Short Updates: Innoscripta & Nomad Foods

Innoscripta

Innoscripta, a company at which I looked a few days ago, had a few news items over the last few days.

First, they announced that they plan to pay a 4 EUR dividend for 2025 in 2026. At a current share price of ~70 EUR, that’s a dividend yield of 5,7% which is quite substantial.

Then they finally come up with a guidance for 2026 which looks as follows:

Munich, 25. February 2026 – innoscripta SE (ISIN: DE000A40QVM8, the “Company”) expects an increase in revenue and earnings for the 2026 financial year based on current business development and continued high demand.

The Company’s Management Board currently expects the following for the 2026 financial year:

- consolidated revenue of at least EUR 140 million and

- EBIT of at least EUR 80 million

The guidance is based on the current order situation, the scalability of the business model, and stable regulatory conditions.

This guidance represents an expected +36% sales growth for 2026 (vs. + 60% in 2025) and +27% EBIT growth (vs. +70% in 2025). The implied 2026 EBIT margin is 57% against 61%.

Overall, despite the slow down in growth rates, these are still very impressive numbers. The stock trades currently at around 14x 2026 P/E. Still, investors don’t seem to be convinced that this is a good investment.

Maybe the “AI fear” is the driver here. To be honest, I find it very difficult for now, to get the conviction to invest into the currently very negative share price momentum, but I will keep watching and hopefully be able to attend the AGM in Munich in person.

Nomad Foods

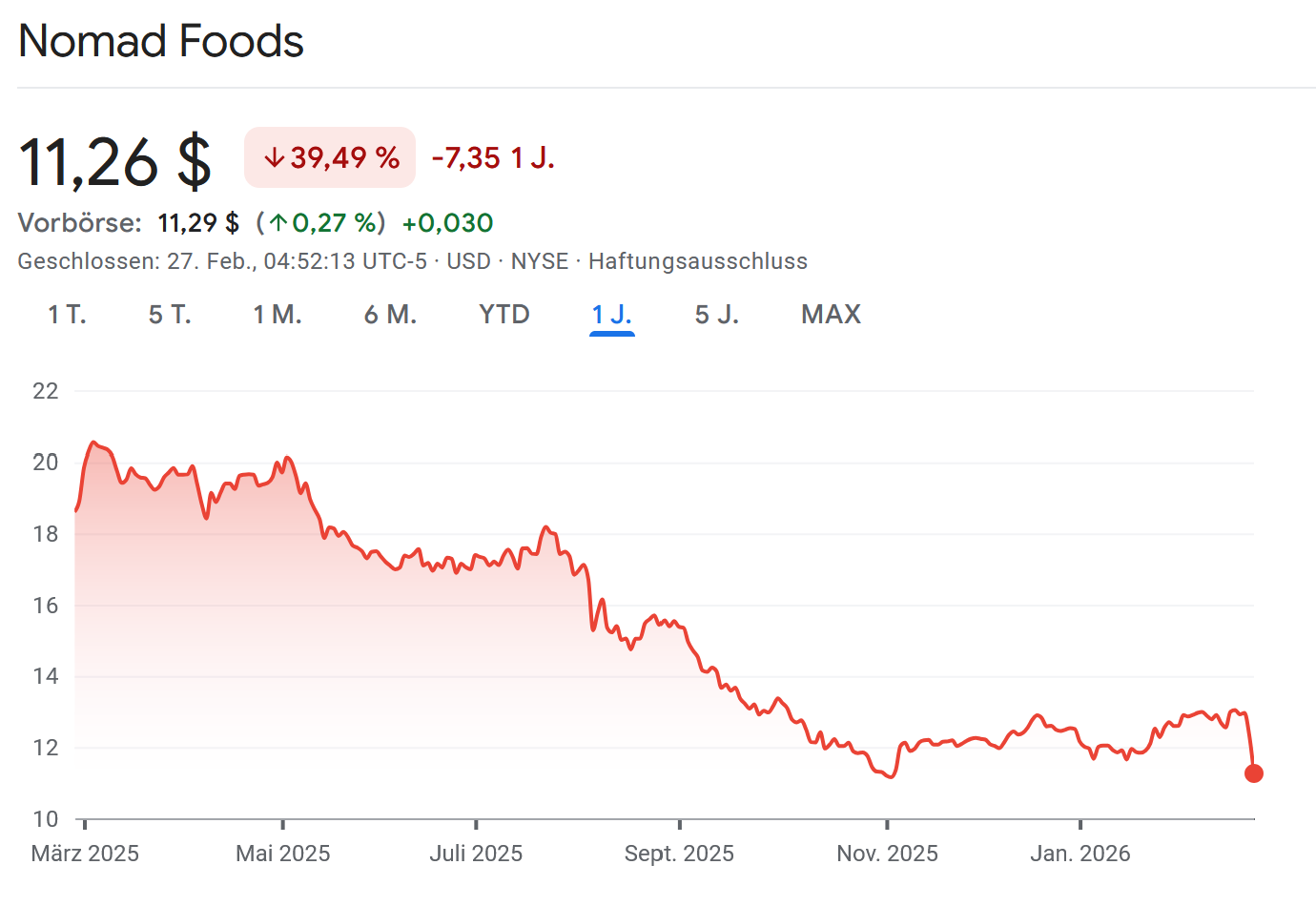

Nomad Foods is the frozen food competitor of Frosta that I mentioned in the Frosta write-up. Nomad released 2025 numbers yesterday.

The picture was not pretty at all. Sales down, margins down, earnings down. Unadjusted they actually made a GAAP loss in Q4.

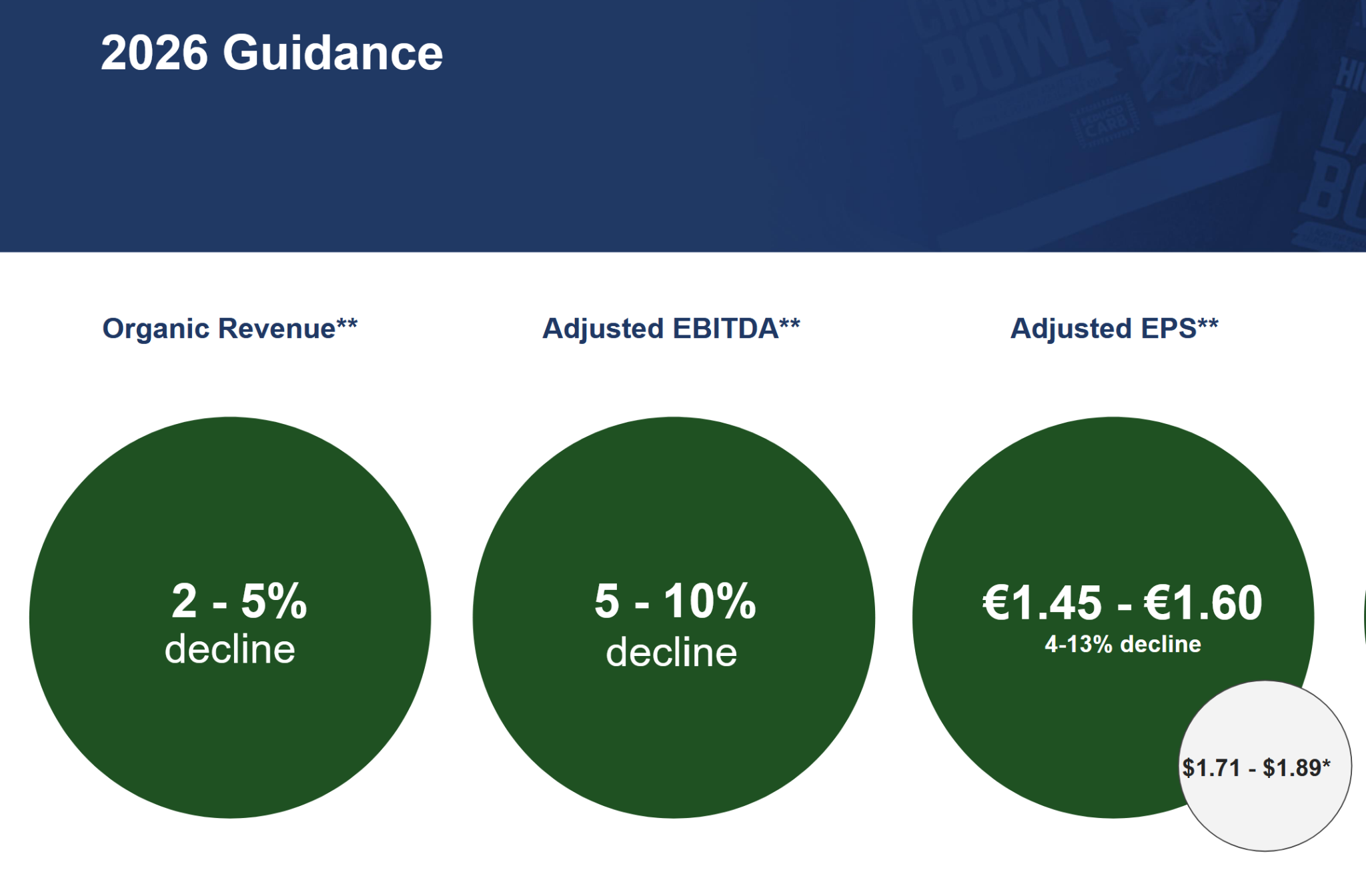

The guidance for 2026 doesn’t look much better either, but rather worse:

If we compare this to Frosta who have increased sales double digits, improved gross margins and only have shown lower net margins because of higher advertising spend, it is pretty clear that Nomad Food and especially the Iglo brand seems to be losing market share.

My gut feeling is that in Nomad’s case, the focus on Cash generation and share buy backs has maybe led to underinvestment into the brand which is not so easy and quick to reverse. Pretty much the same “playbook” and issues like Kraft-Heinz or Anheuser-Busch.

In the consumer space, the safer long term bets are those guys who invest long term into the brand and not the spreadsheet jockeys.

With a further EBITDA decline and current Debt/EBITDA of 3,8x, I am not sure for how long they can continue to pay dividends and buy back shares.

This one looks really vulnerable. For Frosta, there could be a msall risk that if Nomad gets really desperate and needs cash, that they start to dump their products into the market. So I think it makes sense to look at Nomad updates as a Frosta shareholder in any case.

question is: what would have been the result if investing in S&P500 instead (the simplest choice)…. and investing your time helping ur partner cleaning the house…. rather than wasting time writing value destroying blogs & posts…

Why are you wasting time reading my posts then ?