Samse Group (ISIN FR0000060071) – A Hidden French Compounder that is as exciting as watching Paint dry ?

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

As in the past, due to the bad WordPress editor, I’ll post a summary here and attach the full write-up as PDF.

After teasing a new position in the Nabaltec “Post Mortem”, I proudly present the next (hopefully) super boring company for my boring portfolio.

SAMSE SA is a French company that distributes building materials to “professional” customers like contractors, craftsmen etc. It also has a smaller “Direct to consumer” DYI store segment, which represents around 20% of sales. Samse is active only in France and No. 2 after Saint Gobain, which, however is much bigger even only in this specific sector (2000 outlets vs. 350).

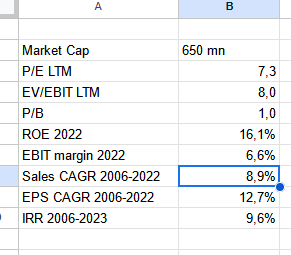

Here is an overview of relevant “KPIs” at a share price of 190 EUR (time of writing):

PDF file with detailed write-up:

Pro’s and Con’s

What do I like:

- Family owned/controlled

- Exceptionally high employee ownership

- Conservative financial profile and business model

- Countercyclical M&A

- Decentralized organization

- Very good company culture

- business that I kind of understand (distribution)

- not attractive at first sight

- potential “soft catalyst” through acquisition in tough times

- reasonable valuation

Risks

- Still Leverage on Holdco level

- maybe over earning in 2021 and 2022

- Cycle in building materials might still get worse

- low free float

- adds to my sector exposure (Thermador, Sto, Solar)

- For some reason, they have discontinued English reports from 2018 onwards

Summary:

SAMSE seems to be one of those high quality “hidden Champion” companies that I am always looking for. The business is extremely boring and subject to economic cycles. On the other hand, the company seems to be very well managed and they seem to be able to use the cycles to get out stronger from the lows than they entered.

I decided to allocate a 3% position into SAMSE at an average price of 190 EUR per share, funded mainly by the sale of the Nabaltec position. The 3% reflects my current exposure to the sector.

Honestly, I do not expect a great and quick run up of the share price. I actually hope that the share price does very little and that I can add if fundamentals slowly get better over time like in the Schaffner and Meier Tobler case.

Sources:

A big thanks especially to Jeremy from “French Hidden Champions” and Philippe Luchesi. Both guys are worth following if you are interested in quality French stocks.

Philippe on SAMSE:

Jeremy on SAMSE:

https://frenchhiddenchampions.substack.com/p/sfaf-analyst-meeting-report-samse?s=w

A recent interview with the CEO:

I finally sold my last SAMSE shares. Why ? At current interest rates, I do not see a quick turnaround in the European construction sector. As I have local French exposure with Thermador anyway, I decided to sell the stock with the lower conviction. It’s still a good company I guess. Maybe I am selling right at the bottom, but who knows ?

Hello,

How are you thinking about the H1 Samse results released yesterday.

Buying opportunity at the reduced share price ?

SAMSE reported 2023 earnings yesterday.

https://live.euronext.com/en/node/12390860

EPS ~22,27 EUR per share, in line with market expectations.

Why do you add the dividend yield in your expected return calculation? If ROE remains constant, earnings growth should be proportional to RETAINED earnings. Hence, higher dividend yield, lower earnings growth and vice versa!?

Sorry, I think I got it. In the past they were able to achieve a certain earnings growth (12,7%) AND pay a dividend (4%) as basis for your own expected return calculation.

Exactly.

Saint Gobain at its 3Q results talked about how the French government is supporting the renovation mkt which should help your Samse position.

“The announcement by the French government in October that it is to double its MaPrimeRénov’ household renovation stimulus package to €5 billion in 2024, along with its objective of a three-fold increase in the number of complete renovations to 200,000 per year from 2024, illustrate the country’s commitment to accelerate energy-efficiency renovation of existing buildings”

Thank you very much. Let’s hope a few breadcrumbs remain for SAMSE 😉

As is implied by your positions the sector seems cheap. I know you did invest in German Hornbach in the past. Why is SAMSE the better business? The higher ROE of SAMSE shows better efficiency despite low leverage. But the advantage seems to have narrowed somehow since the financial crisis. B2B maybe better due to higher switching costs than the mostly B2C of Hornbach. Did you look into the multiples of SAMSE’s peergroup? I think your focus an absolute valuation is great, too. [I am long Hornbach]

I used to own Hornbach, too. Esp. In France, I do think that the B2B Sector is more interesting due to the many regional players. D2C imo is more concentrated and more competitive. Harder to gro through acquisitions.

What happen is 2020-2022… growth was almost non existent from 2012 to 2019… in terms of operating income.. around 50m rolling 12mo from 2012 to 2020 june.. then a sharp rise to 120m now 110m. That would be my concern. Is the growth a one-off event

As I mentioned, if you are looking for smooth growth every year, this is not the stock for you. Also France had to go through a period that was commonly called the “Euro Crisis”. Time will tell.