Updates: STEF SA & Gerard Perrier SA

DISCLAIMER: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Summary

In this update post, I look at two of my French stock positions, STEF SA and Gerard Perrier. For STEF, I reduced my position by 1% of the portfolio because of problems with the integration of newly acquired companies. In contrast, I increased my Gerard Perrier position by 1,5% of the Portfolio as business is accelerating and they seem to have made some very good acquisitions in the Defense/Aerospace and Digital space.

STEF SA

Stef is a company that I analyzed and wrote about 2 years ago. In essence, I considered it a cheap but reliable infrastructure-like cold-storage company with a great track record that is consolidating several European markets. For such a “compounder”, the price looked very cheap at around 8xP/E.

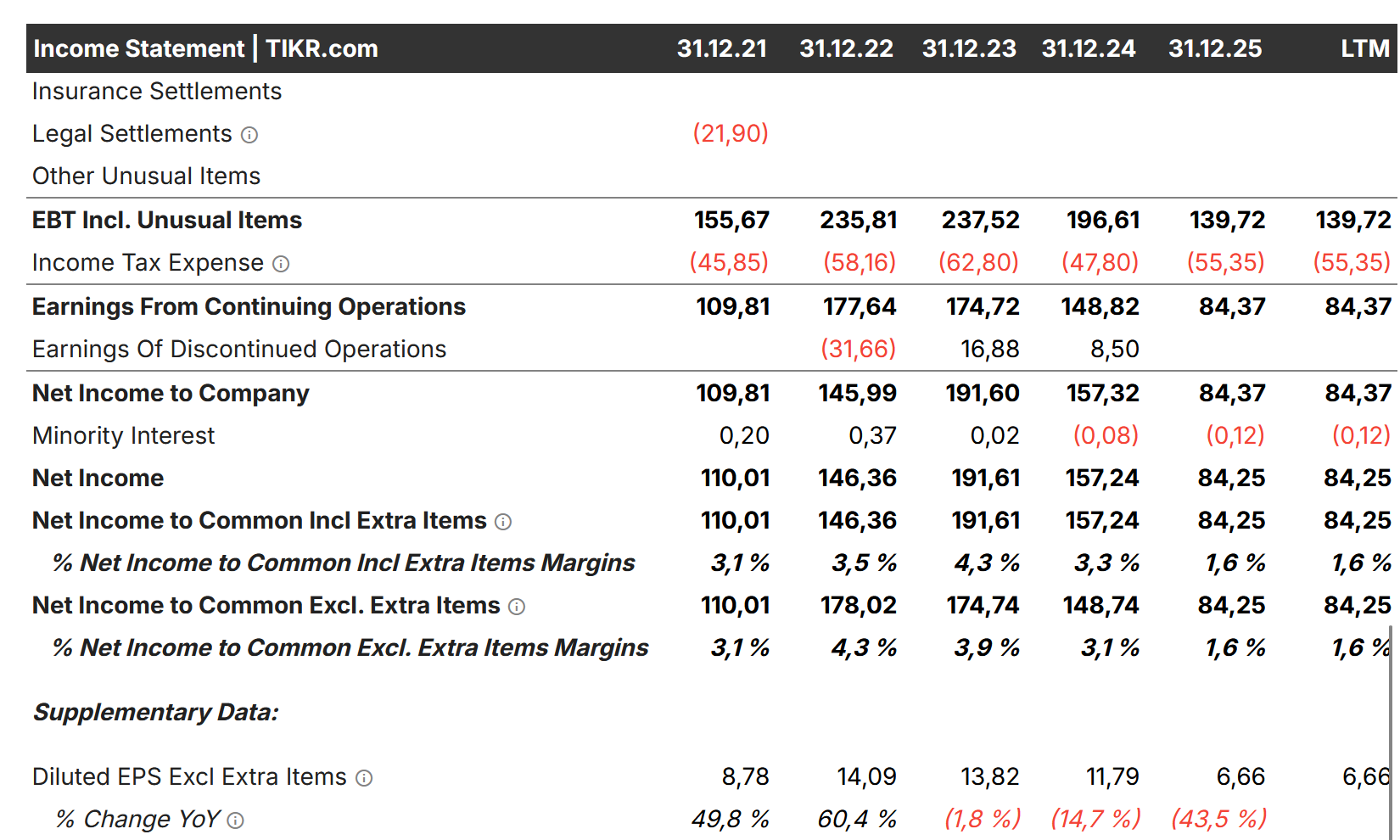

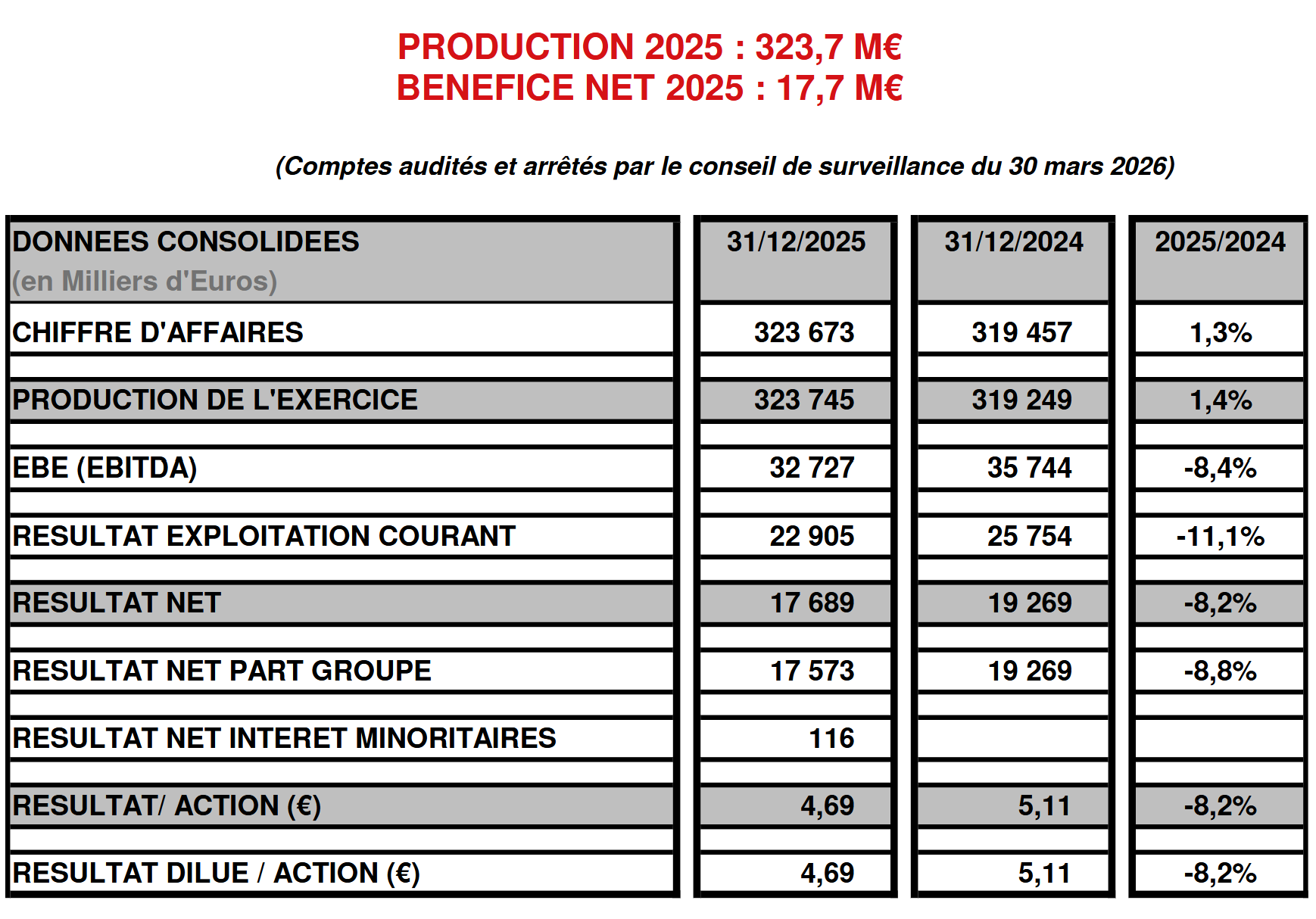

However, things turned out a little differently than I thought. While 2024 was a little bit weaker than 2024, 2025 saw a significant decline in EPS to a level of less than 50% of the 2023 earnings.

According to the 2025 investor presentation, this was a combination of one-time effects (Tax France, VAT Italy) and slower than expected integration success in its recent acquisitions.

To my own discredit, I failed to follow up on the 6M sales release from STEF which still looked good. I should have looked at the full half year report instead.

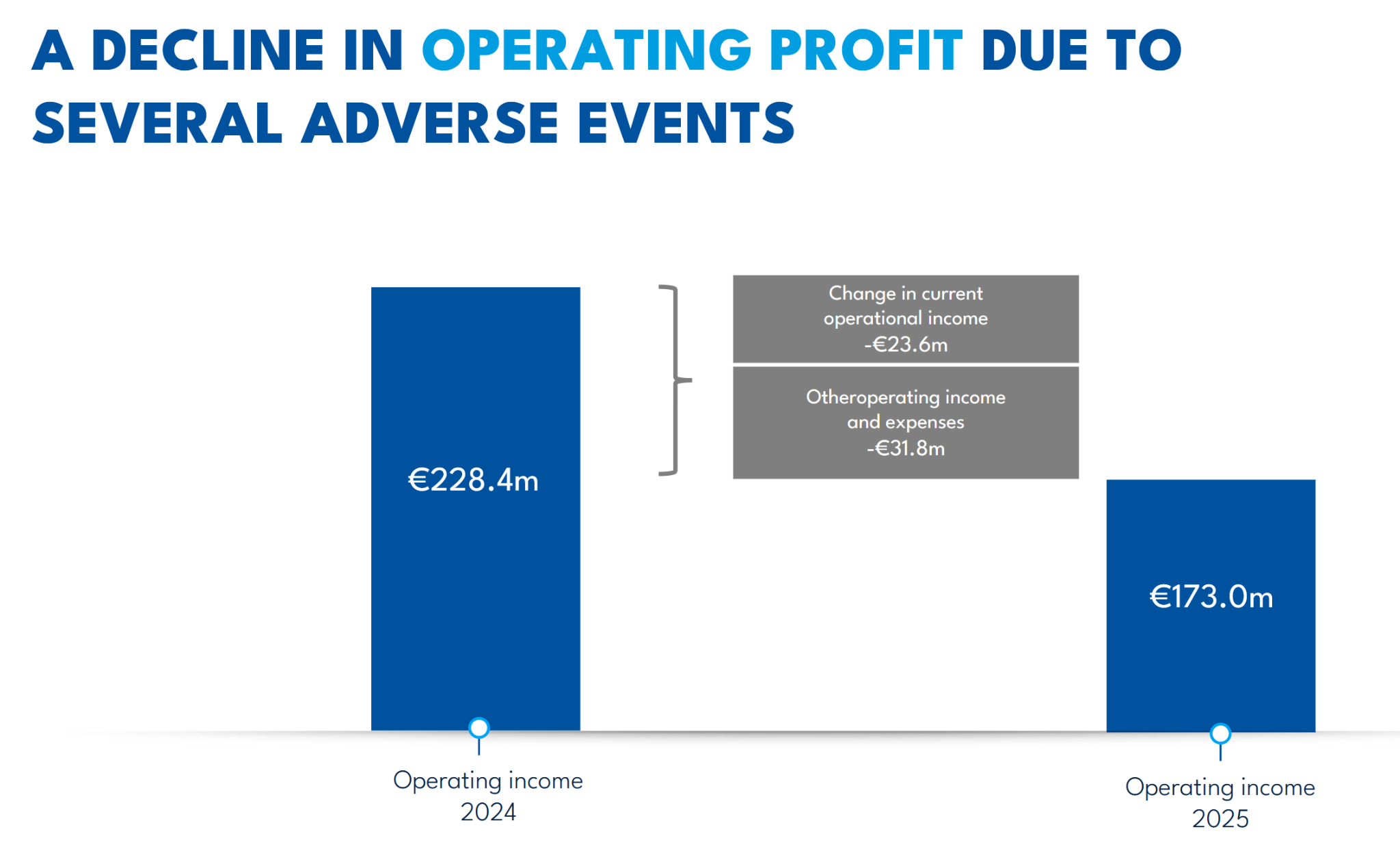

This is how the explain the declin:

Also, net debt increased by 200 mn.

The dividend was cut to 2,70 EUR from 4,15 EUR the year before (and 5,10 EUR in 2023). This is understandable from a company perspective but somewhat unfortunate for investors.

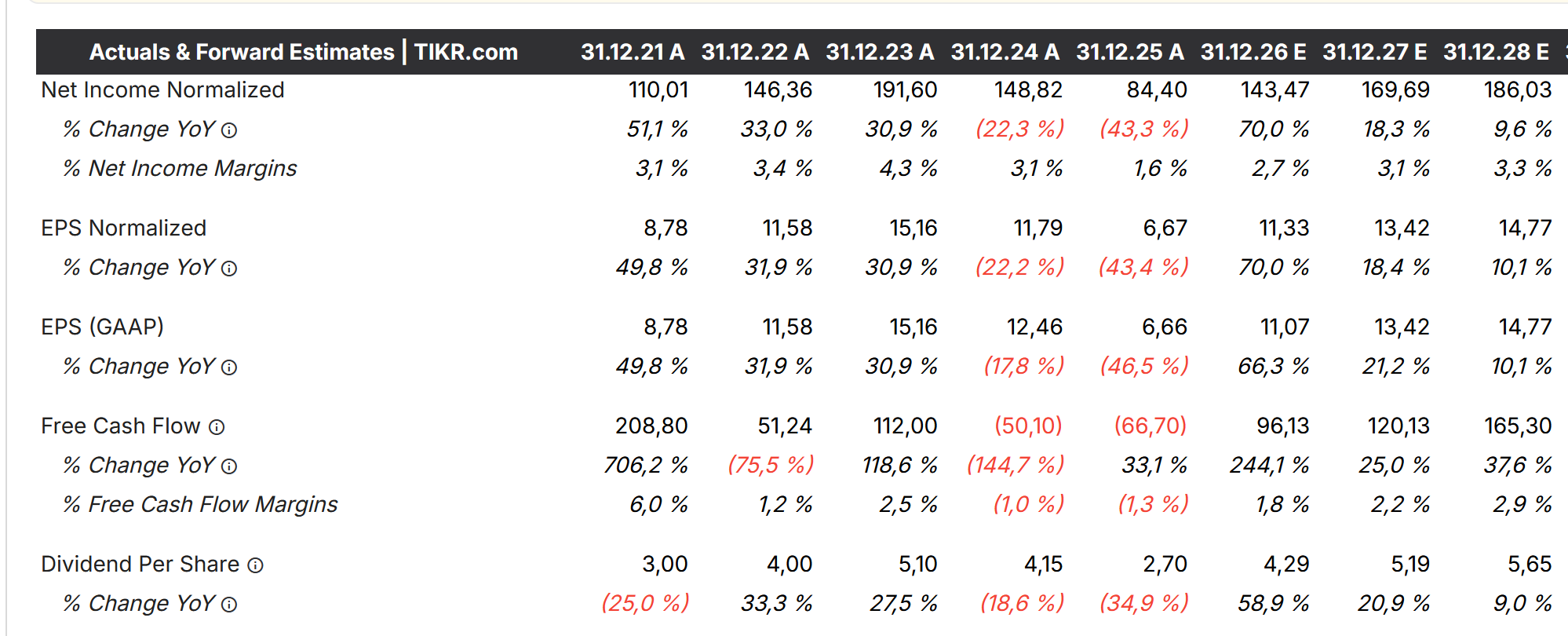

Analyst estimates seem to expect a recovery in 2026 and the following years according to TIKR:

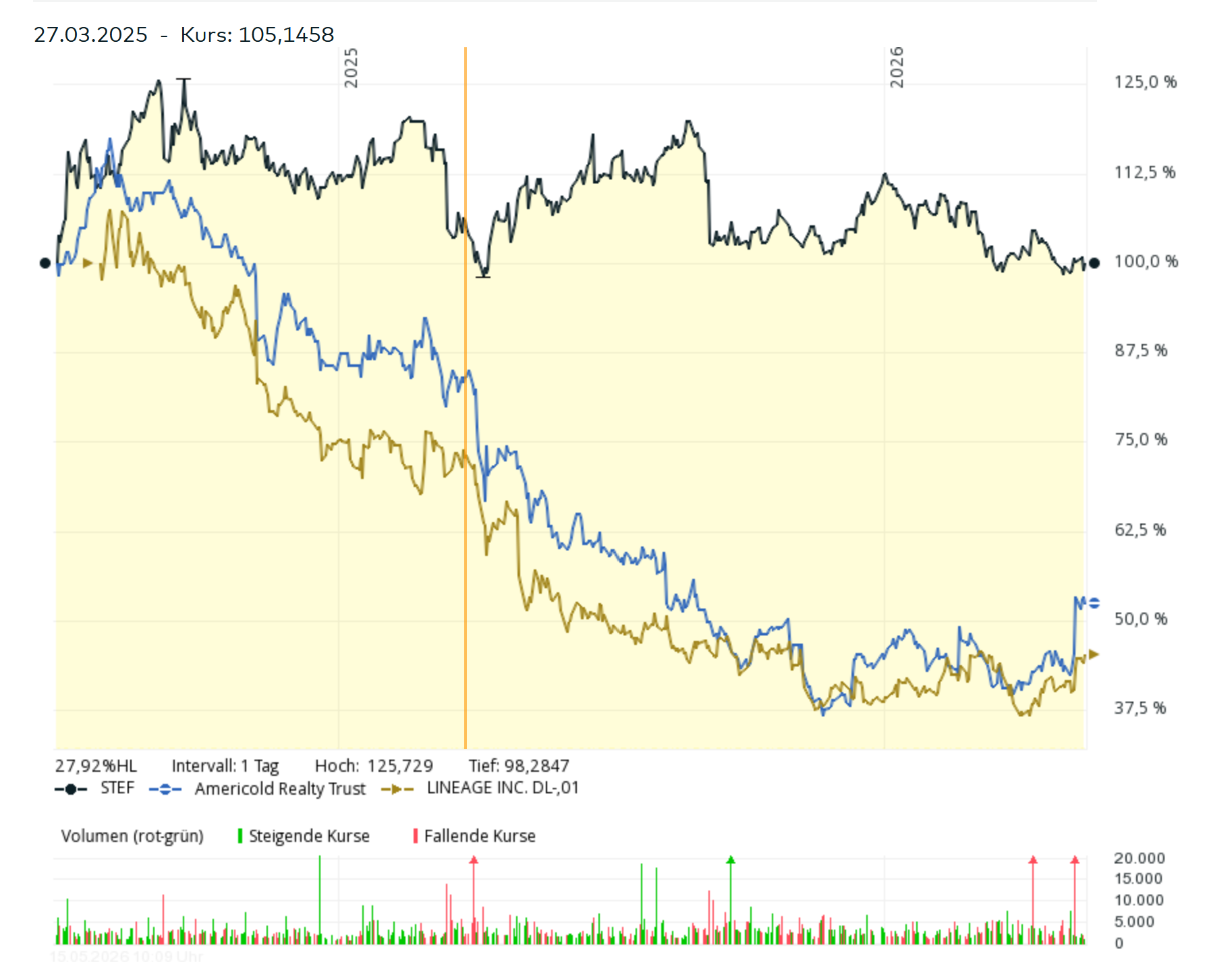

Share price wise, the stock is almost exactly where it was when I wrote up STEF. Interestingly the US peers did much worse:

A quick look into Americold’s 2025 press release shows decliningorganic sales and mention of “speculative developments” in the cold storage industry.

Also Lineage reported declining sales in 2025.

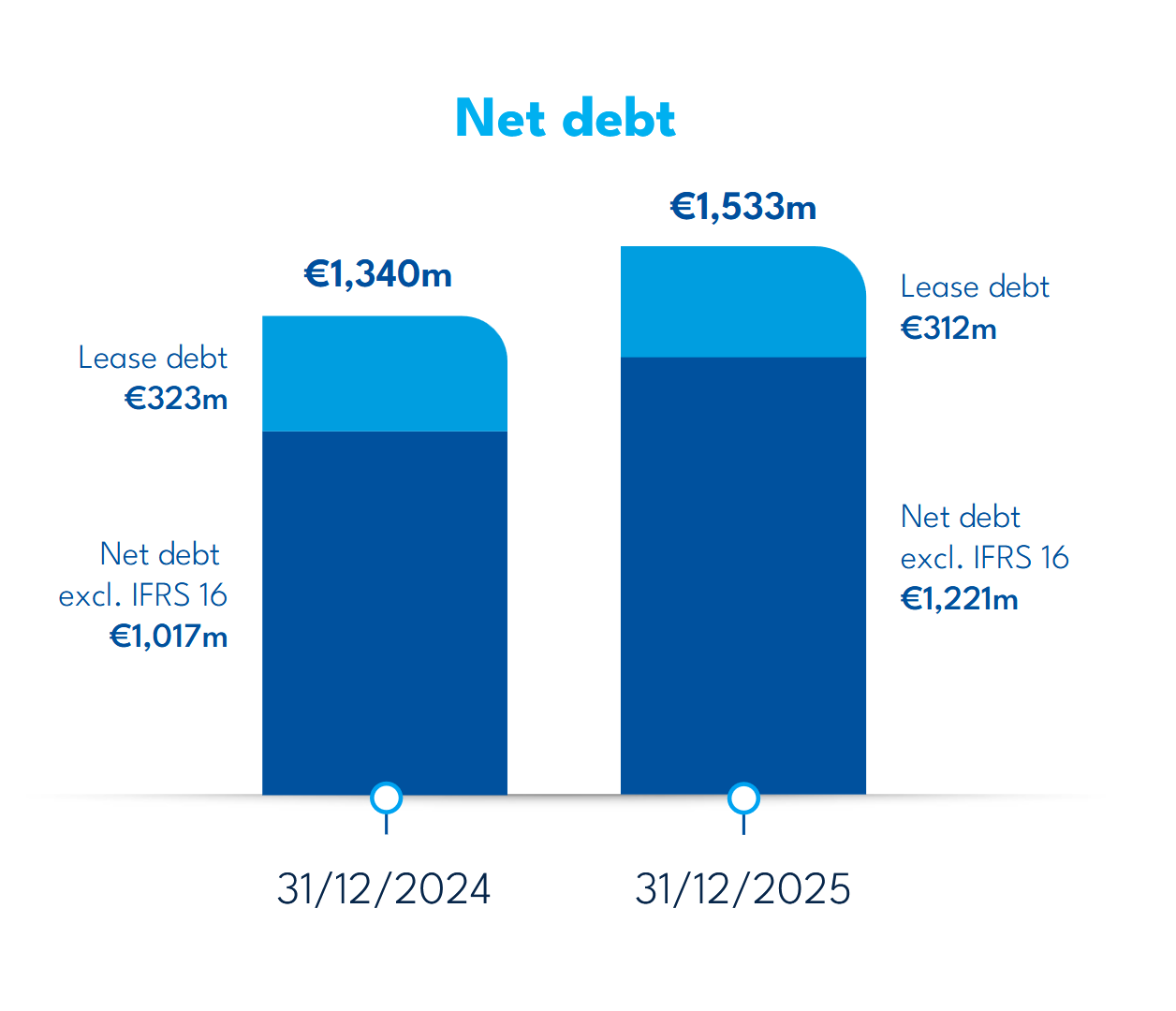

Both US peers are extremely highly leveraged (8x EV/EBITDA) and therefore very vulnerable to negative economic developments. However, also STEF’s net debt to EBITDA ratio increased from 2,5x in 2023 to 3,5x in 2025. Still manageable but if interest rates increase, this will represent another headwind for them.

My conclusion at this stage is that Stef clearly has over-extended itself with its acquisitions in the neighbouring countries and has not been able to integrate them successfully so far.

Management mentions that things should “normalize” in 2026 and Q1 revenue looked ok, but experience shows that the full integration of the newly acquired company can take much more time.

Although I am not ready to throw in the towel yet, I do think that my initial 5% allocation (currently 4,5%) was too high and reduced the position by 1% of the portfolio to ~3,5%.

The positive aspect of this story is clearly that I bought cheap enough which protected me against a significant loss of invested capital.

Gerard Perrier

On the surface, Gerard Perrier is a little bit similar to Stef insofar as 2025 was a year when earnings went down slightly:

Despite still growing sales, EPS was -8% lower than in 2024. 2024 again was more or less unchanged from 2023.

In Gerard Perrier’s case however, the explanation is not that they didn’t integrate new acquisition but a temporal weakness in their Energy segment which comprises mostly the servicing of the French nuclear fleet.

This is the translation (from Gemini) from G. Perriers report:

“The activity of the Energy division (ARDATEM, TECHNISONIC), which includes services for the nuclear sector, saw its production decrease by 8.2%, falling from €89.8 million to €82.4 million. This slowdown is mainly explained by the transitional effect of the reduction in reactor outages and maintenance activities at power plants this year, as well as by a rationalization policy of nuclear operations in France, although the sector remains on a positive dynamic in the medium term.”

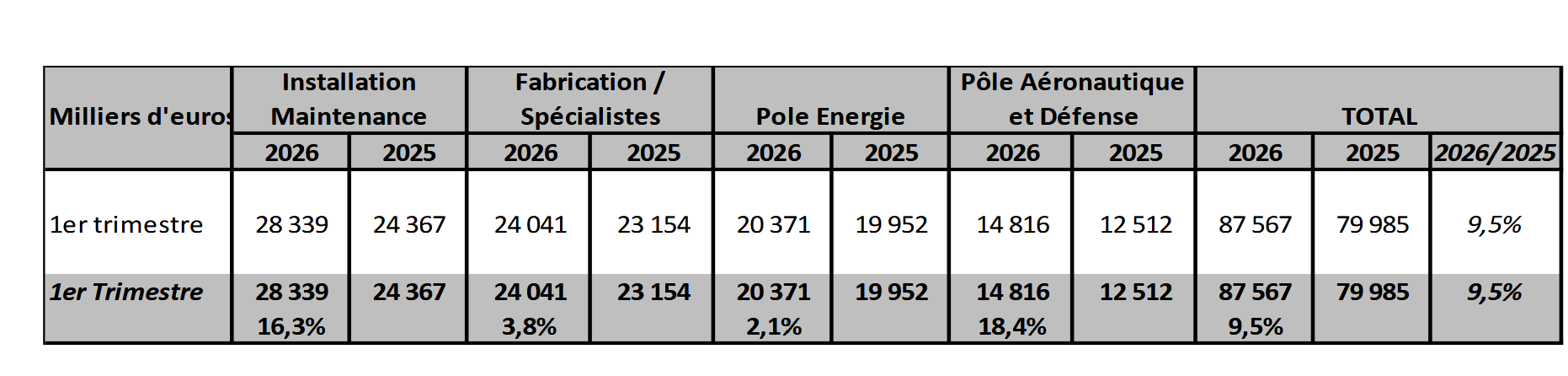

In addition, even without much growth in the Energy segment so far, G. Perrier had a great start into 2026 with sales up by +10% yoy:

As we can see, especially the “Installation Maintenance” and the Aerospace/Defense segments are doing well.

What I found interesting is that there was almost no reaction to this news in the share price:

What I do like is that their recent acquisitions look very interesting. With N-Cyp they acquired a small specialist company for industrial cyber defense, with OFATEC they get access to the Data Center market and with the acquisition of the three companies AQLE, SOMALEC et SOMALEC SUPPLY they strengthened their defense/aerospace segment, including components for the Ariane Space missile program.

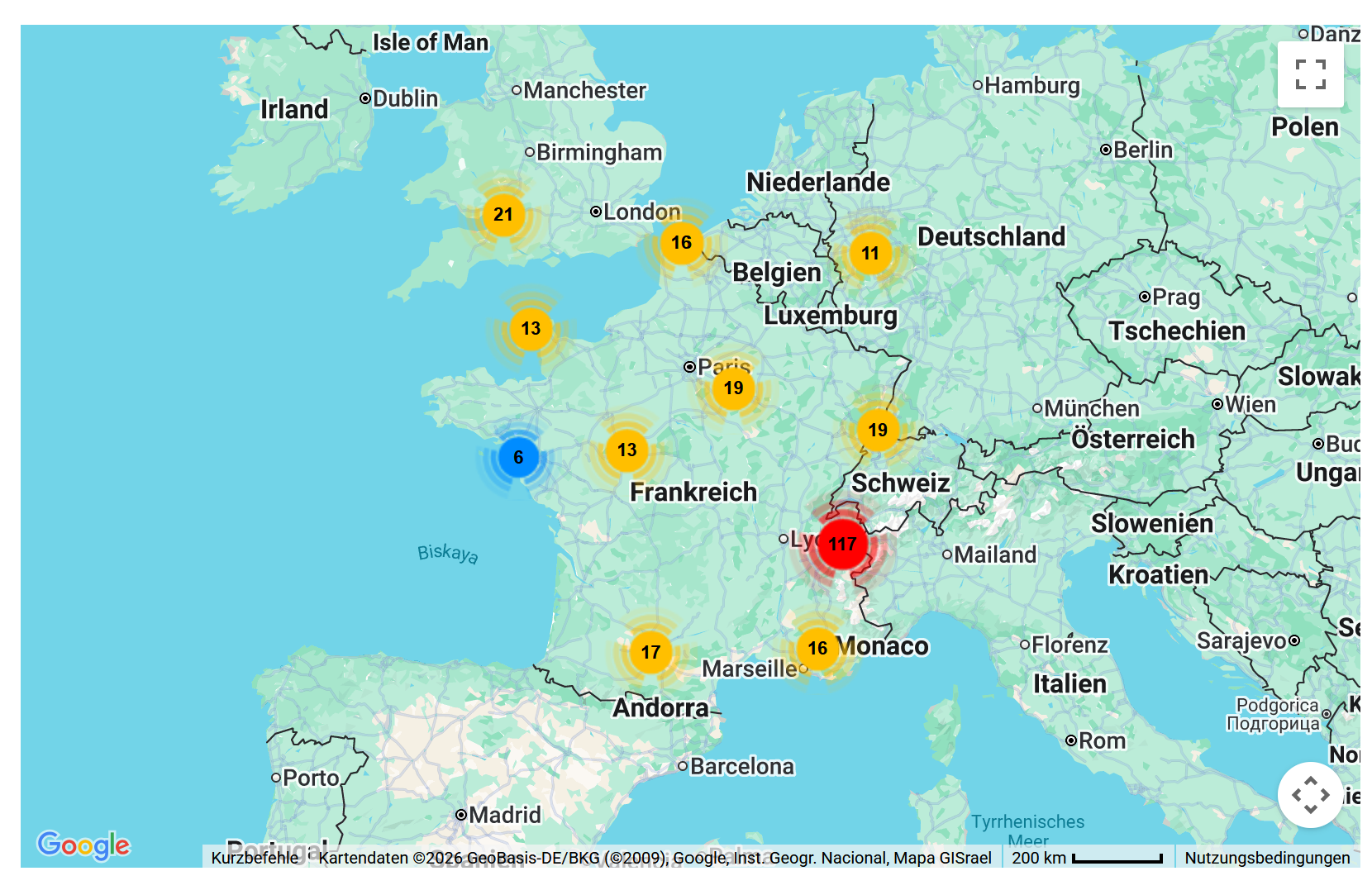

Another data point that I found interesting is that G. Perrier has still around 230 open positions as per their web site:

Most of the jobs are open at Ardatem (137), the Nuclear service company, which seems to imply that they expect a lot more work going forward.

Overall, I do think that Gerard Perrier offers a very attractive return/risk profile especially on the basis of the currently accelerating business numbers, therefore I increased my position from a previous 3,5% weight to 5% of the portfolio. The additional 1,5% were bought at an average price of around 83 EUR per share.