Quick Updates: Frosta 6M 2026, Paypal vs. Stripe&Advent, Easyjet spectacle & DCC “Sweetener”

Frosta

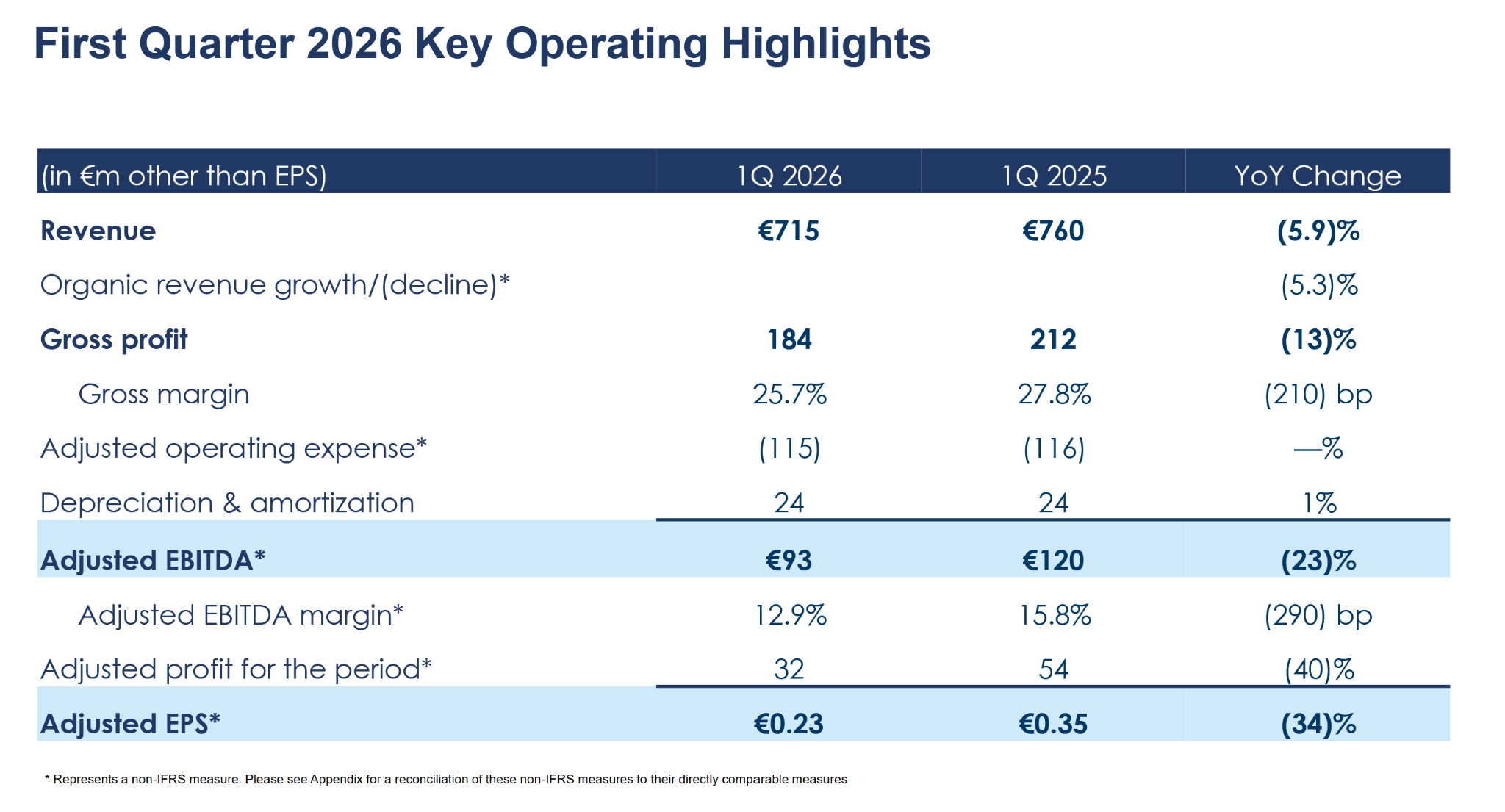

Frosta, the German “Hidden frozen Food champion” that I wrote up in February already released 6M results this week.

Highlights:

Overall sales volume increase by +11,7%. easily beating the market which was around +3%. The real kicker is that the Frosta Brand itself grew by +25% and seems to be further accelerating.

Among other things, Frosta has released two new lines of frozen meals: “High Protein” meals with more meat and “a la carte” restaurant quality meals. Both new lines are at a slightly higher priced point than the original.

I find this a clever strategy, not to increase the prices of their classic range but rather offer even better meals at a higher price point.

After tax income only increased by 2,4%. Gross margins increased a little from 48,3% 6M 2025 to 48,8% in 6M 2026, net income margin declined slightly from 5,5% to 4,9%.

However, the outlook for the full year is VERY positive.

If we take the two midpoints, 13% sales increase and 6,5% net margin, we would end up at 50 mn EUR net profit or an EPS of 7,35 EUR.

Considering that Frosta has ~10 EUR Net cash Cash per share, this translates into 13x P/E for a strongly growing company that is executing extremely well.

If we just compare this with the self proclaimed “Leading European Frozen Food” company Nomad foods, we can clearly see from whom Frosta is taking market share:

As always, Investors were not impressed very much:

I used however the opportunity to increase my Frosta position from 3,2% to 4,5%. And I will keep buying if the share price remains below 100 EUR.

Forsta is in my opinion one of these typical “Peter Lynch” investments: As a german, you can easily go into a supermarket, look how empty the Frosta Shelfs are and buy yourself a few packs to test the quality you get for the rather moderate price.

Paypal

In March I wrote about Paypal and just found it “too hard” for me, given my limited knowledge in the Payment sector.

Even back then, the rumor was that Stripe might be interested in Paypal but I found it not really realistic as there was a limited fit:

Now the Stripe rumour has resurfaced but with an interesting “twist”: Stripe and PE giant Advent (100bn AuM) seem to have teamed up offered 60,50 USD per share for Paypal, however the Paypal Board seems to have rejected that bid as too low.

The share price jumped to around 57 USD, leaving only a 5-6% spread. which indicates that some arb players seem to expect and price in an increased offer.

As it is quite early in the process, I will keep watching this. If the price goes down a bit and we would see a spread closer to 10%, this could be a potentially interesting special situation.

From a structural perspective, teaming up with Advent makes a lot of sense for Stripe because then they can choose exactly the parts that they like and Advents monetizes the rest.

Advent also just has closed fundraising for its 11th flagship fund with a total of 26 bn USD in Commitments, so they do have some decent firepower.

Easyjet

Talking about increased offer: On June 29th, I had written about Castlelake’s attempt to take over Easyjet. Back then the stock was trading at 5,72 GBP and Castelake had increased its bid to 6,50 GBP.

On July 5th, Easyjet approved then an increased offer of 6,90 GBP. And only 2 days later, suddenly Apollo showed up with a 7,15 GBP bid.

Easyjet’s board quickly supported that offer and Apollo has now time until August 7th to come up with a formal bid.

So buying Easyjet back then would have been a good idea, but the Apollo move was clearly not easy foreseeable.

Interestingly, the spread this time is very small, so it seems market participants are expecting a higher counterbid from Castlelake.

In general, the UK market seems to be running hot with takeovers, Rotork/ABB is another example.

DCC

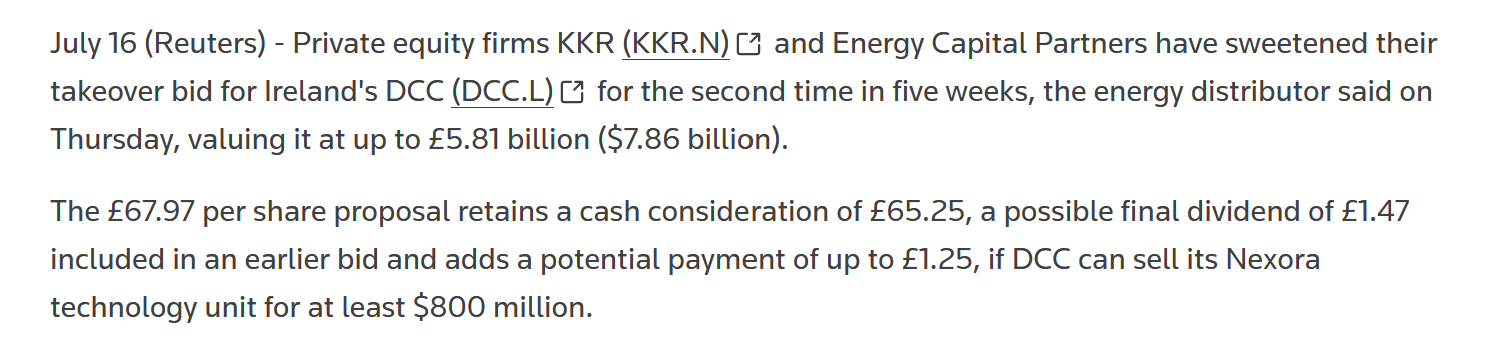

Finally a small update to DCC: KKR and DCC have now added a “Sweetener” to the deal: If DCC manages to sell its US Audio distribution business, shareholders will get an extra 1,25 GPB per share:

July 27th is now the new stop date for KKR to formalize the bid.

Danke für das teilen deiner Gedanken zu Frosta. Ich bin bei der Frosta immer etwas zurückhaltend, weil der CEO eindeutige Prioritäten setzt und da kommen wir Aktionäre nur als notwendiges übel vor.

An was genau machst Du das fest ? Frosta hat u.a. sehr viele Belegschaftsaktionäre und unterstützt das mit einem eigenen Programm. Meines Erachtens ist Frosta eigentlich sehr transparent und agiert langfristig zum Wohle der Aktionäre.

FRoSTA – is there some hidden german word play behind the name? The name together with the logo looks like they are selling finger paint to children. At least to someone used to Scandinavian brand estetics.. Trying to move past my biases 🙂

I am not aware of any hidden meaning. The company used to be named “Nordstern Lebensmittel” (Northstar Groceries) from which the ticker NLM wss derived.