Short cuts: Installux, Kuka, Aixtron

Installux:

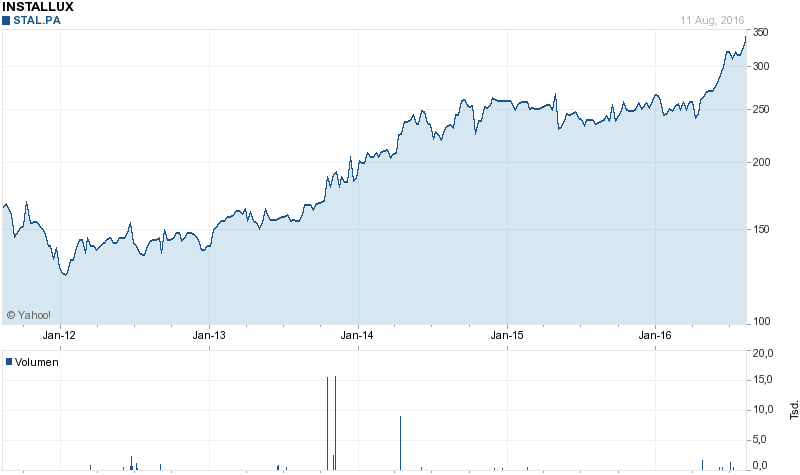

Installux is surprisingly one of my best performing stocks this year, including dividends the stock is more than 30% and is at an all time high.

I did not fully understand why until I read the 6 month report.

Sales are up ~7% yoy, 6M earnings per share are 17,16 EUR vs. 14,37 EUR, an increase of almost 20%. Profit improvements happened across most of their sectors, so it doesn’t look like single special effects or so. Despite the recent run-up, the stock remains exceptionally cheap.

Kuka & MDAX exit

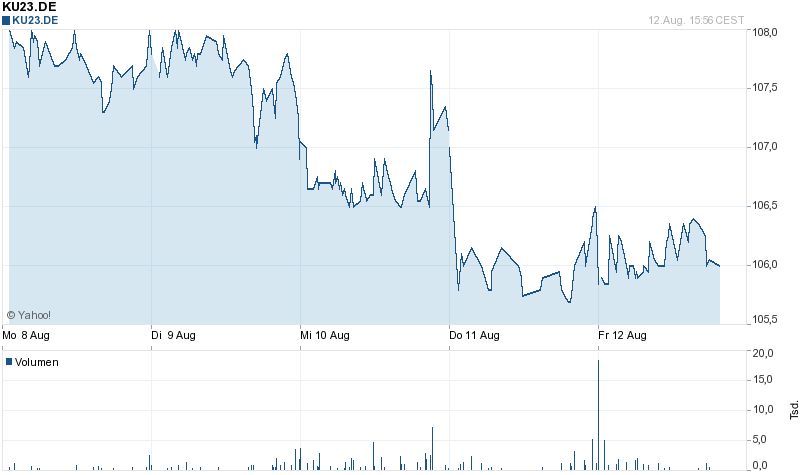

For those who did follow my comments on the original Kuka post, they might have noticed that I sold the stocks 2 days ago and bought them back yesterday slightly cheaper.

The reason was that in the meantime, the tendered shares were kicked out of the MDAX, the popular German MID Cap index.

As I was not sure how the shares would react I decided to manage the risk by staying out.

At the end of the day not much happened:

Nevertheless I was able to cheapen my purchase price from ~107,5 to 106 EUR. As the deal now is more attractive, I invested a total of 4% of the portfolio.

Aixtron – another special situation (with a Chinese buyer)

Aixtron, a former TECDAX star has fallen on hard times. However a few weeks ago, a Chinese buyer showed up and finally made an offer for the company at 6 EUR per share.

With a share price at currently 5,53 EUR, the discount is similar to Kuka at around 8,5%.

The situation differs slightly from Kuka:

- the buyer is a financial buyer, not a strategic one (more opportunistic ?)

- The purchase price is “optically” not as rich as the one for Kuka (below book)

- they require at least 60% acceptance as closing condition (vs. 30% for Kuka)

- within the offer they have a “put” if the index (DAX or TEcDax) goes down more than 30%

On the plus side, there is little risk that anyone complains about the deal as Aixtron was not doing well anyway and they are not deemed “strategically important”. The time horizon here should be shorter than for the Kuka deal.

The offer runs until October 7th. So far, the acceptance is low, as of today, only 1,64% of the shares have been tendered.

I think the risk is slightly higher than in the Kuka case as they might not reach their threshold, on the other hand there might be a chance for a better offer.

Although the situation is less clear for me as in the Kuka case, I start here with a 1% position at 5,53 EUR and will monitor it closely.

Re Installux: They are delisting from Euronext and transfer to Euronext Growth, which is a much less regulated trading venue. Any thoughts on this? Also on the general performance of Installux? I note that their net cash position is mostly gone so they do not appear as cheap anymore.

Nice Chritsmas present: Kuka Take over approved by US authoroties:

http://www.euronews.com/2016/12/30/chinas-midea-receives-green-light-from-us-authorities-to-buy-kuka

I reduced my Kuka position by 2/5. Reason: I found a much more attractive Special situation and ran out of cash….

Hi!

Could you please disclose this “much more attractive Special situation”?

BTW Kuka jumped 3% to 110Eur today…

Best regards and keep posting.. I very much appreciate your blog!

the timing of my reduction was not optimal ….and you need to wait until I have finalized my write up, sorry 😉

Slow investing is orthogonal with real time investing updates!!!

“CFIUS informed the Bidder and AIXTRON that, if the parties did not withdraw their

CFIUS notice (the “Notice”) and abandon the transaction, the matter would be referred to the

President of the United States, who has the power to prohibit the transaction.”

Happy days!

hmm, I think I was lucky to get out of this one relatively early……

The German Government seems to be in “full intervention” mode:

http://www.wiwo.de/politik/deutschland/chinesische-investoren-bundesregierung-interveniert-auch-bei-osram/14748686.html

Beim geplanten Kauf der Osram-Lampensparte Ledvance müssen die chinesischen Interessenten einen Rückschlag einstecken. Das Bundeswirtschaftsministerium hat den Antrag der Bieter auf eine Unbedenklichkeitsbescheinigung abgelehnt, wie die WirtschaftsWoche aus Finanzkreisen erfuhr.

Das Bundeswirtschaftsministerium äußerte sich auf Anfrage dazu nicht, unternehmensnahe Kreise bestätigen die Nachricht allerdings. Die Bundesregierung wird den Deal laut Kreisen nun einer vertieften Prüfung unterziehen. Das bedeutet, die potenziellen Käufer sowie das Unternehmen werden monatelang warten müssen, bis sie wissen, woran sie sind. Ursprünglich sollte die Transaktion im Geschäftsjahr 2017 abgeschlossen werden.

Der geplante Kauf der Lampensparte für 400 Millionen Euro wird nun wohl erst mal auf Eis gelegt, bis ein verlässliches Signal aus Berlin vorliegt. Das dürfte auch für den erst kürzlich bekannt gewordenen Plan der Chinesen gelten, nicht nur die Lampensparte zu kaufen, sondern Osram komplett zu übernehmen.

Am I right in understanding the the tendered Kuka shares (DE000A2BPXK1) will be re-admitted to the main listing if the takeover does not settle by the 31/03/17 ?

This should be the case unless the bidder extends the maturity of the offer.

Regarding Aixtron:

There should be a good chance now that the deal goes through with 65%+

Bundesanzeiger still shows a significant short interest in Aixtron shares of about 11,5%. If they are all going to compete for the remaining 35% of shares outstanding, don’t you think things could get interesting again?

Hmm, fundamentally 6 Euro is the max. What happens in between? Wo knows? This kind of speculation is not part of my circle of competence.

A bit puzzled that Aixtron’s yield is widening…any thoughts?

There was a negative report about the Buyer in a German Newspaper (strawman for Chinese Authorities)

Aren’t you concerned that only 16.5% of the shares were tendered as of yesterday?

I sold my position when I read this…

Sold my position today at 5,34 EUR, a loss of -4%. I do think the percentage might go up until Friday, but I do not have enough conviction to take the risk that the threshold is not reached.

The likelihood that the 60% is reached in 2 days is as much as finding a needle in a haystack…

Managed to sell at a slightly higher price than you and very happy that I am out.

he he he, again a lesson learned. Grand Chip extends the deadline and lower threshold to 50,1%. Stock at 5,75 EUR.

They are at 24,59% as of today. Still 35% to go in 2 days.

Hi,

I got an interest in special situations and your website is great. I am still learning and not acting so far, but just to understand more, would it be now to late to buy KUKA shares to partecipate to the offer?

Thanks

Technically, the ku23 shares participate automatically. However you might want to learn more about the mechanics if you don’t know This. Reading and understandig the offer documents is key.

Bei Aixtron sind übrigens noch mind. 6% leerverkauft.

https://www.bundesanzeiger.de/ebanzwww/wexsservlet

Der größte Aktionär mit 8% sieht die Sache kritisch:

“Barry Norris, Chief Investment Officer of Argonaut Capital has questioned whether the buyout price was actually worth the value for shareholders, since Aixtron had injected about EUR 300 million in R&D over a span of five years.”

Das ist die Sache, die ich bspw. auch an einer Kontron interessant finde. Was ist das im. Vermögen wert, wenn man jahrelang geforscht hat? Da hat keiner einen wirklichen Einblick. Kontron will ja auch in die Ecke Industrie 4,0 & Internet der Dinge. Und hat jetzt erstmal 2/3 des Goodwill abgeschrieben. Da würde mich eine Übernahme oder eine Verkauf des operativen Geschäftes auch nicht wundern.

Ich denke, dass sie die 60% noch lange nicht zusammen haben Bei Kuka brauchten die Chinesen ja netto nur 20%, da Midea schon 10% hatte,

This is an ignorant question but is it common for German stocks to split their trading between shares that have accepted the tender offer and shares that have not (I think this is the difference between KU2 and KU23 but could be wrong)? Is this done at the direction of the exchange or the company? Is there a release from the company that describes the difference in rights between the two share classes? I don’t see anything on their site but could be missing it.

yes, this is common to split the shares and to my knowledge done by the exchange.

Das mit Aixtron ist nicht ganz korrekt. Die erste Annahmefrist ist der 7. Oktober. Sollte es klappen, dann beginnt die zweiwöchige Nachfrist. Und dann kann erst übernommen werden. Sie nennen ja auch März 2017.

Bei Aixtron gibt es 2-3 Bonuszertifikate, die werfen 3,x % bis 5.10. ab. Also vor der ersten Frist und haben Sicherheitslevel von 4,40 Euro. Ich bin am Überlegen, falls es noch ein bißchen günstiger wird (als >4%) mir sowas zu kaufen und dann entweder in den 2 Tagen bis zum Angebot oder in der Nachfrist Aixtron-Aktien. Auch dann sollte noch ein Abschlag da sein. Dazu würde Aixtron wahrscheinlich aus dem TecDax fliegen, wie Kuka aus dem MDAX.

Das Risiko ist m.E., dass irgendjemand auf “mehr” zockt und dann geht es wie bei K+S aus. Daher hätte ich vor einem Einstieg gerne Gewissheit.

Hi,

I have been notified that the Chinese buyer has extended the period to accept the offer of 6 Eur per share for Aixtron until 28.10.2016. Would you advice to accept this offer?

Best regards

No hurry, I will wait….

I love how Installux’ managers are careful with capital investments. Check this sentence taken out of their financial newsletter:

: “Souhaitant cependant de rester prudents, nous avons décidé de décaler le

programme d’investissements dans une nouvelle presse chez IES, mais nous poursuivons le montage technique et financier afin d’être réactifs si la reprise économique se confirme.”

Thats one advantage of haveing an “owner-operator”.