Quick updates: Jensen, SFS, Italmobiliare & Bois Sauvage

As promised last week, part 2 of the updates from the very busy week ago. Let’s go.

Jensen Group

Let’s start with an extremely positive one. Jensen Group had a “blowout year” in 2025.

Sales up 19,3%, EPS up +45%. The Dividend will be 1,50 EUR, up 0,50 EUR from the year before. The only not extremely positive number was order intake which was only slightly up. I think it would be foolish to think that Jensen can grow 20% sales every year, but Management sounded quite confident for 2026 as well:

At a trailing PE of 11, the stock is now exactly as cheap (LTM) as when I published the initial analysis in January 2025, despite a 50% plus share price increase.

I have added a little (0,4% of portfolio) to my position at Friday’s price as I think the stock is still way too cheap given the quality. I should have waited until today, but such is life.

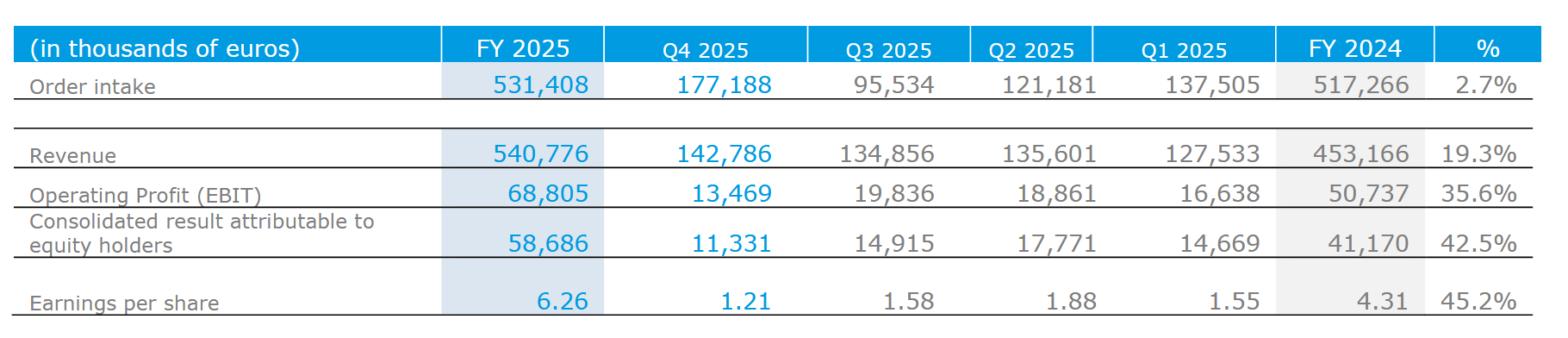

SFS

SFS, the Swiss parts and tools manufacturer/distributor also published preliminary results last week. Given the difficult state of many of its end markets, organic growth of ~3% before FX is quite impressive.

Unfortunately, profit suffered a little more as we can see in this table (before “normalisation”):

To be honest, SFS is quite behind against my expectations from 3 years ago, even factoring in CHF/EUR development.

I think back in 2023, I was too optimistic about manufacturing in Europe which really is struggling:

The stock is now much more expensive despite EPS being lower. So I really need to think about whether I should continue to hold the stock.

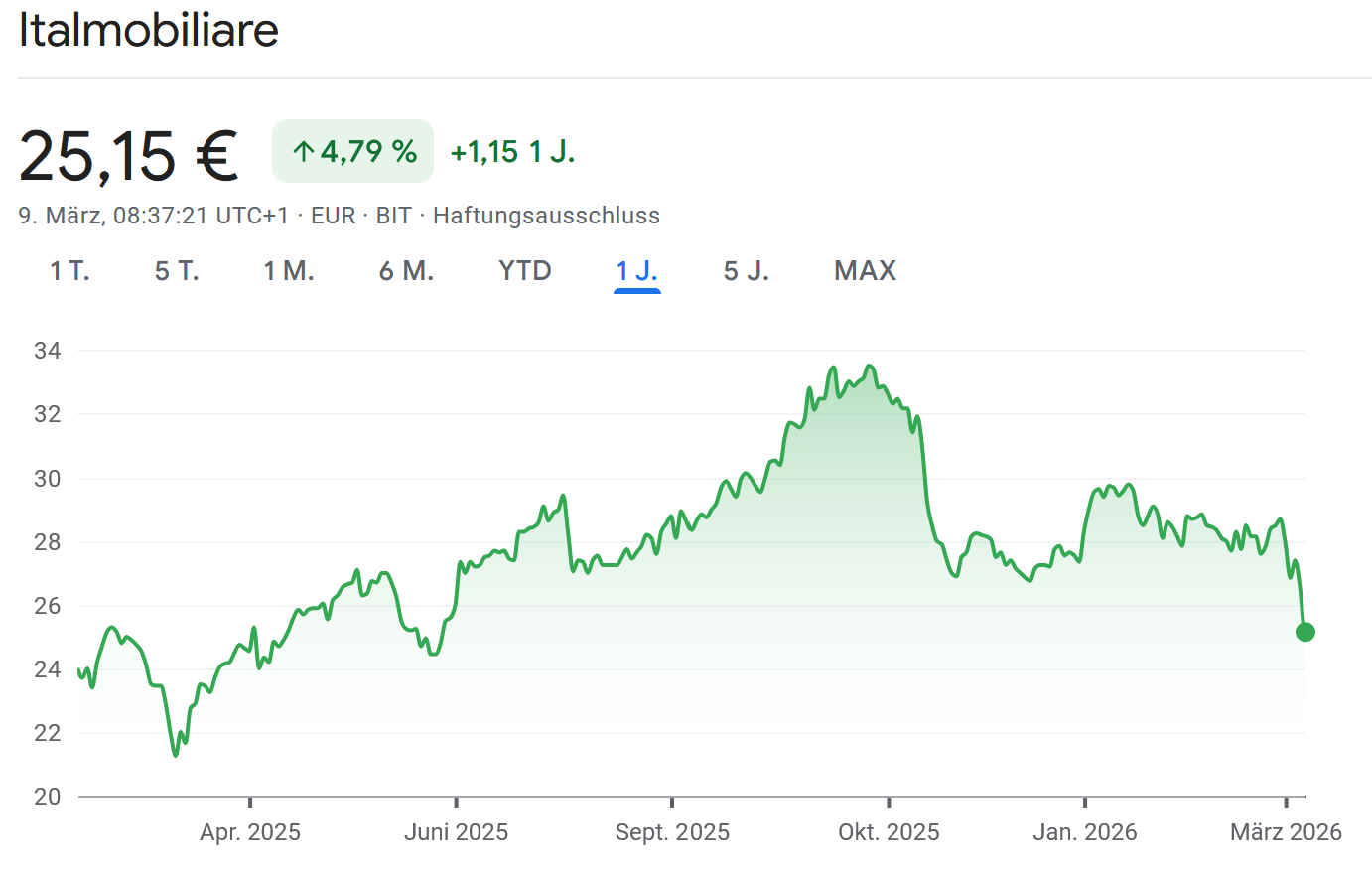

Italmobiliare

Italmobiliare’s preliminary 2025 numbers were a “mixed bag”. NAV increased (incl. dividends) by 6%, but for the two largest stakes, Borbone (Ebitda down because of high Coffee prices) and Santa Maria Novella (only single digit growth), the results were a little bit disappointing.

On the plus side, they managed to acquire an additional 5% stake in Bene and Casa de Salute grows nicely.

The stock reacted quite negatively which lead to an increase in discount to NAV.

At least for Borbone, things should look a lot better in 2026 as Coffee prices have come down again:

It will be interesting to see if SMN can grow double digit again.

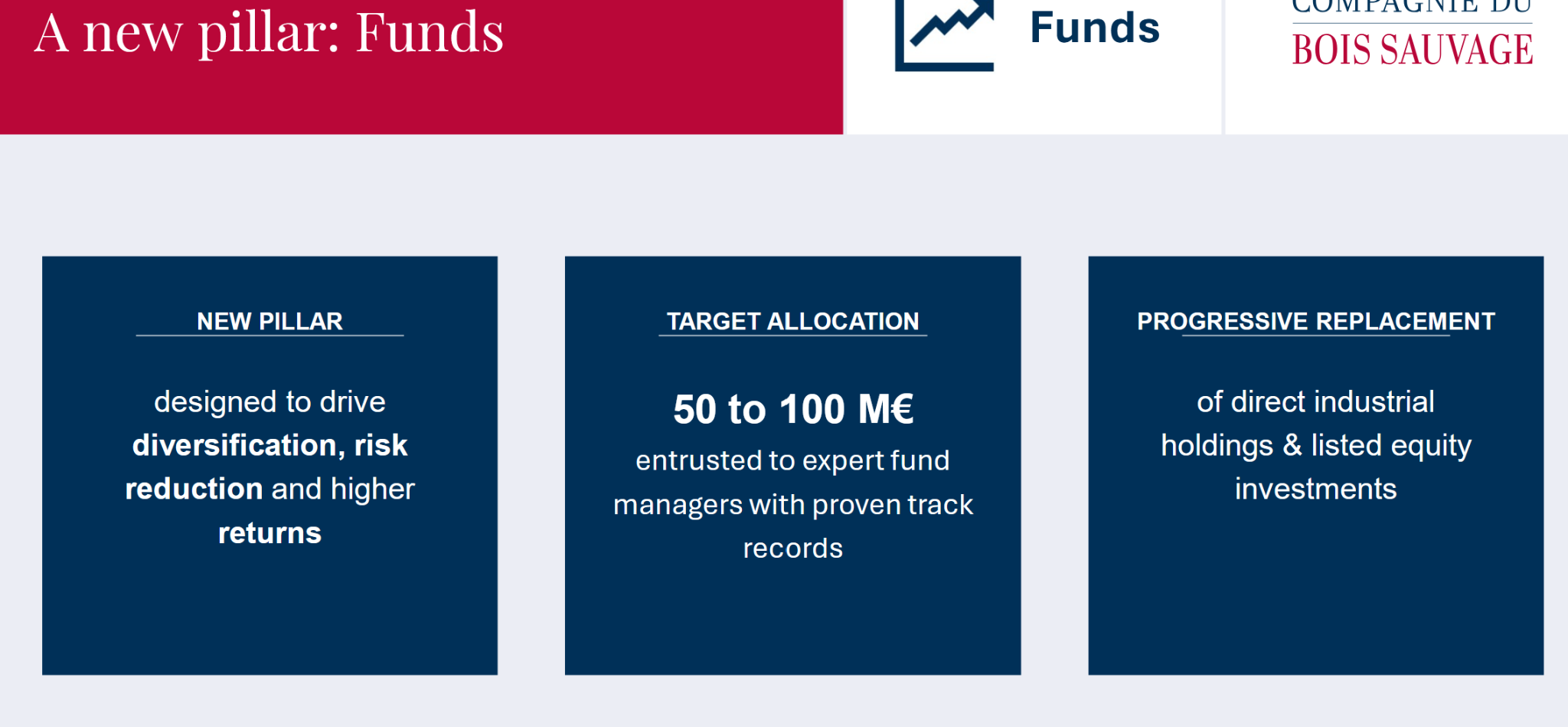

Cie Bois Sauvage

Finally, my “special situation” Cie Bois Sauvage announced preliminary 2025 earnings and the result of their “strategic review”.

On the plus side, the NAV increased by 10% in 2025, mainly driven by the Chocolate business:

Also positive is that they will acquire the remaining 34% of Jeff De Brugges, their second Chocolate Brand.

Less positive was the disappointing development of the Real estate pillar (NAV -10%) and the decision to discontinue industrial participations and invest into PE funds instead:

This is really a downer in my opinion. As much as I like the Chocolate business, I do not understand this “new pillar”. As I mentioned in the initial post, this was meant to be a short term special situation. Therefore I decided to exit the stock at current prices (318 EUR). This was a decent Short term special situation with a 20% plus return in 3 months.