With a delay of a few calendar days against the original 2023 year end target, I am very happy to conclude the “All Norwegian Stocks” series with the final “Top 20” Watchlist.

Overall, I was somehow a little bit underwhelmed by the Norwegian stock market, at least it doesn’t offer that much of what I am interested in.

From the 270+ stocks, there is a large share of what I would call “listed early stage VC companies” that have been IPOed in the last 3 years. These companies have normally little sales and little cash left but high losses. If you pick the right one, one could make a bundle, but most of them will disappear into bankruptcy sooner or later. This is not my game. Then there are something like 40 different Sparebanken, many Shipping companies and Fish farmers that have business models where I am not 100% comfortable either.

I still managed to collect 20 stocks that I find worth watching going forward, In contrast to for instance the “All Swiss” series I didn’t find any company that I felt the urge to directly invest into (besides my portfolio holding Bouvet).

Final Top 20 Watch list

Without further intro, here are the 20 stocks that I decided are worth watching going forward (on top of my portfolio holding Bouvet ASA):

And the final batch of randomly selected Norwegian stocks. The random generator turned this into a “Salmon & Sparekassen” episode, but in between we have a few interesting ones. This was the last post with the short analysis and I am glad that I finished this in 2023. There will be another Norway Summary post in a few days. To keep the tension high, I will only reveal the next country then. Enjoy !!!

256. Aker ASA

Aker is the Top Holdco of the Aker Group, which has several other listed companies that I have covered already. Created by “self-made” billionaire Kjell Inge Rogge, Aker is valued at 4,4 bn EUR, of which 68% is owned by Rogge.

What I like about Aker is that they have very good reporting where you can easily see how the value is distributed across the Group companies. This is from the Q3 presentation:

And on we go witj another 20 ramdomly selected Norwegian stocks. This time, I found 5 of them quite interesting and put them onto the preliminary watchlist. Less than 40 companie sto go. Enjoy !!!

216. Cloudberry Clean Energy

Cloudberry is a 247 mn EUR market cap renewable energy company founded in 2017 and IPOed in 2020. In contrast to Sctaec, Cloudberry is only active in the Nordics. They develop and own and operate renewable power plants in Sweden, Norway and Denmark. Mostly Wind, but also some hydro assets and they seem also to plan to build some hybrid wind/solar parks.

Freshly motivated by Rob Vinall’s kind reference, let’s kiss more frogs in the Norwegian share market to see if we find a princess or two.. I expanded the amount of randomly selected companies to 20 per post as this allows me to finish the serieswith 4 posts overall. This time only two stocks made it on the preliminary watch list. Enjoy.

196. Reach Subsea

Reach Subsea is a 95 mn EUR market cap marine service company that seems to concentrate on “subsea services”, such as pipeline expections, reservoir monitoring etc. As far as I undestand, these services are mostly geared towards the oil and gas industry.

The stock has performed very well since a near death experience early 2020 and has made 5x since then:

And on we go, another 15 randomly selected stocks from Norway. This time, four of them made it into the preliminary watch list. Only 80 stocks more to go….

181. Circio Holding

Circio Holding is a 6 mn EUR market cap Biotech that is loss making and has renamed itself recently from Targovax. “Pass”.

Less than 100 stocks to go after this post…I took some time to continue because I lost a full post to the bloody WordPress editor. As the random generator picked some quite interesting stocks this time, I had written quite a lot. This verson is shorter, but 5 stocks are worth to “watch”. I am still optimistic to finish before year end. Enjoy !!!

166. Zaptec

Zaptec is a 175 mn EUR market cap 2020 IPO that is surprisingly trading above its IPO price. According to Euronext, Zaptec is a “technology company within Electric vehicle (EV) charging systems in Europe. The company develops EV charging systems for multi and single-family homes and office buildings.”

And on we go with yet another 15 randomly selected Norwegian share. Despite many uninteresting or crappy companies, again 2 made it onto the preliminary watchlist. Have fun !!

151. Sogn Sparebank

With around 8 mn EUR market cap, Sogn Sparebank seems to be the smallest Sparebank so far. Maybe interesting for people who live in Årdalstangen, where it is loctated, but not for me. “Pass”.

152. Aqua Bio Technology

From the name alone, I assumed that this 5 mn EUR market cap company would be a crappy 2021/2022 IPO and ….I was wrong. Rather it seems to be a crappy company that has been around for a little bit longer. The company has little income but consistent losses. “Pass”.

And on we go. With this post, I have passed the 50% threshold, so I am very optimistic to finish this before year end. This time, two stocks qualified for the preliminary watch list. Let’s go:

136. Norbit

Norbit is a 305 mn EUR market cap company has three distinct segment of which “Oceans delivers tailored technology to global maritime markets, Connectivity provides wireless solutions for identification, monitoring and tracking, while PIR offers R&D services, proprietary products and contract manufacturing.”

The company IPOed in 2019, and contrary to the 2020 IPO vintages, the share price has done quite well:

And on we go, after a small break, with a fresh batch of 15 randomly selected Norwegian stocks. This time, the random number generator selected a wide variety of businesses compared to the ususal “Fsih & Ships”. 3 stocks made it onto the watch list, one of them had been in my portfolio in the past. Enjoy !!

121. HAV Group AS

HAV Group is a 32 mn EUR market cap supplier to the maritime industry. Looking at the website, they seem to focus on at least optically on “Green” technologies, for instance electric ships and hydrogen solutions.

That all sounds very good on paper and for 2021 has translated into decent profits, but 2022 looks very different, with declining sales and disappearing profits. Q4 2022 was especially bad with an EBIT margin of -16%.

Looking at the chart, we can see that the timing of the IPO in March 2021 seems to have been perfect….for those who were selling:

And on we go after a short break with another fresh 15 Norwegian stocks, selected by the Google Sheets random generator. This time, I have identified six companies that go onto the preliminary watch list. Let’s go:

106. Instabank

Instabank is a 50 mn EUR market cap “fully digital bank that offers loan products, savings and insurance to consumers in Norway, Sweden and Finland.” The company was IPOed in 2022 and surprisingly trades slightly above its IPO price, a clear exception for the 2020/2021 IPO vintage.

Equally surprising is the fact that a relatively young “digital bank” makes a profit. They seem to lend to more “high yielding” customers but overall, they show decent growth and the stock looks cheap at 8x trailing earnings and ~6,5x 2023 earnings.

Although I am not a big fan of Nordic banks, I think this one is worth to potentially “watch”.

107. GNP Energy

GNP Energy is a 19 mn EUR market cap Energy company that has lost more than 50% since its IPO in 2020. I also found very little tangible information on this one. “Pass”.

108. Wilh. Wilhelmsen

Wilh. Wilhelmsen is a 1 bn EUR market cap “global maritime industrial group offering ocean transportation and integrated logistics services for car and ro-ro cargo. It also occupies a leading position in the global maritime service industry, delivering services to some 200 shipyards and 20 000 vessels annually.”.

Looking at the long term chart, it seems that there is significant cyclicality in Wilhelmsen’s business:

The shares currently trade at a historical high and on avery low P/E multiple. The P&L is not easy to read as the majority of net income comes from non-consolidated JVs. My gut feeling tells me that entering at the top of the cycle might not be a smart idea, however they seem to be very active in supporting the offshore wind industry. Therefore I’ll put them on “watch”.

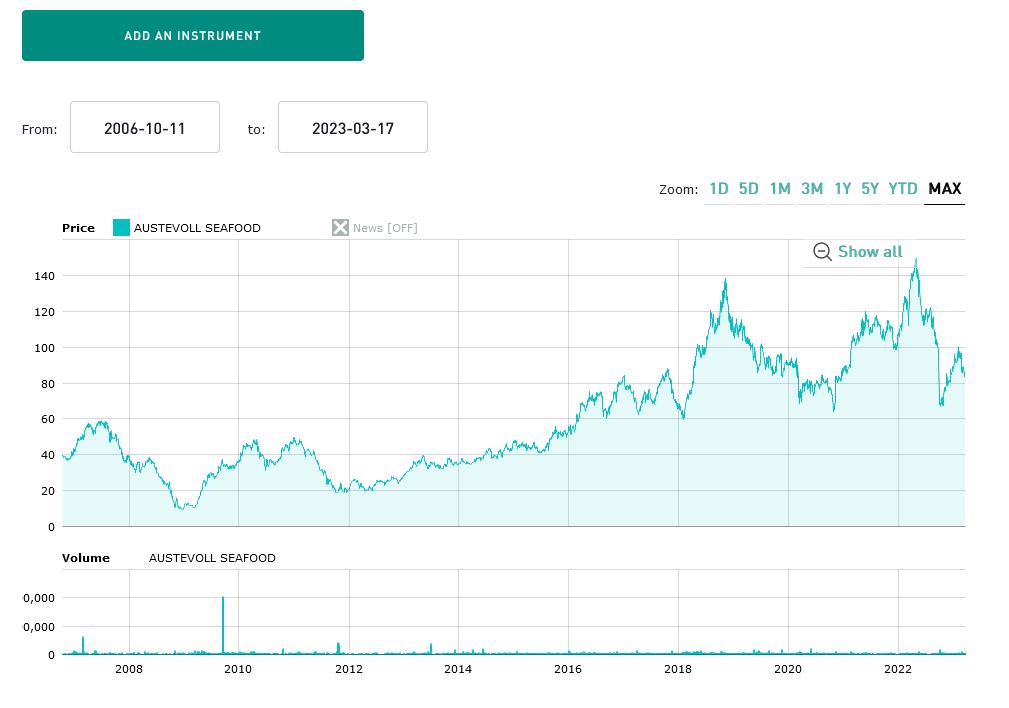

109. Austevoll Seafood

Austevoll is a 1,6 bn EUR fish farmer, which compared to the other fish players so far, is a very established player. Looking at the long term chart we see a relatively good value creation, but quite some volatility:

The stock looks quite cheap at 8x 2023 earnings, but they employ quite some leverage. I think they were also hit by the suprse Norwegian Special tax for Salmon fsih farmers. Overall, this could be one of the fish farms where one could learn something, therefore they go on the preliminary “watch” list.

110. Tysnes Sparebank

Tysnes is a 20 mn EUR local savings bank, which, not surprisingly is located in Tysnes near Bergen. The stock looks cheap, but regional savings banks are not my specialty, therefore I’ll “pass”.

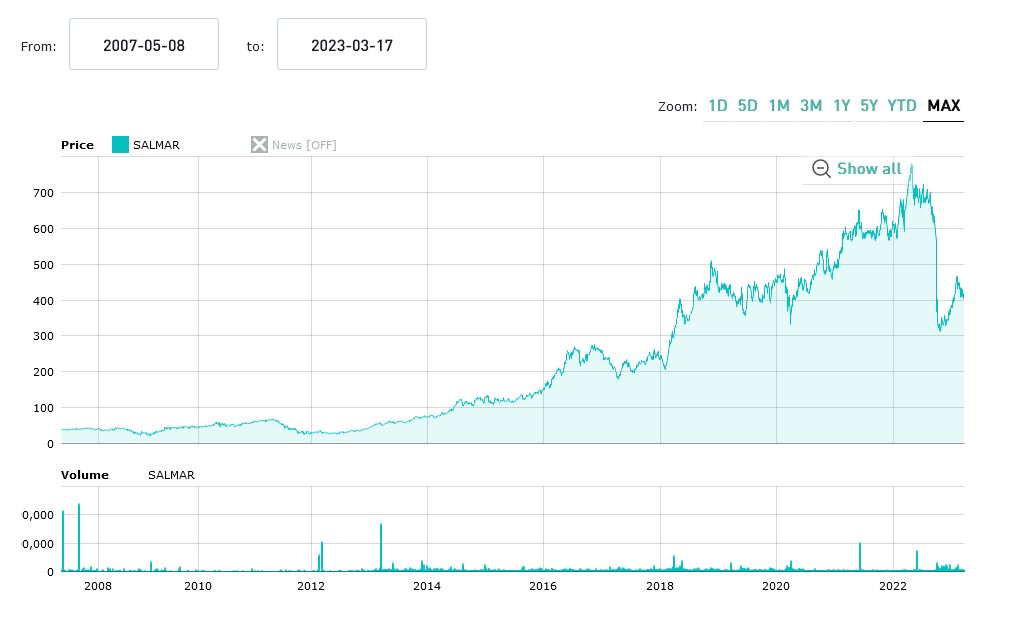

111. Salmar

Salmar, with 5,5 bn EUR market cap seems to be one of the “larger fish” among the Norwegian fish farms. The long term share chart looks impressive, despite the obvious hit from the special tax:

However, the valuation at 17,5x 2023 earnings seems to reflect this already to a certain extent. Interestingly, Salmar holds a 71% interest in another listed Norwegian company called Froy which seems to be a specialist in servicing fish farms. According to the Q4 report, they seem to contemplate selling Froy

Overall, Salmar is also a company which could be interesting to “watch” as their track record seems to be really god.

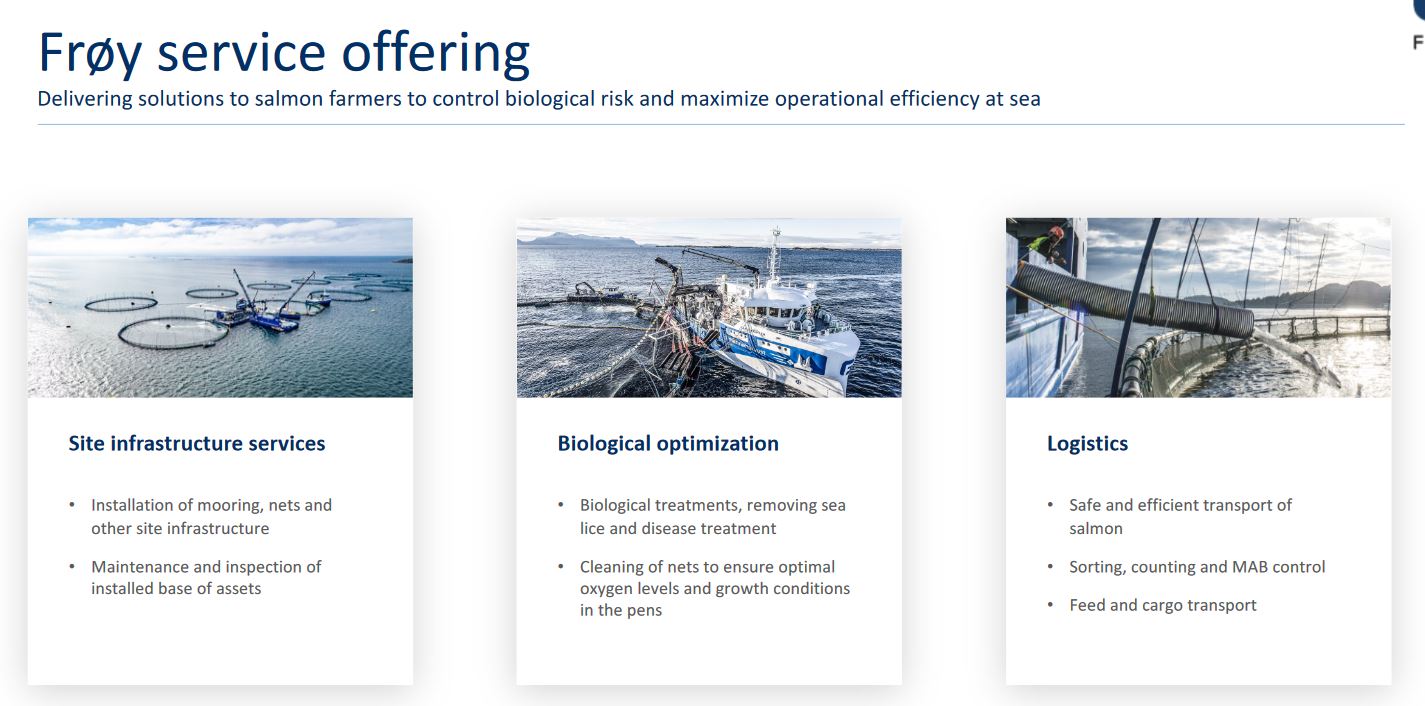

112. Froy

As a one time excepion, I follow up with Froy, a 475 mn market cap stock in which Salmar holds a 72% stake. Froy was IPOed in 2021 and its share price went on a pretty wild ride:

According to their initial investor presentation, Froy seems to be a very important service provider to the fish farming industry, providing all kind of essential services with a focus on Norway:

I guess that their focus on Norway led to the significant loss in the share price follwoing the surpise tax on Norwegian Slamon farming last years.

As mentioned in the Salmar write-up, Salmar seems to be considering “strategic options” for Froy whatever that means. In any case, I find Froy interesting, despite the fact that it is not cheap at 18,5x 2022 earnings. “Watch”.

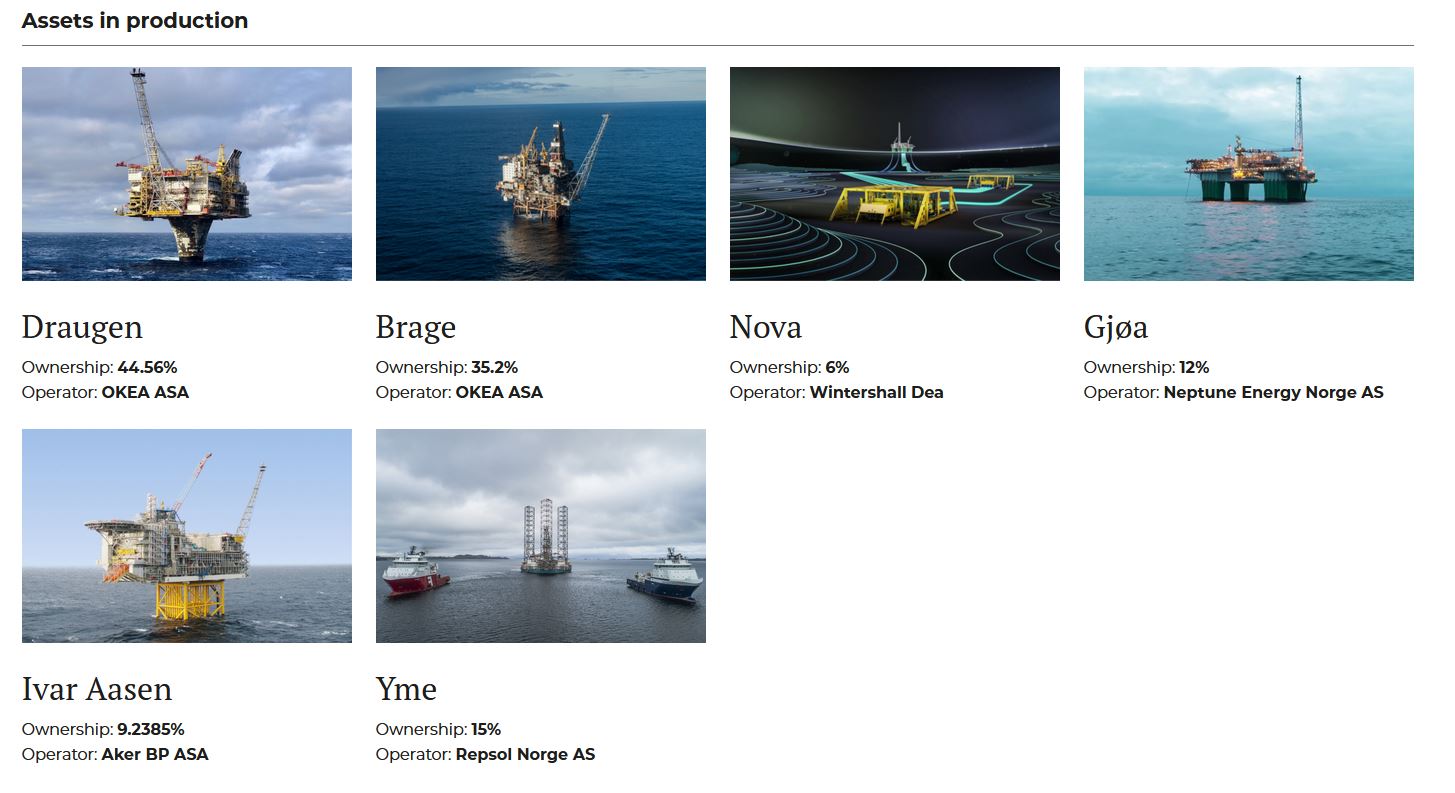

113. Okea

Okea is a 250 mn EUR market cap company that owns minority interest in several Norwegian off shore oil fields.

They seem to specialize on mature oil fields and try to extend the life of these fields.

The company was IPOed in 2020 and the share price has been fluctuation widly between 10 andf 70 NOKs:

As many oil stocks, the stock looks ridicuolosly cheap at around 2,4x trailing P/E and a big juicy dividend. However there seems to be clearly a strong leverage to oil prices which are now declining for some months. Somehow I still find them interesting bexause of their foucs on Norway, therefore they go on “watch”.

114. Techstep

Techstep is a 37 mn EUR market cap company that seems to hav had its best time in the early 2000s, although the current business model seems to have impmented only in 2016. The company seems to offer some mobile services, but only achieved to have a positive operating result in 2 out of the last 6 years. “Pass”.

115. Sparebanken 1 Helgeland

This is a 324 mn EUR market cap regional savings bank that looks quite profitable- The stock has performed quite welll since the GFC and is not too expensive (P/E ~10,5). However. local banks are out of scope for me, “pass”.

116. Agilyx

Agilyx is a 228 mn EUR market cap company that is active in chemical plastics recycling. As a 2020 IPO, the stock trades around the IPO price, which can be considered a succes for this vintage.

As one can expect from a young cleantech company, they are loss making, although they do have sales, currently a run rate of 15-20 mn EUR. However gross margins are negative for the time being and they are burning cash.

The main shareholder is a fund called “Saphron Hill Ventures” and as many such companies they have an impressive list of strategic partners (Exxon etc.). They seem to operate a JV with Exxon in the US called Cyclix, that recycles plasticand another project seems to be in construction in Japan

Plastic recycling is an interesting topic, however a negativ gross margin really turns me off, therefore I’ll “pass”.

117. Aurskog Sparebanken

Aurskog is a small, 89 mn EUR market cap local savings banklocated in Aurskog near Oslo with no specific aspects at a first glance. “Pass”.

118. SATS

SATS is a 110 mn EUR market cap fitness chain that is active across Scandinavia. The company IPOed in 2020 and lost around -75% since then, indicating that not all is great.

The main reason might be that since their IPO, they have not been able to genrate a profit. The company has significant debt, although they managed to lower the debt burden over the past 3 years.

Because of loan covenants, the company is not allowed to distribute dividends and Q4 2022 was not great, most likely due to electricty and heating costs.

At an EV/EBITDA of ~5,5 this might be interesting for turnaround specialists, but for me the risk is much too high, therfore I’ll “pass”.

119. Nykode Therapeutic

Nykode is 570 mn EUR market cap “clinical-stage biopharmaceutical company, dedicated to the discovery and development of vaccines and novel immunotherapies for the treatment cancer and infectious diseases. Nykode’s modular platform technology specifically targets antigens to Antigen Presenting Cells.” Nykode was only profitable in its IPO year 2020 and has been making losses in 2021 and 2022.

As far as I understand, they are using a different technology to MRNA, but they have some interesting cooperations and Cash should last for a couple of years. However, Biotech is far out of my circle of competence, therefore I’ll “pass”.

120. Wallenius Wilhelmson

By coincidence, this 3 bn EUR market cap company has been selected in the same part of the series as Wilhelm Wilhemsen. And indeed, the companies are related as Wallenius Wilhelmsen seems to be a JV between Wallenius and Wilhelmsen, specialising in owning and operating ships that transport cars.

As other shipping companies, the stock did quite well, doing ~11x since the bottom in MArch/April 2020. The stock looks really cheap at a P/E < 5, but buying cyclical stocks at the margin peak is rarely a good entry point. As I have Wilhelm Wilhelmson already on watch, I’ll “pass” here.