DEME (ISIN BE0974413453) – A Contrarian Opportunity to bet on Offshore Wind

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Expectation management: If you like either/or: super cheap companies / high margins / capital light / short term catalysts / recurring revenue / low earning volatility / High dividends / share buy backs / companies with products in the supermarket → THIS IS NOT FOR YOU.

Elevator pitch:

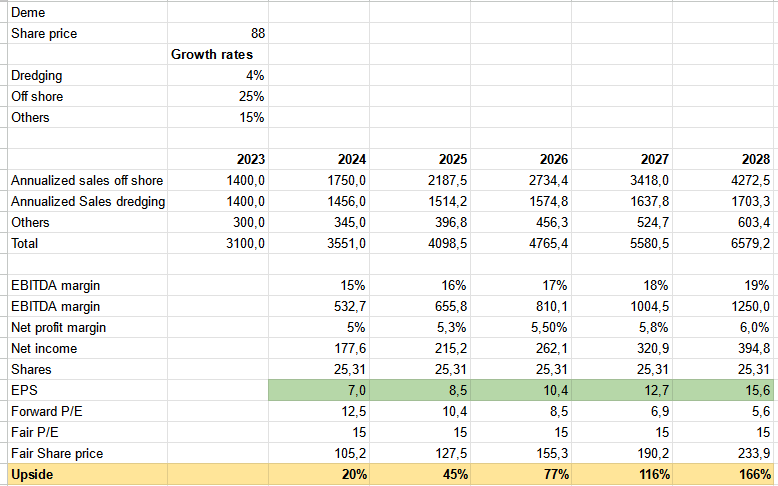

DEME, a Belgian Marine Engineering Group, is a contrarian, secular growth /mean reversion story. Current results are noisy, but growth, especially in offshore wind installation is intact and accelerating. A combination of strong growth and improving margins could lead to a tripling of EPS over the next 5 years.

As the WordPress editor still sucks for longer writups, here is a pdf version of the full writeup. Don’t worry, it’s only 18 pages and a lot of pictures of nice ships 😉

As a special service, the investment case & summary for those to lazy to read the Pdf:

Summary:

Overall, DEME is clearly not a “no brainer”. It doesn’t screen well and you really need to believe that offshore wind is not dead. However, if you look closer, I do think that DEME is a really interesting contrarian opportunity. I am very much convinced that offshore wind will grow for some time and DEME will be able to make a lot of money installing windparks for many years.

But also DEME’s other businesses are at least super solid with profit mean reversion potential. On top of this, I do think that DEME is a high quality company.

It is clearly more risky from a business perspective than my typical target company, as it is project based and capital intensive. As any capital intensive business, it could be subject to strong cycles which could negatively impact profitability, especially in the off shore space.

On the other hand I do think that some of that risk is mitigated by the large and growing order books, the global diversification and the secular tailwinds.

For the time being, I established a 3% position at around 88 EUR per share which reflects the higher risk and that I have still to learn a lot about DEME’s business..

Sold 1/5 of the position yesterday at 156 EUR. Reason: Shareprice is now at the level that I considered fair for 2026.

With a short time lag, I have to say that DEME earnings are really a positive surprise. EBITDA margins are significantly above my estimate an 2023 EBITDA is already higher than my 2024 estimate.

Their 2024 forecast would be slightly above my 2025 forecast. However, the shrare price also went up significantly, do at the moment, DEME would be fairly valued.

Offshore wind is definitely not dead. Cenergy is company that supplies cables for wind parks. Its backlog is in historical highs as its share price. It is also planning new investments to increase its manufacturing capacity.

Thanks. Never heard of them.

a ship costs 300 million euro

are you sure they wouldn’t need another one to make your 2025 estimate?

the orion and green jade are probably the ships that are responsible for the lower net margins?

I assume that more ships are needed and that DEME will keep its market share and grow with the market. This is clearly not a software business.

Just because you asked for it: “offshore wind is obviously dead!!!!” 😉 But even if it’s not dead, where does the 25% p.a. top line growth come from? As I understand it, DEME would have to increase the number of vessels, increase the efficiency of the fleet (the “billable hours/days”) or increase the day rates, right? What are the drivers of your growth assumption? And thanks for all your hard work und good investments. 😀

What do you think of Arise, from Sweden?

What do they do? Never heard of them.

Arise has three business areas: development, production, and asset management.

Project development is the main growth area for Arise, and here Arise develops greenfield onshore wind and solar projects that are later packaged and sold as ready-to-build. Arise then constructs the projects on behalf of its customers, and they are handed over to the customer once comissioned.

https://www.arise.se/

I won’t invest but thanx a lot for your reseach efforts and sharing your ideas for free.

That’s simply awesome!

Have you noticed that the listed Norwegian family company Bonheur Asa owns Fred Olsen Windcarrier (Fowic)? Fowic is quite similar to Cadeler as far as I can tell. Bonheur wanted to list Fowic in 2022 but pulled the IPO at the finish line. This wind installation vessel segment was to be listed with a 4 bn Nok post money value. In 2023 so far, the segment made 573 mNok in EBIT and they have an order book of +500 mEur.

In short, you get Fowic, quite a few wind farms, some billions in cash and a currently profitable cruise segment in Bonheur for 8,3 bn nok whereas Cadeler as a Fowic comparable trades at around 6 bn nok. Yes, Cadeler might be a bit expensive but Bonheur still seems conservatively priced to put it mildly.

Also, Wilhelm Wilhelmsen Holding (WWI) is a bit similar to Bonheur: both are closely held. WWI owns a large part of Edda Wind. That company does not own installation vessels but instead supply vessels that serve wind farms. The valuation of WWI used to be very silly but has now doubled since 8/2021, despite some governance question marks.

Thanks for the info….

Tyvm for hinting at Bonheur ASA Arne ! I started a first position today @ 196 NOK. It fits pretty good in my offshore-portfolio ( NETI, EDDA, Subsea7 ). What I liked about is pretty good diversification. Not so good is the holding character ( like WWI – here I would prefer sub WAWI much more and am holding shares of sub EDDA ) – but that is “cushioned” by a pretty large discount to NAV – if I read the numbers right.

Best regards Robert

Have you had a look at Cadeler A/S ?

Briefly, However I didn’t like it that much, especially this strange business combination.

Granted you mean the merger Cadeler/Eneti: Why do you think it is a strange business combination ? Imo they combine the newest WTIV-ships in the biggest-size-segment and will represent a market share of 60%+. Rates for these types of ships are rising – as you mentioned in your report.

As a shareholder of Eneti – soon to merge into Cadeler by December 13th – I would be very interested in a more detailed exploration – especially as Cadeler/Eneti is and will be by far the biggest competitor of DEME in the future re. WTIV’s. Besides, let me clearly express – I really do like your work and your reports !

Best regards

Robert

Should add that DEME’s core competence in offshore-wind seems to lie more in installing the foundations and the subsea-cables , so a competitor here is e.g. SEAWAY7, a division of Oslo-listed Subsea 7. But they also mention “We have an unrivalled track record in offshore wind turbine installation. To date, more than 2,700 WTGs of all types and sizes have been successfully installed by our experts, including the next generation mega turbines.”

Thanks. Yes, I think foundations is wehre they come from. In some areas you need to dredge the seaground before installing the parks.

Thanks for the inf. Might look at them again.

Agree with your take on offshore wind, though I’m playing it with other WTIV exposure.

People reading about the problems and how the industry is ‘doomed’ are missing the point; it doesn’t really matter about the industry long term, all that matters is government and investors will keep building projects for the next two decades or more. If the economics don’t eventually work out, doesn’t really matter – the rates for the vessels needed to build will skyrocket in the mean time with the limited supply available.

Thanks for the comment.