Insurance vs. Inflation & Interest rates (Admiral, Sabre, DirectLine) – Part 1

Spoiler: Readers only looking for “actionable investment advice” might skip this post as this is about the basics. The short summary is: Inflation is not good for P&C insurers.

Background: Inflation is back

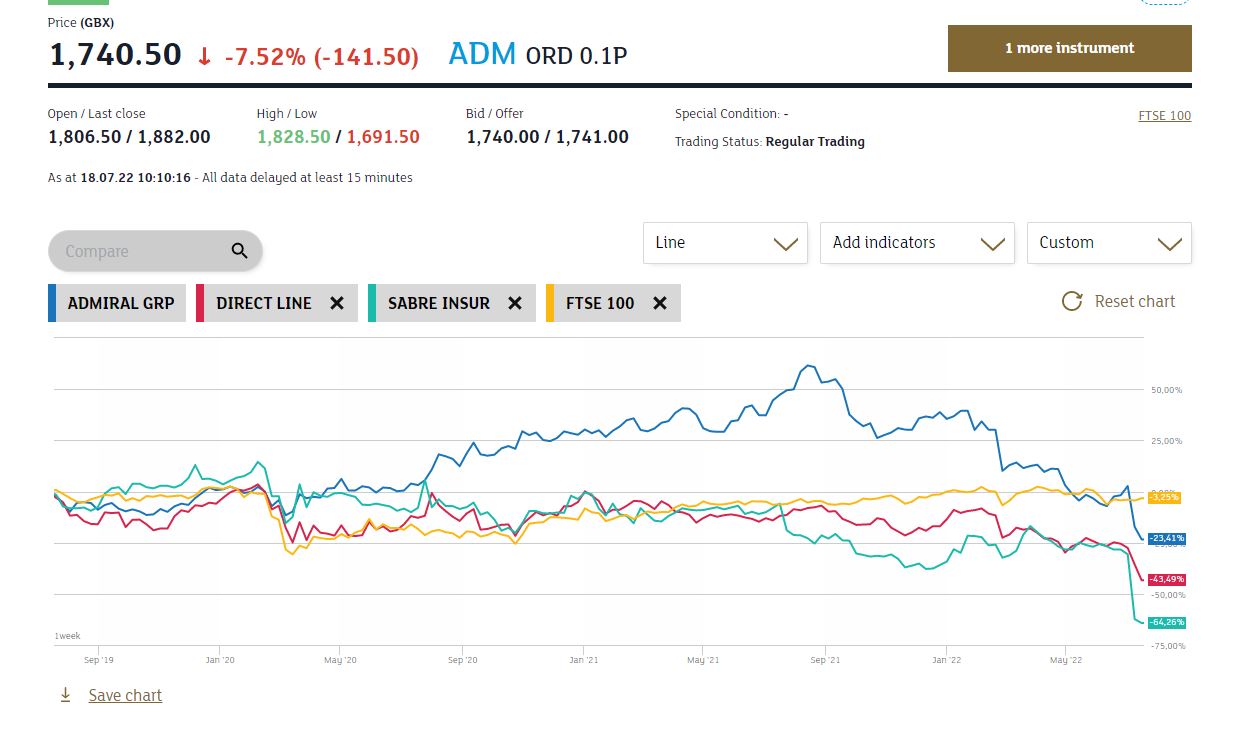

Last week, especially UK insurance stocks were rattled by news from Sabre Insurance that inflation was hurting them both, through rising claims but also rising reinsurance costs.

Sabre lost -40% that day Admiral and DirectLine were down double digits. On Monday, DirectLine, another UK direct insurer issued a very cautious Trading Update which again led to further losses. The whole disaster can be seen in this chart:

Inflation and Insurance

Inflation is indeed a problem for casualty and property insurers, especially when it is unexpected. Searching4value had some thoughts on that in his blog, although I only partially agree to his conclusions (more on that in the end).

The basic problem is that Insurance prices are usually fixed in the beginning of a contract year and can only be raised in the next period, so there is a natural “lag” in passing claims unexpected inflation to customers.

Depending on how rational the competitors are, sometimes raising prices is not so easy because competitors try to use these situations to win clients from the competition, as clients become more active and are shopping for bargains in a rising rate environment. When competition is fierce, it can last a few cycles/years until “normal” profitability is reached again and claims ratios remain high for some time.

Insurers are hit by inflation in 2 different ways:

- Claims inflation

Insurance prices are usually fixed in the beginning of the year and can only be raised in the next period.

Depending on how rational the competitors are, sometimes raising prices is not so easy because competitors try to use these situations to win clients from the competition, as clients become more active and are shopping for bargains in a rising rate environment.

When competition is fierce, it can last a few cycles/years until “normal” profitability is reached again.

In addition, sometimes Governments, regulators and/or public opinion (Newspapers) try to interfere. Although it is an extreme example, in Turkey, Erdogan has limited premium increases several times over the last years which caused significant issues for Insurers. Ireland is a good example for public opinion being very “anti-Insurance”.

I actually sold FBD because of this reason some weeks ago, because I thought they might been even more hit by inflation than Admiral. So far FBD is doing fine whereas Admiral & Co have been slaughtered.

Claims inflation in car insurance happens mostly because Auto parts get more expensive as well as the people working in repair shops cost more. In the current environment, also higher prices for replacement rental cars might play a role and used car prices are high (so replacement value is equally high).

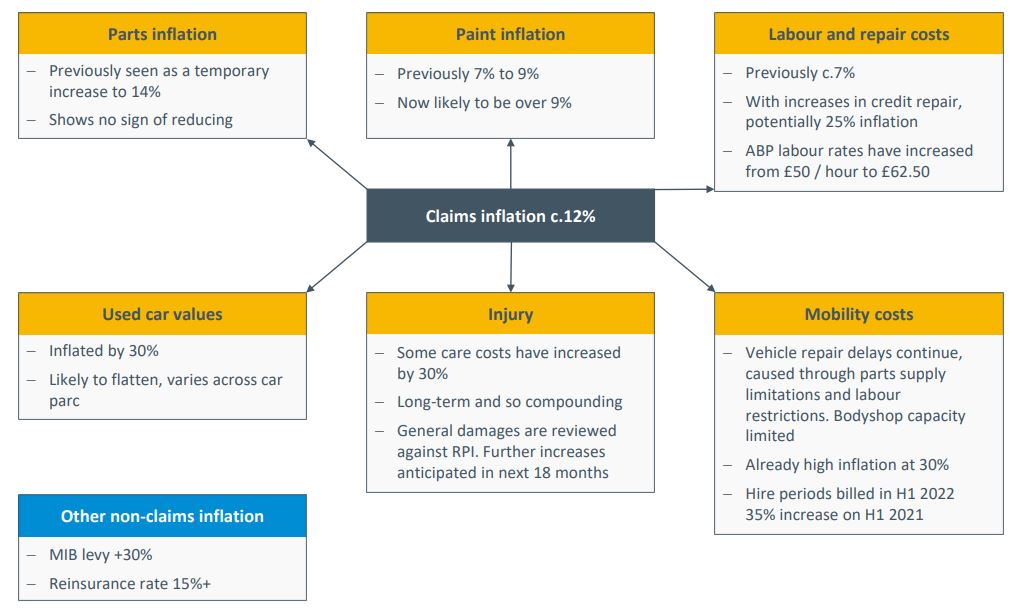

According to several sources, UK claims inflation was already around 4% higher than general inflation in 2021 and 2022 will be worse. Sabre mentioned that they see a 12% claims cost increase for 2022.

Sabre has a pretty good chart on the different cost drivers:

Overall, experts expect the UK Motor market to be technically loss making both, in 2022 and 2023.

But in general, Insurers usually adapt. And as insurance premiums are often “sticky”, subsequent periods with lower inflation lead to higher profits for insurers.

2. “Reserve inflation”

Claims inflation as such is normally quite easy to manage and rarely creates an existential threat for any insurance company, unless it has been managed recklessly.

Much more difficult is the issue for long term reserves, especially when they are exposed to inflation (as most are). For some types of insurances like liability insurance, the claim can come decades after the initial coverage was granted and the premium paid. These long term claims need to be estimated in the underwriting year by discounting with a certain interest rate but also by assuming a certain inflation level.

In the past few decades, due to declining inflation, those long term reserves have often been a source for “extra profits” through “reserve releases” as inflation turned out to be lower than expected. The main exception here were insurance policies that covered medical expenses, as they rose much faster than expected.

2a. UK Motor PPO reserves

Admiral doesn’t write long tail business but the UK motor market has one big topic which is called “PPO Claim” or “PPO Liability”. A PPO is a “Periodic payment Order” and has been introduced in the late 2000s and required the insurers in a case of a severe bodily accident, to pay for the care of a person for the rest of the life. More on that for instance here in short, before that, victims got a lump-sum payment and had the risk that this would not last until the end. Now insurers have to pay a a lump-sum plus life long payments that are indexed to relevant inflation.

The problem here is that the insurers need to reserve a Net present value on their balance sheet for both, the assumed discount rate but also the expected inflation rate. For young persons, these PPO claims can run for 50 years or more. A change in the discount rate as well as in the long term inflation rate can therefore have significant impacts on the reserve level (and Solvency) of insurers.

When these reserves need to be increased, this is at first a “non-cash” event but due to Solvency rules it limits the ability to pay out dividends or even trigger a requirement to increase capital.

The issue is of course: How big is the problem ? UK Insurers don’t report that well on PPO liabilities. There are some statistics available but in general I have not been able to find Exposure numbers for any single insurer.

One specialty of PPO claims is that the annuities are not indexed by a general index but rather a very special “AHSE 6115” index that looks at the wages of Health Care workers. The “good news” is here that this index seems to increase slower than for instance claims cost with “only” +4% in 2021. The big question is how this looks in 2022 and beyond.

2b. Reserve Inflation sensitivity

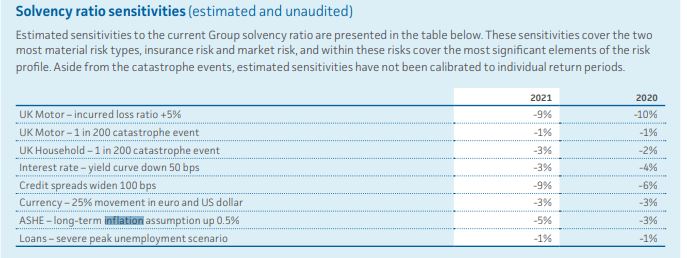

Admiral thankfully issues a table in the annual report that indicates the sensitivity this table might be the best indication:

This shows that an upward revision of 0,5% p.a. of the long-term AHSE inflation assumption results in -5% Solvency. And this is up from -3% in the year before. At the moment I do not understand where that increase in sensitivity comes from, but it is clearly not insignificant. Admiral had a 195% Solvency ratio at the end of 2021.

Even the 2021 Solvency report doesn’t really explain this increase. Although in the report they claim that (page 42):

“The Group has a relatively low number of settled PPO claims, and therefore, life underwriting risk does

not reflect a significant contribution of risk.”

The question is of course how much insurers have to raise long term expectations. there is a lot of wiggle room for insurers to delay the inevitable especially when it is an industry wide issue.

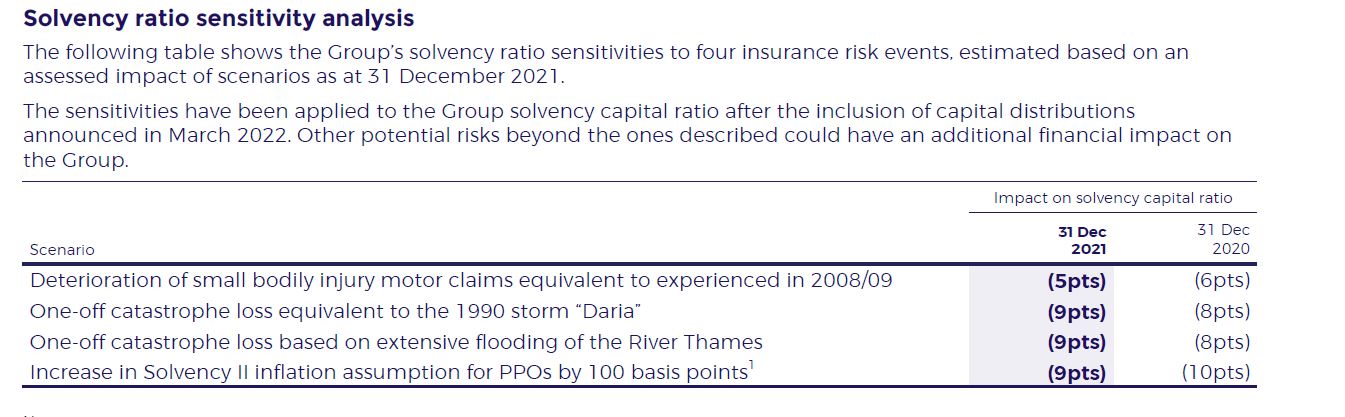

Sabre Insurance does not disclose inflation sensitivities. Direct Line does disclose inflation sensitivities and they are similar to Admiral’s, although they show less sensitivity in 2021 compared to 2020:

Just to be clear: A decrease in solvency decreases the ability to pay dividends, write new business or even require raising new capital. DirectLine mentioned that their 6M Solvency ratio was 150% and that they cancelled the second part of their buyback program. Sabre’s Solvency Ratio seems to be higher, although they gave no clear number. Admiral usually has a 20-30% better Solvency ratio than DirectLine.

Interest Rates and Inflation

Having now looked into detail how rising inflation leads to all kind of bad effects for insurers, rising interest rates are usually a net positive.

The positive effect relates both, to P&L through higher returns on newly invested funds as well as again a an effect on discounted reserves: the higher the interest rate, the higher the discount rate and the lower the NPV of the reserves.

The effect on Solvency for both Admiral and DirectLine is roughly 50% of the effect of inflation, i.e. if interest rates move up by 0,50%, for both insurers, Solvency goes up by around half compared to the same shift in inflation.

The problem in the current environment is however, that inflation is moving up faster and higher than interest rates, which means “real yields” are getting even more negative. So overall, the current environment.

Overall, the effect of higher interest rates in my opinion is not so clear, or more precise, cannot be assessed in isolation. Searching4value thinks that insurers with the highest relative investment income should do best, but as outlined above, an assessment can only be made with the full picture, i.e. the full effect of higher inflation. Especially long-tail exposures are very inflation sensitive. I tried for instance to find inflation sensitivities for MunichRe but it is “buried” under market risk.

But my assessment for P&C insurers as a whole is as follows: If inflation rises quicker than nominal interest rates, i.e. real interest rates becoming even more negative, the overall impact on P&C insurance is negative.

Second order inflation effects

Overall, the inflationary effects outlined above are also a good proxy for what is usually called a “second order” inflationary effect at a Macro level.

Insurance premiums will rise first with a delay. Secondly, Insurers will need to increase the premium both, for the claims inflation but also to compensate for the reserve increase from existing reserves and additional reserves required for long term reserves. So the rise in insurance premium will need to be higher than for the underlying claims inflation, unless shareholders “eat the difference”.

I think this applies to a lot of other business sectors as well, so I would really be very hesitant to call a “inflation top” based only on fuel or energy prices.

Summary part 1:

Looking at the issue as a whole, I do think that the current environment, with inflation increasing faster than nominal rates, is clearly an overall negative for the P&C insurance sector and for UK motor insurance in particular.

To me that is not such a big surprise, but the market seems to have been completely wrong footed from the recent announcements. Clearly, the current environment has increased uncertainty significantly for the whole sector, so just buying insurance stocks now because they are cheaper than 6-9 months ago is maybe not the smartest strategy.

It is really difficult to figure out how things develop especially if we would run into a longer stagflation period with high Inflation and relatively low interest rates.

With regard to my Admiral position, I will need to dig deeper and “re-underwrite” the position especially in comparison to the direct competition.

In general however, in this environment, Insurers with a very solid Solvency position might have an mid- to long-term advantage.

“Insurers with a very solid Solvency position might have an mid- to long-term advantage”.

Are you thinking about Protector Forsikring with its 206% Solvency ratio? ; )

I was notified about this (copy?) post: https://makefundsinternet.com/value-investing/insurance-coverage-vs-inflation-rates-of-interest-admiral-sabre-directline-half-1/

Oh my god 😖

A very bad auto-rewrite software apparently…

And there is another one https://teckinsuranceinfo.com/insurance-coverage-vs-inflation-rates-of-interest-admiral-sabre-directline-half-1/

Thanks. Yes, this unauthorized republishing is happening quite often these days.

Minimum three now for this post. Guess nowadays one can earn some money this way…

yes, unfortunately, looks like it. For sure an “AI Algo” or so….