Koc Holding & few thoughts on Turkey

Koc Holding

On Monday, Koc Holding released 2015 results. As always, they have a very decent presentation which nicely summarizes what happened.

Consolidated net income went up +32% in 2015 in local currency. Even including the 2015 depreciation of around -12%, for me as EUR based shareholders, profits increased significantly.

Based on 2015, Koc now trades at around 8,5 times P/E. The discount to a “sum of part” calculation is around 20%, a value which has been relatively stable over the last 2-3 years.

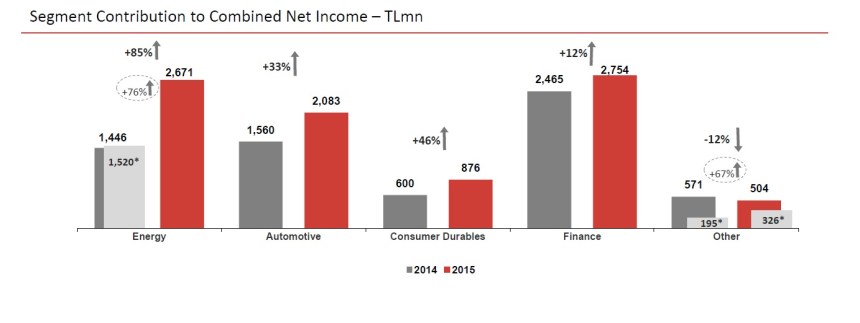

Looking more deeply into Koc numbers, we can see that the energy segment was clearly the driver of the profit increase:

This is not a surprise. The biggest part of the energy segment is Tupras and mangement already communicated a year ago that profits will go up:

Management made a point that the largest subsidiary, oil refiner Tupras is expected to increase earnings significantly in 2015 as a 3 bn USD investment program will be finished and the refinery then will run on full capacity. Although Tupras had losses on inventory, Koc stresses that margins are independent of oil prices.

So it is also not a surprise that the stock held up well in 2016 so far and is up 7,7% in local currency (va. -0,4% for the ISE) and +3,2% in EUR.

What surprised me was the fact that despite automobile production being up more than +20%, exports went down. So a lot of cars were sold within Turkey in 2015.

One the negative side was clearly the surprising death of 55 old year Mustafa Koc, the head of the family. I do not know any details about succession but his two younger brothers were also working at holding level and I guess one of them might take over, maybe the one who was responsible for the energy unit.

Turkey & Turkish Lira

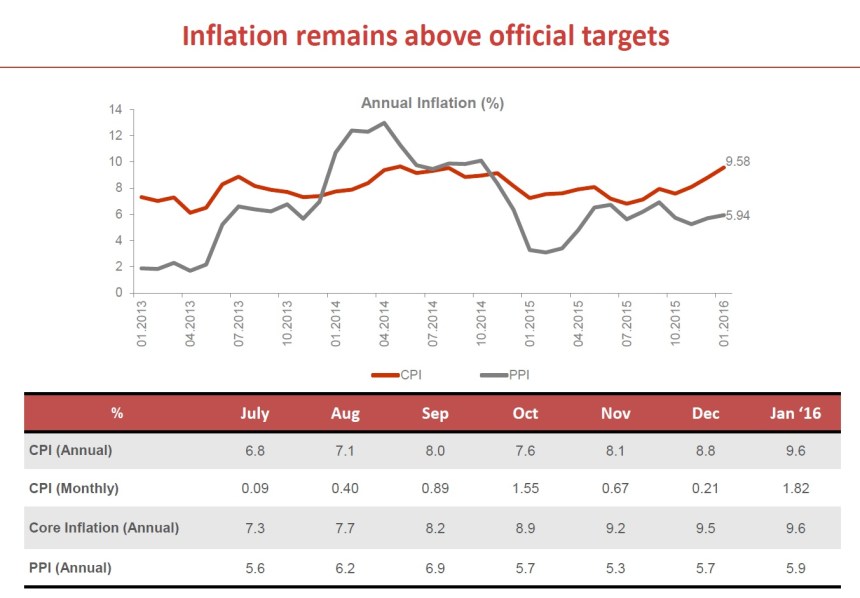

Another slide in the Koc presentation was very interesting:

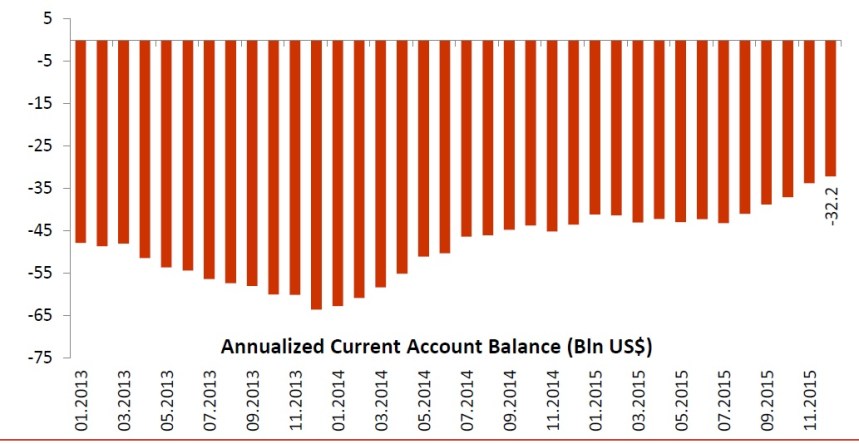

Inflation is clearly heating up which I find very surprising. Turkey is a large net importer of oil and natural resources. The lower prices lead to a still negative but clearly improved current account balance for Turkey in 2015:

When I initially bought the Depfa TRY Zero bond in 2014 I identified 3 risk factors for the bond as follows:

As an investor you can gain (or loose) money with this bond based on 3 risk faktors:

A) TRY/EUR exchange rate. Based on the current interest rate differential, the market assumes that the TRY will devalue vy ~8% p.a. against the EUR.Perosnally, I see a good chance that the devaluation could be less than that. Under many metrics (PPP, BigMac index etc.) the TRY is fundamentally cheap compared to EUR and USD although there is clearly political and econimical riskimplied. The currency factor is clearly no “free lunch”.

B) Turkish interest rates. As a zerobond, the bond has a duration of ~6,5 years, i.e. if interest rates go up or down 1% the bond price will move +/-6,5%. Currently the yield curve in Turkey is flat or even inverse, with the short end slightly higher. even if long term rates stay constantand only short terms go down, one can expect some “extra juice” from the potential roll down of the bond.

C) Depfa Spread. Compared to an EIB Bond, the implicit credit spread is around 3-4% p.a. although in my eyes the credit risk is similar to an IB or german Government bond. I think there is also a good chance that this could normalize over 2-3 years. If there is some rating action following the transfer, this could even happen quicker.

When I look at the 3 points, I think the first 2 are at risk. With Turkish inflation running at close to 10%, the devalutation risk is clearly higher. Plus there is a risk that interest rates could actually increase which would be the normal course of action if inflation increases and negatively impact the price of the bond.

But obviously Mr. Erdogan is not a fan of interest rate increases and the Central bank is not acting:

“The longer Turkey’s central bank refrains from raising rates, the stronger the perception that its hand is being forced by Mr Erdogan’s economics team and the greater the strain on Turkish assets at a time when sentiment towards emerging markets is particularly bleak,” Spiro said.

Although I don’t think that this is a problem for Koc, I do think this could be a huge problem as a TRY bond holder. It clearly shows that Turkey is not that interested in a stable Lira which can easily wipe out any gains on the bond for the foreseeable future.

Koc, on the other hand has “real assets” and they seem to be in the position to increase prices accordingly and maybe even benefit from a weak curreny.

Another clear lesson for me is that any kind of macro and/or currency speculation is clearly difficult. As the name says, it is a speculation and not an investment and maybe not really in my circle of competence.

Consequences: TRY bond “on watch”

As a consequence, I will put the Depfa TRY bond “On watch” for a potential sale. If inflation increase further and the Central bank remains inactive, then I will exit the position. As an institutional investor I could maybe hedge out the Lira and “harvest” the spread, as a private investor however, it is not that easy.

With regard to Koc, I will keep the position for the time being.

Sold my Koc Holding shares today. No Turkey exposure left.

You sold and bought more frequently lately. Sticking to slow investing still?

Good observation. You could see it as a kind of “spring cleaning”. I am now down at 24 stocks which is within my “comfort zone”….

I think it is a good Idea to use a hard “Shopping restriction” like “not more than X new stocks per month/3 months”.

But I dont see the point in taking a hard “selling restriction”. If there is fire under the roof in several companies, you shouldn’t limit your actions to only one company per defined time.

So I think it is good that MMIs takes more selling actions now, as several fires now appear to happen.

I agree to some extend. However, I understand mmi’s rule as a way to prevent dealing with buying/selling decisions in an overly emotional way. Unless situation materially changed from the underlying thesis at several stocks at the same time there is no reason to act on all of them. Assuming a structured process at buying stocks the larger mistakes are often made selling them.

well, selling winners too early was clearly my biggest mistakes. However, not every stock I sold became a winner….

Sold my Depfa TRY Zerobond at 50,50%. and EUR/TRY 3,22 with a loss of -6,0%. I am not comfortable with the FX risk anymore. As an instittutional I could hedge, as a private investor I can’t.

Good uestion. I think a position in a high volatility, high interest currency like TRY or BRL is clearly speculation. A position in USD or GBP could be diversification. If you actually plan to spend money in USD in the future, a USD position would actually be a hedge.

Do you think it is speculation if you do not hold all your fixed income in your base currency or could it also be diversification? For me the speculation angle depends on the concentration of the position.