All Norwegian Stocks Part 9 – Nr. 121-135

And on we go, after a small break, with a fresh batch of 15 randomly selected Norwegian stocks. This time, the random number generator selected a wide variety of businesses compared to the ususal “Fsih & Ships”. 3 stocks made it onto the watch list, one of them had been in my portfolio in the past. Enjoy !!

121. HAV Group AS

HAV Group is a 32 mn EUR market cap supplier to the maritime industry. Looking at the website, they seem to focus on at least optically on “Green” technologies, for instance electric ships and hydrogen solutions.

That all sounds very good on paper and for 2021 has translated into decent profits, but 2022 looks very different, with declining sales and disappearing profits. Q4 2022 was especially bad with an EBIT margin of -16%.

Looking at the chart, we can see that the timing of the IPO in March 2021 seems to have been perfect….for those who were selling:

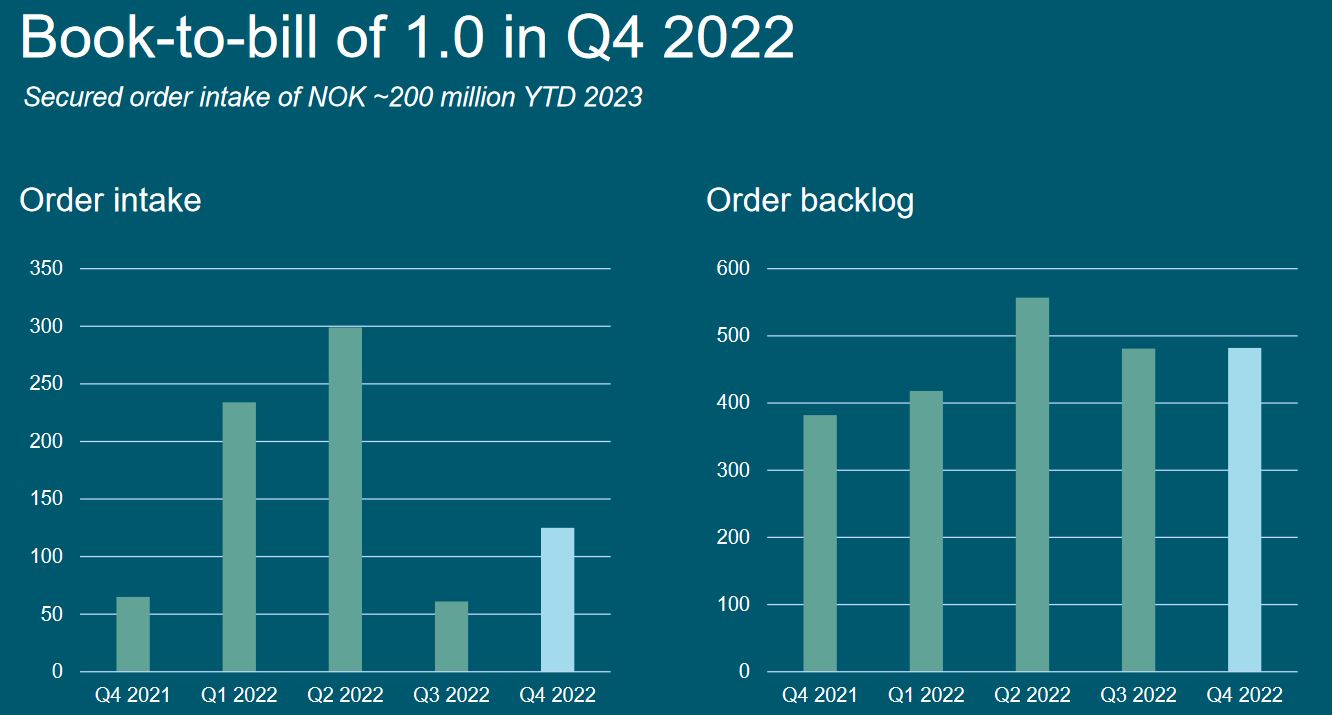

Looking at the order book, things are not really booming either:

The company does give an optimistic outlook for 2025 but nothing really for 2023. In theory, the business looks like a great opportunity but for some reason things are not really improing. On the plus side, they don’t have financial debt as of the end of 2022.

I’ll put them onto the “watch” list but it is not a very strong candidate.

122. Nordic Halibut

Nordic Halibut is, as the name says, a 60 mn EUR market cap fish farmer that specialices on Halibut. Again, a 2021 IPO, the company trades around -20% vs the IPO price. The company does have sales, but losses are almost as high as sales and the business model seems to be still in a relatively early phase. Although I do like Halibut on a plate more than Salmon, I’ll “pass”.

123. Integrated Wind Solutions ASA

Integrated Wind is a 113 mn EUR market cap company that owns 6 ships that service the offshore wind industry. The company was incorporated in 2020, IPOed in 2021 and trades ~15% below the IPO price.

As promised a picture from the ships:

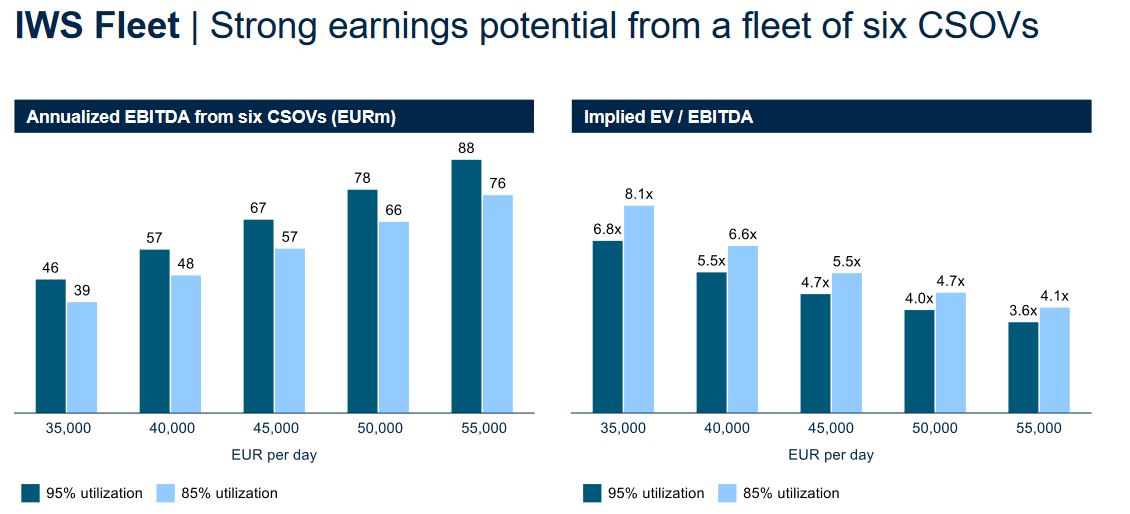

The company has been losing money in 2022, however based on their presentation, the future looks (of course) quite good. This is hwo they see their valuation based on prices to be achieved:

I have to say that this is the first Shipping company that I find remotely interesting, therefore I’ll put them on “watch” but again a weaker one.

124. Sparebanken 1 SMN

Sparebanken 1 SMN is a 1,5 bn EUR market cap savigs bank headquartered in Norway. Interestingly, looking at the share price, shareholders of this bank might be the happiest banking shareholders in Europe, making 7x over the past 20 years. At around 9x earnings and 5% dividend yield, th stock doesn’t look expensive. I have no idea what these guys did differently to any other bank in Europe, maybe is hould try to find out at some time, but at the time being I’ll “pass”.

125. Grong Sparebank

With 50 mn EUR market cap, Grong is clearly one of the small savings banks and surprisingly located in a City called Grong. Nothing to see here for me, “pass”.

126. Sparebank 1 Nord-Norge

The random generatr is tormenting me with Sparebanken. This one has a a market cap of 820 mn EUR, operates from Tromsoe and concentrates on Northern Norway. The stock has also a decent long term performance, but less spectacular than SMN. Valuation is similar, with a slightly higher dividend yield. “Pass”.

127. Airthings

Airthings is a 43 mn EUR market cap company that is in pricnple active in an interesting area, dealing with “air quality sensors and hardware-enabled software products for air quality, radon measurement, and energy efficiency solutions worldwide.”

As an opportunistic, end of 2020 IPO, the share lost ~-70% from the IPO price. 2022 showed only little growth after a big jump in 2021, but losses are increasing and inventory is piling up. The company issued shares early in 2023 and reduced their 2024 outlook. Overall, despite an interesting business, this looks a little bit too shaky for my taste. “Pass”.

128. ELMERA Group SA

ELMERA is a 173 mn market cap electricity distributor and mobile phone provider that doesn’t own a grid/tework and doesn’t produce electricity. As such, the basically buy wholsale and sell retail. So it is not a big surprise, that 2022 was tough for them. Looking at the chart, we can see however that things seem to have worsened already earlier in 2020:

The company grew a lot in the past few years, but margins are razor thin and debt is substantial. “Pass”.

128. Induct

Induct is a 10 mn EUR market cap company that offers some kind of project collaboration plartform. The stock is thinly traded, the company is loss making for the last 6 years or so and all in all doesn’t look very interesting. “pass”.

129. Aker Horizons

Aker Horizons is a stock that actually had been in my portfolio but I exited it a few months ago as I reduced my Renewables exposure. Aker Horizon has a market cap of 540 mn EUR and covers everything within the wider Aker Group that is related to Climate and Energy transition.

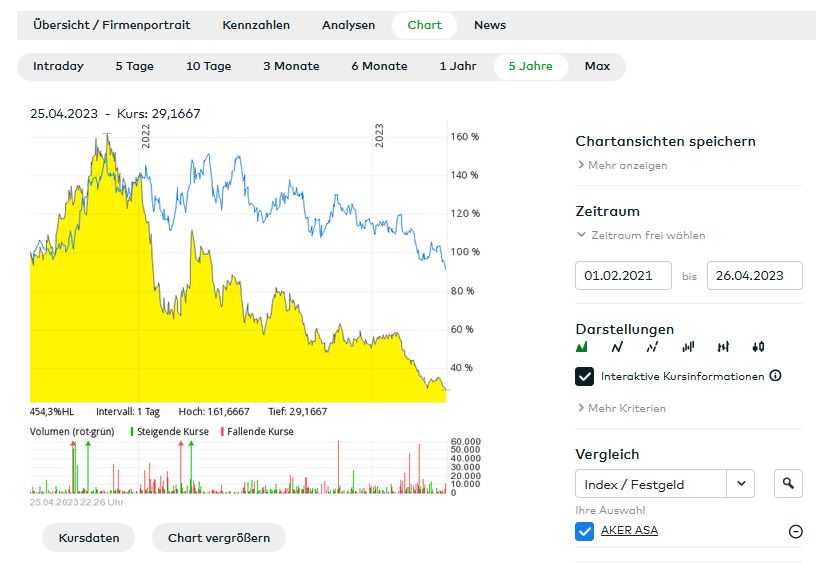

As we can see in the stock chart however, after in initial jump, the stock price is on a long way down since its IPO in Ferbuary 2021:

One reason for the declining share price is clearly the frantic reorganization. Initially, Aker listed 3 additional subsidiaries, Aker Carbon Capture, Aker Offshore Renewables and Aker Hydrogen. However, Aker Offshore and Aker Hydrogen have been taken private in 2022 with significant losses for the shareholders with only Aker Cabon Capture remaining listed.

The P&L of Aker Horizon is really hard to analyze at it is mostly a development company with a lot of expenses upfront and little operational revenue and/or profits.

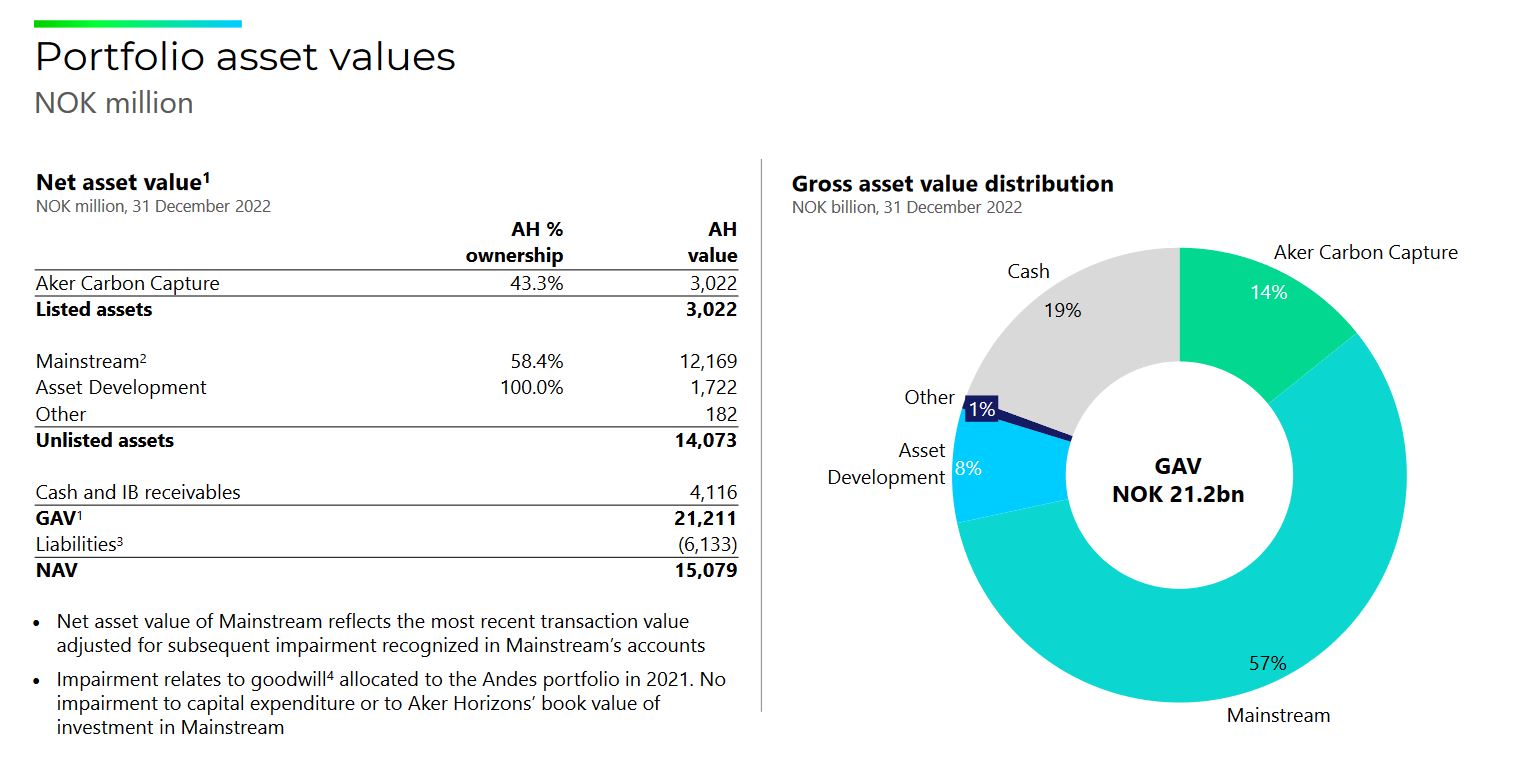

From the Q4 presentation, the most interesting slide is how they report their NAV :

Their NAV of ~1,3 bn EUR is significantly above the market cap, put partially relies on historical valuation (Mainstream). Overall, I still find it very interesting and Aker Horizon remains on the “watch” list with a high priority.

130. AMSC ASA

AMSC is a 255 mn EUR market shipping company that “operates as a ship owning and lease finance company in the United States. The company is involved in the purchase and bareboat chartering of product tankers, shuttle tankers, and other vessels to operators and end users in the Jones Act market. It operates a fleet of nine product tankers and one shuttle tanker.”

The Jones Act is a US law that only allows US based ships to operate within a certain distance of the US coast and therefore protects these ships from any foreign competition.

As many shipping stocks, the stock looks cheap but they carry a lot of debt and the stock did nothing for the last 10 years. I am also not sure if owning ships as such is a really good business, even when protected through the Jones Act. “Pass”.

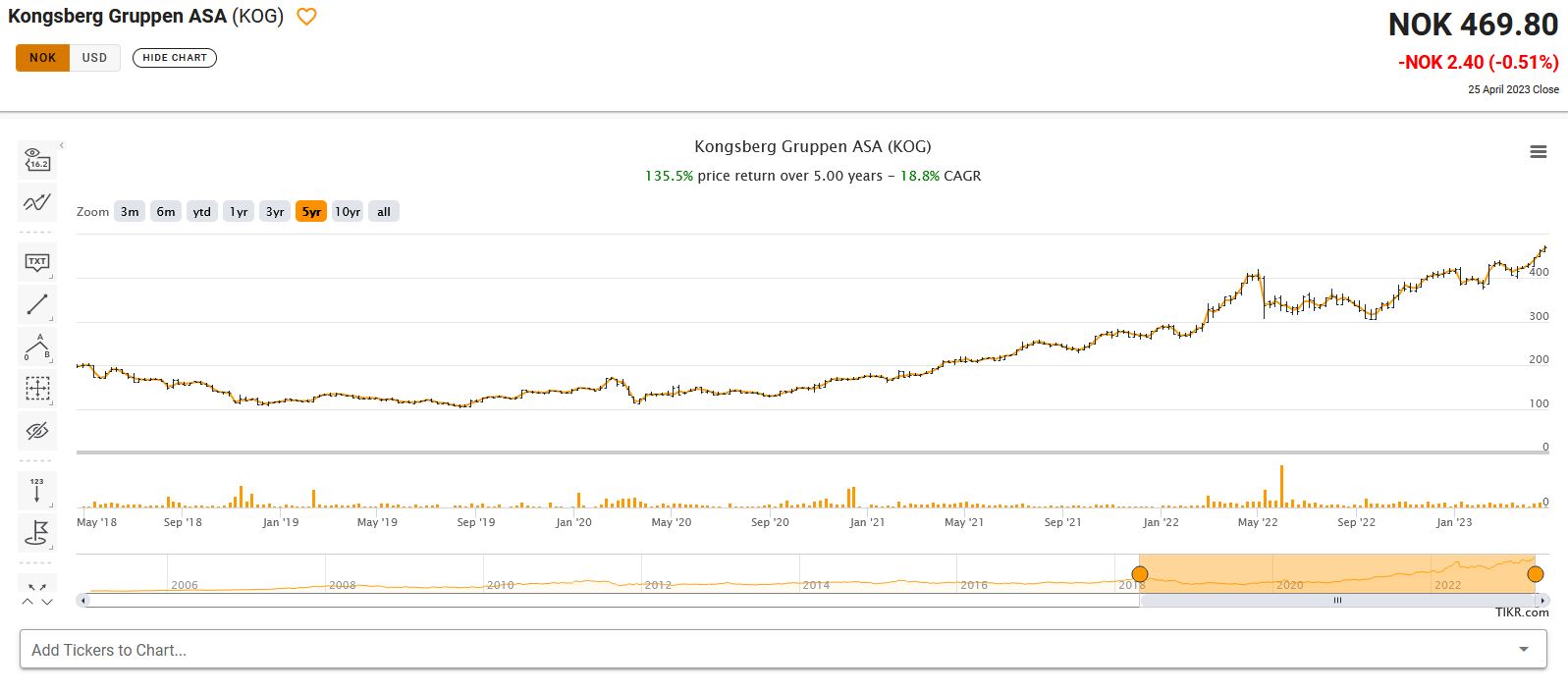

131. Kongsberg Gruppen

Kongsberg Gruppen is a 7,3 bn EUR market cap Technology Group that is active across a wide range of sectors such as marine and aerospace with a focus on defense and military technologies. The stock has been performing well, doing 19% CAGR over the last 5 years:

This is supported by a strong increase in operating profit and EPS after a slump in 2017 and 2018. It seems that as a defense stock, a lot of things currently go into their directions.

However the stock now also looks quite expensive at 30x P/E and 25x EV/EBIT. The Norwegian Government owns 50% of the shares. As I have no real angle on this, I’ll “pass”.

132. PGS ASA

PGS aka Petroleum Geo Services, is a 626 mn EUR market cap company that is active in the collection of Geological surveys for the Oil & Gas industry. In contrast to competitor TGS Nopec (which I woned some years ago), PGS still owns its own ships which makes it a capital intensive, leveraged and therefore vulnerable cyclical business.

PGS had to raise frequently capital and the share price is super volatile. Not my area of interest, “pass”.

133. Norsk Titanium

This 73 mn EUR market cap company is, as the name indicates a “producer of aerospace-grade, additively manufactured, structural titanium components for commercial aerospace tier one suppliers”.

Unfortunately, the production seems very small, with revenues less than 100K EUR for 2022 and now growth but increasing losses. As many of its peer 2021 IPOs, this seems to be more a venture investment. “Pass”.

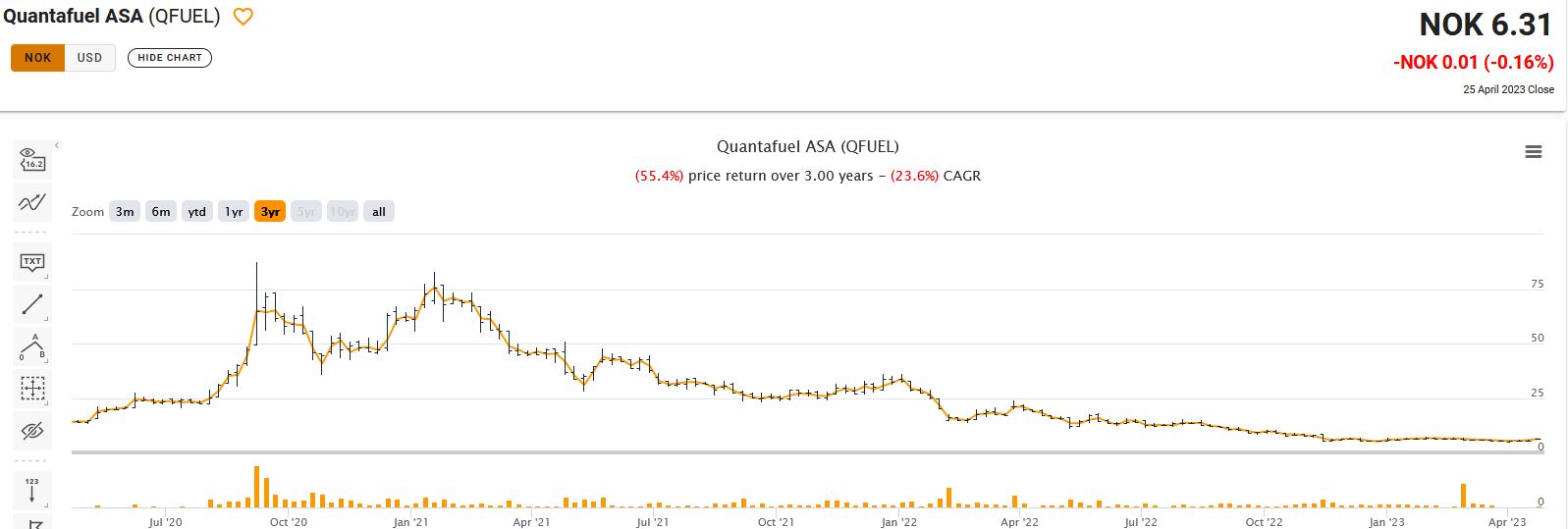

134. Quantafuel

Quantafuel is a 92 mn EUR market cap “Cleantech” company that aims to recycle plastics into useful raw materials by chemical processes. Quantafuel was IPOed actually just before Covid hit and the stock participated in the “Covid hype” before than declining far below the IPO price:

In February 2023, Quantafuel received a take-over (or take-under) from KKR at a price of 6,38 NOks per share and the two largest shareholders have alreay agreed, representing more than 40% of the shareholders.

Looking at the current price, it seems that the likelihood of the deal going through is quite high, therefore I’ll “pass” although the space as such is interesting.

135. Nordic Mining

As the name says, Nordic mining seems to be active in mining operations in the Nordic. The company has a market cap of 105 mn EUR. As far as I understand, they are at a relatively early stage and started developing the sites, but had to do a capital raise in March in orther to finance the next step. Mining is clearly not my circle of competence, therefore I’ll “pass”.

Your picture of the ships is computer animated. Integrated Wind Solutions will get their first ship on the water in Q4-23. The fleet shown in the picture will be complete in Q4-25. This of course only in case if everything goes according to plan. IWS will need at least one more private placement to get the financing for those ships in place. This is the way the Awilhelmsen group runs their startups (e.g. Awilco LNG or Awilco Drilling).

Awilco Drilling by the way is an example in which not everything went according to plan.

If you are interested in service providers for the offshore wind industry, you may want to instead consider one of the two main competitors: The Danish Esvagt is owned by i3-infrastructure plc. The Norwegian Edda Wind has J. Fredriksen and the Ivan Ofer family among its main shareholders. Both companies have vessels on the water (9 resp. 5) which are built in European shipyards, not in Chinese ones as the IWS-vessels.

Idan Ofer of course.

Thanks for the comment. Took them off the watch list….

Elmera used to be listed as Fjordkraft a few years ago, before a big scandal because of price shenanigans (https://e24.no/boers-og-finans/i/GaGvxV/fjordkraft-beskyldes-for-aa-lure-kunder-storaksjonaer-tar-kritikken-alvorlig). I had a small position but sold right away, despite a decent gain.

It’s also one of the most hated utilities in Norway https://www.bytt.no/erfaringer/strom/fjordkraft/mjjejw/variabel-pris-skandale

Wow, most hated utility is indeed something