Performance review 2014 – The year in review & Short outlook 2015 & Happy New Year !!!

Performance 2014

In 2014, the portfolio perfomed 5,42% vs. 2,37% for the Benchmark (Eurostoxx50 (25%), Eurostoxx small 200 (25%), DAX (30%),MDAX (20%)). This is the 4th year in a row with an outperformance but such a small difference is rather arbitrary, so nothing to get excited.

If I would need to promote my results for 2014, I would argue that the result has been achieved with significant less volatility than the Benchmark. A quick look at the monthly returns:

| Perf BM | Perf. Portf. | Portf-BM | |

|---|---|---|---|

| Jan 14 | -1,9% | 3,7% | 5,5% |

| Feb 14 | 5,2% | 2,7% | -2,5% |

| Mrz 14 | -0,8% | 0,5% | 1,3% |

| Apr 14 | -0,3% | 1,4% | 1,6% |

| Mai 14 | 3,2% | 0,8% | -2,4% |

| Jun 14 | -1,2% | 0,9% | 2,1% |

| Jul 14 | -4,5% | -2,5% | 1,9% |

| Aug 14 | 1,1% | -0,1% | -1,3% |

| Sep 14 | -0,1% | -2,2% | -2,0% |

| Okt 14 | -1,7% | -0,8% | 0,9% |

| Nov 14 | 5,4% | 1,2% | -4,2% |

| Dez 14 | -1,6% | 0,0% | 1,6% |

| 2014 | 2,5% | 5,4% | 3,0% |

Interestingly, the Benchmark showed 7 months with negative returns vs. only 4 months in the portfolio. The returns are (by design) relatively uncorrelated to the market, although in extreme scenarios I expect correlation to be higher but still significantly lower than 1.

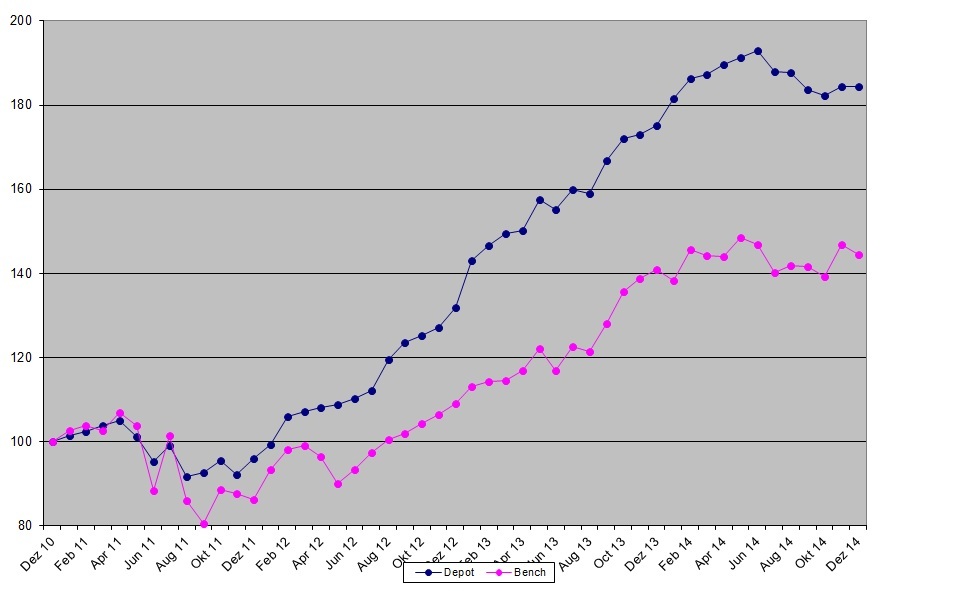

Performance 2010-2014

Over the 4 years the blog portfolio is now in existence, total performance has been 84,5% or ~16,6% p.a. This compares to 44,5% or 9,6% p.a. for the benchmark. Honestly, I didn’t think it was possible to outperform with such a portfolio in an “up market” like this. Graphically it looks like this:

The Top 5 performers in 2014 for the portfolio (including sold positions) were:

1. Koc Holding +61,6%

2. Installux +39,5%

3. Cranswick +23,4%

4. G. Perrier +20,2%

5. Citizen Financial + 15,8%

The 5 biggest losers were:

1. Sberbank -46,5%

2. Sistema -39,5%

3. Trilogiq -32,2%

4. Portugal Telecom -23,8%

5. Bouvet -15,8%

Interesting for me is the fact that 4 of the 5 top losers were new positions whereas only 2 of the 5 best stocks (Koc, Citizens) were bought in 2014. My second try in Russia with Sberbank and Sistema was clearly not a success, although the overall performance of the Emerging Market “expedition” was positive due to higher weightings and positive returns especially of Koc Holding and the TRY Depfa Zerobond

Transactions

New buys:

+ Admiral

+ Ashmore

+ Citizen financial

+ Energiedienst

+ Koc Holding

+ NN Group

+ Depfy TRY Bonds

+ Romgaz

+ Electrica

Sells

– EMAK

– Sol Spa

– SIAS

– Celesio

– April

– Poujoulat

– Vetropack

– Draeger (partial)

In & Out

– Sberbank

– Sistema

– Rhoen

– Flughafen Wien

– Sky Deutschland

– Portugal Telecom

Some Portfolio statistics

The current portfolio can be seen as always under its regular place. A few statistical facts:

Holding period

Around 66% of the portfolio were part of the portfolio in the beginning of 2014. So including the “in and outs), portfolio turnover was maybe around 40% which is pretty OK.

Average Holding period for what I call “core value” stocks is 1,9 years, overall, including “opportunity” investments and Emerging markets, this number is 1,8 years. This is something I would like to see increasing above 2 years, but it is not a “hard criteria”, just something to remind me to slow down trading ….

By country

| % Portf | |

|---|---|

| Germany | 21,1% |

| France | 20,7% |

| UK | 11,3% |

| Netherlands | 10,0% |

| Norway | 6,6% |

| Romania | 5,0% |

| Belgium | 4,2% |

| Turkey | 4,1% |

| US | 2,8% |

| Switzerland | 2,7% |

| Denmark | 2,5% |

| 91,0% |

My primary use for such a country allocation is risk management. As I do bottom up, stock-by-stock research, for me it is important to limit exposure to certain political and economic environments.

The markets in 2014

In 2014, you were basically an idiot if you didn’t own US stocks. In EUR, the S&P 500 made an amazing 28%, the Nasdaq over 30%. On the other hand, even for US stock pickers, it was a hard year to outperform as Josh Brown shows in this post.

Just five stocks—Apple, Berkshire Hathaway, Johnson & Johnson, Microsoft, and Intel— accounted for 20% of the market’s gains. If you weren’t at least equally weighted toward them, you had virtually no shot at making up for missing their enormous, index-driving gains.

For European small cap investors (like me), the year was tough A couple of European markets were deeply negative, such as Austria, Portugal, Greece, Norway. Everything with Oil and Russia got burned heavily which clearly showed in the portfolio.

My home market Germany had a year which is extremely rare: A low single digit positive return for most indices, 2,65% for the DAX 30 index. In the 26 years since the DAX is calculated, only 2 other years showed a positive single digit performance, 2004 (+7,3%) and 1995 (+7,3%). Normally, the DAX goes up and down in two digits percentage points annually despite the well-known fact that long-term equity returns are single digit positive.

For a European investor, “sell in may and go away” would have worked pretty well, my own portfolio had the peak end of June where it was around +4,4% higher than now.

Despite being neutral on interest rates, the further drop in interest rates was a surprise for me. The Bund future showed a 2014 performance of 12%, outperforming the DAX by a wide margin. At a current yield of 0,3%, there is not a lot of room left, unless long rates go negative.

Finally, the -50% drop in oil prices surprised me most. I didn’t see that one coming and I am still not sure what it means to the stock market.

Short Outlook 2015

As I am not a macro guy, I spare myself an my readers some meaningless forecasts with regard to Gold, oil, interest rates and stock index levels.

For me, the current environment is clearly challenging. I still have conceptual issues with negative nominal interest rates (I will need to sort my thoughts on this a little bit more to make a post) and I don’t really understand why oil is doing what it is doing. On the other hand, as I lined out in my oil price post, I am not convinced that the sudden drop in oil is all good for the economy AND the stock market.

I still believe it is important to look at intrinsic value of companies as this determines returns for investors over the long run. As a reminder, the intrinsic value of companies is derived out of the following components:

1. Future earnings (which is a function of current earnings and earnings growth rates)

2. appropriate discounts rates in order to calculate present values

If 2015 interest rates in the US rise, one will have to pay attention if earnings growth can keep up with this. Despite some (in my opinion useless) “historic evidence” that rising interest rates do not harm stock returns, all other things equal, rising interst rates mean lower present values and lower intrinsic values. And long term lower returns for shareholder.

One should also be prepared for more volatility and drawdons which last maybe longer than the ones in 2014 which reversed always extremely fast. Overall, I think it is still worth to play this “defensively”.

Happy New Year !!!

Finally, Happy New Year to everyone. For me, the year started already great with a fantastic day in a “Winter Wonderland” setting in my hometown Munich. Attached three pictures from a walk in the Nymphenburg Park (taken with a crappy Blackberry camera):

Congratulations on your nice Performance.

I also think that the holding periode for core value stocks should be larger than 2 years and opportunity trades get ‘unpredictable’ if the time to closing the deal exceeds 6 months…

So inherently, two very different time scales you try to handle here.

Besides reading on stocks I always enjoyed postings on books or more general things here, so what do you think? How about some discussion how ‘well known value investors’ developed over time, which contibutions they made etc ?

I’m sure you know James Montier (formely DrKW, now GMO) who recently warned that shareholder value is the dumpest idea out there, Download Website here: https://www.gmo.com/America

Maybe a little bit forgotten but still a very nice writeup: 7 sins of Fund (aka Portfolio) Management from the same guy from 2005: http://www.er.ethz.ch/teaching/Seven_Sins_fund_Management.pdf

And in between he wrote ‘the Little Book of behavioral investing’ which you may have read as well.

Just an idea of course…

thanks for your comments. Well, from time to time I write more general stuff, but only if I really have something to say. It is much easier for me to wirte about my stock research….

Nice and relaxed winter photo….

Hi there

Happy new year to you too…

Why don’t you open an investment fund ?

Happy new year to you as well.

Happy to open one if you provide the seed money 😉

The Blogger of “Simple-Value-Investing” recently announced that he won´t continue to analyze stocks publicly on his website. He obviously has founded his private investment firm after having a very successful Investment record. Could be a benchmark for you as well as the US based hedge fund guys tracked on gurufocus.

The question is: How much money do you think is necessary to start with? Maybe you can try a crowd funding approach with your own community and just go for it. I think the quality of your analysis is very very high… So why not?

Other option if you think on monetizing your work: Create a small cap investment news letter such as Fool.com. I I always wonder who is going to fill the gap for a similar service in Europe.

hmm, no there are too many investment newsletter out there already.

I was quite surprised by the “Simple Value” guy,,too. I am not sure if his strategy scales up and how he will do in a real down turn.

Ever thought about your own wikifolio? With a lot of small but trusting “seed investors” you can also collect quite a nice volume as Katjuscha proves.

Main hurdle in my opinion: Shares have to be traded quite frequently at the DAX to be included to the tradable list. I fear that is not the case for many of your shares…

It is interesting: Even if I got a better performance than you the second year in a row I see you as the much much better value investor! Your value analyses investments are the best I know, they set standards.

I I would give any advise: Think about adding a technical check as a second step, if you already like a company at its actual share price. I think it could have saved your some bad timings.

Hi Roger,

I don’t like Wikifolio for 3 reasons:

– limited investment universe

– no control over trading / money in- and outflows

– costs are too high for investors

Thenaks for the advice and congratulation for your performance. Yes, investing against momentum is maybe not such a good idea but over th elong run this cancels out.

mmi

#Marcheso,

as a bottom up investor, I do not target a particular cash level, this comes more naturally if a sell expensive shares and have problems to find attractive ones.

Re USD: No, I would not want to speculate on the USD/EUR rate. I know that I have no edge in FX.

mmi

Great work and congratulations! Since I have the same “gut feeling” that volatility will rise and draw downs might take longer to compensate than this year one question: What are your thoughts on rising cash levels in the portfolios und exchanging some Euros into Dollars?