOed in 2011 as a previously PE held company (3I), the stock price did well until 2019 before then losing -80% when the stock price reached a low of below 10 EUR per share in early 2025:

Interestingly, according to TIKR, Operating margins had been on a downtrend since the IPO date and EPS peaked in 2017, but until 2019 no one bothered too much:

Norma was active in what they called “joining technology”, mainly connectors and other small parts out of metal and plastics for industrial applications, the car industry and “water applications”. Here a sample picture:

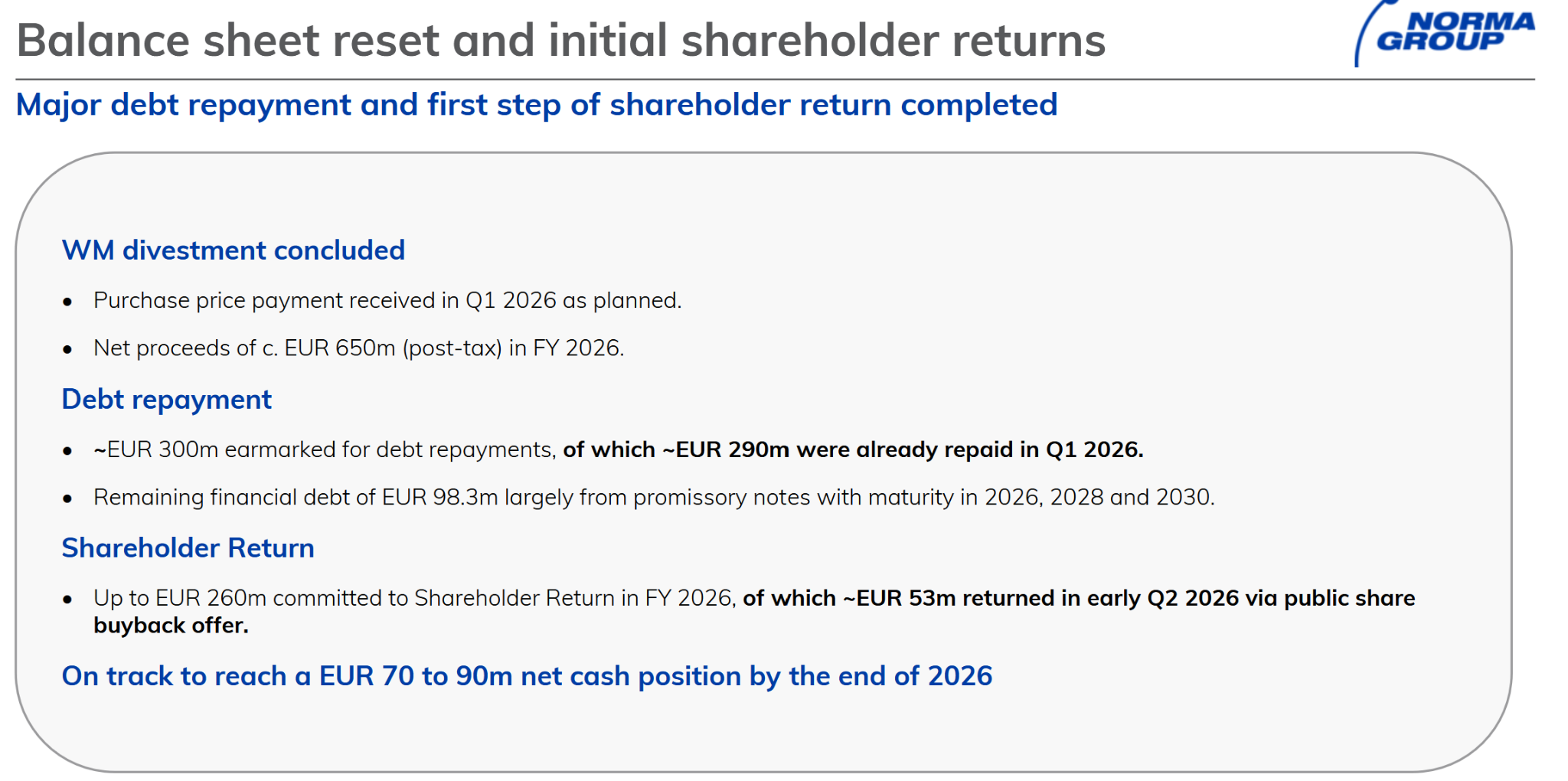

Norma said that they already paid back most of their debt and will keep 70 mn for investments into the remaining business and use the rest to buy back shares.

However, that only partially resolved the Excess Cash problem which leads us to this

The special situation: A 30% (plus) buy-back tender at a (up to) 30% premium

Three weeks ago, Norma announced a 208 mn EUR share repurchase tender at a premium of “10% to 30%” to a certain reference price.

Under German corporate law, in this case the AGM has to approve this decision before the board can formally issue a tender offer. The AGM will take place on July 1st in Frankfurt.

The long stop date for both, the acquisition and the cancellation of the shares is February 27th 2027

The buy back premium will be between 10% and 30% (the management board has signaled that they are going for 30%) compared to a certain “reference price”

The total amount that will be spent is 208 mn EUR in any case

Shareholders will receive a dividend of 0,14 EUR after the AGM in any case

That reference price is defined as follows

Initially I thought that this was referring to the date of the initial board resolution,which would have translated into a reference price of 15,62 EUR, but after an in-depth discussion with Gemini, I think it is the 90 day period prior to actually publishing the offer.

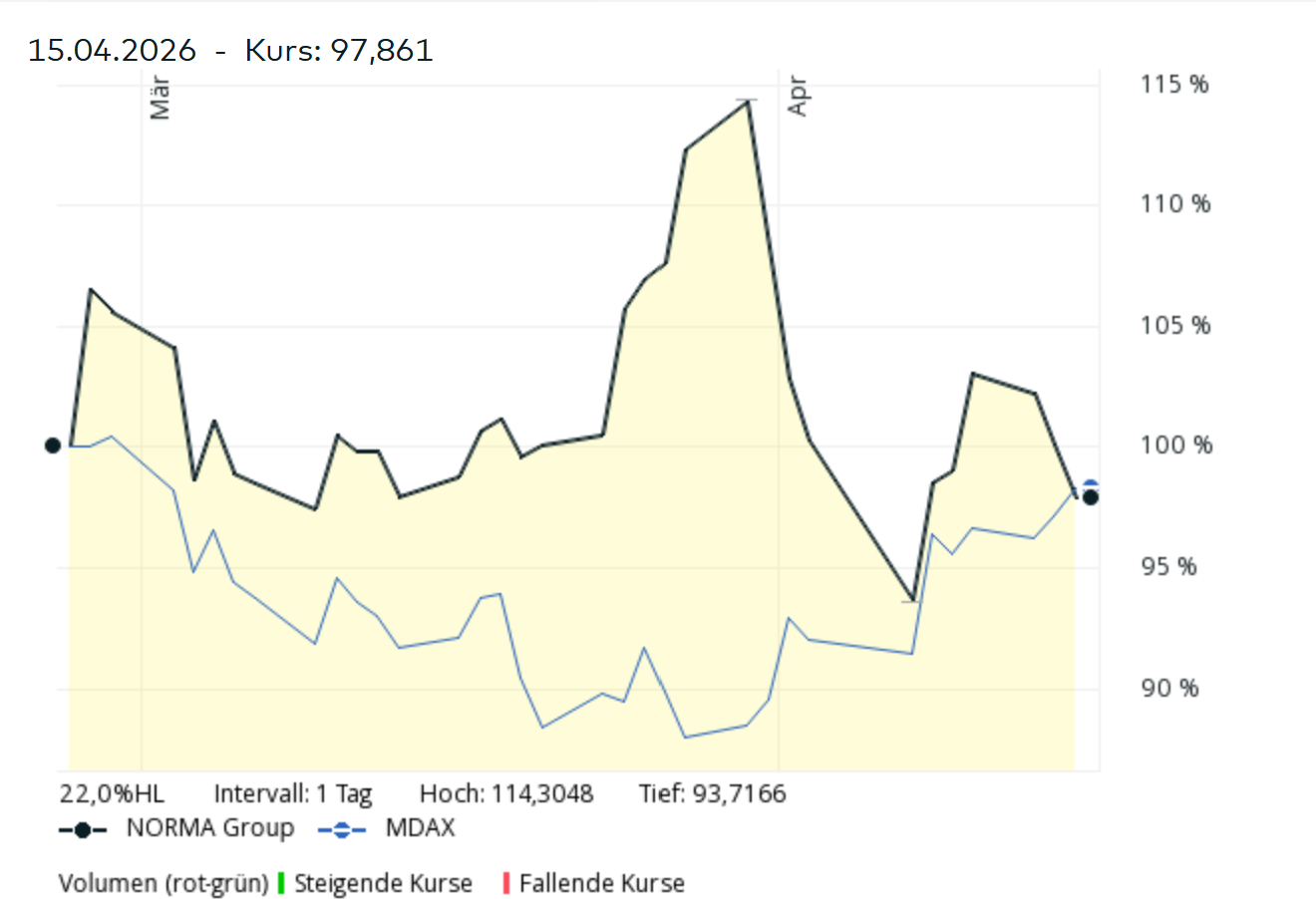

At the time of writing, the current 90 day average of Xetra closes is 16,09 EUR and increasing as long as the share price is at the current 17 EUR as we can see in this chart:

That the upper cap of the buy-back price is 20,87 EUR which is a “fair value” estimate by the Management

This is how this has been derived:

The Management Board has therefore, in preparation for the Capital Reduction proposed to the Annual General Meeting, commissioned a valuation of the Company in accordance with the IDW S1 standard as at 31 March 2026. This valuation resulted in an average value of EUR 20.87 per NORMA Group Share as at that date.

Looking back: How did the first tender offer in March work out ?

In March, Norma made a buyback tender for 16,59 EUR per share for up to 10% of the total share capital.

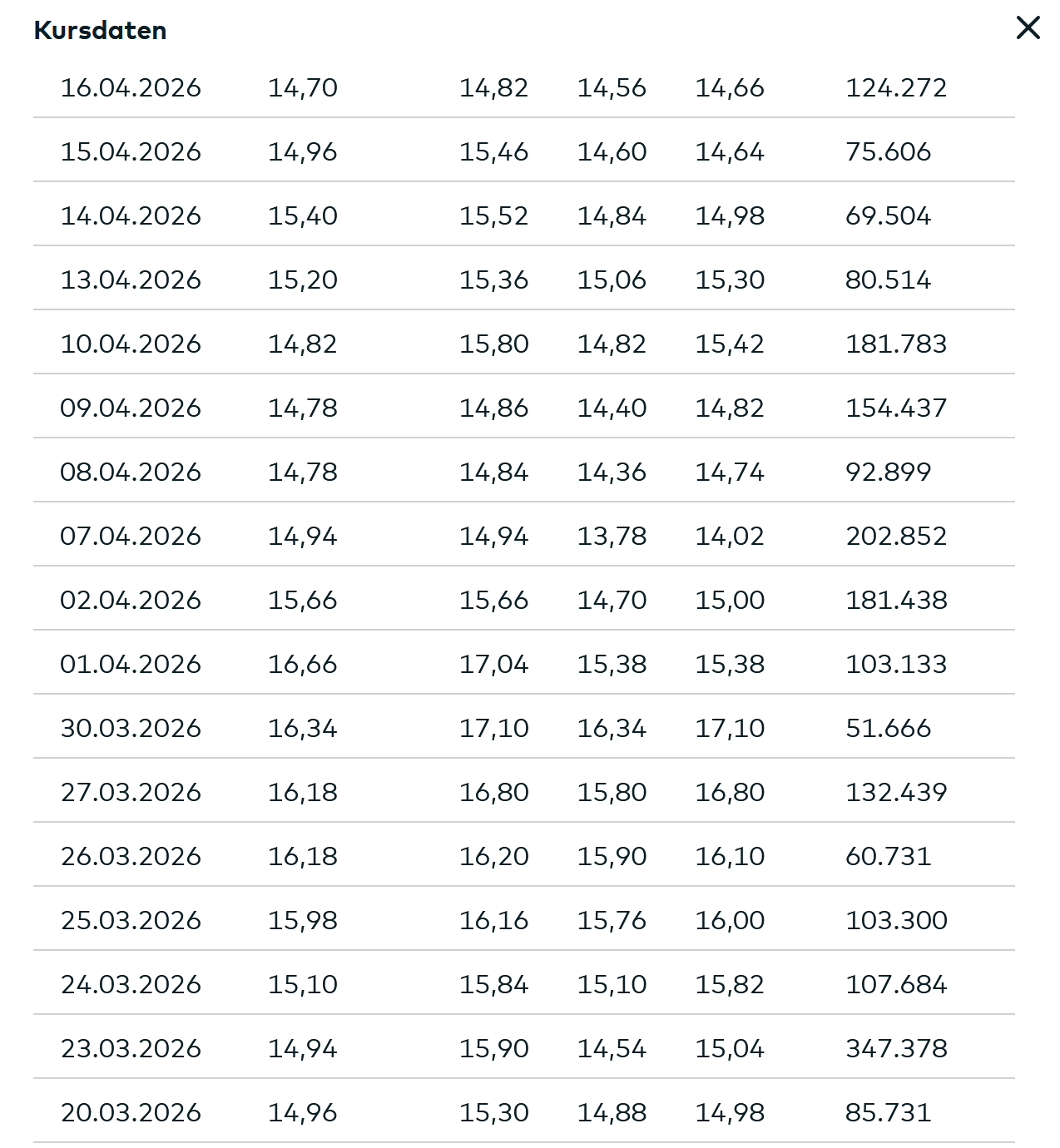

This was released on February 26th 2026. The closing price the day before was 14,92 EUR per share, so ~10% premium. The offer period ran from Feb 27th to March 27th.

Interestingly, 18,1 mn shares or around 57% of all shares were tendered, which is a lot for such a small tender with a relatively small premium. As only 10% of the shares were available, only 17,6% of the tendered shares were bought back. We will look at this later once again.

Interestingly, as we can see in the chart, the share price reached a high of 17,10 EUR on the day after the end of the tender period. One week later, on April 7th, the share price reached a low of 13,78 EUR, around -20% vs. the tender offer price:

Maybe that had to do with the release of the 2025 numbers on March 31st and the news that the CEO would step down.

The current Tender: What we don’t know

As I have outlined above, we know certain things about the tender already, but not everything. The main variables that we don’t know are as follows:

What will be the ultimate premium & share price at which the tender will take place ?

Although they state that the buyback will happen at a range of between 10-30% above the reference price, certain wordings indicate that they will go towards the high end. The most telling sign is the wording in the supplement to the AGM invitation

“The price clause described in section 2.2 enables the Management Board to offer shareholders a repurchase price closer to the intrinsic value of the share.”

For me, this is a very strong indication, supported by their largest shareholder, which will join the Supervisory board, that they will aim for the upper end of the range or close to their “fair value”.

Just to show the numbers:

With 16,09 as reference price, the low end of the range would be 17,70 EUR per share, whereas at the high end would be 20,87 (capped by the “Fair value”).

What will be the acceptance rate of the tender ?

If we assume the 20,87 as the ultimate tender price, this would translate into 208 mn/20,87 EUR = 9,97 mn shares which represents 31% of all shares or ~35% of all shares ex current treasury shares.

So if all shareholders tender fully, the minimum acceptance rate for every shareholder should be 35% (around 2x the acceptance rate from the first offer)

Another assumption is that Teleios, the 17,15% shareholder, will not want to lower their stake when they simultaneously join the board. So if we assume that they tender only 35% of their shares, we can assume that another 17,15-(0,35*17,15%)=11,2% of shares will not be tendered for sure.

This translates into a “worst case” acceptance rate of around 40% for the scenario with the maximum purchase price.

On the other hand, it is also very likely in such cases that not everyone tenders. I will solve this issue by creating several scenarios and weighting them with my subjective probabilities. More on this later.

At what price will one be able to sell the shares that are not accepted in the tender

This is clearly a tricky one, but it is also necessary to assume that one in order to be able to calculate an expected return for this special situation.

My assumption here is that one should at least get the current reference price of 16,09 EUR per share. I will share some thoughts on the potential value of the “stub” at the end of this post.

Actual timing of the offer

To be honest, I am not 100% sure how fast they can execute after the AGM approval. There might be some regulatory requirements (entry into the company registry) or maybe some of the usual suspects will try to blackmail the company with legal challenges.

But my assumption would be that the tender offer period starts in August and will be concluded in September. So from today, the time required for this to fully play out will be 3,5 to 4 months.

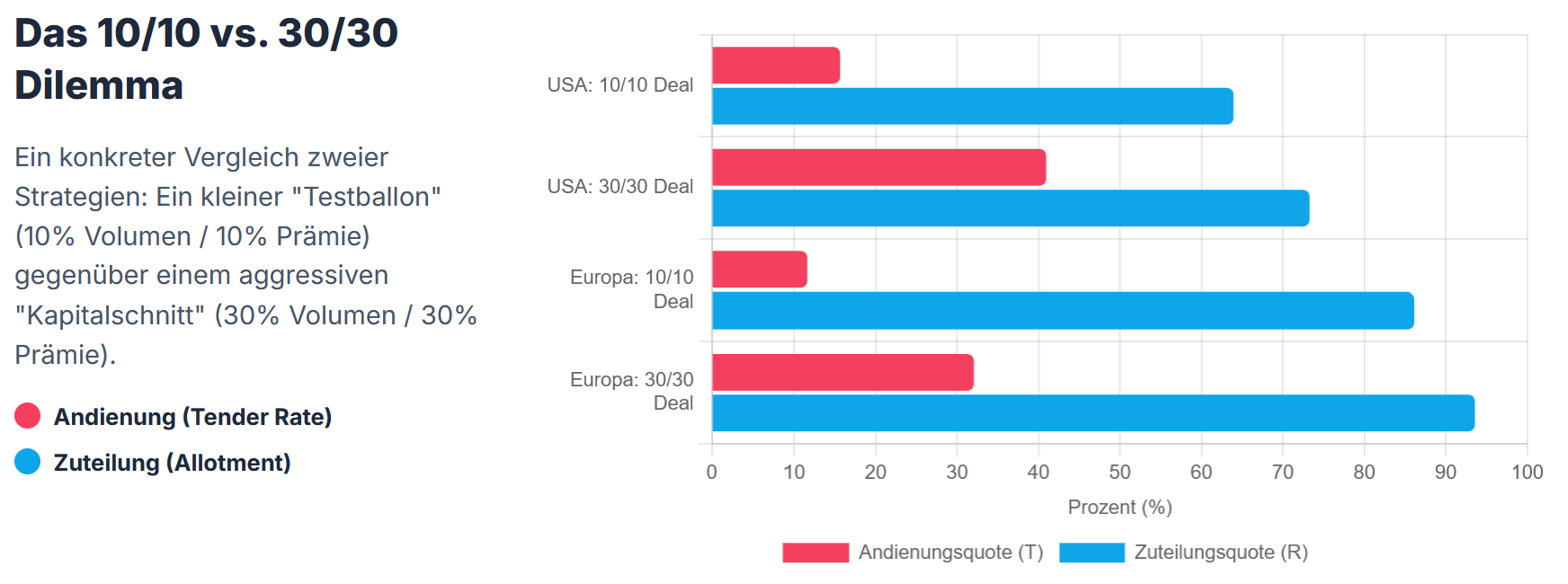

AI excursion: Analyzing the potential tender rate and resulting Acceptance rate

One main element that one needs to estimate is the percentage of shares that will actually be tendered. I have mentioned in the beginning, that in the first tender, 57% had been tendered with only 10% available, resulting in a relatively small acceptance percentage of 17,6%.

Based on empirical evidence, a higher premium increases the tender rate, but a bigger tender size relative to the outstanding shares increases the acceptance rate.

I asked Gemini to analyze tenders from the past years and estimate a regression. Interestingly, tender ratios are often quite low and acceptance rates much higher than one would normally think.

This is what Gemini estimated for a 30% Tender with a 30% Premium vs. a 10% Tender with a 10% premium both, in the US and Europe:

According to their regression, a 90% Acceptance/Allotment should be expected and only 30% of shareholders would tender. Now this sounds to good to be true and the first tender of Norma earlier seems to have been already a clear outlier.

So looking at historical data clearly helps but in any case one has to make one’s own assumptions for this case.

Overall; I do like to use AI models as a sparring partner especially in these Special Situations. Although one needs to get used to its “cocky” behaviour, I do think the discussions and additional analysis improve the process and hopefully, in the long run over many transactions, the outcome.

Return estimation based on a 30% premium to the reference price:

So now we have everything to estimate an overall expected return, of course based on all the assumptions I described above.

Here is my return estimate based on the 30% premium (capped at 20,87 EUR) and on a current share price of 17 EUR (including the dividend and 16,09 selling price for not tendered shares):

So 13,3% “expected return” over 3,5-4 months is not too bad given the current 2,25% short term interest rate in EUR.

Of course this is based on my assumptions that I have laid out above and different assumptions lead to different results.

Many of the uncertainties will go away over time such as:

The AGM will take place on July 1st. After the AGM we will know if someone wants to play games with the tender offer or not and how a realistic time table will look like

Once, the legal requirements are met, the management will formalize the offer and we will then know the actual premium

Finally, after the end of the tender period, we will know the final acceptance rate and then also the share price for the shares that can not be tendered

What happens at the low end, a 10% premium ?

This would of course be less attractive but one needs to consider the following: Norma intends to spend the full 208 mn, so the assumption here would be that they buy back more shares and the acceptance ratio will go up. The minimum acceptance would be 47%.

Also, there would be more value for the stub, but I will stick with the 16,09 EUR as selling price for the non-tendered shares. The probability of the acceptance rates also needs to be adjusted upwards.

Based on these assumptions. my return expectation looks as follows:

So at the low end which is basically almost the worst case, I would have a return of ~2% based on a current share price of 17 EUR. Only in the worst case, when basically everyone tenders, there would be a small loss.

So based on my assumptions, the situation looks like a pretty cheap “option” on a potentially higher acceptance ratio.

Some thoughts on the “Stub”:

If we assume that the tender gets through and that the shares will go back to 16 EUR per share, we will have a company that has around 18,7 mn Shares outstanding at a market cap of 18,7*16= 300 mn EUR if they pay the 30% premium

They plan to have a net cash position of 70-90 mn EUR by the end of 2026 according to their Q1 presentation, so EV would be between 210 and 230 mn EUR.

For 2026, Norma expects 820-830 mn EUR in sales and a 2-4% “adjusted EBIT margin” which would translate into ~16-35 mn in “adjusted EBIT”. At the midpoint, this translates to 25 mn adjusted EBIT or an EV/Adjusted EBIT multiple of 8,4-9,2x.

In the case of a 10% premium and a 16 EUR share price, the market cap would be ~270 mn EUR and EV/EBIT between 7,2-8,0 x EV/EBIT.

Not “dirt cheap” but not expensive either. In the second half of 2026, they plan to present a “2028 strategy”.

I think despite the relatively unexciting business, the valuation of the stub is cheap enough that I think that from a fundamental side, the downside risk is limited to a certain extent after the execution of the tender. Of course, if there is an overall market crash, no one cares about fundamentals anyway.

One important point here: For the time being, I am not planning to bet on a turn-around.

For me this is a Special Situation investment and I will exit once the tender is settled.

Technicalities:

This is an interesting detail from the invitation to the AGM

To the extent technically possible with reasonable effort, tender rights trading (Andienungsrechtehandel) is to be established.

The shareholders’ declarations of acceptance are taken into account according to shareholdings by tendering the tender rights attributable to the shareholding as well as any additional tender rights acquired from other shareholders.

So this means that there might be a mechanism that similar to a capital increase with subscription rights, in this case the tender rights might be split of from the shares and traded separately.

I haven’t seen this before and if this is implemented, it could create a special situation in itself, if those rights might trade higher or lower than the intrinsic value. So from that perspective there might be an additional “option” to improve the outcome

Timing option

As we have seen in the example of the fist tender, during the official tender period, the shares had already approached the tender price. Depending on how this is structured, I will definitely make sense to tender rather late in order to keep the option of selling the shares at a decent price before the execution of the tender.

If we have separate tender rights, then the opportunity will be mostly in analyzing the tender rights as mentioned above.

Summary:

At the current price of 17 EUR, I do think that the upcoming tender offer of Norma Group offers a decent return to park some cash for 3-4 months at an expected (probability weighted) return of 13% (not annualized).

Even at the low end, under my assumptions one would be able to make a 2% profit and the very worse case would result in a small loss (less than 1%).

For a special situation, I think there is also a lot of additional optionality baked into this whole process which in my opinion outweighs the uncertainties.

There are still a couple of moving parts and the tender is rather complex, so my overall allocation to this is rather small at 3% of the portfolio.

I will watch this very closely and I might increase the position if the price goes down or if new positive information comes in and the price stays low.

What I do like is that the risks are very specific and not much correlated to the overall market, which makes it attractive for the “opportunity” part of the portfolio.

I guess that also the complexity of the offer creates an opportunity here.

DISCLAIMER: This is not investment advice. The author might own, buy or sell shares without advance notice. The assumptions might be flawed or outright wrong. PLEASE DO YOUR OWN RESEARCH !!!!

DISCLAIMER: This is not Investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

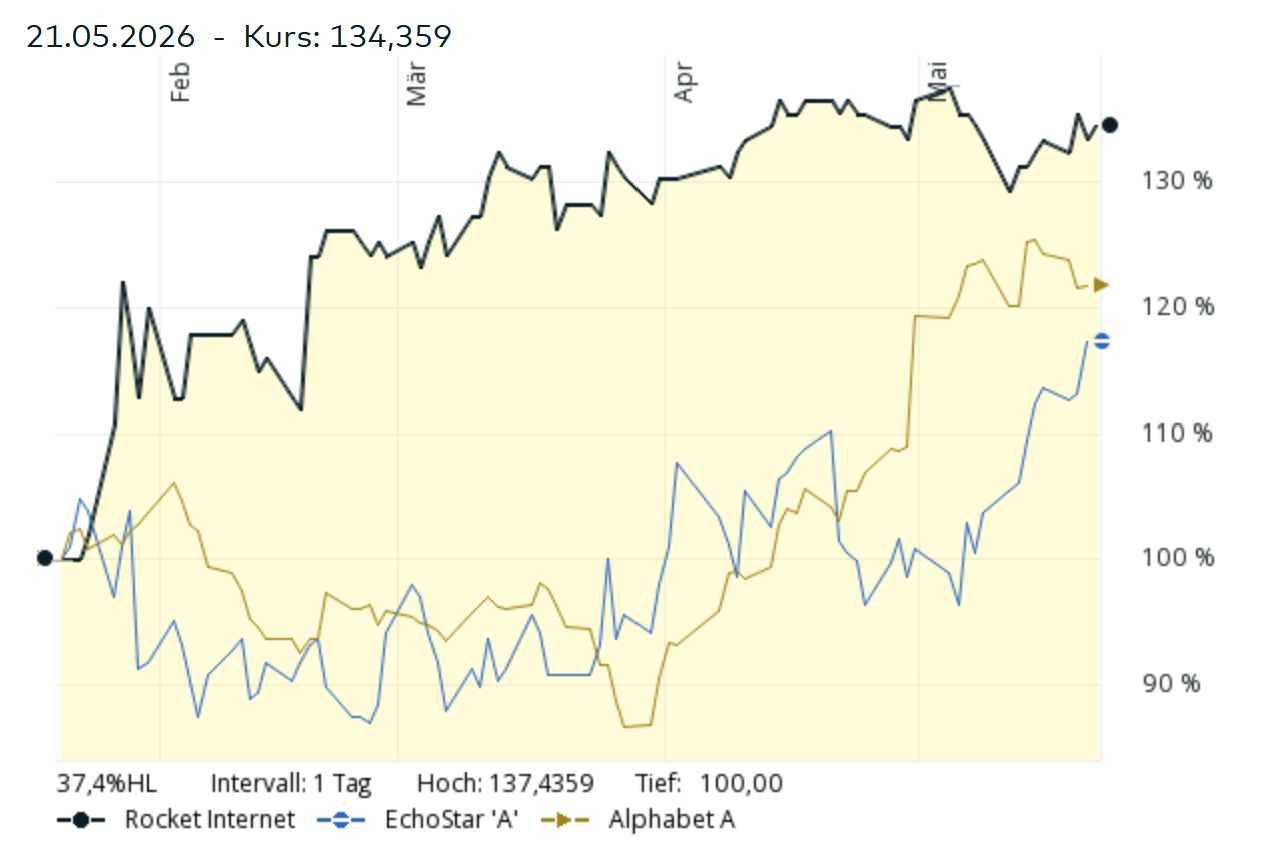

A lot has happened since I published my Rocket Internet write-up from the end of January. Just as a refresher: I found Rocket Internet interesting, despite some Governance issues as the “sum of the part” value was significantly higher than the share price back then and that it offered some relevant & discounted exposure to Elon’s SpaceX IPO.

But before we start, I would recommend to click on the following link and get David Bowie’s Space Oddity as a nice background sound for reading this post:

My time horizon for this would be either the (Rocket) AGM or the actual SpaceX IPO. On Polymarket,the odds are 60% for an IPO before end of Q3 2026

Compared with two other “SpaceX Proxies” that I mentioned, EchoStar & Alphabet, Rocket actually did quite OK if we look at the chart:

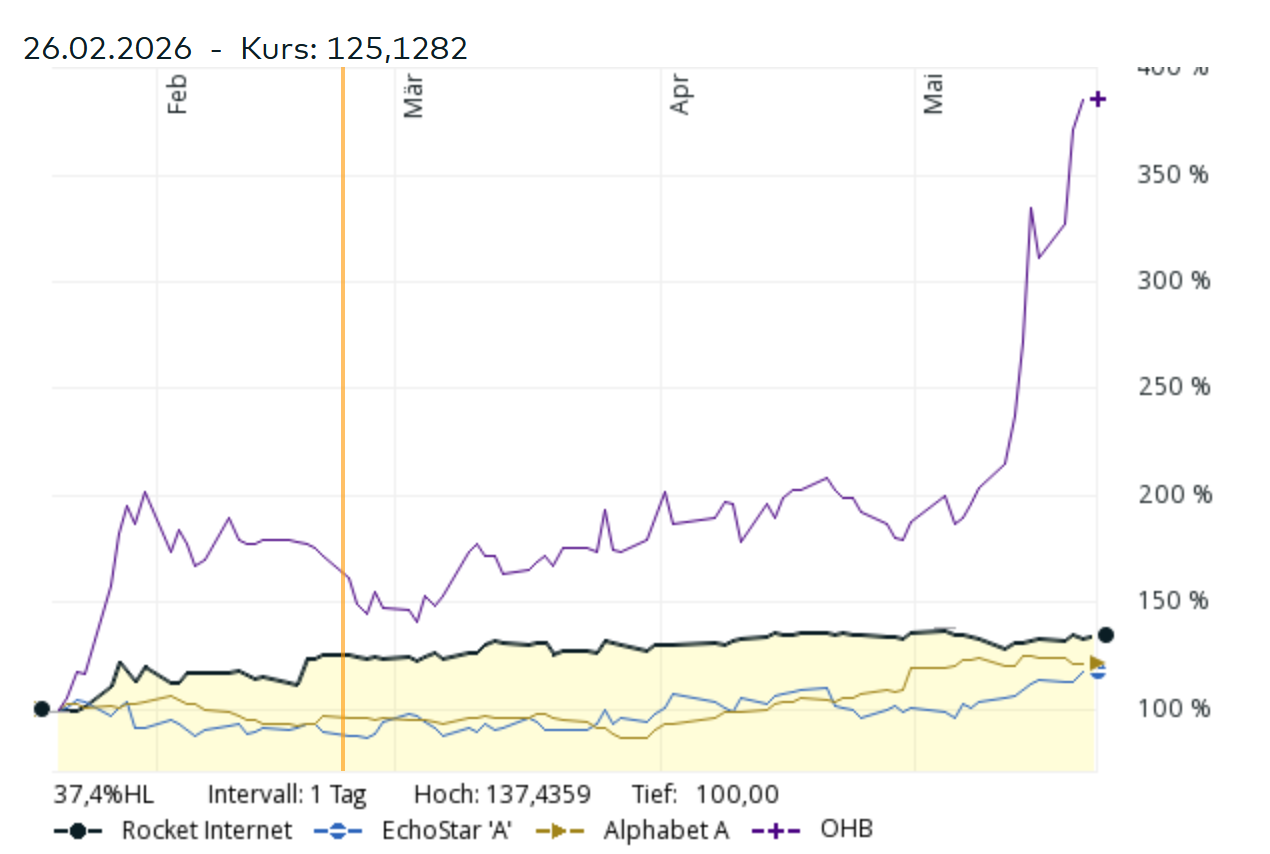

The real Space Superstar: OHB SE

However, the real “Performance Rocket” would have been another German stock called OHB:

OHB, a German/Bremen based Satellite manufacturer went parabolic despite having a really small free float after KKR acquired a significant portion of the minority free float at 44 EUR in 2023. Initially they wanted to delist but then kept the listing.

The main reason for this increase seems to be that OHB is included in a very popular ETF called Tema Space Innovators ETF with the great Ticker NASA.

This ETF is one of the fastest growing ETFs ever and currently has a 5% allocation in OHB. At around 1,4 bn AUM, that’s around 60 mn EUR in OHB. As most of the OHB shares are held by the founding Fuchs family and KKR (together ~94%) and some specialized “Squeeze out” players, there seems to be a pretty hard squeeze on the few remaining shares.

I also guess that you cannot short OHB shares. Operationally, OHB has been doing okayish, but nothing that would justify a 130x P/E.

In any case, this is a monster deal for KKR who (obviously) plan to exit while its “hot”. I am pretty sure that after that exit, OHB will be one of those “Christmas Tree” charts that we know from the Covid times.

Back to SpaceX

Elon seems to target a valuation of 1,75 tn USD, that would be the upper range of what I assumed in my January sum-of-the part valuation. However, “old” SpaceX shareholders from the beginning of the year have been diluted by ~20% after the “merger” of SpaceX with XAi, so we have to take this into account.

I am sure that Matt Levine will write and say much smarter things than I do about the SpaceX IPO, so here are just some observations:

The S1 prospectus contains some really nice pictures of rockets

Overall, SpaceX is clearly much more resembling a giant “Elon Venture Fund” than a normal company. I think I read this in one of Matt Levine’s newsletters about Tesla. Elon has assembled a relatively loosely connected group of companies (XA, Twitter, SpaceX, Starlink, maybe Cursor) with which he can more or less credibly jump on any new hype that will come his way.

Like the VC giants Sequoia or A16Z, he has two talents: To raise funding and to attract (a certain type) of tech people with which he can at least create the appearance of riding the next big thing.

If Ai hits a brick wall, Elon finds something else like maybe Quantum computing or he will merge Neuralink into SpaceX or become the Number 1 in obesity pills.

His hardcore fans are not looking for earnings but to ride the next hype

A lot has been already said about the “total Addressable Market” figures from the deck which equal the US GDP.

The great thing about both, the socalled “Space economy” and also AI is, that both at the moment seem to have indefinite TAMs. Mathematically, even a small slice of something indefinite is worth an indefinite amount of money.

So that’s clearly much better than something like earth bound EVs where there is a clear ceiling or humanoid robots that just don’t work and where the Chinese are obviously much better.

I am pretty sure, Cathy Wood or someone similar will come up with an “analysis” that SpaceX is worth 100X from wherever it is trading.

A nice contrarian take can be found at the “Wertegang” Substack with the nice title : SpaceX is a Zero. Here, my friend Dirk argues that the SciFi bestseller “The three body problem” clearly shows that reaching to the stars is pretty risky from a cosmic perspective (Dark Forrest theory). But I am pretty sure that if needed, Elon will also promise to manufacture Pocket Universes in one of his Gigafactories.

What I am really curious about is, if Elon manages to really hype two companies, Tesla and SpaceX at the same time. Also, how will the typical “Elon retail hardcore supporter” react ? If he/she is a real Elon fan, he/she will have all of their money already in Tesla (plus maybe some more). But of course, they want to have SpaceX exposure, too. So will they sell their Tesla shares to get a 50/50 allocation ? I think this will be interesting to observe.

Anyway, the SpaceX IPO is great financial entertainment and might only be topped by an OpenAI IPO in autumn.

Rocket Internet Update

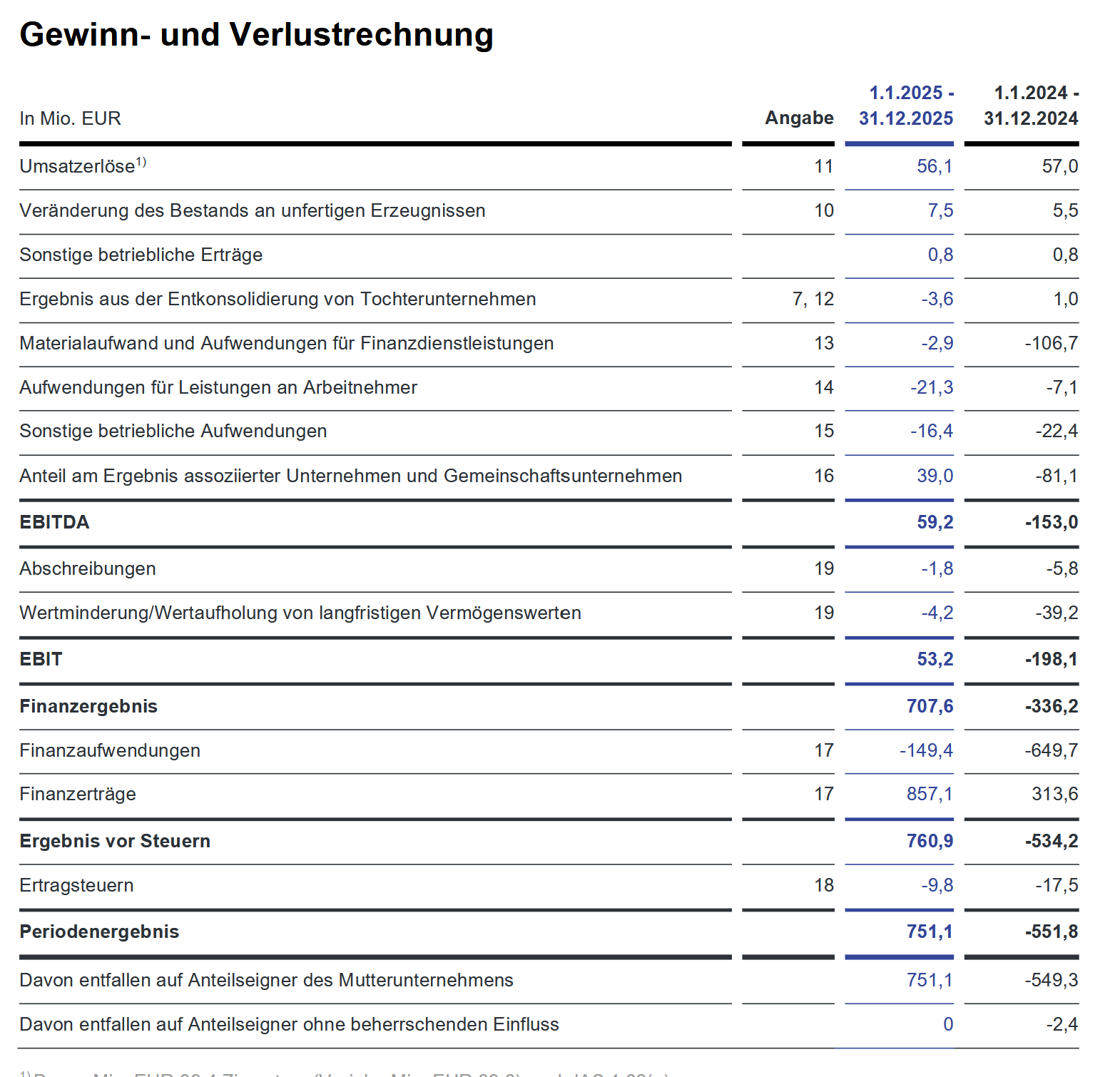

In the meantime, Rocket Internet has “published” its 2025 annual report. Interestingly they did revaulue their participations upwards to a certain extent. After a loss of -550 mn EUR in 2024, they now show a profit of 750 mn EUR. It seems that the letter from Scherzer AG to the auditors did have some effects.

If I would be in the Microcap Stock promotion game, I would maybe post something like: “Hidden Perfromance Rocket trading below NAV at 3x P/E ratio”, but economically the shown profit is pretty meaningless.

On the negative side, there will be no large cash distribution and Rocket seems to intend to make the company even less transparent going forward.

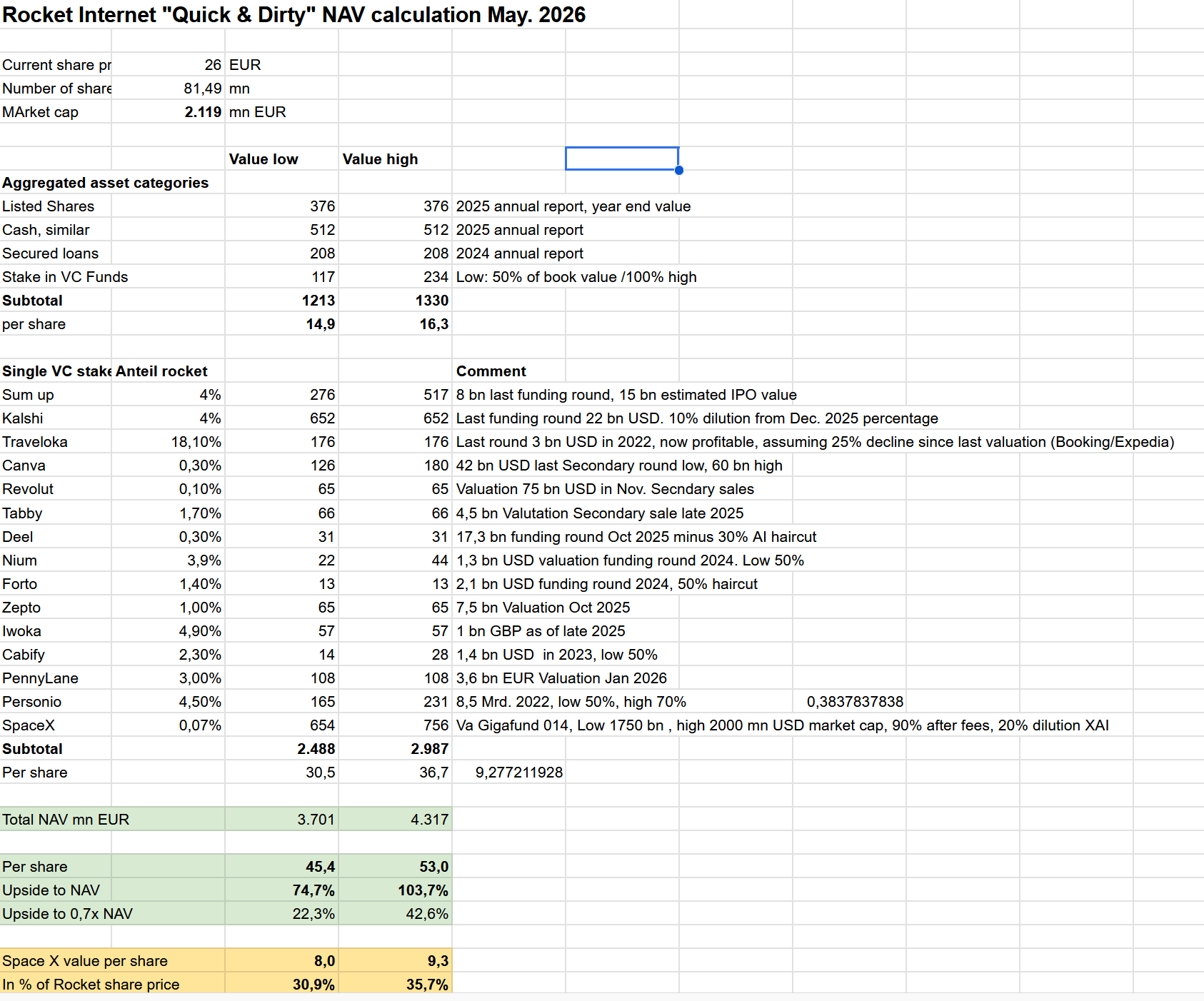

In any case, I updated my valuation sheet, including some “bug fixes”. Again, this is a quick and dirty exercise and definitely not investment advice !!!

Here is the new sheet:

The main changes that I made were some haircuts on Software companies andTraveloka and adjusting Kalshi and SpaceX for the most recent values. For SpaceX I incorporatedthe 20% dilution from XAi and a new range of 1750 to 2000 mn USD as valuation. For Kalshi I used the 22 bn valuation and implying a further dilution of 10% from the YE 2025 number.

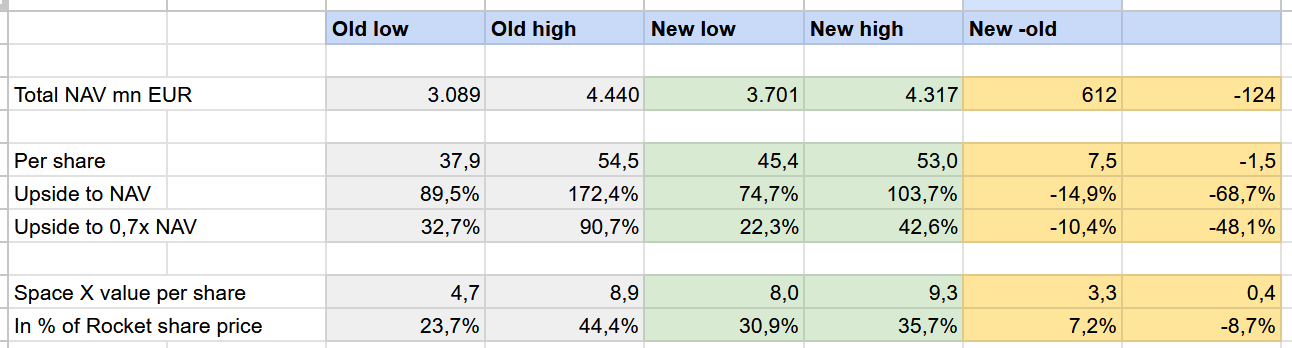

This is a quick comparison between my old and the new exercise:

We can see that the Upside NAV is more or less the same at 53 EUR per share vs. 54,5EUR despite the “haircuts” applied to Software, but the downside valuation is singinifcantly higher, mainly because of the expected valuation of SpaceX at theIPO and the recent Kalshi round which was only a rumour in January.

The upside to the NAV is of course lower, as the shares gained ~+30% since the write-up.

As mentioned in the beginning, I will keep the shares until the IPO hoping for some more irrational exuberance around the SpaceX IPO. Unless I’ll change my mind earlier 😉

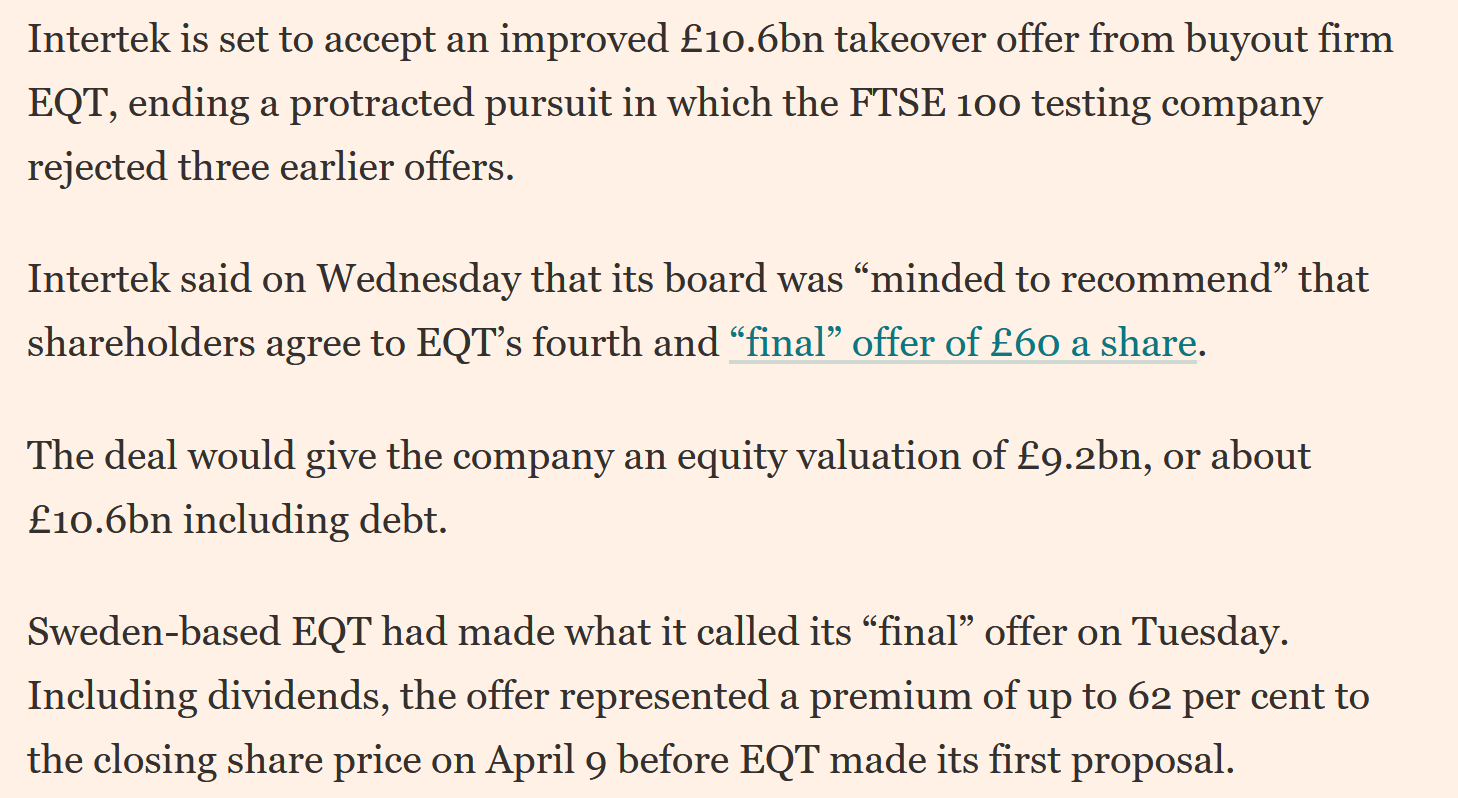

A little bit similar to DCC, EQT tried at first a low ball offer, but had to increase that offer 3 times within a time frame of ~ 4 Weeks.

This is how the bids developed per share

1st April 10th: 51,50 2nd: 54,00 3rd: 58,00 4th May 13th: 60,00 plus 1.07 final dividend accepted

So from the first to the final bid, the bid price increased by almost 20%. Interestingly enough, after rejecting the third bid, EQT threatened to walk away but obviously didn’t.

What I find quite interesting is, how volatile the share price behaved after each rejection, it traded down significantly below the bid price after each round.

Another interesting point to mention is that at the time of writing, the Intertek share price trades more than 10% below the bid price. A certain discount is normal, but this looks quite wide as I do think that the deal is relatively certain to close.

So Intertek might itself be an interesting “Merger Arbitrage” situation.

So what does this mean for DCC ?

Looking at how things worked at Intertek, one should expect some volatility around further bids from KKR and maybe several rounds of rejection and threats to walk away.

I would expect that, as with Intertek, an overall 20% uplift on the initial bid would do the trick which would be an offer of ~70 GBP/share. For anything below that, most shareholders would just point at Intertek. But as in the Intertek case, one should not expect that DCC will then directly trade up to the bid price.

If the DCC price overshoots my 70 GBP target in between, I would maybe sell a part of the position.

Disclaimer: This is not investment advise. PLEASE DO YOUR OWN RESEARCH !!!!

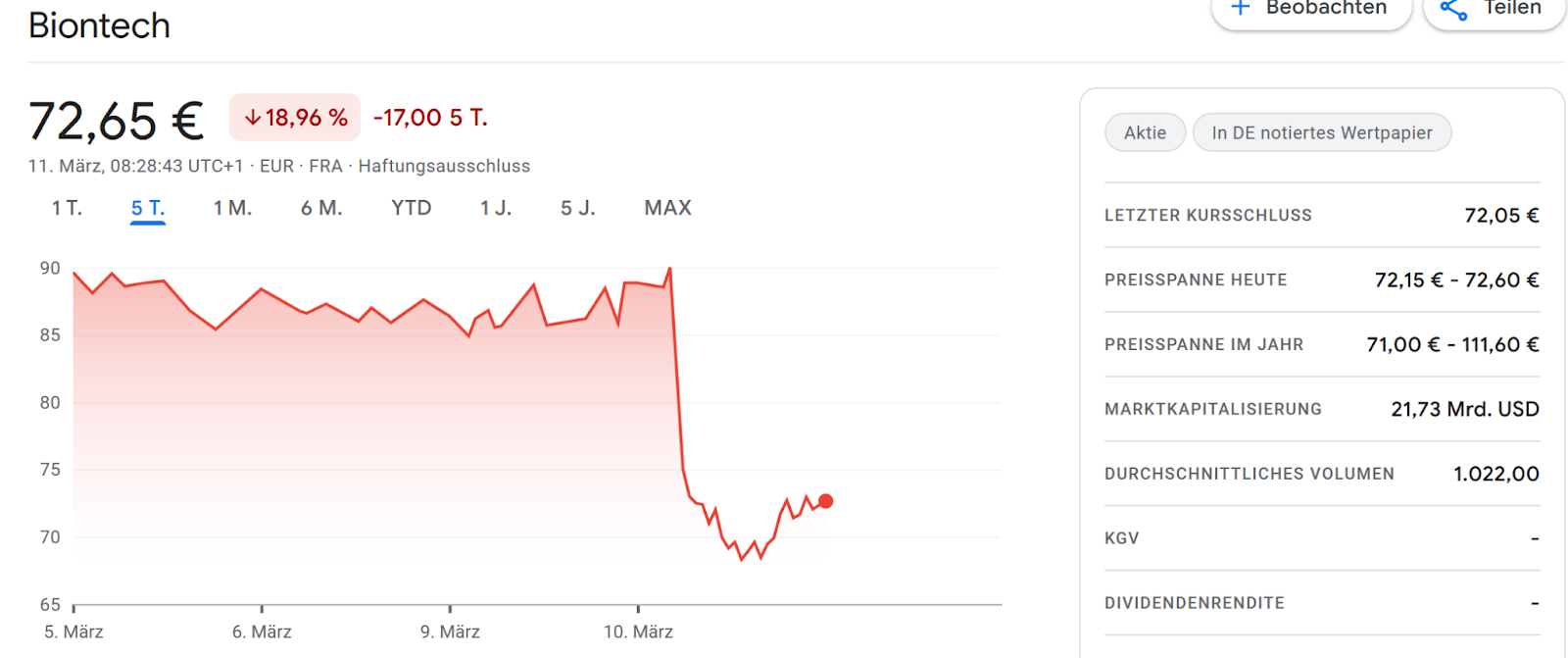

I wrote this post this morning (CEST) when the stock price was around 73-74 EUR. I then had to run some errands before being able to post and the stock price moved already significantly. All calculations etc. are based on a stock price of 73,50 EUR.

Now two things happened yesterday on March 10th, when they were supposed to talk about Q2 earnings:

The two founders announced that they will leave by the end of 2026 in order to start a new company

The share price dropped significantly after the announcement

This is the stock chart in Germany (in EUR):

After a low of around 68 EUR, the shares currently trade at 73-74 EUR at the time of writing.

Funnily enough, this is almost exactly the current net cash per share and even 10% below my “worst case” assumption:

Using my “old” scenario, the potential upside would now be obviously a lot higher.

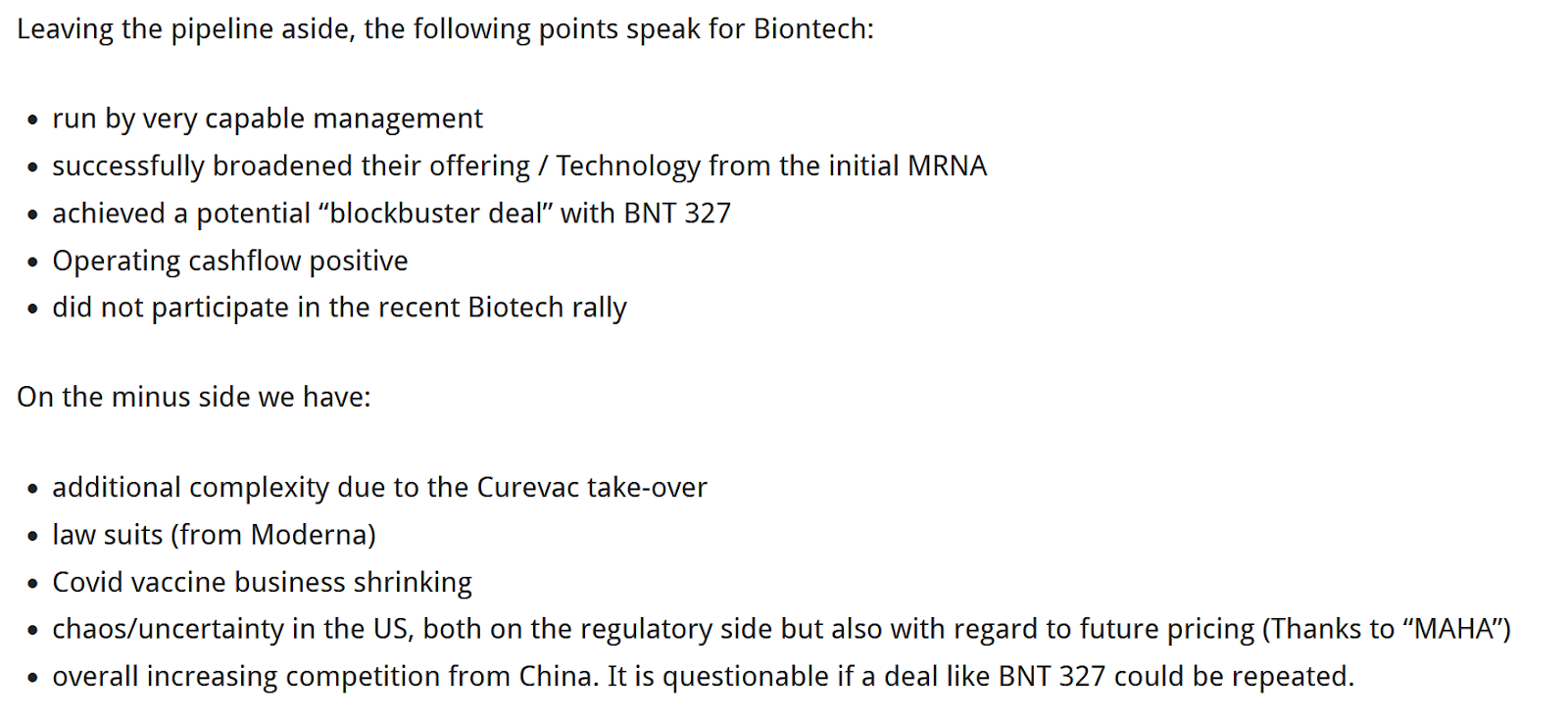

But, and this is a BIG BUT: With the founders leaving, one of the main qualitative arguments became a lot weaker. This was my Pro & Con list back then:

We just don’t know who will run the company from next year onwards. Initially this was a big negative news for me.

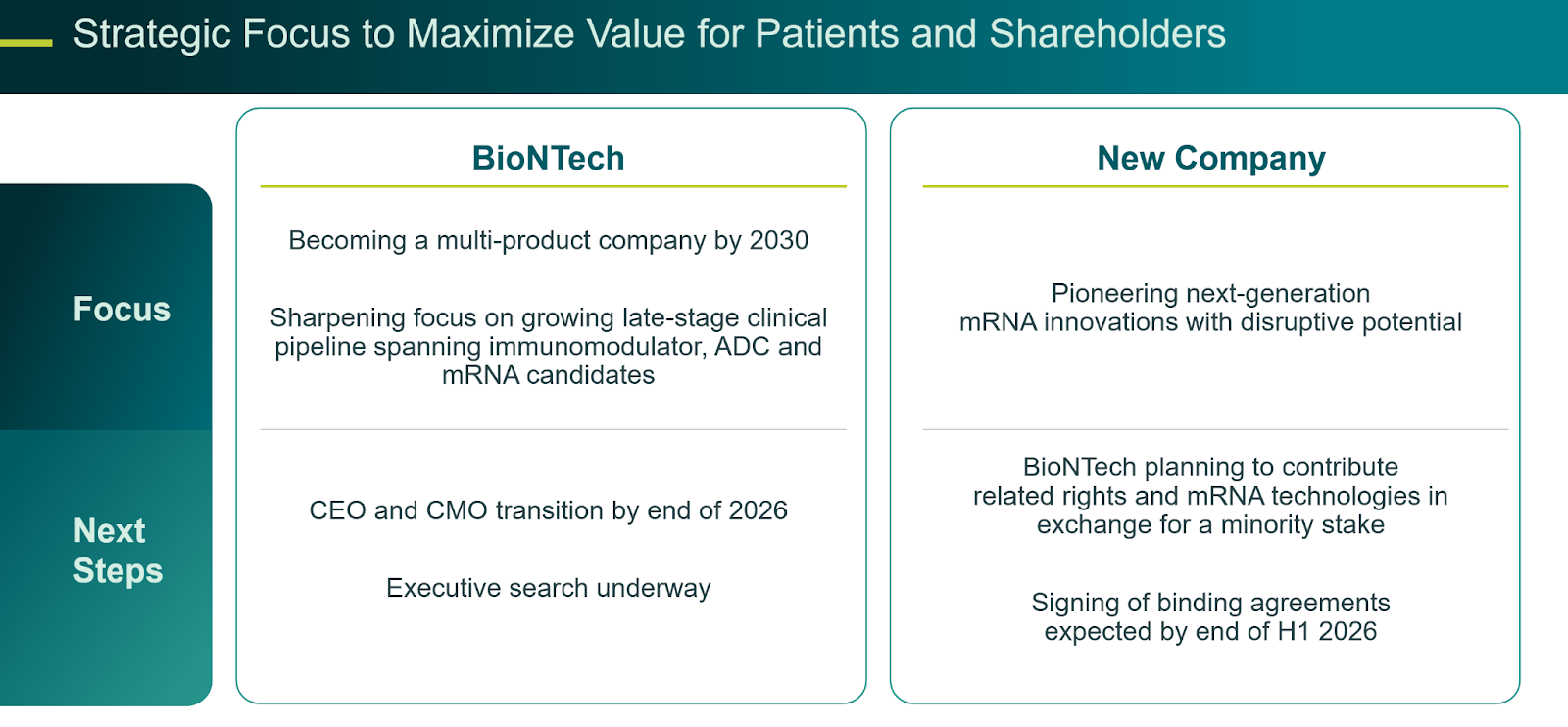

So Sahin and his wife will leave by the end of the year and basically take some (or most ?) of the mRNA technology in exchange for a minority stake into a new company. We do not know if they also get cash or not. I would assume not.

Normally, one sees such “deals” only after a Biotech company is taken over by a big Pharma company and a founder wands to make sure that early stage projects are not getting killed.

One such situation was the Actelion/Idorsia Special Situation I invested 9 years ago, where after the take-over of Actelion by Johnson & Johnson, the founder Clozel took the whole development department including the early stage pipeline into a new company called Idorsia which was then spun-off to shareholders.

Interestingly, Idorsia, even after 9 years didn’t do too well and trades significantly below the value right after the spin-off:

In the German press, there are some rumors that the founders have made that move because a sale of Biontech to a bigger Pharma company might be imminent, although officially the founders have said this is not the case.

What I find most striking is the issue that they haven’t announced a successor for the founders yet.

Without a potential sale of Biontech on the horizon, the founders could have just “hired” or promoted someone to CEO who takes care of commercializing the late stage pipeline and continue to do their research within Biontech.

I get the impression that maybe, after 18 years, the billionaire Strüngemann Brothers who put up the initial funding and still own 40% do not agree anymore with the founders who own around 15%. In some older articles, both the Strüngmanns and Sahin always made the point that they want to create a “full blown” BioPharma company that can play in the first league internationally.

At least Sahin and his wife now decided that they actually prefer to do research.

Another dicey issue is that the founders will basically negotiate the transfer of the mRNA technology with themselves as they want to close this before the end of the next quarter, maybe specifically before a new CEO is installed. My impression is that they are honest people and really interested in research, but it is of course not ideal if they negotiate with themselves.

Also the announcement that Biontech will only get a minority share seems to indicate that this time, Sahin and his wife want to have the full control which they currently don’t have.

It will be also interesting to see if and how many of Biontech’s R&D staff will follow them to the new company.

What is the worth of a charismatic founder ?

Yesterday’s announcement is also an interesting datapoint regarding the question: What is the worth of a charismatic founder? In this case, for most shareholders, the announcement was clearly a big surprise.

The -20% clearly indicate that at least in the short term, investors think that the company is worth less without its founders.

So what about Biontech now ?

As I mentioned in the beginning, the share price is now around -25% lower than in January. On the other hand, without the founders, a lot of things could be more difficult, especially if a lot of people follow them to the new company..

As a compensation, the possibility of a take-over/sale of the company to a large international player has clearly increased, I would assume that in the case of a takeover, the pipeline value would be paid to a large extent by an acquirer.

I have asked various versions of LLMs who the most likely acquirer would be. The favorites were Merck (US), Bristol Myers (with which they partnered) and Roche. All of them could make use of Biotech’s pipeline and have the means to do the transaction.

I also think that once the mRNA deal is signed, a subsequent sale of the company could happen rather sooner than later.

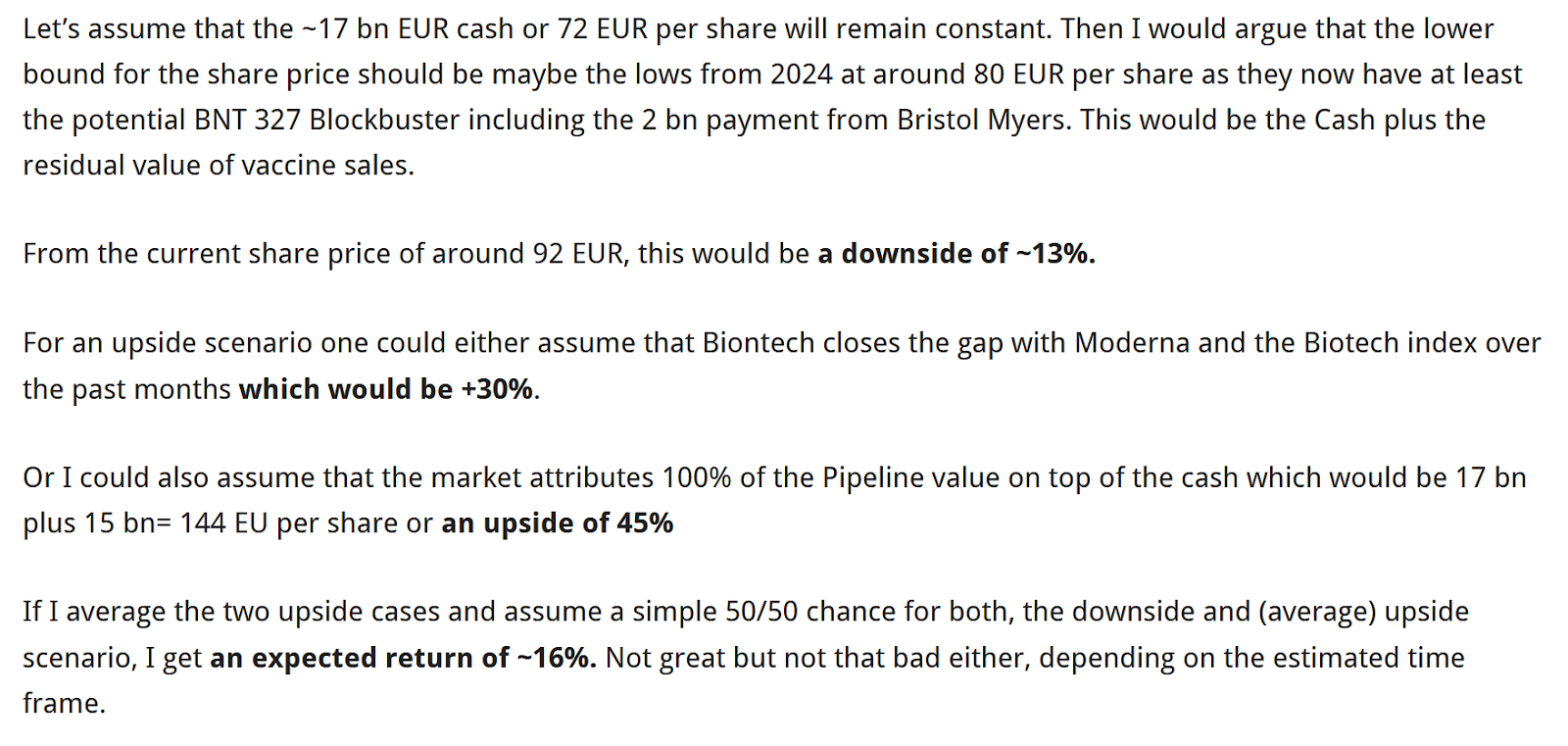

New scenario:

My new downside case would be 80% of net cash which is a level that many loss making Biotech firms trade at.

My upside scenario would be the 144 EUR with the pipeline value from the last post.

If I use a 50/50 scenario this would translate into (-20%+100%)/2= +40%

That looks a lot better than in January.

Of course anyone could add a lot of other cases but I like to keep it simple.

There is still the issue that we don’t have a “hard” deadline for a potential deal, but on the other hand, the year end deadline for their exit could be interpreted as a deadline for the Strüngmanns to find a buyer.

Playbook:

My assumption is that this situation doesn’t escalate totally between the founders and the Strüngmann brothers. One big warning sign and red flag would be, if the agreement for the new company would not be signed until the end of June.

Summary:

In a nutshell, Biontech now looks much more like an interesting “Special situation” than in late January.

Yes, the founders will be gone by year end, but the stock is 25% cheaper and we now have a “soft deadline” for a potential M&A announcement.

My “back of the envelope” calculation indicates and expected average return of 40% for roughly one year which is attractive. I therefore allocate 1,5% of the portfolio into Biontech at current prices of 73,50 EUR/Share.

Bonus Soundtrack:

I imagine that the founders will play that Soundtrack if the walk into their new company in 2027: Jon Batiste – Freedom

HEALTH WARNING & DISCLAIMER This is not Investment Advice. The stock discussed in this post is a “Pink Sheet” OTC stock with limited liquidity and almost no reporting. The author may own, buy or sell shares in this company without pre-warning. DO YOUR OWN RESEARCH !!

As a change to previous write-ups, I will start with the sound track for this write-up. And of course it is “Rocket Man” from Elton John. It fits in more than one way to this Special situation and you maybe want to listen to it while reading the write-up.

As again, this write-up became a little bit longer, I’ll just show the “elevator pitch” here but will embed the PDF document.

0. Elevator Pitch

Rocket Internet AG, a former German Venture Capital super star company run by the Samwer brothers has gone “dark” and delisted in 2020. Since then, the stock price languished until more recently, when a German activist sent an open letter to Management and the auditors criticizing the “low balling” of accounting numbers. Diving a little bit deeper, some true gems are hidden in Rocket Internet’s portfolio, especially a participation in SpaceX and prediction market superstar Decacorn Kalshi. The current share price reflects most likely less than 50% the current NAV. In my opinion, the upcoming SpaceX IPO and further positive development of Kalshi could maybe act as a “catalyst” and lead to a higher share price. In addition there is a (low) chance that Rocket Internet might distribute another special dividend as they did in 2024.

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!!

Background:

Bombardier is a Canadian company that after a colorful past as a conglomerate and an “almost bankruptcy” in 2020 is now fully focused on manufacturing Private Jets and until recently has been a poster child of a very successful turn-around. My friend @Govro12 from the Wintergems substack has written a very nice post on Bombardier just a few weeks ago which I highly recommend to read.

High level Presentation:

Although I only could convince myself to buy a small starter position (<1%, to keep me interested), I presented Bombardier as a potential interesting investment case in a private investor meeting some days ago. Here is the presentation which I admit is pretty high level. Spoiler alert: I would not recommend to invest right now.

Disclaimer: This is not investment advice. The guy who is writing this has problems distinguishing USD and GBP. PLEASE DO YOUR OWN RESEARCH !!!

A friendly reader alerted me that I made an error in the Ocean Wilson Special Situation NAV calculation. I seem to have gotten confused by the fact that Ocean Wilson reports in USD. I did translate the Wilson and Sons stake into GBP but not the investment portfolio. Instead of 319,6 mn GBP, the investment portfolio is worth 319,6 mn USD which equates ~ 239,7 mn GBP

So the initial calculation should have rather looked like this:

The expected return is a full -8% lower than inititally (and wrongly) calculated. Still not bad, but clearly less advantageous.

Based on this, I reduced the positon to a ~1% position.

I am deeply sorry for this mistake and a big thanks to the reader who alerted me. Going forward I will need to be more dilligent for these calculations-

One other remark: A reader congratulated that my post has moved the stock price. This is not my intent for the blog. I try to avoid writing about illiquid stocks as some readers tend not to read the posts and seem to blindly buy. With Ocean Wilson, I was very surprised how illiquid this 500 mn Market cap stock actually is. For me this is a good lesson for the future that I don’t write much about illiquid stocks. I leave that to others.

Disclaimer: This is not investment Advice. Never trust an anonymous dude on the internet. DO YOUR OWN RESEARCH!!!

As always, I have attached a pdf with the full writeup and only focus on a few sections in this post. And the Sound Track of course.

Elevator pitch:

Ocean-Wilsons, a UK listed, Bermuda domicile HoldCo which owns a 56% stake in a listed Brazilian Port/Maritime company called Wilson Sons and an investment portfolio, is trading a a deep discount (-48%) to its SOTP value. Now however it seems very likely that the Brazilian Asset will be sold by year end 2024, which could potentially trigger a re-rating of the stock on top of any premium paid in the sale.

2. Introduction:

Longer term readers of my blog know that in addition to investing into boring GARP stocks, I also invest into Special Situations from time to time. A special situation is a more short term oriented investment with a clear trigger or catalyst. In earlier times, I did more of them, these days I have less time and only look into them if they jump at me but usually with a relatively small allocation. There are different types of Special Situations. This one is of the “Undervalued company sells major operating asset” type of Situation, of which I have done a few in the past. The last one was Exmar two years ago with a decent outcome.