Special Situation EXMAR NV (BE0003808251) – “Time to Tango ?”

Disclaimer: This is not investment Advice. Never trust any anonymous dude on the internet. DO YOUR OWN RESEARCH!!!

IMPORTANT UPDATE: Due to a formula error, I double counted the Net cash in the SOP calculation. Kindly check out the updated numbers ! Fair value is now ~14 EUR per share compared to 17 EUR. Still attractive but a little bit less then initially thought.

Background:

Due to time restrictions, I am not so active in special situations anymore, as the “return on time invested” is often not so great. However if a Special Situation basically “jumps at me”, I won’t say no. In this case some starts aligned: Two people I respect a lot (M. and C.) both independently mentioned this sitation.

In addition, I have a certain weakness for Belgian special situations since my SAPEC investment some years ago and at first sight, a lot of aspects “clicked” with what I am looking for in a special situation.

Just as a reminder for newer readers (and myself): A special situation in my definition is an investment where I am looking at shorter time horizons and where there are some kind of catalysts that could help to realize a significant undervaluation of a security. I have different requirements for special situations, for instance, the long term quality of the business or the management are less important.

The company:

![]()

Exmar NV is a Belgian holding company that comprises a couple of maritime activities. The major activities are LPG shipping, the operation of “maritime infrastructure” and other activities, among them interestingly a travel agency and a Yachting service.

In the past, the most reliable segment has been LPG shipping with around 60-70 mn USD EBITDA p.a. LPG shipping seems to do OK at the moment.

The infrastructure segment has been the problem child for some time. It consists out of two large LNG related assets that have been mostly idle for the last 2 years or so and two “floating offshore accommodation” vessels. The segment has been showing some profits both, in 2020 and 2021, but mostly due to termination fees for contracts.

Overall, I would not call Exmar a “great company” but rather a mediocre shipping company that I wouldn’t normally touch with a 10 foot pole.

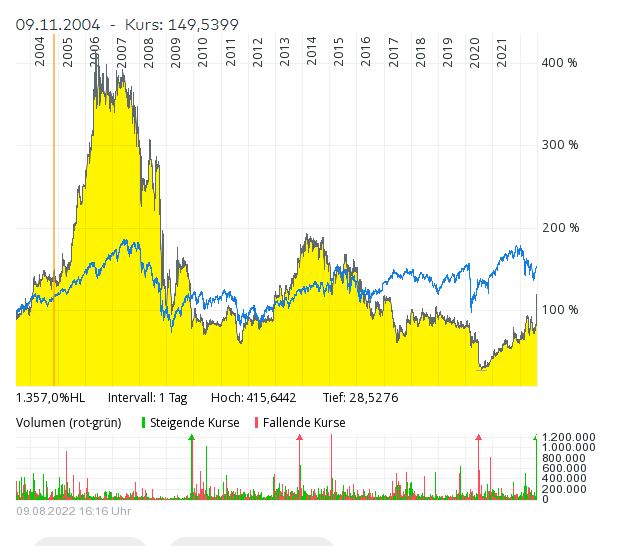

The long term stock chart shows that Exmar clearly was not a very good performer, although the stock already had recovered from the Covid lows:

The event: Tango Baby

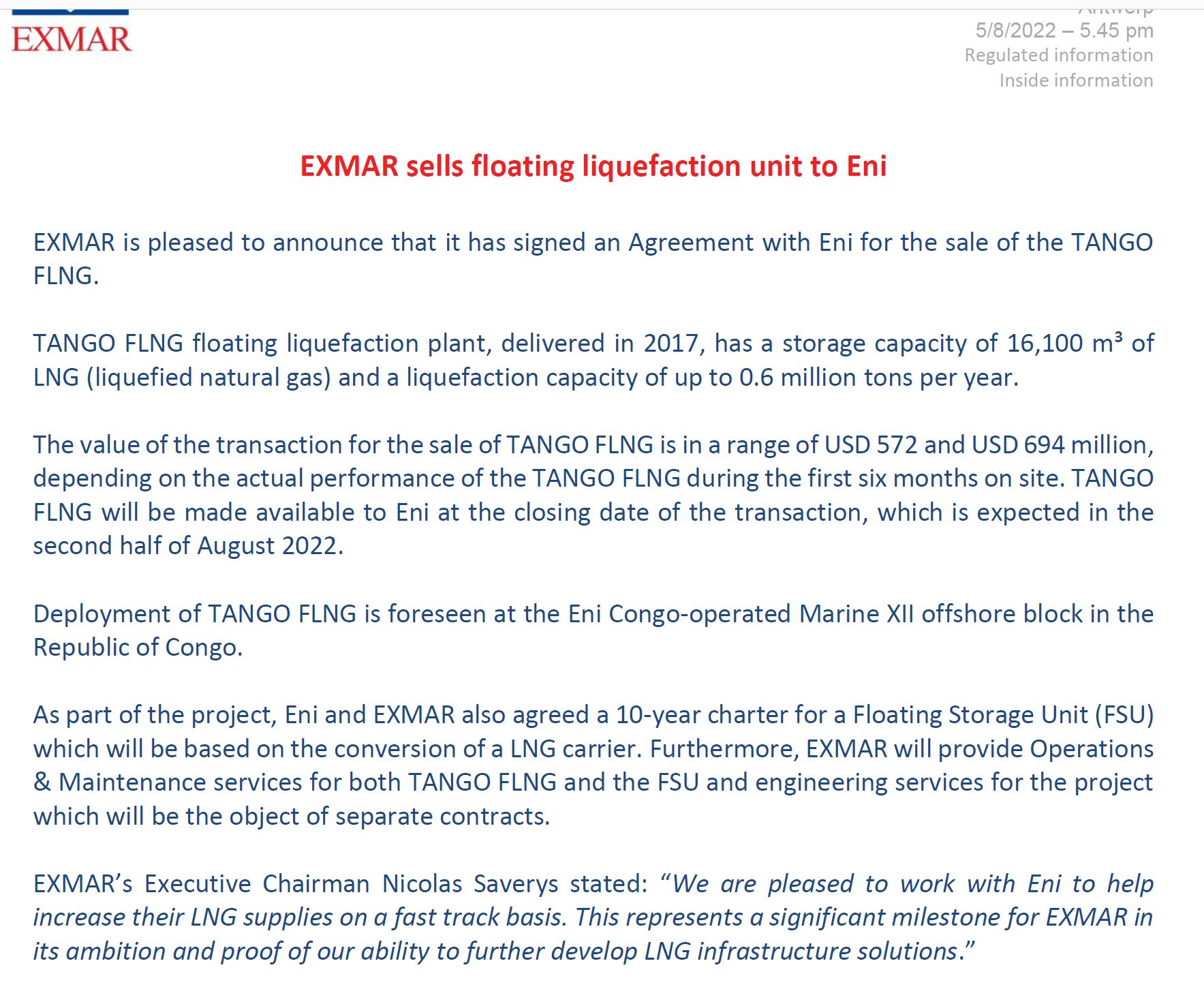

Pretty much out of the blue, Exmar published the following release on August 5th.

So in a nutshell, Exmar managed to sell their idle LNG liquification platform for an amount close to the total Enterprise Value before this announcement (~340 mn Equity, 460 mn debt). Although it was clear that their LNG assets have gained in value due to the Ukraine crisis and the new European thirst for LNG, this seems to have surprised the market somehow and the stock jumped around 35% and added ~110 mn in market cap on the first day.

Sum of the parts valuation Step

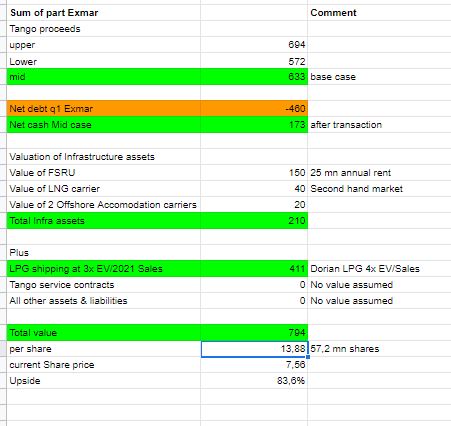

In Exmar’s case, a sum of the parts valuation can be done relatively easily: The remaining infra structure assets can be valued separately, the LPG business based on a peer multiple. To make things simple, I value the remaining business minus the corporate overhead at zero. This then looks like this as a “base case”, assuming proceeds of the Tango sale in the middle of the range:

The biggest uncertainty is how to value the FSRU. I have seen values in the second hand market for comparable vessels of ~300 mn EUR, a Keppler sell side analyst only assigns a 100 mn EUR valuation for whatever reasons. The 150 mn I have assumed are in my opinion realistic. According to the same analyst, Exmar has leased out the FSRU in MAy for a rate of around 20-25 mn USD p.a. for the next 5 years and the vessel is pretty new.

However it would be naive to assume that the stock price will move quickly to this SOP value without a real “catalyst”.. More on that later.

Major Risks & Why is the stock cheap

- there is a residual risk that the deal doesn’t close or Tango doesn’t perform at all. I would consider this as quite low though, lower than in the SAPEC case

- the main risk is clearly capital allocation: What will Exmar do with the money they receive ? In gross terms, Exmar receives ~11 EUR per share in cash. It is realistic to assume that some of the debt in the Infrastucture segment is linked to that vessel and they need to repay it. In total, Infrastructure had around 200 mn in debt, I guess a conservative assumption s that they need to repay 75% of those loans (150 mn) and that ~480 mn are available for whatever purpose Exmar decides

- So far, Exmar has not announced what they will do with the money. Some sell side analysts expect that they will pay a rather significant dividend (Kepler estimates 7 EUR per share). However Exmar could decide to just keep the money on its balance sheet or do something really stupid with it, like buying a company or lending the money within the family. THIS IS THE MAJOR RISK ONE IS TAKING AT THE CURRENT STAGE

- In case Exmar will pay a rather large dividend, as in the SAPEC case, Belgian retail shareholders will sell before the dividend payment as dividends in Belgium are taxed whereas capital gains are not taxed for retail investors

- Assuming an ongoing conglomerate discount for whatever “stub” seems to be appropriate. In the SAPEC case, a much larger part of the value was cash, so the “stub” risk is higher here

- overall, the stock is not so well known, Belgium is not a focus country for many international investors and the accounts of the company are not easy to read (JVs vsproportional consolidation etc.)

- Existing shareholders have gone through a lot of pain and have been selling after the announcement without fully understanding the increase in intrinsic value

Valuation part 2 -different Dividend assumptions and Discounts on the stub

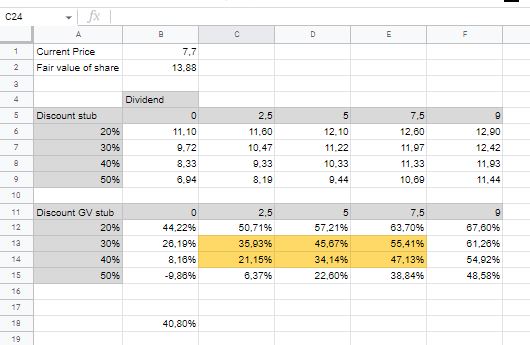

As mentioned above, we currently do not know if and how much of a dividend Exmar will pay and what the discount to intrinsic value will be after the payment of the dividend. Therefore I have created a table with a couple of scenarios where I use different assumptions for the dividend per share and the final discount to intrinsic value for the stub. This looks as follows.

The first table shows the estimated value in EUR of the dividend plus the assumed value of the stub based on different assumption. For instance, a dividend of 5 EUR and a discount in the stub of 30% would lead to a total shareholder return of 5 + (1-0,3)*(13,88-5)=11,22 EUR. The second table transforms this into a return vs. the current share price of 7,7 EUR /share.

The orange box covers in my opinion the most likely outcomes and results in an “expected” return of around +68%. To me this looks very attractive.

Shareholders & the Saverys family

The Saverys family controls ~44% of the shares, 3,8% are treasury shares and a fund controls around 5% of the shares. According to local sources, the Saverys family is a complicated one and is active in shipping across some participations in the maritime business for a couple of generations. They control for instance CMB which they took private in 2015. Through CMB they have a significant stake in listed oil tanker company Euronav, where they are currently fighting for control with “Shipping Man” John Fredriksen.

Exmar is led by Nicholas Saverys, who seems to have a reputation of a gambler. He clearly gambled by investing into these large LNG assets. The gamble seems to have worked out but there was a lot of luck involved.

The current struggle at Euronav could indeed mean that they might want to extract cash by paying a dividend, but so far this is only speculation.

Game plan / Catalysts

According to their investor calendar, the half year report is due on September 9th. I would assume that at that point they will communicate something with regard to dividends. This would be the first catalyst.

The actual deal closing in the next days will most likely be not a big event.

As in the SAPEC case, in case of a large dividend payment, it might make sense to actually wait for the dividend payment to realize the relative Tax arbitrage one can make as a German Investor compared to Belgian investors. This would then be the second catalyst.

So my game plan is as follows:

- If the Saverys family announces to do something stupid with the proceeds, I will sell no matter what

- If the Stock moves up quickly to around 11 EUR per share until the begining of September, I will take some profits and see if I can invest again pre dividend

- otherwise I will keep the stock until 4-6 weeks after the dividend unless my overall return target of 70% is reached before that time

- Note to myself: This is not a long term investment.

Summary:

Overall, Exmar in my opinion offers a very interesting risk/return profile: I am underwriting a +40% expected return for a 12 month period. The risk I am underwriting is mostly capital allocation, which is an uncorrelated risk that fits well into my risk appetite.

I therefore decided to allocate ~5,3% of the portfolio into this special situation at inception at an average price of around 7,65 EUR per share.

Due to time restrictions, my research process has been shorter than in other cases, therefore I am more than happy for additional information, especially potential risks that I have maybe failed to identify.

Disclaimer: This is not investment Advice. Never trust any anonymous dude on the internet. DO YOUR OWN RESEARCH!!!

Please could you update your view of Exmar now that it has announced the super dividend and also its intention, despite recent second failed attempt, to take the company private. I hold shares in other LPG companies, but not so far in Exmar. I am tempted by the dividend, but am concerned as to whether Exmar could delist without warning once they get up to 95%, leaving the share price in the dust. Would welcome your analysis, thank you.

Pingback: Exmar – Update Q3 numbers: “Thank you for the Tango” & SELL - My Intermix

so interim dividend of EUR 0.95 and no further comment from exmar about the use of the remaining proceeds from the sale of Tango. not exactly the result you were hoping for?

Well, it ain’t over until it’s over. But clearly I would have preferred the announcement of a higher overall dividend at that stage.

However, the “fair value” assuming a 30% discount is still at around 10 EUR even with a 1 EUR dividend only.

Perhaps any further comments in the next Numbers in October…TANGO sale was in Q3.

Excalibur contract is great, and debt reduce, so fair value should bei over 10 I think.

„The Board of Directors of EXMAR has decided to convene a special general meeting of shareholders to decide on the distribution of an intermediary dividend of gross 0.95 euro per share.“

Thanks. Hopefully the first installment…

Not sure whether this is related to the Tango deal, but Exmar has ordered two new LNG carriers:

https://www.offshore-energy.biz/exmar-lpg-orders-two-dual-fuel-lpg-carriers/

Thanks. However these are LPG ships. Not LNG. LPG is their remaining core business.

Thanks for pointing out the typo (I should proofread my comments more thoroughly). My thoughts were that this is maybe where (some of) the money from the sale of the Tango unit goes. Unfortunately the press release does not tell us how much these new vessels cost.

For mid-sized dual-fuel vessel I would estimate $80m, so $160m out the door.

That happens within the LPG business which is a JV. I assume that the proceeds of the sale are not used for this.

LPG shipping by the way might be a nice growth industry for the next 3-5 years. I read about several businesses wanting to switch from NatGas to LPG.

Here is some additional on Exmar an the Tango-deal:

https://www.world-today-news.com/gas-tanker-shipping-company-exmar-sells-floating-lng-factory/

Problem with shipping is that people always look at the trading numbers when in fact the share prices mostly trade on narrative. Think about it – you invest in a commodity asset with like a 30 year lifetime. Your return on that asset depends on supply and demand for that asset over a 30 year lifetime, and supply and demand can turn on a penny (COVID, ballast water legislation, sulphur emissions, dual hulling of tankers, now propulsion post 2030) as you have seen last few years. Most shipping assets have prolonged periods of losing a bit of money and a few killer years every now and then. No reliable way to value that 30 years into the future. Therefore the real world cashflows are really an input into a story telling machine and management have 1001 ways to spin a story. And somedays Mr Market likes the story and some days he doesn’t. If I understand the numbers right, your return thesis is based on Mr. Market giving you ~50% of the value coming from the story telling machine. And if that assumption is correct, you’ll do well. And you also have the fact that gas shipping tends to have longer term contracts so ought to be less volatile.

But who knows what shipping’s story will be in 12 months’ time, and so for me that’s the real risk. Good luck.

pogonific,

thanks for their comment. i agree that shipping is really difficult. However in a special situation like this I am very agnostic to the asset. The bet is clearly that for the remaining part of the business (LPG) the world will not change within the next 12 months. However there is enough buffer even for some adverse developments.

Interestingly, my best special situation investments since running the blog were in assets that I wouldn’t normally touch like HT1 subordinated bank debt, Aire real estate and Sapec (fertilizer).

What about the „Quellensteuer“ for the dividend for german tax payers?

Kindly reger to the sapec post. Belgium will reimburse with a delay of 1-2 years. The potential loss ex dividend will be set off against the dividend frim atax perspective.