Exmar – Update Q3 numbers: “Thank you for the Tango” & SELL

Exmar was a special situation that I entered in August, following a surprising significant asset sale (a LNG liquification platform called “Tango”)

Yesterday evening, Exmar reported Q3 numbers including the final numbers on the ENI transaction. A few points that I found important:

- Cash proceeds for the ENI transaction were slightly higher (+13 mn) compared to my base case

- Net cash at company level however was -23 mn lower than I had calculated

- Interestingly, Exmar only reported net cash at Group level, not gross cash at Holding level

- The remaining core LPG business seems to do quite well, with sales up ~6% and EBIT up ~50%

- They didn’t provide explicit number on how much they earn with the remaining regasification unit that is operating since August. The earnings of the “infrastructure” segment are really hard to read

- Next week, there will be an extraordinary shareholder meeting declaring a 0,95 EUR dividend per share

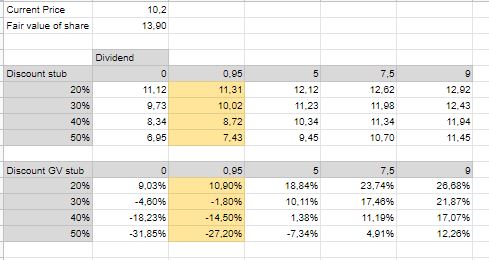

The share price has done quite well. At the time of writing, Exmar traded at 10,20 EUR per share, an increase of almost exactly 1/3 vs. when I entered the position and even better in relative terms:

Here is the updated matrix that I used initially to calculate expected returns. The only thing that I have changed is the current share price and exchanging 2,5 EUR special dividend with 0,95 EUR:

We can see that depending on the assumed future discount, the potential is quite limited if 0,95 EUR remains the only special dividend.

To be honest, I am somehow skeptical that they distribute much more. Maybe I am a little paranoid, but not reporting the gross cash number for instance could indicate that they might want to keep a significant portion of the cash.

With regard to the remaining business, one could argue that this might be worth more than a few months ago, as profitability is increasing significantly, on the other hand, this special situation was never about the the remaining business as such, but that the gap between “fair value” and price would narrow, driven by the closing of the Tango deal and a special dividend.

As I mentioned in the initial post, I don’t think that Exmar is a great company, but rather that Exmar got very lucky with how things developed for anything that was LNG related.

Therefore I decided to say “thank you for the Tango” to Exmar and sold my position at 10,20 EUR per share with a profit of ~33%.

Sapec reloaded… Exmar NV will be taken private at 12.10 Euro per share cum dividend.

Click to access exmar_pr_-_saverex_intends_to_go_private.pdf

Thank you again for introducing the case.

Pingback: Exmar – Replace Q3 numbers: “Thanks for the Tango” & SELL - Get Invest USA

Many thanks as well for this! It has been quite interesting to follow and invest myself a little.

One hopefully not too stupid question: Why don’t you wait for the company to pay out the dividend? For you this would be an additional return of 11-12 percent on the dividend. Am I missing something here?

Theoretically, the stock will trade “ex dividend” the day after the payment if the dividend. Maybe it catches up maybe not. I would also have to apply for a refund of the withholding tax…

Thanks from me as well. Long time reader of your blog, but this was my first time investing with you. Made a quick +20% too. And yes, I do my own research, but I probably would not have found this one without you. Win or lose, what I like really like about your blog is that you seem to strive for honesty. We all have our blind spots and biases, so what counts for me is a genuine effort to overcome them.

Thanks for the feedback.

Thank you very much for covering of the Exmar-Story. It made me 20% within a rather short time.

You are welcome. But remember: Sometimes you win, sometimes you lose.

Kindly wire my profit share to account number 0070815 at ElonBank as always 😉

In Euro or in Bitcoin?

Dogecoin of course 😉

Neutral. I don’t know them well and as mentioned, this was a short term special situation and not a mid to long term bet on the jockey 😉

any thoughts on the fact that the saverys family recently bought some chunks of stock at close to the current prices? would you consider that positive or at best neutral?