All Belgian Shares part 8 – Nr. 141-160

After a short vacatation break, I am back with the next “All Belgian shares” post. Besides the usual Real Estate and non-traded Expert market stuff, this time three stocks made it onto the watch list. For one of them I even started a 1% position in order to motivate myself for a deep dive rather sooner than later. Enjoy !!

141. EVS Broadcast Equipment SA

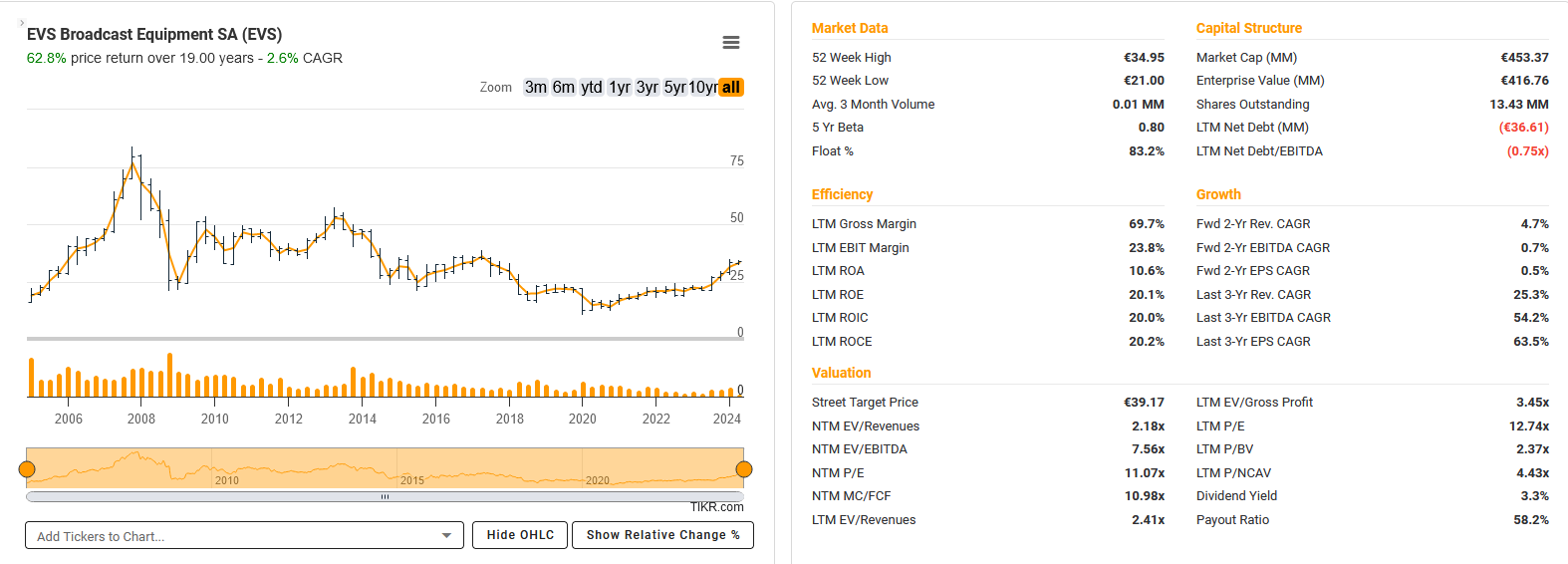

EVS is a 411 mn EUR market cap stock that I analyzed almost 10 years ago as a potential “high quality compounder”. This was my summary back then:

Looking at the chart, this is also one of the stocks where the “shiny new HQ curse” fully hit:

The stock lost more than -50% at its low but recovered in the past months somewhat.

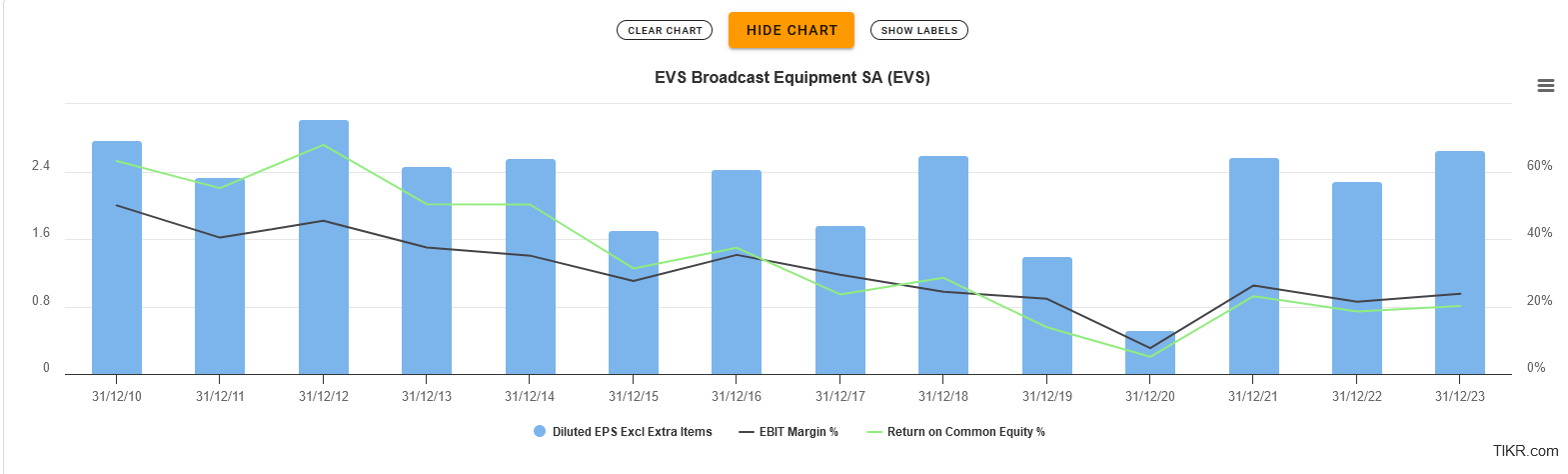

Interestingly, EPS per share recovered almost to the old levels:

OE and EBIT margin stabilized at a level of around 20%.Sales rebounded nicely after Covid. Ennismore owns EVS since a couple of years, it has become one of their largest position.

Overall, at the current moderate valuation, EVS is clearly a stock to look at. In order to increase the motivation for a deep dive, I bought a 1% position at current price. “Watch”.

142. Weyveld Nossegem (Expert Market)

This is another Real Estate certificate from a company called Immolease Trust. It traded last in December 2022. “Pass”.

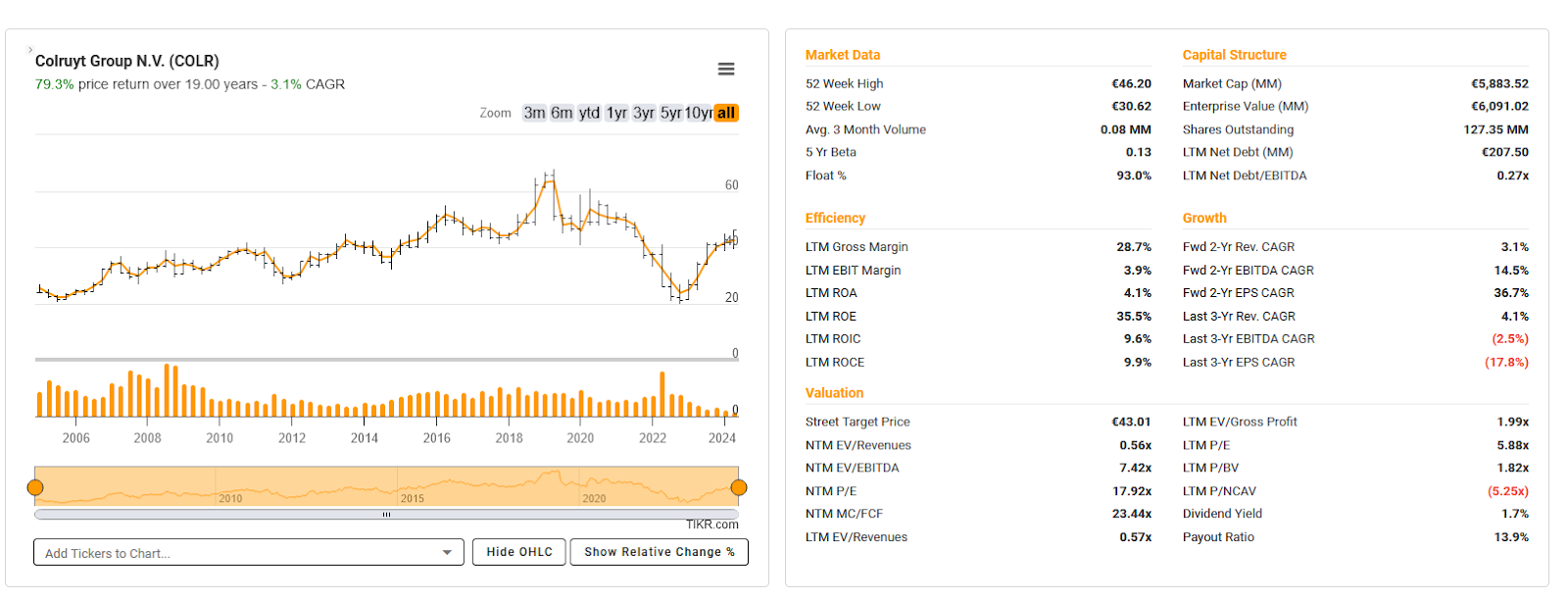

143. Colruyt

Colruyt, a 5,9 bn EUR market cap company is clearly one of the better known Belgian companies. According to TIKR it “engages in the retail, wholesale, food service, and other activities in Belgium, France, Luxembourg, and internationally. It operates through three segments: Retail, Wholesale and Foodservice, and Other Activities.”

Long term value creation is rather mediocre and the stock is not cheap:

The company has been struggling especially in 2023, however the bought back shares for many years. 2024 looks better, they also seem to have excited some non-core participations.

The Colruyt family owns around 70% of the share. In Belgium they seem to have 33% market share in food retail. Overall, nothing that jumpers at me. “Pass”.

144. Biotalys

Biotalys is a 2021 IPO with a market cap of 95 mn that “discovers and develops novel biological products for the protection of food and crops. It primarily develops biofungicides, bioinsecticides, and biobactericides”.

So far, that has not been too successful, as the stock lost more than -50% since IPO. “Pass”.

145. Crescent

Crescent is a 27 mn EUR market cap penny stock doing some kind of technology. “Pass”.

146. Schreder Group (Expert Market)

Schreder is an Expert Market stock that traded last in September 2022 and at least, with a price of more than 5000 EUR per share, it’s not a penny stock. According to TIKR it “designs and manufactures outdoor luminaires for urban or rural communities. It provides outdoor lighting products for roadway, urban, flood, industrial, tunnel lighting, and special applications worldwide”.

However, I did not find any financial information on their website, so it’s a “pass”.

147. Charbonnages de Gosson Kessales (Expert Market)

From the name, this sounds like another former coal mine. There is a detailed Wikipedia page about it. The stock was traded last in 2015. “Pass”.

148. Generale Belge Argentine (Expert Market)

This one traded last in 2018. It sounds like a Belgian Bank active in Argentina, but it’s a “pass”.

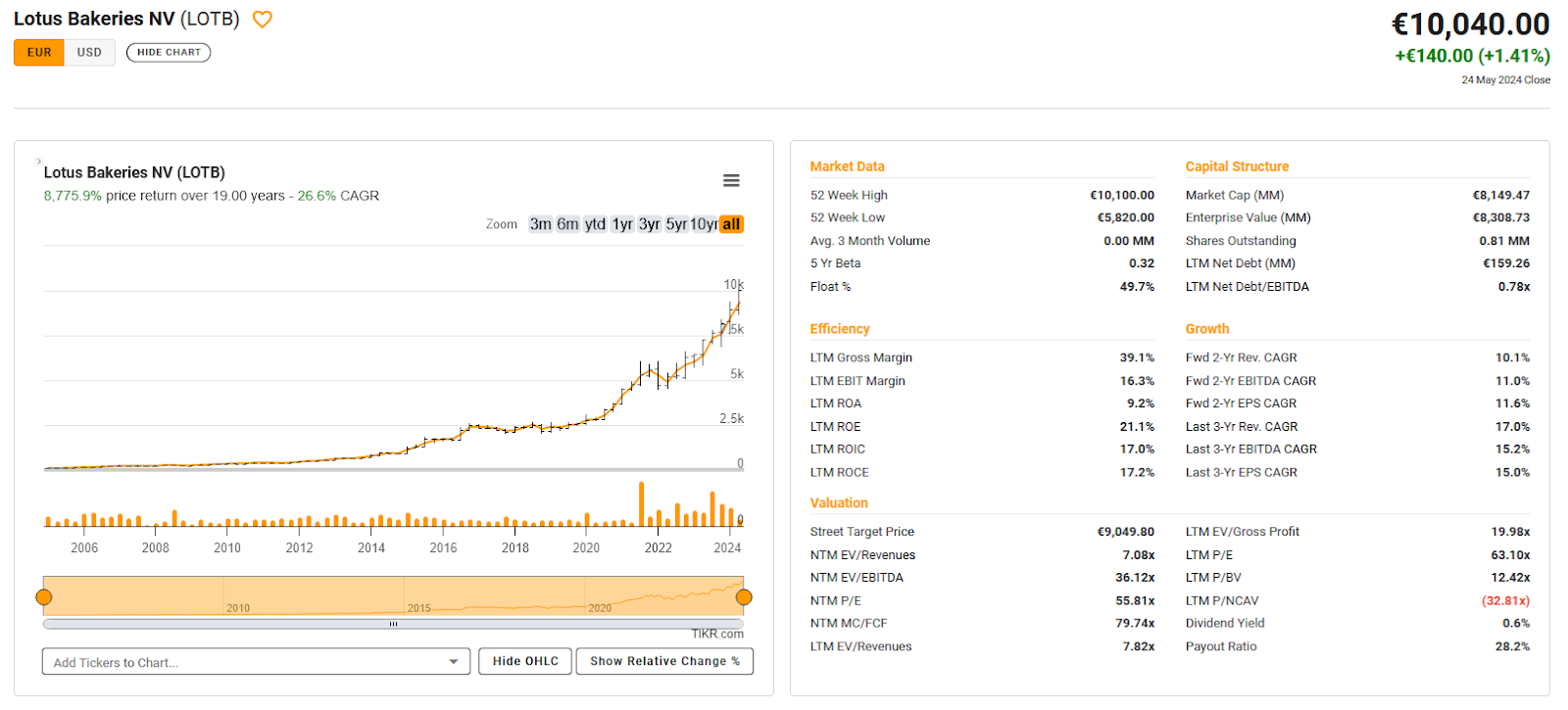

149. Lotus Bakeries

Lotus Bakeries, an 8,1 bn EUR market cap cookie and biscuit producer is clearly one of the biggest investment mistakes I made in my carrier. Why ? Because I researched it more than 10 years ago and passed because I thought it was a good company but too expensive at 20x P/E.

10 years later, this would have been a 10 bagger and nothings seems to be able to stop them:

In the last 10 years, earnings quadruplet, but also the P/E increased from 20x to 55x which is “rich”:

Although they are not crazy profitable, the manage to grow at high rates. Eben in 2020, they grew by 6%:

There most famous product is the “Biscoff”, the single packaged cookie one often gets with an Espresso.But they have a large line-up of very tasty other biscuits.

They have a very nice annual report which for some reason cannot be downloaded. 50% of the shares are family owned.

A P/E of 55 is unfortunately far north of my pain level, so I guess I will watch another 10 years and see the stock go to 100000 EUR per share. Nevertheless I will “watch” this company which is clearly one of the best Midcaps in Europe..

150. Candela Invest

This 3 mn EUR market cap company doesn’t seem to have a real business. “Pass”.

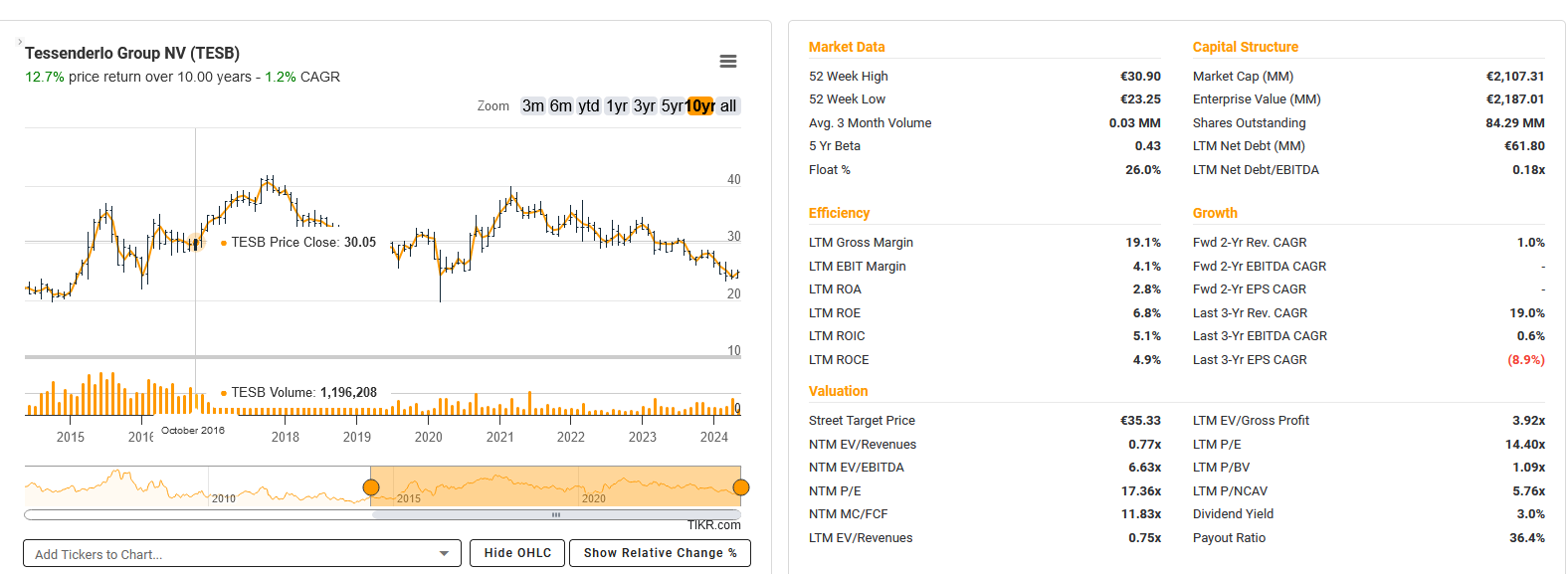

151. Tessenderlo Group NV

Tessenderlo, a 2,1 bn EUR market cap company is one of the most interesting Belgian companies. I actually started to write-up the company some time ago but didn’t continue. The company is majority owned and run by Luc Tack, a Belgian businessman who combined a quite strange collection of chemical companies, fertilizers, textile machines and Gas fired powerplants under one roof.

Initially he ran two companies, the other being Picanol, but he merged Picanol into Tessenderlo in 2023. After a record 2022, 2023 was quite bad across the company which had depressed the share price:

Tessenderlo’s accounts were always hard to read and they don’t smooth anything, rather the opposite.

One very unique feature is that Tessenderlo owns via the merged/Acquired Picanol around ¼ of its won shares which for some reasons are not “officially” counted as own shares.

Another interesting aspect is that they actually started to pay a dividend and that a new CTO and COO have been announced, as Luc Tack’s long term partner seems to have retired.

The Group has no debt and are continuously buying back shares. They also manage to pay very low taxes. The big risk here is that Luc Tack will take them private at some point with little or no premium.

Overall however clearly a stock to “watch”.

152. Compagnie Financière de Neufcour S.A

Another, 4 mn EUR Nano Cap that doesn’t seem to have a real business. “Pass”.

153. Mechelen (Expert Market)

Mechelen is another Real estate certificate, last traded in 2022. “Pass”.

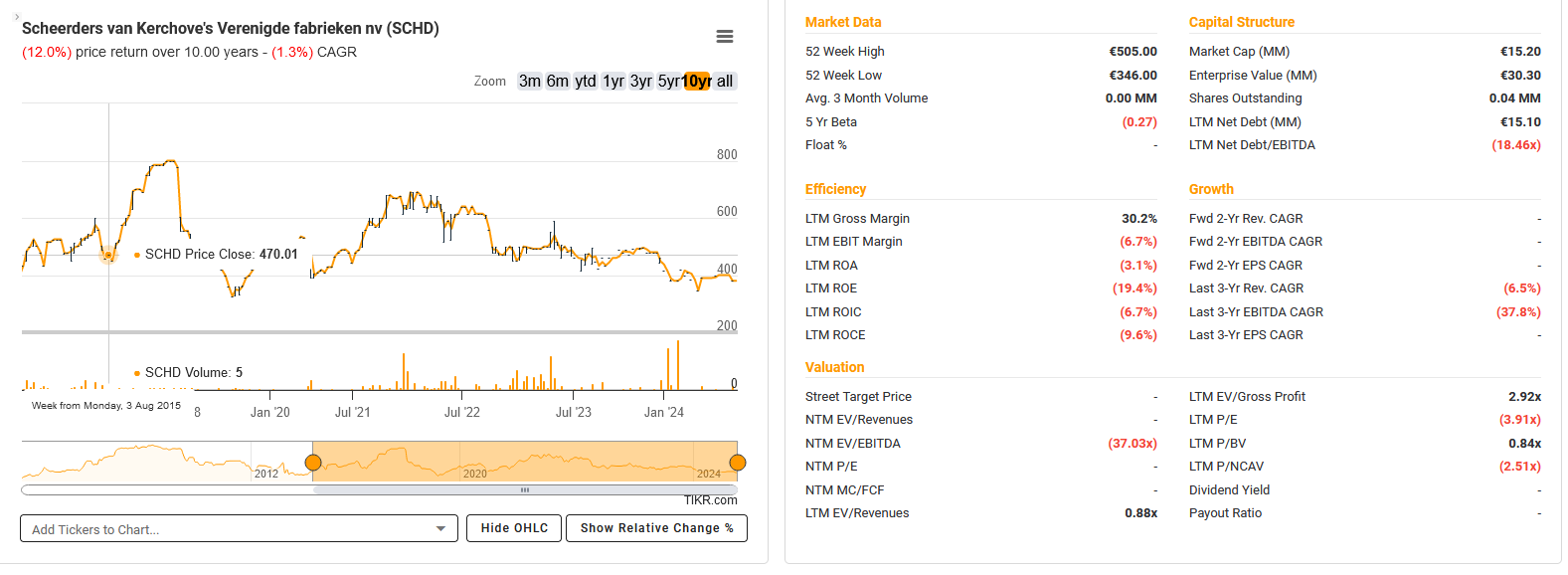

154. Scheerders van Kerchove’s Verenigde fabrieken nv

According to TIKR, this 15 mn EUR market cap company “manufactures and distributes building materials. It offers façade panels, slates, facing bricks, and corrugated sheets. “

The company is currently loss making and has seen better days:

Out of the last 8 years, 4 years were loss making, the company is also indebted. “Pass”.

155. Entreprises et Chemins de Fer en Chine S.A. (ECFC) – Expert MArket

ECFC is actually the main owner of Cie Bois Suavage and owns 50,1%. The stock traded last in 2020. “Pass”.

156. Euronav

Euronav is a 3 bn EUR market cap Crude Oil tanker company that is majority owned by the Savery’s family which also controls Exmar.

It became somehow famous because the Saverys family and Tanker Tycoon John Fredrikson fought for the control of Euronav for 2 years before Fredrikson gave up and they settled for a deal.

As Oil tankers and shipping in general are very difficult businesses, I’ll “pass”.

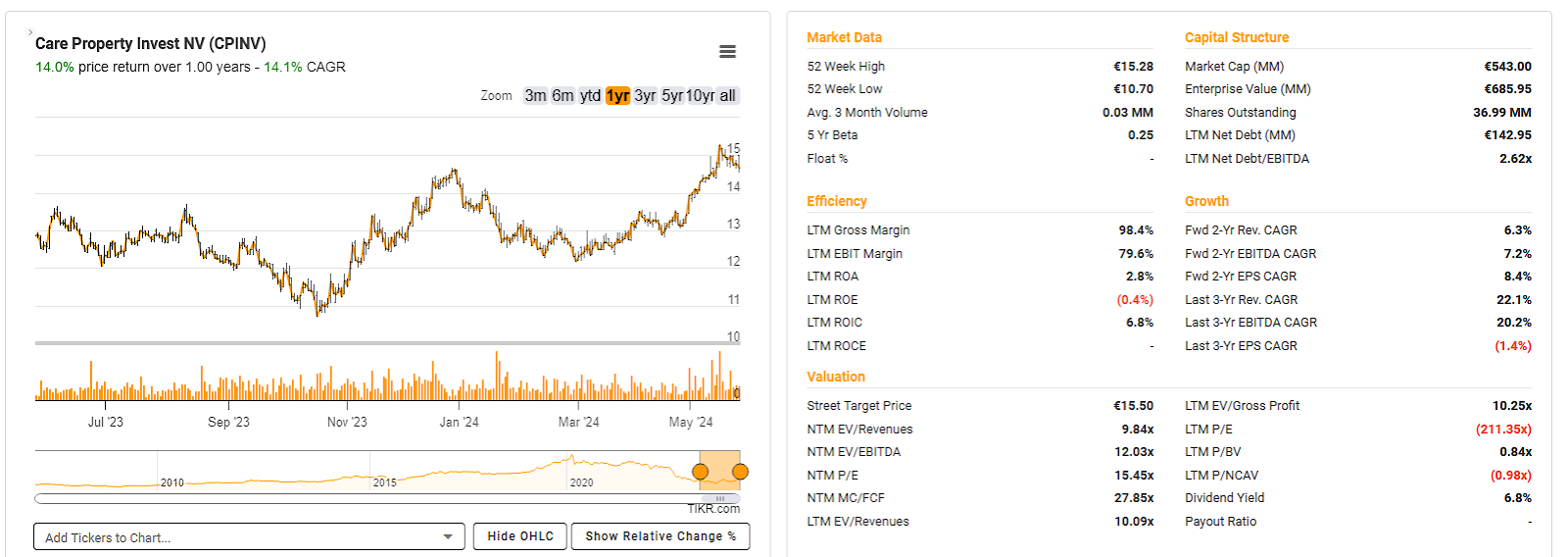

157. Care Property Invest

This 540 mn EUR market cap property Group “purchases, builds and renovates high-quality healthcare real estate (residential care centres, groups of assisted living apartments, residential complexes for people with a disability, etc.), fully tailored to the needs of the end user and then makes it available to solid healthcare operators on the basis of a long-term contract.”

Among the Belgian Real Estate stocks, this one stands out with having pretty decent stock performance:

Nevertheless, I’ll “pass”.

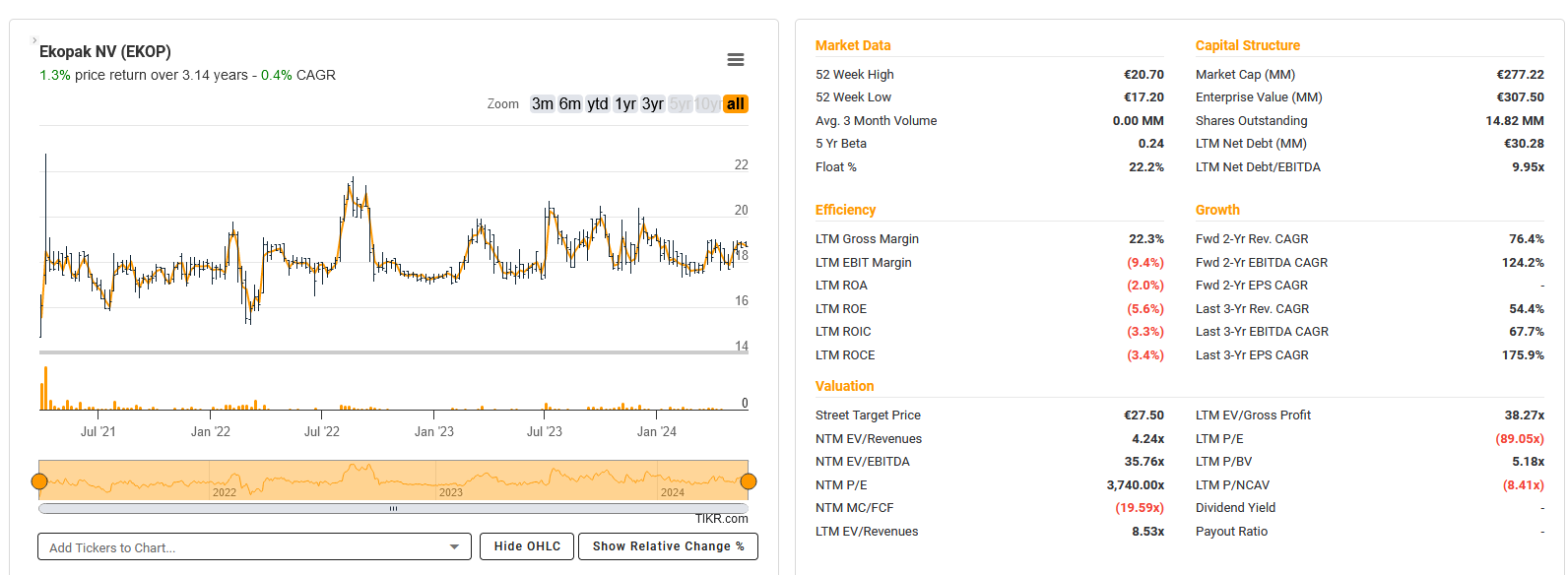

158. Ekopak

Ekopak is a 277 mn EUR market cap company that “designs, builds, finances, and operates industrial water processing solutions in Belgium, France, and internationally. It operates in two segments, Water-as-a-Service (WaaS) and Non-WaaS.”

As a 2021 IPO, the stock has run sideways since then:

The company is loss making. It is growing quite fast bt still needs to grow into the current valuation. Gross margins are low with ~20%. “Pass”.

159. IMBAKIN Holding (Expert MArket)

IMBAKIN Holding has actually traded in 2024, but as a Penny stock, my interest is very limited. “Pass”.

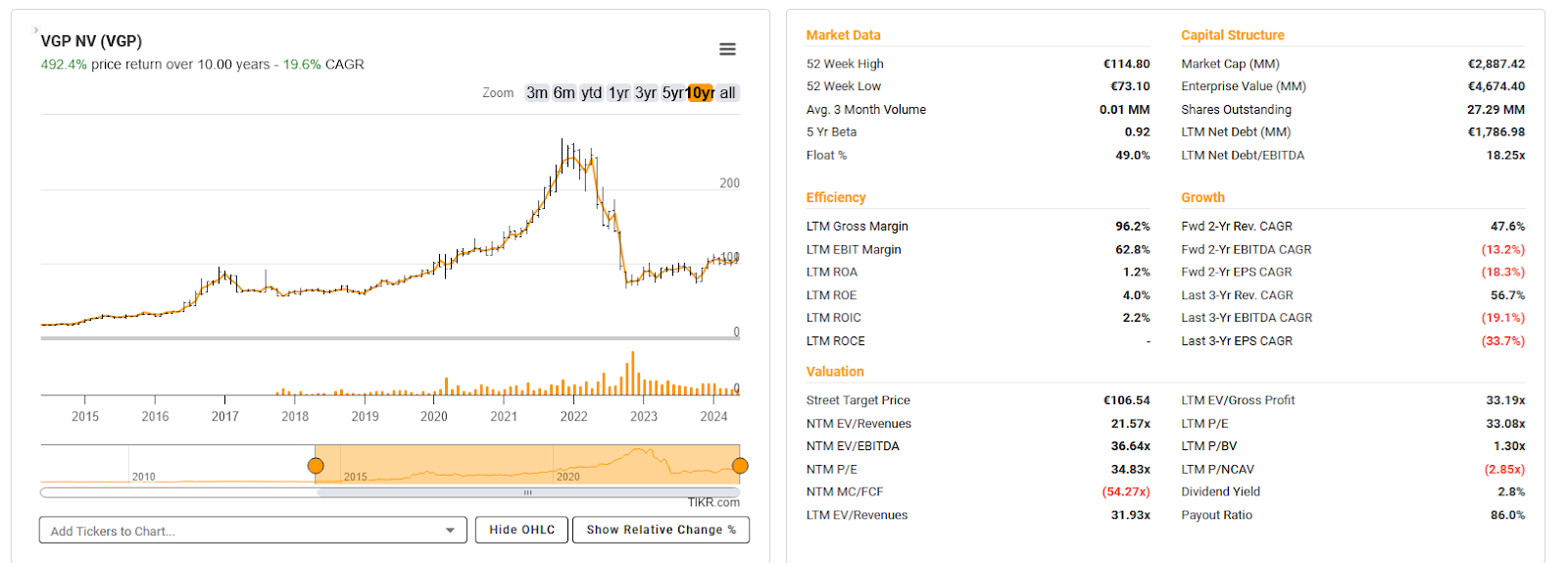

160. VGP

VGP is a 2,9 bn real estate company that “develops, owns, and manages logistics and semi-industrial real estate, and ancillary offices. “

The stock has seen better days, but long term the value creation is still quite good:

Nevertheless, as all real estate stocks, a “pass”

Imbakin is actually a pretty interesting penny stock. In the past it was split off from Texaf and its sole asset is a claim on the Congolese government of roughly 51 MEUR. Per share that’s about 16 EUR, compared to the current price of 0,17 EUR one could make an argument for an asymmetrical trade. A negligible amount of a portfolio could be invested in exchange for an educated bet with a very large upside. But that’s just how I’m thinking about it.

Imbakin is actually a pretty interesting penny stock. It is a small piece of Texaf which was carved out and it’s sole asset is a claim on the Congolese government for an amount of c. 63 MEUR (of which 12 MEUR is owned by a third party so say 51 MEUR). The IMF has already put the claim on a transactions list and if a payment scheme would be established that would mean that Imbakin’s stock is worth roughly 16 EUR/Share. Compared to a current share price of 0,17 EUR/Share it seems like an asymmetrical bet is worth it (a very negligible part of the portfolio can be invested for a potential 100x). The market (for about as far as we can call the expert market an actual ‘market’) currently prices the probability of the claim being paid out at 1% so it’s very cheap to make a bet on it.

Thanks a lot for that information. Fo you have any source / link for this ?

http://imbakin.com/investisseurs.php

On their website they published all the information I know of (the latest ‘annual report’ states the part of IMF). All of their information is in French. I also noticed that another comment of mine went through (Queenie), for some reason I thought I deleted that one and posted only the more elaborated one (apologies). The probability of the claim being paid is just a ‘dirty’ calculation based on the risk arbitrage notion ((downside/(downside+upside)) which, in this case roughly translates to 0,17/16 = 1%.

The 21.86m own shares Tessenderlo holds following the Picanol transaction will be cancelled in H2:2024; effective overall share count therefore about 62m, for an EV of currently about EUR 1.5bn