Electrica S.A. (ISIN US83367Y2072) – A deeply discounted infrastructure stock from Romania ?

Again, this has turned out to be a long post. So a quick “executive summary” upfront:

Electrica S.A. looks like an interesting play on infrastructure in Romania. The stock is attractive as

– the current valuation is cheap compared to grid companies in Spain, Portugal and Italy

– the underlying business (electrical grid monopoly) looks structurally attractive due to high guaranteed returns on investment

– there is good visibility on growth for the next 5 years

Overall, based on relatively conservative assumptions, an investor could expect to earn 17-21% p.a. in local currency over the next 5 years.There are clearly lots of risks (regulatory, politically) but overall the risk/return profile looks good and the risks are less correlated to overall market risks.

DISCLOSURE: This is not an investment advice. Do your own research !!! The author may have already invested in the stock prior to publsihing the post.

When analyzing Romgaz I said this:

Why Romgaz ? Well that one is easy: This is the only Romanian stock you are able to invest if you don’t have access to the Bukarest Stock Exchange. There are no ETFs on Romania either.

Well, that was wrong, because another formerly Government owned Romanian company IPOed in June this year on the LSE, the grid operator Electrica.

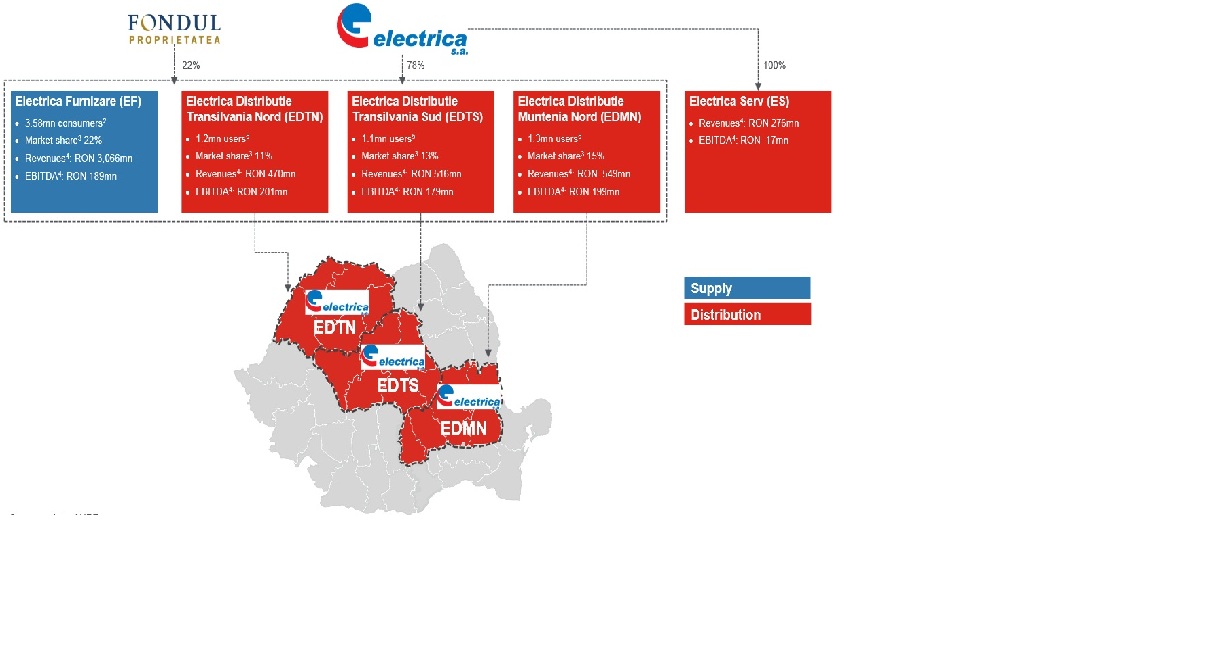

Electrica – the business

![]()

Electrica’s main business is owning and running the electrical grid in an area covering ~40% of Romania. Additionally, they are also an electricity supplier, however they do not generate any power. This graphic from the recent 9 month presentation shows how this looks on the map:

Similar to Romgaz, the IPO prospectus is a pretty interesting read, covering many aspects of the Romanian electricity market. Those were the major points that I extracted from reading the prospectus:

+ IPO proceeds went 100% to the company to fund future growth

+ significant potential for additional guaranteed investments

+ conservative balance sheet

+ efficiency gains possible (10% grid loss)

+ underlying growth potential

+ valuation ex cash VERY cheap for a grid company

+ potential M&A opportunities (ENEL assets)

+ EBRD as shareholder actively protecting minority rights

+ local regulation creates attractive “float”

– guaranteed return on regulated assets has been just lowered from 2014 peak (7,45% vs. 8,35% in 2014)

– business is partly electricity distribution, no pure “grid” play (no guarantees for distribution)

– limited experience with regulator (previous head of regulator convicted for bribery)

– some distressed subsidiaries (external grid maintenance)

– 22% minorities in all major subsidiaries

Electrical grid as a business

Building and maintaining an electrical grid is a very capital-intensive business. The electric grid is one of the most dominant monopolies available. There is competition on the generation and supply side, but there is always only one electric grid as this represents the archetypical network effect.

There is just no reason to build a second electrical grid and unlike as for instance telephone landlines, there is a pretty low risk that electricity could be distributed via an alternative way. This is one of the reasons that grids are almost always heavily regulated as the potential power to abuse this monopoly would be pretty high.

One additional features is the fact in many countries the grid was not designed to cope with locally generated renewable energy, so there is clearly a need for massive additional investments. Normally, a sector with large investment requirements is not that attractive, but if you combine this with stable yields and leverage potential, things can suddenly become very interesting in a low growth environment.

I had written 2 years ago that even Warren Buffett thinks utilities can be attractive, if the earnings are stable or even guaranteed, especially if you then can leverage up accordingly. Also the announced E.On spin-off ties to move grid and end-user supply into the good ship

Although there is always a risk that regulators run amok, at least for electrical grids the seem to be on the soft side as they know that a lot of capital is required to cope with the renewable energy revolution. As a consequence, the valuation of listed grid operators are the highest among the overall utility sector.

Let’s look at the valuations of 4 listed electric grid companies in Europe:

| Name | Mkt Cap (EUR) | BEst P/E:2FY | P/B | ROE | ROA | Debt/capital |

|---|---|---|---|---|---|---|

| REDES ENERGETICAS NACIONAIS | 1.352 | 12,2 | 1,2 | 11% | 2,4% | 70% |

| RED ELECTRICA CORPORACION SA | 9.922 | 16,5 | 4,2 | 24% | 5,8% | 60% |

| TERNA SPA | 7.811 | 14,6 | 2,5 | 17% | 3,7% | 71% |

| ELIA SYSTEM OPERATOR SA/NV | 2.442 | 16,1 | 1,1 | 9% | 3,3% | 55% |

It is interesting to see that despite being located in the more critical countries of the Eurozone (Portugal, Spain, Italy and Belgium) those companies enjoy quite rich valuations. ROAs are low single digits but due to the monopoly character of the business, it can easily be leveraged up between 50-70% of the total capital (and several times equity).

Romanian electricity market

This is an interesting quote from the IPO prospectus:

The average electricity consumption per capita in Romania is still significantly lower than the average electricity consumption in the 28 EU member states. In 2012, Romanian electricity consumption per capita was 2.3 MWh, whilst the average electricity consumption per capita in all the EU countries was 6.0 MWh and in the selected Central and Eastern European countries (excluding Romania) in the table above it was 4.3 MWh.

<

So assuming that Romania will catch up to a certain extent with the Eurozone, underlying growth in the electricity market should be strong. Romania has separated grid and power generation, however, at least in the case of Electrica, supply to end users is still part of the package.

The power market for end users is still highly regulated to a large degree but will be liberalized going forward. For Electrica’s grid business, this is irrelevant, but the supply business could be affected.

Electrica has a 25 year concession to operate the grid with an option to extend another 25 year. They can charge a fee to customers which guarantees them a certain pretax rate of return on assets if the meet minimum requirements set by the regulator. The base rate which they can charge is currently 7,45% for the next 4 years, higher rates seem to apply for “smart grid” investments.

One interesting specialty of the Romanian market is the existence of the “connection fee”. This is what they say in the IPO prospectus:

According to the law, the value of new connections to the electricity network is charged to the final users as a connection fee. The new connections to the electricity network are the property of the Group. The Group recognises the connection fee received as deferred revenue in the consolidated statement of financial position and subsequently records it as revenues on a systematic basis over the useful life of the asset.

The total amount they show as deferred revenue is 1,4 bn RON which is quite significant. For them, this is a very attractive “float” as it doesn’t carry interest and no covenants are attached. I assume that this also explains why they don’t use external debt as the investments are basically financed by the clients.

Valuation – simple version

Electrica has a market cap of 4 bn RON. Including IPO proceeds, the sit on 2,8 bn liquid assets, so the core business is valued at 1,2bn RON. With a run rate of 250 mn Earnings, this equals P/E of 4,8 ex cash. Assuming that a unlevered grid company in Romania could be worth 10 times earnings (still cheap compared to a highly levered Portuguese grid company at 11x earnings), the upside for the stock would be at least 30% based on current earnings.

Valuation including growth

Now comes the interesting part. Normally as a value investor I would assume zero growth. But in Electra’s case I would make a difference. Why ? Well, because:

1. They can invest (“compound”) at a guaranteed rate

2. The have already raised the money

3. The guaranteed rate can be charged irrespective of power prices or volume

4. There is no competition

The “only” risk that remains is the regulator. In order to model the profit growth, I have built a very simple model for the next 5 years using the information form the IPO prospectus:

I made the following (conservative) assumptions:

– supply business remains more or less constant despite significant growth yoy 2014

– I assume the losses from the “distressed” service subs will be phased out over 3 years

– they will distribute 85% of earnings as dividends

– they will invest according to plan at a blended guaranteed rate of 7,7%

Based on those assumptions, the profit after tax and minorities should double within 5 years. Assuming 8%% dividend payout (all of which can be funded by existing cash on operating cashflow), one can expect a return of 17-21% p.a. assuming an exit P/E multiple of 11-15.

Assuming exit multiples is of course already quite aggressive, on the other hand, if the price wouldn’t move, the assumed dividend yield of Electrica would be more than 10% in 2019. So some multiple expansion would not be unrealistic.

Addtitional (significant) upside could come via profit increases in the supply sector or opportunistic M&A as the ENEL grid seems to be for sale. My required rate for such an investment would be 10-15%, so at the current price Electrica looks attractive.

Other considerations

Stock price: In local currency, the stock price is only slightly above the IPO price of 11 RON:

Analysts: According to Bloomberg, a surprising number (8!) of analysts cover the stock. Their price target on average is around 14,6 RON, a potential upside of 30%.

Shareholders: During the IPO, the EBRD (European Developement Bank) acquired 8,6% of the shares. According to this article they are actively working to protect/ensure minority shareholder rights:

“Our participation demonstrates the EBRD’s commitment to supporting the government’s plans for increased privatisation of the energy sector,” Nandita Parshad, Power and Energy Director at the EBRD, said in a statement.

Parshad said the EBRD will work with Electrica to align its corporate governance with international standards: “This will provide additional comfort and confidence to potential future investors.”

The Romanian government still owns 49%.

Management: There is unfortunately not a lot of information on management. The CEO is an “Old timer”, joining the company in 1991. there seems to be some variable component in their companesation package but it is not clear how this looks like.

“Frontier” market: Despite being an EU member, Romanian stocks including Electra are considered “Frontier” stocks by MSCI, not even “Emerging”. That might make it more difficult for “established” funds to invest.

Summary:

As I have written in the Romgaz post, I find Romania fan interesting market in general especially with the lection of the new President. Electra is similar to Romgaz a privatization story. What I like about Electra is the fact that there is good visibility on growth.

The major risks are from the regulatory side, although I am quite optimistic that with the new president there will be even more of a “pro business” and “pro growth agenda”. Plus, the risks in this case in my opinion are relatively uncorrelated to other issues within my portfolio, so I think this could be a good diversifier.

With relative conservative assumptions and the guaranteed part of Electrica alone, one should expect between 17-21% return per annum over 5 years. If the non-guaranteed supply business improves or they are able to get other parts of the Romanian grid then the upside could be even higher.

I am pretty sure that not many investors will be interested in the stock as it seems to be both, too exotic and a strange mixture between “deep value” and growth, but for me it is the perfect stock as I don’t have to track any indices.

For the portfolio, I will buy a 2,5% position at current prices. This increases my “Romania bet” to 5% and total EM exposure to 13%. Time horizon is 5 years.

A few days ago, I sold 1/4 of my Electrica SA position at ~9,90 RON/Share.

Energetica fired the CFO during the board meeting on Friday: http://www.stockmarketwire.com/article/5785191/Electrica-appoints-CFO.html.

Interestingly, the news is not yet on the company’s homepage.

Hey Falko,

Although Electrica has the potential to be a great company, the current administration in Romania is nothing short of a mess. The decisions taken are erratic and this reflects upon companies the State has a significant stake in. Even worse, you can be sure the people they name on the company boards and management are mostly incompetent :).

As a Romanian, this hurts to see, but it’s something people need to know about.

Now, the stock is probably still attractive (as it’s extremely cheap), but it’s hard to gauge the effect an extremely incompetent manager can have on the company’s profitability. Given that this is a utilities company, I’d say it should be limited, but visible.

This does nota happen only in Romania, but in nieghbouring countries and Turkey (including the iberian part of Turkey).

Very Good news from Electrica: Minorities from Fondul seem to have been purchased at a very attractive price.

Click to access ELSA_EN_CurrentReport_FP_MoU_14Jul2017.pdf

Based on 2016 eanrings, the purchase price is around 7x net eanrings which is VERY cheap and should improve Electrica’s 2017 results significantly.

I increased my Electrica position from 3,6% of the Portfolio to 5,4%.

Der Grieche (Public Power) hat jetzt sein Stromnetz (IPTO) auch per SpinOff an die Börse gebracht. Das ist Teil der Forderungen der EU aus 2015 gewesen. Wenn ich es richtig verstehe, dann hatte Terna zumindest für einen Teil geboten.

Könnte man mal anschauen. PP + IPTO sind inzwischen schon +20% mehr wert als die alte PP.

http://www.admie.gr/nc/en/home/ (leider mit sehr spärlichen Infos zu den Geschäftsberichten)

Hi mmi

Electrica reported ist preliminary (consolidated) results two weeks ago.

Net Profit was RON 401m (vs. your 324m estimate) and after minorities it looks to be RON 288m (72% of pre-minorities net profit vs. your 78% share assumption). 85% paid as dividends to shareholders equals RON 245m or 0.7217 RON/share, a dividend yield of 5.9% at current prices.

Using the current market cap RON 4170m, the TTM P/E is 14.5x and 6.9x excluding the net cash position of RON 2188m reported in Q3 2014.

Do you have a view on this set of preliminaries or do you wait for the annual report to be published on the 28th of April?

hi,

thanks for the update. Yes, I want to wait for the annual report for further analysis.

mmi

Hi mmi,

You may have seen this already but the 2014 financial statements and board of directors report for Electrica have been published under the materials for the shareholder meeting here:

http://www.electrica.ro/en/general-meeting-of-shareholders-as-of-april-27nd-2015/

You have to scroll down past the EGMS agenda to the OGMS agenda to get find the consolidated statements. Also posted on the site is the company’s forecast for 2015 capex as well as for profit and loss. The respective documents are here:

Click to access ELSA_RO_EN_AGEA_EGMS_item_01.pdf

Click to access ELSA_EN_AGOA_OGMS_item_05_1.pdf

Electrica is forecasting net profit of RON 461mm in 2015 on revenue of RON 5,398mm. Capex is expected to be RON 672mm in 2015.

Thanks !!! the 2015 plan is far above my estimate…..

Sounds really interesting. At 4-traders they show the average estimate of analysts. The averaged estimate for 2015 is 348 Mio RON. If electria should really outperform that estimation by more than 30% – wow!

As far as I understand, outperformance of expected estimates is one of the best receipt to get rising stock prises.

Hi MMI

The annual report & investor presentation is out as are the results of the AGM. A few things really struck me and I would be great to get your opinion on them:

Non-controlling interests

Net profit for the year was RON 401m of which RON 287.8m is allocated to the parent and RON 113.5m to non-controlling interests (annual report p. 79). The split therefore is 72%/28%. At the same time Electrica holds 78% in each of its subsidiaries.

On page 124 the details of the NCIs are shown. The RON 113.5m is actually calculated as 22% of the comprehensive income of the subsidiaries which was an aggregate RON 516m in 2014.

My question here is: Why is there such a large difference between the RON 516m comprehensive income of the subsidiaries and the RON 401m profit of the Group.

Budget 2015

Electrica plans to increase net profit from RON 401m to RON 461m, a 15% increase (presentation page 10).

If one looks at the budgets for the distribution segment and the supply segment, the numbers look as follows: Distribution net profit to increase from RON 306m in 2014 to RON 352m in 2015 (presentation page 15). For the supply segment the net profit is expected to drop from RON 180m in 2014 to RON 86m in 2015 (page 26). Even though the 2014 net profit numbers of the subsidiaries don’t add up to the 401m group net profit, one can see that the expected decline in the supply business is bigger than the growth in the distribution business (-94m vs. +46m). So how do they arrive at the overall planned increase in profits for 2015?

AGM 2015 (http://www.electrica.ro/wp-content/uploads/2015/04/ELSA_RO_EN_AGOA_27Apr2015.pdf )

Approved resolutions:

– annual report for 2014

– 2014 dividend

– income and expense budget for 2015

Rejected resolutions:

– investment (capex) plan for 2014

– framework management agreement

– remuneration of the board

– remuneration of the management

I’m not sure how to interpret the rejection of several AGM resolutions by the government of Romania, but I feel rather uncomfortable with the controlling shareholder voting/working “against” the management.

The capex plan for 2015 was RON 671m vs. 1.4bn stated in the IPO prospectus. It looks like the state wants Electrica to invest substantially more than management has planned. Even more surprising is the rejection of the framework management agreement which was apparently drafted with the help of reputable consultants and inputs from the EBRD.

What will happen now? Will there be an EGM to approve a new capex budget and management framework or will they just do what the state wants them to do?

http://www.romania-insider.com/state-asks-romanian-electricity-distributor-to-revise-investment-plan/147757/

It would be great to get your (and any other readers) view on these different items/ developments and if these somehow change your view on the investment case.

Cheers

maybe one quick comment to the 22% non-controlling interest and the Group result: Electrica has some 100% subsidiaries (service companies) which made a loss in 2014. So therfore the group net income is lower overall than if you just add 78% of the profiatble subsidiaries.

mmi

Interesting! How much of the profit is made from the distribution business, and how much comes from the grid itself?

What I dont understand is how they will grow. Since the grid in other regions is operated by other companies, and the distribution business isn’t self-generated, the only sources of growth that I can see is higher electricity usage by existing customers, expanded capacity within the region (if there’s demand for this?) or aquisitions.

With so much cash on hand it seems shareholders are very depending on the capital-allocation skills of the managers. If they make a pricey acquisition it might hurt the return, no?

Thank you for an interesting analysis.

thanks for the comment. If you have ever been in Romania, you will know that the grid is not the most recent one, in fact it is very old. So there is a lot of investment need for modernization. With some caveats,any modernization increases the regulatory asset base and therefore growth is guaranteed within the current area at least for the next 5.10 years.

Clearly capital allocation is key, on the other hand they have committed to a fixed investment plan so i think growth is quite predictable.

Re split. You might want to read the reports, they are actually quite good 😉

Volume is very low at the moment compared to their free float market cap.

Thanks for picking up my encouragement to look at Electrica.

In my view, the article makes sense including your thoughts on valuation.

Main downside risks I see are:

– regulatory risk, i.e. the regulatory body starting to deviate from the framework they promised. I agree that this looks unlikely for now and even less likely with Iohannis in charge.

– Increased competition in the supply business. For now, the large chunk of the supply business is regulated, i.e. Electrica is the only service supplier. This will change and may result in price pressure (but also in market opportunities.

On the upside, they may surpass your assumptions by:

– making better better efficiency gains than projected

– making smart acquisitions (both Enel and E.On are still active in Romania but may reduce their involvement)

I agree that Electrica is an attractive investment and have also picked up some shares.

hi Lathinker,

thank you for the comment and thank you for the idea which came from you and from a Romanian investor independently. I forgot to mention this on the post, but will correct it.

mmi

Hey Lathinker,

Electrica is only one of the electricity distribution companies in Romania. At the moment we have several regions, each with one distribution company serving it – Electrica is the supplier for a few of these regions, Enel for others and, finally, eOn for the rest.

There will be no competition between these 3 any time soon (as far as I know), so it’s safe to assume that the only way Electrica will lose its dominating position will be by selling the business in one of the regions to a rival.

The regulatory risk is indeed a major risk for Electrica. Not only that the regulatory body can choose to cap the selling price and cause margins to decrease, but the Government can also create additional taxes, which might suck profit from the company straight to the State Budget (this is what happenned in 2014).

Having said that, Electrica is currently a pretty decent investment compared to other companies in the region and, probably, a significantly better investment compared to other utility companies in Western Europe (even after adjusting for risk).

Thanks for the post. In the prospectus, does the company mention that it will pay a dividend in the future and what the implied dividend yield is? Thanks.

#Imran,

I would not recommend to invest without reading the prospectus. So yes, I could answer you, but in your own interest I will not 😉

mmi

I was thinking of doing research on it if it was paying out something

I was only teasing you. This is what they said during the IPO:

Management’s intention is to distribute dividends, based on a guidance of approximately 85% of consolidated profit attributable to shareholders of Electrica SA.

http://www.londonstockexchange.com/exchange/news/market-news/market-news-detail/11969259.html

If you look at my model, you will see I assumed a 85% payout.

Tut mir leid dass ich nochmals nachfragen muss, scheinbar bin ich zu blöd zum Ordern. Ich wollte jetzt gerade über comdirect eine kleinere Order von Romgaz kaufen (150 Stck.). Über die Börsen Berlin oder Frankfurt ist der Spread bei fast 10 %. Tagesvolumen 0, Über Stuttgart sinds 7500 Tagesvolumen über London Stockexchange 543000 d.h. ich wollte ne Auslandsorder abgeben. Wenn ich bei Comdirect den Kurs über LondonStockexchange anzeigen lasse und auf Kaufen klicke kommt nur Inlandsorder und die 3 deutschen Plätze. Wenn ich auf Auslandsorder klicke und die WKN A1W7WE eingebe kommt diese Mitteilung:

Es konnte kein ausländischer Börsenplatz ermittelt werden. Bitte notieren Sie Ihre Order und rufen Sie bei unserer Kundenbetreuung unter 04106 – 708 25 00 an

Ich kapiers einfach nicht, bin ich zu blöde oder was mache ich falsch. Gibts für Ausland ne andere WKN? Liegts an der Uhrzeit/Zeitverschiebung (wollte um 17.20 Uhr ordern) .Klar ich könnte dort anrufen und telefonisch ordern aber ich denke ich möchte ja für die Zukunft lernen. Das muss doch auch Online gehen.

Ich danke euch schonmal für eure Hilfe

Viele Grüße

London geht bei denen nur telefonisch, ich empfehle aber mehr eigenes Research vor dem Kauf. Zumindest einen annual report lesen.

Hallo,

London dürfte m.E. teuer sein. Ich habe kein Comdirect Depot und kann Dir da nicht helfen. Wenn Du kaufen willst würde ich trotzdem Deutschland empfehlen. Der Brief Kurs ist eigentlich gar nicht so schlecht und der Geldkurs sollte Dir egal sein, da man das Ding mind. 3-5 Jahre halten solltest. Wenn Dich bei so einem Investment ein hoher Geld/Brief Spread stört, solltest Du m.E. eigentlich nicht investieren.

Glad to see you like Romanian stocks, Electrica is a fine choice :).

Please note that Electrica is not the equivalent of the Spanish Red Electrica – that would be Transelectrica, a different company (also listed under the ticker TEL).

Electrica just transforms high voltage electricity (received from the national grid, operated by Transelectrica) and then distributes it to end-consumers.

Of course, it does operate its own “local” grid (inside cities) and is in no danger of losing customers, but there is a higher risk with regards to Electrica than Transelectrica (as you already mentioned).

Congrats for another good analysis!

hi Lucian,,

yes, I am aware that the high voltage grid is run by Transelectrica, but I still think those are the better peers than the “integrated” utilities.

mmi

Agreed, it’s definitely closer than companies that also own electricity generation assets.

wie kauft ihr sowas? ich seh nen Spread von fast 10% bei comdirect über Frankfurter Börse, die Ölfirmen sehen zur Zeit ja auch wieder interessant aus muss ich sagen. Kaufen wenn die Kanonen donnern heisst es ja immer

der Briefkurs ist eigentlich ziemlich fair. in London kann man zu 1% Geld/brief handeln.