Fondul Proprietatea (ISIN US34460G1067) – Where discounted Romanian stocks meet Paul Singer & Mark Mobius

Background:

Fondul Proprietaeta is a Romanian based closed end fund which was set up in 2005 to compensate victims of communism by granting them shares in the fund which in term held most of Romania’s state-owned stakes in Romanian companies.

![]()

The fund has been traded on the Romanian stock exchange since 2011 and now finally starting April 29th, the fund is also traded via GDRs on the London Stock Exchange.

I have mentioned the fund a couple of times on the blog already as it is both, a shareholder in Romgaz as well as a 22% minority holder of the operating subsidiaries of Electrica.

What is in there ?

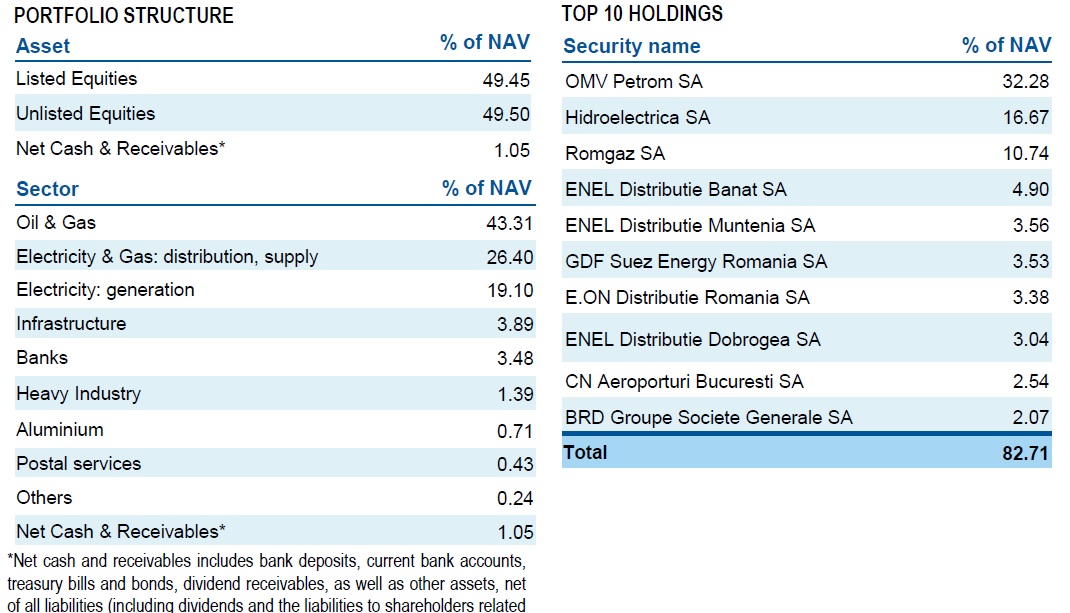

Luckily, the fund has “Top notch” reporting. On the website one finds monthly fact sheets and the top 10 positions. The full list is published Quarterly, under this link you’ll find a handy Excel spreadsheet. Those are the Top 10 positions from End of April and the portfolio composition:

1. The portfolio is heavily tilted towards Energy

2. There are also a lot of unlisted participations in the fund. Overall the percentage of unlisted companies is 50%.

There is a very recent and good presentation available on Fondul homepage.

Templeton / Mark Mobius

Before moving into more investment detail’s, lets look at some specialities of the fund. On of the special features of this fund is the interesting fact that Templeton is managing it as a sole investment manager. If you look into the annual report one actually sees a picture of this guy who actually signed the annual report:

Again, this is not Dr. Evil but Mark Mobius, boss of Templeton. Templeton won a contest in 2010 to run the fund which was then not even listed.

Templeton gets 60 bps per annum which is slightly less what they normally charge for their funds. Templeton seems to be quite active in managing the portfolio,especially in pushing the Government to list more of the unlisted companies such as the Bucharest Airport and the port of Costanza which could turn out good investments. As we know from Electrica, they are not always succesful but honestly they are much more trustworthy than any Government related agency.

Paul Singer & Elliott

To make things even more interesting, famous activist investor Paul Singer owns around 20% of the fund, having increased his stake as late as April this year. If I understand correctly, he was also one of the driving forces behind the London listing.

Interestingly, and I assume this is also due to Singer’s influence, Templeton has actually a formal target to narrow the discount vs. NAV to a value of 15%. For Singer this is a major position. So far his activities have been quite beneficial for all holders as the NAV discount has clearly narrowed. In my personal experience however one has to be carefull when one invests “along” Singer/Elliott. More often than not they will try to get special deals which only benefit them and not the shareholders. So far this hasn’t happened here to my knowledge but one should keep that in mind.

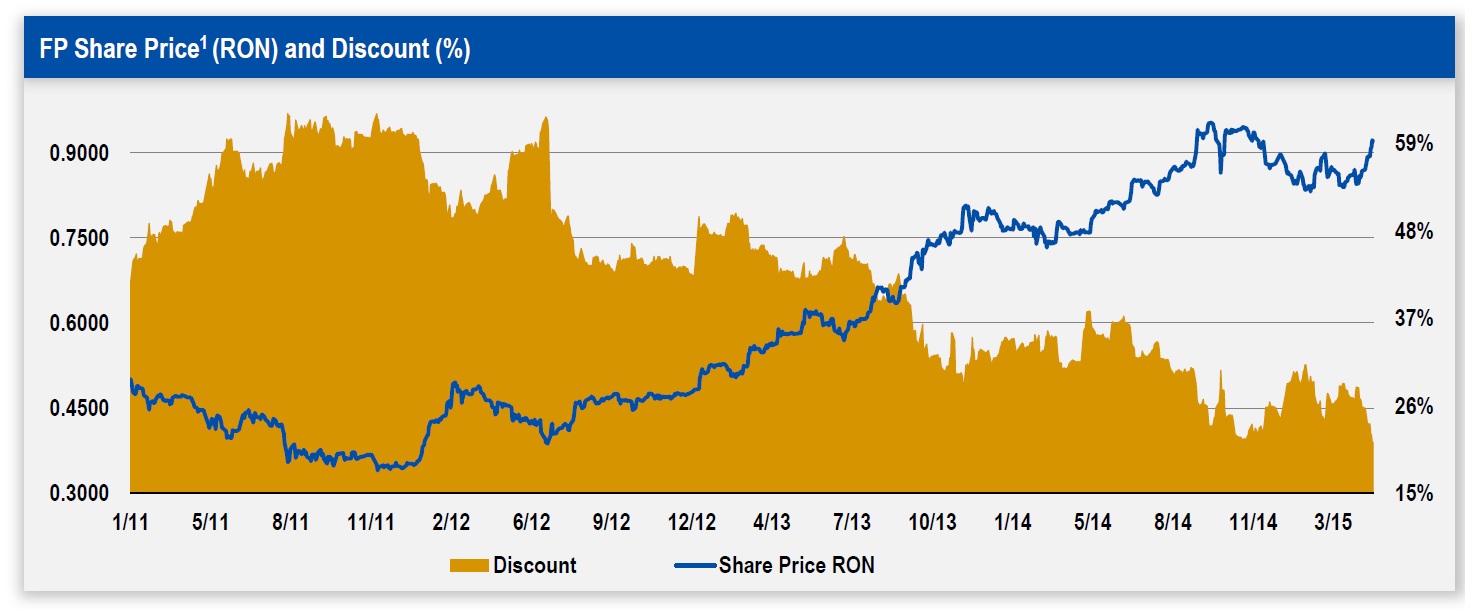

“Discount” to NAV & Valuation

As of April, the discount to the NAV was around 25%. Historically, the discount has been much higher:

One critical issue with regard to the “discount” is of course the fact that for the unlisted shares the verification is quite difficult. Readers of my blog and myself of course do have a small informational advantage. In my last post on Electrica, I had quoted the following about the negotiations between Electrica and Fondul:

Fondul Proprietatea holds stakes of about 22% in each of these companies, which are valued at EUR 173 million in its portfolio. Electrica, which is 49% controlled by the state, was looking to pay a price closer to EUR 100 million, according to sources familiar with the negotiations.

According to Fondul’s annual report, the value unlisted companies in the following way:

Illiquid or unlisted securities are valued using either the value of shareholders’ equity, as per the latest available annual financial statements, proportionally with the stake held, or according to international valuation standards which permit fair valuation.

One could say OK, valuing at book value is even conservative. But if we look at Electrica itself, which is currently valued at around 0,72 x Book, one could argue that valuing 22% minority stakes in subsidiaries at book is optimistic based on current market values. In Electrica’s case I would argue that the intrinsic value is a lot higher but still, market values are market values. So for the time being, I would adjust all the minority stakes of the electricity distribution companies at least by 25% to reflect current market valuations.

The big “unknown” however in the portfolio is Hydroelectrica. With around 17% of the portfolio, it is the second largest position after OMV Petrom. The interesting fact is that currently the company is still insolvent at the time of writing. According to Fonduls annual report however, the company is now profitable again and the most likely candidate for the next privatization. In any case, the actual value of this stake does have some uncertainty as well. As most of the big Romanian energy shares trade below book value (Transelectrica at 0,8, Electrica at 0,7 etc., I would also discount this position by 25%.

So a very simplified valuation with a 25% discount on all unlisted shares and values as reported for the rest would give an NAV (based on April 30th) of:

Listed + Cash 6.641

Unlisted 4.858 (6.477*0,75)

– liabilities – 43

_____________________

Total 11.456

Divided by 12.200 mn shares we would get an “adjusted NAV” of around 0,94 RON against a price of 0,90 RON end of April with a resulting discount of around 4,2%. Still a discount but clearly lower as the “official” discount.

Summary:

+ short-term catalysts (Sale of OMV Petrom, IPO of Hydroelctrica)

+ active management including share buy backs

+ underlying assets are also in principle attractive

+ Romanian economy on a growth path

– relatively low discount with conservative adjustments

– “oil price risk”

– be careful when investing alongside Singer/Elliott

All in all it is an interesting position but not a “must buy” for me at the moment. What could change my perception ? I guess mostly a strong drop of OMV-Petrom which will most likely directly feed through into the fund price and/or a succesful float of Hidroelectrica.

Great write-up. Are you sure you are using the right share count? They are buying back shares quite actively. From their latest NAV report (http://www.fondulproprietatea.ro/sites/default/files/van_report_30_apr_2015_0.pdf) I get 10.278m shares (excluding treasury shares). Keeping your adjustments I get an adjusted NAV of 1.07 RON which would mean almost 17% discount or 20% upside to NAV. I don’t know if I am missing something.

I am not sure to be honest. I guess it depends if the “official”NAV does include the Treasury shares or not or if they are already canceled out. I need to look that up again. Anyway, even at this discount I would most likely be not a buyer.

Hey,

The NAV does not include treasury shares, as all of them will be cancelled. It should be around 1.2 RON / share minus all the adjustments you want to make for specific holdings.

About Hidroelectrica: that is a very special situation. The company was always profitable and was forced into the insolvency process in order to get rid of some contracts signed by some previous managers (these contracts were worth about 1 bil EUR / year). The new management is not influenced by political parties, but that might change at any time (hopefully it won’t).

In FP’s portfolio at the end of Q1 2015, it was valued at 10 bil RON (~2.25 bln EUR) with a net profit of around 0.27 bln EUR for 2014. Given the current valuations and Hidro’s position in the Romanian economy, probably the holding can be worth more IF the company keeps the current management.

Finally, regarding Templeton and Paul Singer: let’s just say those guys have done almost nothing good for FP. Given the assets they had, the performance was lackluster at best.

Everyone was thrilled to have Romania’s largest investment fund managed by a prestigious company such as Franklin Templeton, but their lack of investment ideas and ethics (fighting with the media, arguing with shareholders at GSM, using ABBs to sell shares instead of public offers) proved that the local FT people are mediocre by our standards (and we have low standards, as most of our asset managers are probably not as good as those in developed economies).

And to put some facts behind my statements: Templeton sold a LOT of valuable companies (eg: Romgaz) at a significant discount just to get cash in order to buy-back overvalued shared because Singer said so. He wanted to cash out immediately, so FT just sold whatever they could to get the resources for the buy-backs (guess who benefited from those most).

They had a lot of money and valuable assets to work with and they made almost no investments except one in Erste Bank that generated a decent loss. Shareholders could have paid an individual a fraction of what they paid Templeton and he could have done the same thing: selling Romgaz at a 10% discount to private buyers (via ABB) and buying back shares at 1 RON/share doesn’t really require any experience or financial expertise.

You pointed out really well that partnering with Singer does not mean that you’ll get anything, as he will do anything to make a profit, even at the expense of other shareholders’ money.

I think the conclusion is right: FP will probably be a decent investment, but there are (in my opinion) way better companies out there. If you want to invest in Romanian investment funds, a deep discount is needed to compensate for the management’s lack of vision and ethics (it’s true for other companies, not just FP, but we hoped FP will be different thanks to Templeton).

Lucian,

again thank you for your extremely valuable comments. I agree with everything.

mmi

Why do you think Romgaz sold at an undervalued price? The total return since IPO has been 4%, so doesn’t seem like they sold at that much of a discount!

Fondul actually has had a better return since Nov. 2013 — so not a bad way to invest funds in buybacks.

Btw –Lucian, you are clearly very familiar with the Romanian market. I have come to conclusion Electrica standalone appears to be better risk-reward than Fondul at this stage, but I am having hard time finding companies in Romania with r-r as good as Electrica. Would like to hear your take on that.

@Valuedude – please note that FP sold Romgaz in june 2014, at a discount to the market price (5% of Romgaz was sold at 33.5 RON / share, about a 5% discount from the market price of that day).

Yes, FP’s performance was slightly better for the past year, but I think you have to look at it in terms of discounted cash flow: which of the two has a higher expected value in the future. Most analyses I’ve seen consider Romgaz as a way better investment than FP, so it’s either that Templeton were able to foresee the short term market fluctuations or they thought all external models used to value Romgaz were missing something.

But in order to better assess the quality of Templeton’s management, I think we should look at the choices they made overall and not focus on this single one:

1) In november 2014 they sold Conpet (COTE) at 48.75 RON/share

– a 10%! discount to the market price (pretty large by any standards).

– total offer value: 100 mln RON (~23 mln EUR)

– they used the cash to buy back shares that are now worth exactly the same as in november

– meanwhile COTE is now trading at 71.7 RON / share

– so they “lost” 46 mil RON just from this transaction (~10 mil EUR)

2) In may 2013 they sold Petrom (SNP) at 0.39 RON / share

– a 12% discount to the market price the day before the announcement and 6% discount to the market price of the announcement date

– total offer value: 246 mln RON (~57 mln EUR)

– they used the cash to buy back share that are worth about 10% more now

– SNP went to about 0.48 RON/share the year after they sold. It’s now back to 0.38, but this is only because of the unexpected drop in oil prices, which I assume they didn’t foresee back then.

– Not sure how to look at this transaction, but let’s call it a successful deal – about 5 mln EUR (I’m biased, but I’d say it was just pure luck given the other choices they made)

3) In july 2014 they sold Transelectrica (TEL) at 21.5 RON / share

– a more than 10% discount if I recall correctly (don’t have this particular information now)

– total offer value: 212 mln RON (~48 mln EUR)

– again, cash used to buy back shares that did not go up at all

– TEL is now trading at 29 RON / share

– They “lost” 74 mln from this decision (~16 mln EUR)

4) In december 2013 they sold Transgaz (TGN) at 172 RON / share

– a “mere” 5% discount to the market price

– total offer value: 303 mln RON (~70 mln EUR)

– the shares they bought back are now worth about 10% more

– TGN is now trading at 275 RON / share and they also distributed dividends worth 22 RON/share meanwhile (297 RON / share overall)

– They “lost” 220 mil RON from this (~50 mln EUR)

5) The only large investment they ever made: buying Austrian bank shares in 2013

– The shares were bought in 2011 (Raiffeisen and Erste) for about 280 mln RON (~63 mln EUR)

– Estimated acquisition price: 35 EUR/share for Erste and 39 EUR/share for Raiffeisen

– The shares were sold in april 2014

– They had an 82 mln RON loss on this investment (18 mln EUR)

I’m not cherry picking here, these are all the large decisions they made for the past two years (or at least the ones I found). I’d also like to add their tender to buy back shares of FP at 1 RON/share when they were trading in the market at ~0.8 RON/share – which sane manager would do something like this?.

The point I’m trying to make (in a very verbose way 🙂 ) – the management did not live up to their reputation and the choices they made were rather poor. What everyone expected was for them to find new investment ideas and impress us with the long-term performance. They did exactly the opposite: focused solely on the short term and only divested, while at the same time losing a lot (percentage-wise) from their only major investment.

Fondul Proprietatea was a failed experiment for the Romanian economy and it wasn’t entirely Templeton’s fault. I’d even go as far as to say they were the only ones that had a somewhat positive impact on the company, but overall the Romanian State and Singer had their way and turned what could have been a major regional investment fund into an accelerated divesting fund that bleeds assets.

Regarding other companies in Romania:

– Agreed with Electrica. I don’t know too much about the company, but from what I’ve seen they have have the potential to be a good investment if they state doesn’t mess with the regulated prices too much.

– Are you interested in Romanian companies listed on the London Stock Exchange or any company listed on our local stock exhcange (BSE/BVB)?

A few things to add to my previous post:

1) Romgaz had an IPO price of 30 RON/share, and distributed dividends worth 2.57 RON/share in 2014. It is now trading at 36.24 RON/share, so the absolute return for the company was ~30% in the 1.5 years since the IPO.

2) There are a few typos in my earlier comments, apologies for those.

The most important one is in the last paragraph, regarding Electrica: it should read “the State doesn’t mess”

3) Templeton did have a positive influence on some local companies, so it’s not all gloomy: they helped uncover the issues with Hidroelectrica’s previous management and contracts and opposed different appointments made by the state at a few key companies. I still think their performance is rather poor, but they certainly had some good moments.

British Empire, an excellent closed-end fund specialised in investing in holding companies at a discount to NAV, is also a shareholder: they got in last fall (http://www.british-empire.co.uk/content/uploads/2014/12/british_empire_2014_oct.pdf) and recently converted the holding into the GDrs.