Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

As always with my more detailed writeups, I will focus on the gernal section in the post and attach the full pdf for anyone interested in the details.

- Elevator pitch:

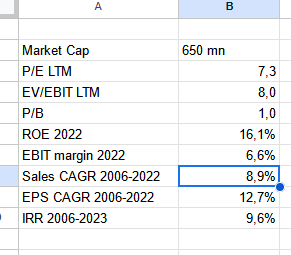

EVS Broadcast is a 400 mn EUR market cap Belgian technology firm that is the global leader in Live sports broadcasting/production technology that once earned margins higher than Nvidia does today.

After a relatively long phase of stagnation from 2008-2019, EVS seems to have found its path to decent growth again under new management. The main driver is a new technology cycle that will shift the product offerings from hardware focused solutions to more Software/Saas products and a move into adjacent markets (Studio production).

For a company with EBIT margins > 20%, capital return >20%, net cash and a targeted growth rate of 10% p.a. (which they have achieved since 2019), the current valuation of ~9x EV EBIT or 10-11x P/E is dirt cheap and offers considerable upside for the patient investor.

As EVS has been working on AI solutions since at least 2017 and has already functioning products to show, one gets any potential “AI upside optionality” for absolutely free.

Read more