Amadeus Fire AG (AAD.GR) – Come on and rock me Amadeus !!!

Disclaimer: This is not investment advice. DO YOUR OWN RESEARCH !!!!

As in the previous write-ups, the full 13 page document is attached as PDF. Within the post I will present the Elevator Pitch, Stock Price/Valuation, Risks and Summary. And of course a bonus music track !!

Elevator Pitch:

Amadeus Fire is a 590 mn EUR market cap small cap business service company that offers temporary staffing and training for finance and IT professionals in Germany. The company is well managed, has a strong track record with 10% p.a. growth for many years, decent double digit margins, high returns on capital and strong cash generation combined with a clear capital allocation strategy. The current valuation at an EV/EBIT below 10x and an even lower EV/FCF at looks quite compelling for such a boring but high quality company. GARP at it’s best in my opinion.

7. Stock price/ Valuation/ Return expectations

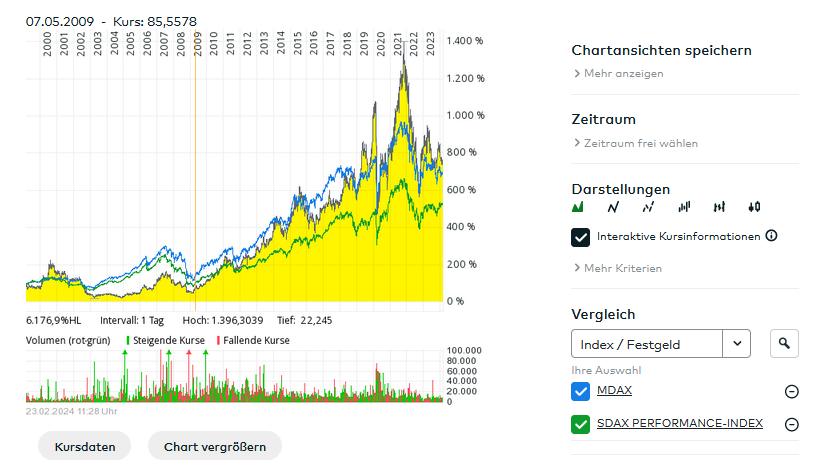

The price chart is quite interesting. It took Amadeus Fire quite a long time to surpass the 2001 peak, almost exactly 10 years until 2011. In any case, the stock outperformed both, the German MDAX and SDAX even without including dividends. The current share price is roughly where it was like 5 years ago, despite the fact that EPS has increased by almost +60%.

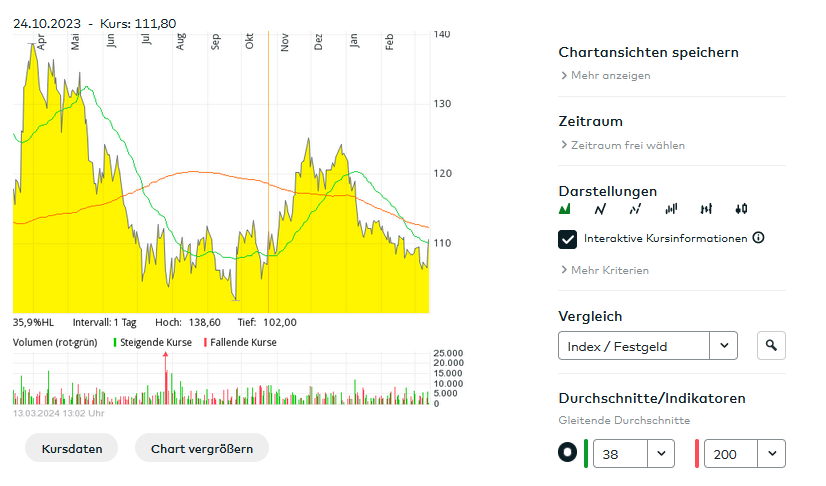

Also momentum currently is still negative:

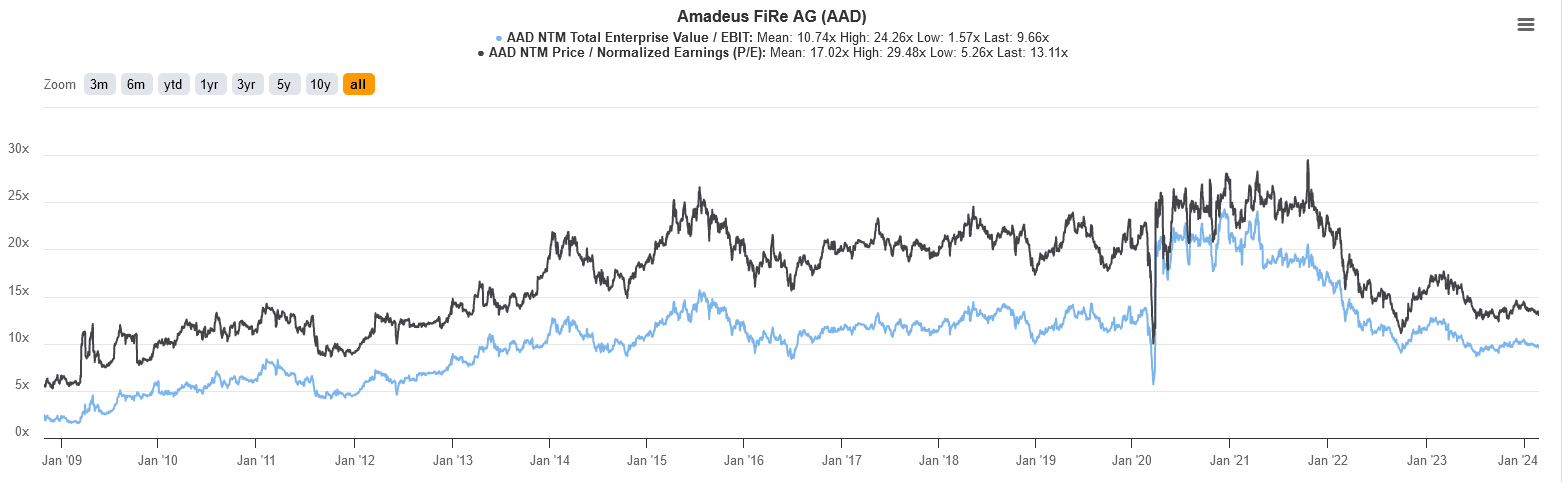

With regard to historic valuations, Amadeus Fire trades both below the long term average for EV/EBIT (9,7 vs. 10,7) and P/E (13,1 vs. 17) which could indicate some long term multiple expansion potential.

Amadeus Fire itself last year showed this guidance for future results:

This would roughly imply total growth of ⅓ from 2023 to 2026 or ~10 p.a. As mentioned before, organic growth requires very little capital,. I am not sure hw much m&A they need for 10% growth, but I think a 5% organic growth rate should be realistic. Even if they don’t manage 10% growth for some reason or another, I think this looks like a very attractive value proposition, as any multiple extension would come on top.

8. Risks:

As any investment, also Amadeus Fire clearly faces risks. Here are a few of them:

8.1. Regulatory changes

Temp staffing is regulated and regulations could change in a way to make it less attractive. As Amadeus Fire is only active in Germany they have full exposure to German regulation

8.2. Size of the Niche & “Diworsification”

As I attribute Amadeus Fire’s success to their specialization, any attempt to “diworsify” outside the focused temp staffing (finance, IT) and Training would clearly be critical. The question is also how big their niche is and for how long they can grow in that niche by 10% p.a.

8.3. Germany’s economic situation

The biggest risk is clearly that I misinterpret the impact of the current economic situation in Germany. Low or no growth, structural change, lack of skilled employees and inflating wages in my opinion are all positives for Amadeus Fire, but of course I could be totally wrong. The same goes for the increasing influence of AI in the workplace

8.4. Supervisory board member age

As mentioned, some members of the Supervisory board are quite old. It needs to be seen if and how these members will be exchanged in the next few years

8.5. Low ball takeover

A final risk is in my opinion also that without a strong shareholder, there might be the risk of a “low ball” take over offer by a competitor or a PE company. While that would bump up the share price in the short term, it could prevent shareholders from participating in the full upside potential.

9. Summary / Game Plan:

Based on my assumption that the future for Amadeus Fire looks not so much different from the past 5 or 10 years, the stock offers a potential return of at least 15% p.a. depending on what organic growth looks like and if they can do value add m&A on top of that.

From a quality perspective, Amadeus Fire ticks almost all boxes, with the only exception that there is no founders/large shareholder present.

For a “high quality” company, this looks like a very good value proposition to me. That’s why I decided to allocate an initial 3% allocation into Amadeus Fire at an average price of 109 EUR per share.

Amadeus Fire will release final 2023 numbers, their 2024 outlook and the dividend proposal on March 19th. Depending if the outlook changes or not, I might add to the position, especially if momentum turns a little bit more neutral/positive.

Extra Bonus Music track:

As in my last write-up on Eurokai, once again I add a Youtube Video that expresses my hope for this investment: Rock me Amadeus (Fire) from Austrian music legend Falco:

https://www.reddit.com/r/Aktien/s/ZNLtS213RH

Interessanter Post auf Reddit zum FCF und dem Management

Ich stimme zu dass ökonomisch der Free cashflow um die Leasingzahlungen gekürzt werden muss. Das EBITA hat aber damit nicht direkt was zu tun. Das ist ja eine reine Buchhaltungszahl.

Nach nochmaligem Lesen fällt auf, dass der Verfasser wohl nicht so ganz genau weiss, dass die IFRS Änderungen zum Ausweis der Mietverträge allgemein in 2019 eingeführt wurde, nicht nur bei Amadeus Fire und nichts mit der Akquisition zu tun hat.

Hi there, I bought the stock in January (roughly the same price, 111 EUR or so). You’re right that FCF ist even better than net profit. But one thing: The FCF they put up in their report is in my understanding not correct. Because of Leasing (IFRS 16) in the cash flow from financial activities the lease repayment has to be deducted, that is about 20 mn p.a. Please correct me if I am wrong, but I think this is the correct approach. Anyway, valuation is attractive anyway.

great pitch. another interesting german high quality company i like even more right now is hermle, with more of a hard moat to use your words. the german discount is just too big right now imo.

You´re very kind to share these thoughts for free!

Cheers

great idea. don`t you think they kind of have a network effect? i think after a lot of people get hired from amadeus, amadeus is well known among companies and kind of entrenched and interwoven. just like mckinsey etc. Hermle looks also similarly interesting right now imo, with more of a hard moat due to large switching costs what do you think?