Admiral Plc – Deep Dive and Re-underwriting the Stock

Disclaimer: This is not investment advise but some rather incoherent ramblings of an extremely incompetent former value investor. DO YOUR OWN RESEARCH AND NEVER TRUST ANONYMOUS DUDES ON THE INTERNET!!

On “re-underwriting” an existing position

While writing part 1 of the UK Insurance update and even earlier, during the analysis of Naked Wines, I realized that my investment process has (among other issues) one serious gap: I have no systematic way to reassess or “re-underwrite” a position, especially for those who are in the portfolio for a longer time.

I do a short review every year in my “xx stocks for 20xx” series, but I do not seriously analyse my longer term holdings unless there is a problem.

In some cases that works well, but in other cases, I have been missing things or the case goes far away from the original case. Due to time constraints, doing this every year is not realistic, but going forward, I plan to do this on a 3 year rolling basis for each long term holding.

Review of my initial Admiral case

My original Admiral investment case was from 2014 and can be read here. The initial “underwritten business case” was as follows:

- Admiral had a unique business model and a competitive advantage as the lowest cost player in the UK

- the concentrated on an underwriting focused, capital light business model not relying on investment income but made a lot of money with ancillary services

- It was run by two of the founders who owned ~16% of the company

- Combining insurance with price comparison gave them an informational advantage

- They had growth options in other European countries

- it had a clear capital allocation policy by paying out everything they didn’t need

Financial performance:

My initial position was established at 13,80 GBP in 2014, i added at higher prices along the way. At the end of 2021, Admiral was my biggest position with 7,1% portfolio weight (those were the days…..).

As of yesterday, this is how the long term performance looks like since buying the initial position:

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | |

| Share | -13,8 | 17,29 | |||||||

| Dividends | 0,494 | 1,00 | 1,26 | 1,08 | 1,18 | 1,29 | 1,268 | 2,01 | 1,18 |

| Total | -13,31 | 1,00 | 1,26 | 1,08 | 1,18 | 1,29 | 1,268 | 2,01 | 18,47 |

| IRR | 11,80% | ||||||||

| GBP / EUR | 1,24 | 1,4 | 1,29 | 1,15 | 1,14 | 1,13 | 1,12 | 1,17 | 1,16 |

| Total EUR | -16,5 | 1,4 | 1,63 | 1,24 | 1,34 | 1,46 | 1,42 | 2,36 | 21,4 |

| IRR | 10,92% |

An IRR of 11,8% in GBP and 10.9% in EUR is not too bad. It compares to 9,1% p.a. for the whole portfolio and 4,6% for the benchmark, so a clear outperformance. This outperformance was mainly driven by the high level of dividends distributed over the last 8 years. Since the first purchase, 10,76 GBP have been distributed as dividends, or around 80% of the purchase price. 75% of the realized performance has come via dividends (pre tax).

As we seen in the following table, this performance was achieved despite a significant multiple compression based on trailing earnings (from ~13,4 to 8,7) and some major events in between such as the Brexit, Covid-19 and the Ogden rate issue.

Just to be clear: My overall Admiral position has performed worse as I have added to the stock during the last 8 years at higher prices. My current weighted purchase price is at around 17,7 GBP/20,455 EUR per share.

Operational KPIs

The following table contains a few KPIs based on 2013 and 2021 numbers. Admiral has developed as follows since then:

| 2013 | 2021 | CAGR | Comment | |

| Gross turnover | 2030 | 3510 | 7,08% | |

| Net Premium | 483 | 855 | 7,40% | |

| Total sales | 924 | 1553 | 6,71% | |

| Operating profit | 370 | 731 | 8,88% | Ex Special |

| Earnings | 287 | 583 | 9,26% | Ex special |

| EPS | 1,04 | 1,96 | 8,24% | Ex special |

| UK Motor premium | 1699 | 2244 | 3,54% | |

| International premium | 188 | 690 | 17,65% | |

| Non Motor Uk premium | 33 | 218,8 | 26,68% | |

| International in % | 9,3% | 19,7% | ||

| UK Motor uw profit | 233 | 646 | 13,60% | |

| UK Motor other profit | 204 | 225 | 1,23% | Ancillary |

| UK Motor UW profit in % | 13,7% | 28,8% | ||

| UK Motor other profit in % | 12,0% | 10,0% | ||

| International profit | -22 | -11,6 | ||

| Total investment income | 12 | 75 | ||

| in % of Operating profit | 3,24% | 10,26% | ||

| Trailing P/E | 13,5 | 8,7 |

A few remarks on these KPIs:

Total profit for Admiral was around 1 bn GBP in 2021, however slightly more than 400 mn GBP were a one off from the sale of the comparison portals (more on that later).

In general one can see that the top line growth drivers are clearly Non-Motor UK and International insurance. The main profit driver in the recent years have been nevertheless UK motor profits. Personally, I do not think that the 2021 result is sustainable but more on that later. However this explains that profits increased faster than revenue, despite the international business being normally run at a zero profit level.

Ancillary earnings have remained more or less constant, it seems that there the UK regulator has capped what is possible for insurers. Investment income has become a little bit more relevant, partially driven by their new direct auto loan business.

What has changed against my initial business case:

- Management

First, both founders retired and didn’t even remain as non-exec directors. The successors are long term Admiral employees. CEO is now Milena Mondini, initially CEO of the Italian subsidiary who joined Admiral in 2007. The other Executive director is Geraint Jones who works in the company since 2002.

Both own shares, Admiral has a requirement of 400% shareholding compared to (base) salary. Ms. Mondini has 5 years to reach that point. Outright, Ms. Mondini owns 65k shares and Mr. Jones ~100k shares, which at current prices is less than their annual total compensation (which was > 2mn GBP) each.

In 2013, both founders took a salary of around 400k GBP each (all in) compared to around >2 mn GBP for each of the current executive directors.

As a side remark, MunichRe seems to have reduced their stake at some point from 10% to 5%.

I am not able to judge the abilities of current directors against the founders but their financial interest is clearly more like a “Manager” than a “Founder/owner”. However I assume that Admiral is able to keep its Corporate Culture which in my opinion is clearly part of their success.

2. Price comparison & Ancillaries

Initially, the integration with Admiral’s comparison sites was a competitive advantage in my opinion. However over time that changed, as both ,access to the data become easier and it was difficult as an insurer to run these portals independently. Therefore, in my opinion it was a good move to sell the business for ~460 mn GBP (or 38x 2021 earnings) in 2021. It resulted in a 400 mn profit for Admiral which shows that they seem to account quite conservatively.

Ancillary services, which at the time of my initial investment, have become less relevant. I do think the uK ragulator limited this kind off additional services that could be sold to clients. Ancillary revenues were already in decline in 2013 at 67 GBP per car and have reached around 45 GBP in 2021.

3. International markets

Admiral clearly delivered on their promise to expand internationally. However the US subsidiary still seems to have issues. For Spain, France and Italy, I do think that they run this exceptionally well, investing their profits into growth. In the US, the success to me is not so clear. The US unit has made consistent losses over the last yeuar but is unfortunately also the largest international entity (equally with the Italian entity).

Overall, these changes were either “natural” due to age or logical as time goes by. The main but unavoidable issue is clearly that Management and owners are now more separated.

4. Reinsurance

Admiral continues to rely on Reinsurance in order to reduce capital requirements. I was often asked if this doesn’t pose a big risk. This would be the same question if you ask Volkswagen, if it isn’t a big risk to buy the wheels from a supplier.

Reinsurers are simply suppliers to the primary insurance companies. A supplier needs to sell his/her products. Sometimes the negotiation power is more on the supplier side, sometimes more on the client side. A good rule of thumb is the following: as long as you write profitable business, there will always be decent Reinsurance capacity at a decent price.

Despite their lower stock participation, MunichRe conitnues to provide ~40% of the capicity. Admiral actually managed to renew the MunichRE contracts in 2021 at more favorable conditions. this is form the 2021 annual report:

Co-insurance and reinsurance

We were pleased in the first half of 2021 to conclude important negotiations with our largest reinsurer, Munich Re, to extend our risk-sharing partnership in the UK car insurance business covering 40% of the total premium. The coinsurance contract which expires at the close of the 2021 underwriting year has been in effect in some form for nearly two decades and we’re delighted to be renewing the long-term arrangement. Munich will underwrite 20% of the business via a new co-insurance contract due to expire at the end of 2029 and a further 10% via a new quota share reinsurance contract expiring at the end of 2026. The existing 10% quota share contract will also remain in effect until at least the end of 2023. The changes should result in higher profit commission income for Admiral from 2022 onwards compared to the expiring arrangements.

So compared to Sabre, which warned of (much) higher Reinsurance costs, it looks like Admiral was lucky in renewing this major contract last year and actually getting more out of it.

In the Reinsurance market, other Reinsurers often follow the lead insurer, however Admiral hasn’t given more insights.

5. Capital allocation

Overall, they executed as promised and distributed most of what they earned on top of hwat they needed to support growth. Personally, I would prefer share buy backs but the dividend seems to be a significant part of the renumeration for employee shareholders.

Re-underwriting the stock

In order to re-underwrite Admiral, I need to assess if at today’s share price, Admiral offers an attractive enough entry point to justify an investment. As mentioned above, I think that 2021 profitability was exceptional and that inflation is clearly an issue.

However; I also think that Admiral is in relative terms the strongest UK player and might benefit in relative terms. I assume that they can grow at least as strong as the market without raising capital and paying their usual dividends and over time reach a Combined Ratio of 88% in the UK Motor market.

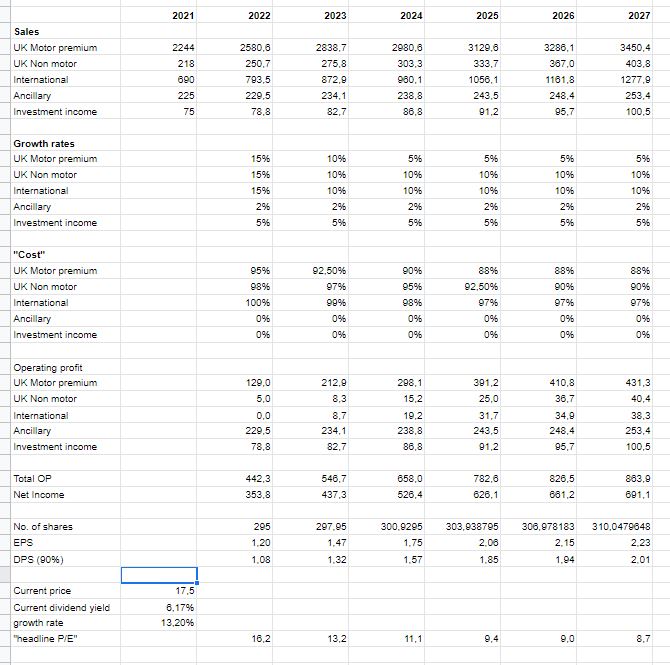

The general idea here is that my return expectations for any stock are basically the expected current dividend yield plus the growth of that dividend. For this, I have created a relatively simplistic model, included my assumptions and this is how it looks like:

My current assumption is that 2022 profit will drop by almost half to around 1,08 GBP/share. I assume relatively little reserve releases although Admiral clearly has some buffer there as 2020 and 2021 were very good years, and the releases of those years usually only show up after 2 or 3 years. Nevertheless we will see a significant strengthening of PPO and other reserves.

However, based on my assumptions there will be decent growth for the next years if things return to more “normal” in UK motor and the growth engines continue to grow. So far, UK Insurance has always adapted relatively fast and the players seem to be quite rational (or capital constraint).

Overall, at the current price, I “underwrite” a 6,2% dividend yield plus ~13% in growth with a total expected return of 19% before any multiple gains. This is my “expected case”. I didn’t model a worst case or a best case but I think they should be relatively symmetrical.

This looks attractive to me. I would require something between 10-12% to “break even”, so the conclusion is clear: I happily “re-underwrite” at the current price for at least another 3 years.

Competitors: Direct Line & Sabre

in the past, 2 “mini Admirals”, Esure and Hastings have been taking over. Esure by Bain Capital in 2018, Hastings in 2020 by Sampo. Looking at current UK market shares in Motor, Admiral is the largest player with 14% market share, but there are still al lt of “market share donators” such as AXA, LV, RSA and other “high cost” insurers with significant cost disadvantages.

Admiral also seems to have among the highest retention rates which is extremely important to keep costs down. Overall, Admiral is slowly increasing market share in the UK, during my holding period form ~11% in 2013 to around 14% in 2021 and this be remaining very profitable. Interestingly, 14% is a similar market share as Geico and Progressive in the US as well as HUK in Germany, and all of those are still growing.

The two direct competitors, Direct line and Sabre are quite different. Direct Line is a bigger player that struggles to bring down costs to Admirals level (~24-25% cost ratio vs below 20% for Admiral). Sabre is a niche player which IPOed in 2017. Both stocks look even cheaper than Admiral on past earnings/sales etc. however both competitors have been stagnating or even shrinking over the last 3-5 years compared to Admiral’s steady progress. Both competitors also run on significant lower Solvency levels which might restrict their ability to pay dividends or write new business more aggressively.

Clearly, in the short term or even mid term, the stock price of both, DirectLine and Sabre could do better than Admiral and maybe Sabre might even become an acquisition target similar to Esure and Hastings.

However, long term I do think that the better quality of the business model and the growth opportunities will favor Admiral.

Summary:

As outlined above, i feel comfortable with re-underwriting Admiral at this level. they have delivered in the past and despite the leadership change, I am very positive that they will manage though the current issues.

As the portfolio weight has actually fallen to around 5,3% at the time of writing, I will “fill up to 6%” at current prices of the time of writing (17,50 GBP).

What the share price will do over the next 6, 12 or 24 months will be quite random, but over the next 3-5 years, I expect the share price to follow fundamentals.

After re-underwriting Admiral 2 years ago, I sold out completely today at around 30 GPB/per share. I will do a more detialed post mortem in a few days, but the main point is that at current levels, I see a lot less upside in the stock. I am especially disappointed with the international business where very little progress has been made.

More on this mabye in 2-3 weeks.

Is there a Information about Admiral Group? I can’t find corporate news which cause the weekly performance. Thank you.

What is right? Admiral Website ex DIV 2.9.. London Stock Exchange is today ex Div.

I don’t know

Vielen Dank für Deine Antwort, hab ich wirklich bisher noch nicht gehabt. Die Firmenwebsite schreibt das und die Londoner Boerse was anderes. Kann sein, dass ich zu blöd bin das Asset zu managen, aber bei mir fliegen die morgen aus dem Depot.

Warum ist das ein Grund die Aktie rauszuwerfen ?

Admiral 6M update slightly better than expextec (run rate 1,34 GBP EPS).

Click to access half-year-results-2022-slides.pdf

Biggest concern is overall UK economy. Normally you go fishing in waters where fishes grow strongly and reproduce. But UK waters look like with little fishes and weak reproduction. :-s

Good write up as ever. I’ve looked at a few insurers, but in the current environment my concern is how quickly insurance pricing adapts to inflation – if it’s too slow then insurer earnings will have quite a drag over the next few years (you get the bills long after you’ve collected the premium), making the current share price overly attractive. Any thoughts on that?

Please excuse my comment – clearly you wrote a very extensive article on this topic I had not seen. Sorry.

No worries

Thank you for sharing your thoughts and the great work on this blog. I agree with your assessment. Have you seen any new information on self-driving cars that would be worth taking into account for the 5-year perspective? Obviously some growth funds are betting heavily on this technology and in the past you commented on the potential effect for auto-insurers. Another issue could be an oligopoly in electric vehicles, with producers one day providing a full package of services / IT and also mandatory insurance.

Oskarr,

thanks for the comment. I am not an expert but I do not expect FSD over the next 5 years. Interestingly, all these sensors increase claims as a small bump with a modern vehicle often requires significant repairs to make the sensors work again.

EV Oligopoly: I don*t believe in this story. It’s one of many Tesla stories but I don’t buy it.

mmi

Are German citizens taxed on UK dividends by the UK?

UK has no withholding tax (except REITs).